aware3.com | Kansas City, MO | REMOTE, Onsite | Full-time

We help non-profits (churches, schools, etc) connect with their communities via technology. Currently still a small team, but we must be doing something right, because we’re growing.

Have you ever wondered what exactly is on your corporate credit report? For instance, what is it telling lenders about your business? How are lenders using the information in their decision-making process? Are they simply taking the information at face value? Do they have their own formulas and algorithms that they apply? Your corporate credit … Continue reading Real Corporate Credit Report Review

In 2010, Google made 516 algorithm changes. That number increased to 1,653 in 2016 and to 3,234 in 2018. We don’t have data for the last couple of years, but still, you can bet that the number is continually going up.

With over 9 algorithm changes a day, it’s safe to say that it is no longer easy to manipulate or game Google.

So, is SEO dead?

Well, let’s look at the data and from there I’ll show you

what you should do.

Is SEO dead?

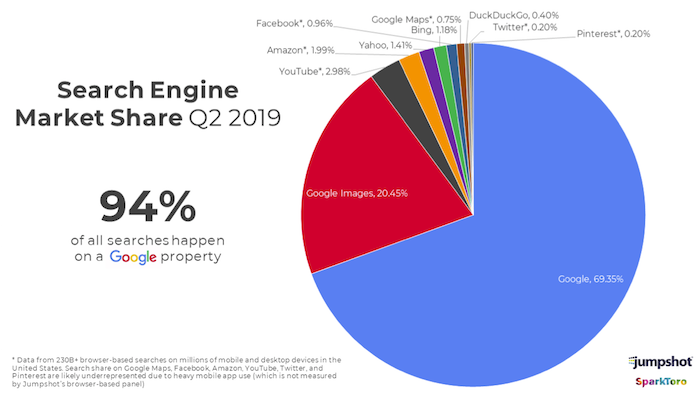

Do you know how many searches take place on Google each day?

There are so many blogs that you can find an excessive amount of content on most topics out there.

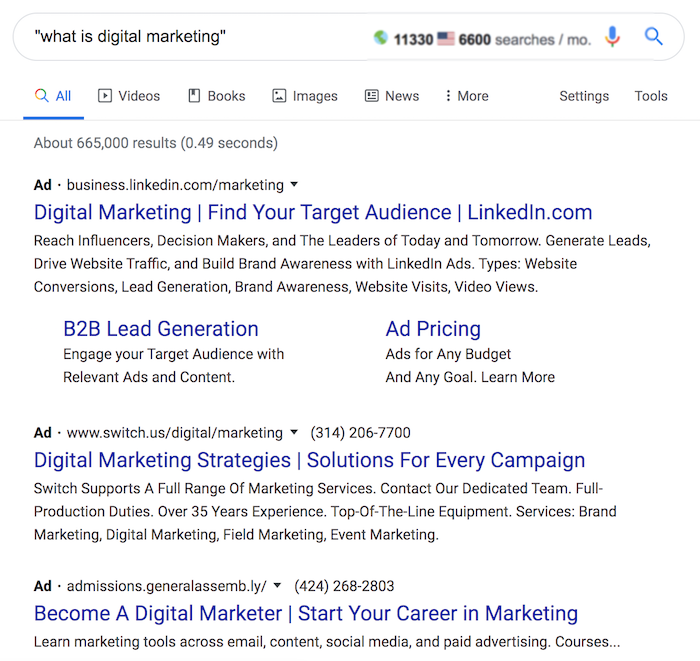

For example, if you look at the long-tail phrase, “what is digital marketing”, there are only 11,300 global searches a month but a whopping 665,000 pieces of content trying to answer that question.

In other words, the supply is much greater than the demand.

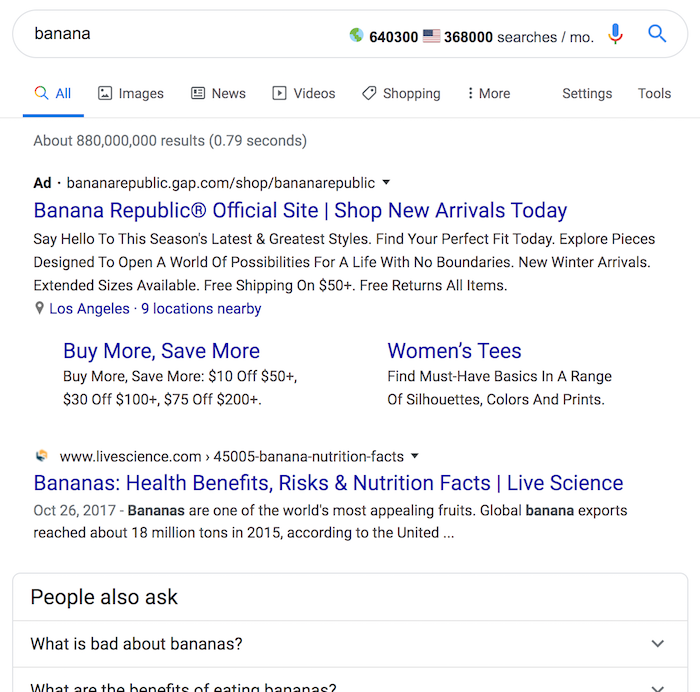

You’ll see even more of this for head terms. Just look at

the phrase “banana”:

640,300 global searches seem like a high number but there are 880,000,000 million results. Sure, some of those results may not be on the food, banana, but still, that’s a lot of content compared to the search volume.

You can still find search phrases where there is more search volume than content but the trend is continually increasing in which content production is exceeding search demand.

On top of that, Google is turning into an answer engine in which they are answering people’s questions without them having to go to a website.

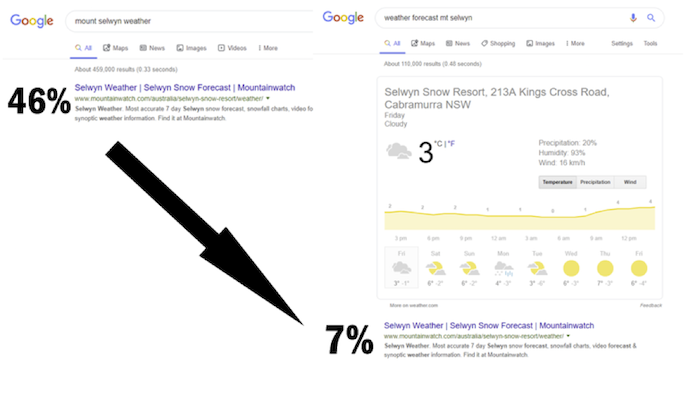

According to Dejan SEO,

they saw CTRs drastically decrease once Google started answering questions.

Just look at this weather search query:

Their clicks from weather-related queries went from 46% all the way down to 7%.

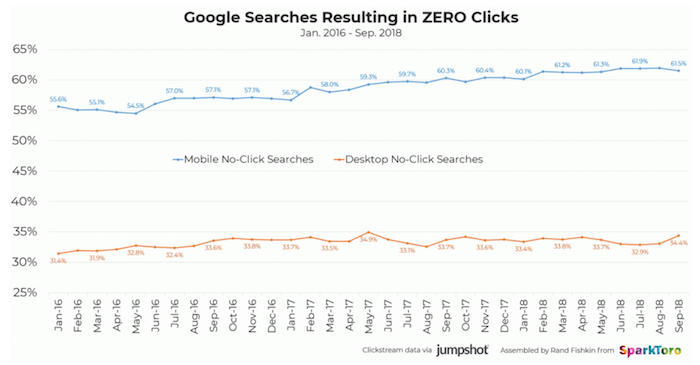

This trend has become so common that the percentage of traffic that Google drives to organic listings (SEO results) has been decreasing over time.

So, does this mean SEO is dead?

It’s actually the opposite.

SEO is not dead

With all of the data, how can that be the case?

First off, all marketing channels become statured over time. It’s just a question of when.

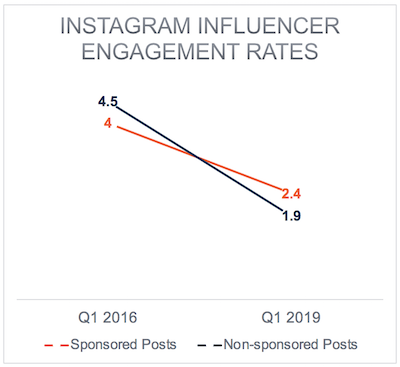

You can say the same thing about Facebook, Instagram,

Twitter, and even email marketing.

Heck, just look at the image below. It was the first banner ad on the Internet.

Can you guess what company created that banner ad? It was

ATT.

Of the people who saw it, 44% of them clicked on it. Now banner ads generate an average click-through rate of 0.5%.

The numbers are on the rise because companies are generating

an ROI.

So, how is SEO still not dead?

As I explained above, just because the metrics aren’t going in your favor doesn’t mean that a channel is dead.

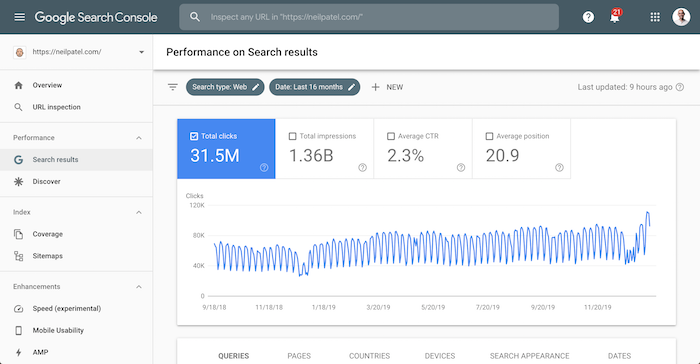

Just look at my search traffic on NeilPatel.com.

Not only do I have to deal with Google’s algorithm like you, but my competition includes other marketers who know what I know… yet I am still able to grow my search traffic even with Google’s decreasing CTRs.

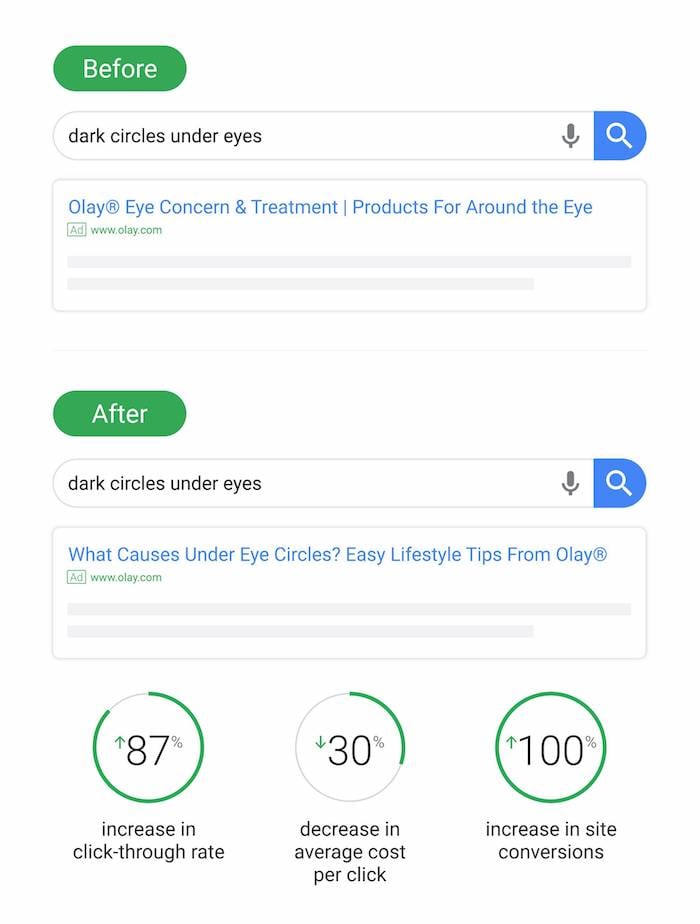

Olay sells products related to skincare. One of their products happens to reduce darkness under your eyes.

So, they used to push heavily on ads that sold their

products directly.

But the moment they changed their ads to focus on education by teaching people how to reduce dark circles under their eyes instead of forcing people to buy their products, their ROI went through the roof.

By sending people to educational-based content first (and then selling through the content), they were able to increase click-throughs by 87%, decrease their cost per click by 30%, and increase conversions by 100%.

This is a prime example of how more people are using Google as a discovery engine first instead of a commerce engine.

SEO isn’t dying it is just changing

Now that you know that Google is shifting to a discovery

engine (for both paid and organic listings), there are a few other things you

need to know if you want to dominate the organic listings.

1: Google wants to rank sites you want to see

Their algorithm core focus isn’t backlinks or keyword density, or a specific SEO metric… the focus is on the user experience.

If a site has millions of backlinks but users hate it, the site won’t rank well in the long run.

Even if you hate the social web, you need to use it more. Not only can it help with your site’s indexing but it can also help with brand building, which indirectly will help boost your rankings as well.

Here are some articles to follow to help boost your social

media presence:

As your brand grows, you’ll find that your rankings will climb as well.

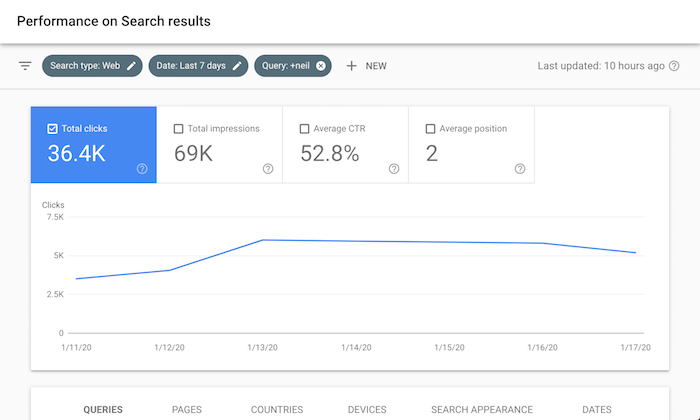

You saw my search traffic stats earlier in the post, but

here’s a breakdown of how many people found my site by searching for my name in

the last 7 days.

And that number doesn’t even include the misspellings. You would be shocked at how many people spell my name as “niel” instead of “neil.”

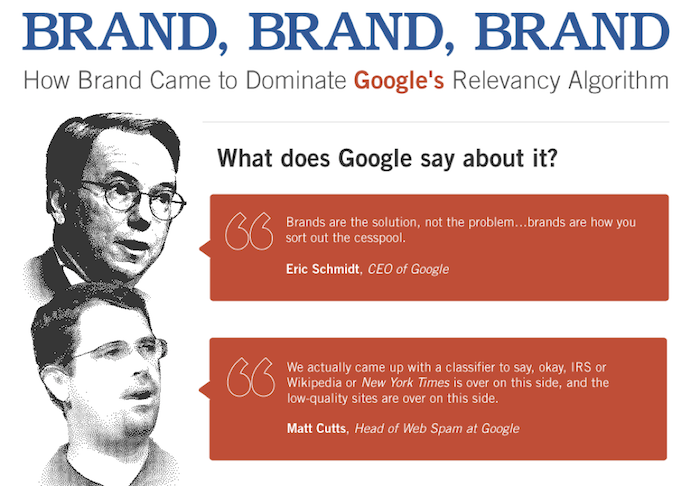

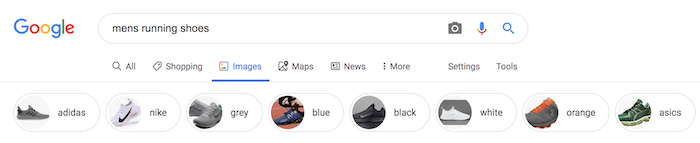

Google loves brands. Heck, when you type in “men’s running shoes,” they even have Nike, Adidas, and Asics there.

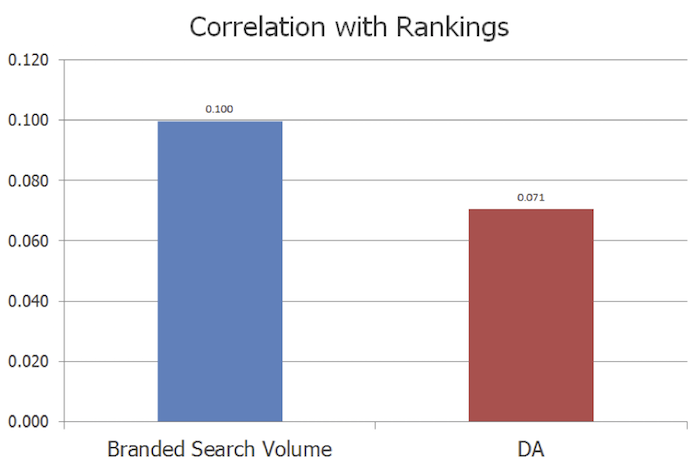

Branded search volume is more correlated with rankings than links or domain authority.

If you want to build a brand, focus on the social media

articles I linked to above and follow the brand building articles below:

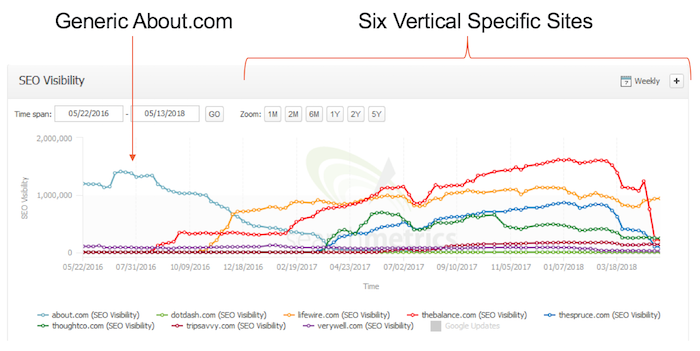

If you want to do well in today’s world of SEO, focus on one niche. Google prefers topic-specific sites because that’s what you and everyone else loves.

Just think of it this way… would you rather read medical advice from About.com or WebMD?

WebMD of course.

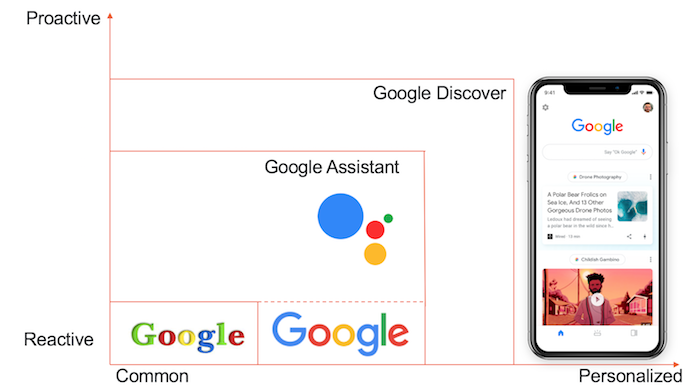

5. Future is personalization

Have you noticed that when you search on Google the results you see are different than the results of your friends?

It’s because Google is trying to personalize the results to

you.

Not just on Google search but anywhere you use a Google device… from a smartphone to Google Home to even their autonomous cars.

With all of the data they are gathering, they are better

suited to understand your preferences and then modify the results to that.

Just think of it this way: Every time you visit a place and you are carrying your mobile phone (especially if it is an Android device), Google may be able to potentially use that information to tailor results to you.

With your website, don’t try and show everyone the same message. If you personalize your experience to each and every user, you will be able to rank better in the long run as it will improve your user metrics.

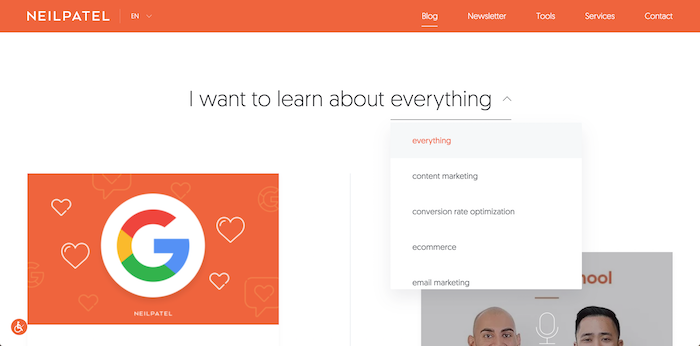

A good example of this is on my blog.

Right when you land there, I let you pick the type of content you want to see and then the page adapts to your interest.

It’s actually the most clicked area on the blog, believe it

or not.

Conclusion

SEO is not dead, it’s just changing.

Sure, click-through rates are going down and Google keeps adjusting its algorithm but that’s to be expected.

Google has made it so you can easily target your ideal customer through SEO or paid ads.

It used to be much more difficult before they came along. That’s why they are able to generate over 100 billion dollars a year in advertising revenue.

Don’t worry about things that aren’t in your control. Instead, start adapting or your traffic and business will be dead.

What do you think about the changing SEO landscape?

Even small loans can be challenging without a great bank rating. Learn why this little-known number matters, and how you can improve yours.

Need Small Loans for Your Business?

Even the search for small loans can be a recipe for frustration if you aren’t ready and don’t take the time to build your bank credit score. But what’s a bank credit rating, anyway?

Your Bank Credit Score – What’s it All About?

Do you know the distinction between bank credit scores and small business credit?

Company credit is the full and complete amount of money that your business can get from all manner of creditors. That means the banking system, credit unions, credit card companies, and also leasing firms. And it also means providers, under what’s called trade credit or vendor credit or trade lines. That is, the vendor credit tier.

A bank credit rating, on the other hand, is a measure of the full amount of borrowing capacity which a business can get from the banking system only.

Bank Credit Scores Clarified

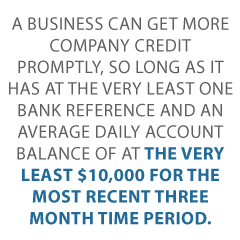

A business can get more company credit promptly, so long as it has at the very least one bank reference and an average daily account balance of at the very least $10,000 for the most recent three month time period. This setup will generate a bank credit score of a Low-5. So this means it is an Adjusted Debt Balance of from $5,000 to $30,000.

A lower rating, like a High-4, or balance of $7,000 to $9,999 will not instantly turn down the small business’s loan application. Nevertheless, it will slow down the approval process.

What is a Bank Score?

A bank rating is a measure of the average minimum balance as kept in a business bank account over a 3 month long period. Hence a $10,000 balance| will rank as a Low-5, a $5,000 balance will rank as a Mid-4. So a $999 balance will rate as a High-3, etc.

A company’s chief objective should always be to maintain a minimum Low-5 bank rating (or, an average $10,000 balance) for at least three months. This is because, without a minimum of a Low-5 score, most banks will operate under the assumption that the business has little to no capacity to pay off a loan or a business line of credit.

But there is one thing to remember: you will never actually see this number. The financial institution will simply keep this number in its back pocket.

The Bank Score Ranges

The numbers work out to the following ranges:

To get a High-5 score, your company will need to have an account balance of $70,000 to $99,999. For a Mid-5 score, your business must have an account balance of $40,000 to $69,999. And for a Low-5 rating, your business needs to hold onto an account balance of $10,000 to $39,000. So your company needs this level bank score or better to get a bank loan.

For a High-4 score, your company has to have an account balance of $7,000 to $9,999. And for a Mid-4 rating, your small business must maintain an account balance of $4,000 to $6,999. So for a Low-4 score, your small business will need to have an account balance of $1,000 to $3,999.

Ruining Your Bank Score

Unfortunately, there are a lot of ways to really destroy your bank rating. Here are 7 – and how you can fix them in order to get small loans or really any level of financing.

7th Way to Ruin Your Bank Credit Score and Lose Out on Small Loans

Do not maintain a minimum balance for a minimum of three months. Given that every bank rating cycle is based on the previous 3 months, a continuously seesawing balance ought to damage your bank score.

6th Way to Destroy Your Bank Credit

Don’t bother to ensure that your business bank accounts are reported precisely the same way as all of your small business documents are, as well as with the exact same physical address (no post office box) and telephone number. Sow confusion here by editing one and not another, or not remedying an error if there is one.

5th Way to Destroy Your Bank Credit and Lose Out on Small Loans

To accompany #6, do not see to it that each and every credit agency and trade credit supplier also lists the business name and address the precise same way. This is every keeper of financial documents, earnings and sales taxes, internet addresses and e-mail addresses, directory assistance, and so on.

No loan provider is going to stop to consider the myriad manners in which a business might be listed, when they explore the business’s creditworthiness. For this reason if they are not able to locate what they need quickly, they will either deny an application or it won’t be reported to a business credit reporting agency such as Experian, Equifax or Dun & Bradstreet.

Therefore, if they are not able to discover what they need quickly, they will just reject the application. So see to it your records are a mess!

4th Way to Damage Your Bank Credit Score

Never manage your bank account responsibly. This means that your small business must not avoid writing non-sufficient funds (NSF) checks at all costs, because those annihilate bank ratings. Non-sufficient-funds checks are something which no business can afford to let happen.

Balancing checkbooks and accounts is so dull anyway. You’ve got adequate money without even making sure, right?

3rd Way to Destroy Your Bank Credit Rating and Lose Out on Small Loans

To add to #4, do not include overdraft protection to your bank account ASAP, in order to avoid NSFs. Why bother thinking in advance or preparing for the future? Everything is going to be fantastic forever, right?

Writing checks insufficient funds (NSFs) is a sure way to destroy your bank score.

2nd Way to Damage Your Bank Credit Score

Do not let your small business show a positive cash flow. The cash coming in and leaving your business’s bank account must show a positive free cash flow.

A positive free cash flow is the quantity of profits left over after a business has paid every one of its expenses. According to Investopedia, it “represents the cash a company can generate after required investment to maintain or expand its asset base. It is a measurement of a company’s financial performance and health.”

When an account shows a positive cash flow it indicates your small business is producing more earnings than is used to run the business. That means the financial institution will feel your company can pay its expenses.

So if you actually intend to trash your bank score, get whatever’s expensive for your business so your expenses overtake your profits. Doesn’t every manufacturing facility deserve plush carpeting in the loading dock?

1st Way to Ruin Your Bank Credit and Lose Out on Small Loans

Financial institutions are extremely motivated to lend to a company with consistent deposits. And a business owner should also make regular deposits in order to preserve a positive bank score. The business owner needs to make several regular deposits, greater than the withdrawals they are making, in order to have and preserve a good bank rating. If they can do that, then they will have a great bank credit rating.

Consistency is the hobgoblin of little minds, right? So be a free spirit!

Damage Your Business’s Bank Score and Losing Out on Small Loans – Even Though You Will Never See This Number

You, the entrepreneur must never make regular deposits. And these deposits ought to never be more than the withdrawals you are making, in order to ruin your bank credit rating.

If you can do these things, then your company will have a dreadful bank credit rating. And, subsequently, a bad bank credit rating means your firm is far less likely to get small business loans.

Just Kidding: Obviously We Do Not Really Want You to Miss Out on Small Loans!

So, where do you go from here?

The First Great Way to Rescue Your Bank Credit Score

Possibly the most convenient way to attain and maintain a good bank credit is to deposit at least $10,000 into your small business bank account and maintain it there for as much as a half year. While you will still have to make consistent deposits, this one straightforward step will aid in 3 ways.

One, you will have maintained an excellent minimum balance for at the very least three months. Two, you will probably not overdraw with such an excellent balance. And three, you will get to the magic minimum for a Low-5 bank credit rating. Hence you will be dealing with our #4 and #7, above.

And you might even have the ability to get around our #3. But we still highly recommend overdraft protection.

The Second Wonderful Way to Rescue Your Bank Credit Rating

A 2nd need is to make sure your small business account details are consistent across the board, all over. While it might take some work order to ensure everything is right, you will be taking care of #5 and #6, above.

The Third Great Way to Rescue Your Bank Credit

A third necessity is to make regular deposits. And make certain they are more than the quantities you are withdrawing every month. This will take care of our #1 and #2 smoothly.

Takeaways for Your Bank Credit Rating and Small Loans

Your bank rating is not to be trifled with. Although the financial institutions maintain a secret regarding them, failing to keep your bank credit rating high will make it a great deal harder to do well in business. You might not even get small loans, so be diligent!

Have you ever wondered what exactly is on your corporate credit report? For instance, what is it telling lenders about your business? How are lenders using the information in their decision-making process? Are they simply taking the information at face value? Do they have their own formulas and algorithms that they apply? Your corporate credit report may not be what you think it is. This real corporate credit review will answer these questions and more.

What Does Your Corporate Credit Report Say About You, and How Do Lenders Use It?

Before we dive in, there are a few things you need to know. First, there are many companies from which a lender can pull your corporate credit report. Next, each company offers lenders more than one report. There is no way to know, without asking the lender directly, which report they will pull from which company. It could be all, one, or any combination.

Lastly, many lenders do actually apply their own formula to the information in the report to calculate a score that they feel is most useful to them. As a result, they may not even use the actual score on your corporate credit report.

All of these things are out of your control. What you can control, to a point, is the information on the report. For example, does it contain positive information? Is the information on it accurate? These are things you can work with. If the information lenders are seeing is both positive and accurate, you should be in good shape. However, you cannot do anything about the information on the reports unless you understand what it is they are reporting, and where they get their information. So here we go.

Corporate Credit Report: Dun & Bradstreet

Dun & Bradstreet offers six different reports. The one utilized most often by lenders is the PAYDEX. This is most likely due to the fact that it is the one most like the consumer FICO score. It measures how quickly a company pays its debt on a scale of 1 to 100. Lenders like to see a score of 70 or higher. To put it in perspective, a score of 100 reveals the firm makes payments ahead of time. A rating of 1 shows they pay 120 days late, or more.

Together with PAYDEX, they offer following.

Delinquency Predictor Score

This rating determines the chance the company will not pay, will be late paying, or will come under bankruptcy. For scoring, the range is 1 to 5, with 2 being a good score.

Financial Stress Score

As you might guess, this is a measurement of the pressure on a firm’s balance sheet. It shows the possibility of a closure within a year. The range is 1 to 5, and a 2 is good.

Supplier Evaluation Risk Rating

This is a ranking that predicts odds of a firm surviving one year. It ranges from 1 to 9, with a 5 being a good score.

Credit Limit Recommendation

As the name implies, this is a recommendation for the amount of debt a company can handle. Financial institutions usually use it to establish how much credit to extend.

D&B Credit Rating

This is an estimation of overall business risk on a scale of 4 to 1, where a 2 is considered good. The smaller the number the better. The rating is given in conjunction with letters, the combination of which show a company’s net worth.

Consequently, if there isn’t enough data on a business to assign a regular rating, an alternative score is assigned. This is called a credit approval score. It is based on the number of employees. They will use any data they have available to calculate this alternative rating. That means, a company can control this to a point by ensuring D&B has all of the information they need.

Commercial Credit Score

Along with the PAYDEX, Dun & Bradstreet releases a commercial credit report in three components. Each part shows how likely the business is to default on expenses or become seriously late on payments.

Commercial Credit Score

On a range of 101 to 670, the commercial credit score anticipates the likelihood of a firm making late payments. A rating of 101 indicates it is very likely that the company will be late with payments. Likewise, a score of around 500 is good.

Commercial Credit Percentile

For this measurement, the scale runs from 0 to 100. It shows the chance of delinquency too. However, it determines this probability versus other companies in the Dun & Bradstreet system. A rating of 1 is the highest possible probability versus various other companies. The majority of loan providers consider a rating of 80 or higher to be an advantage.

Commercial Credit Class

In contrast to the other reports, this is an approach of dividing businesses into classes based on the chance of delinquency. Firms in class 1 are the least likely to be overdue. Likewise, if you are in class 2, that’s great.

What Information is Used to Calculated the Dun & Bradstreet Corporate Credit Report?

Unfortunately, the exact formula that Dun & Bradstreet uses to calculate their rankings is proprietary. However, we do understand what information they use, as well as where they get it. In fact, the main source of information is the business itself.

You see, a company has to send a financial statement to D&B before getting a complete score. Without that, a business receives a restricted score based on how many workers they have. For example, the ranking would be 1R if the business has 10 employees or even more. It’s 2R if they have fewer than 2 staff members.

Without financial statements, a composite debt evaluation might still be offered. However, a business is only eligible for a ranking up to a 2 in this situation. They are ineligible for a 1 rating without a financial statement.

Additionally, businesses can submit trade recommendations to Dun & Bradstreet. However, it costs money to do so. Of course, there is no guarantee it will lead to a score boost. Also, if you are building business credit properly, it will happen for free anyway.

In addition, Dun & Bradstreet accesses public documents. In doing so, they try to find liens, insolvencies, or anything else that can show creditworthiness, or its absence.

Corporate Credit Report: Experian Business Credit Scores

Experian gathers data from a lot of the same sources as Dun & Bradstreet. As a result, their reports are similar. There are a few key differences in sources, calculation, and also presentation however.

Intelliscore Plus

Experian uses the Intelliscore Plus credit score, which shows a statistics-based credit risk. The result is, it is a highly predictive score that can help users make well-informed credit decisions.

The Intelliscore scores range from 1 to 100, with a higher score indicating a lower risk class.

Score Range Risk Class

Low Risk

76-100

Low-Medium Risk

51-75

Medium Risk

26-50

High-Medium Risk

11-25

High Risk

1-10

Exactly How Does Experian Compute the Intelliscore Rating?

One of the things Intelliscore is most known for is the identification of key factors that can indicate how likely a business is to pay its debt. In fact, over 800 variables go into the Intelliscore Plus calculation. Many of them are from the list of general information all credit agencies look at. However, some are unique to Experian. So here’s a breakdown.

Payment History

As you might imagine, this is your current payment status. That means, it shows how many times accounts have become delinquent. It also shows how many accounts are currently delinquent, as well as the overall trade balance.

Frequency

This one shows how many times your accounts have gone to collections. In addition, it notes the number of liens and judgments you have. Also, it shows any bankruptcies related to your business or personal accounts.

Frequency also incorporates information about your payment patterns. Were you regularly slow or late with payments? Did you decrease the number of late payments over time? That affects your score.

Monetary

This specific factor focuses on how you make use of credit. For example, how much of your available credit are you using right now? Do you have a high ratio of late balances when compared with your credit limits?

Of course, if you are a new business owner, a lot of this information will not exist yet. Intelliscore Plus handles this by using a blended model to identify your score. This means your personal credit score becomes part of determining your business’s credit score.

Experian’s Blended Score

The blended score is a one-page report that provides a summary of the business and its owner. A combined business-owner credit scoring model works better than a business or consumer only model. In fact, blended scores have been found to outperform consumer or business scores alone by 10 – 20%.

Experian Financial Stability Risk Score (FSR)

FSR predicts the potential of a business going bankrupt or not paying its debts. Consequently, this score identifies the highest risk businesses by using payment and public records. They look at a number of factors, some of which include:

high use of credit lines

severely late payments

tax liens

judgments

collection accounts

risk industries

length of time in business

Corporate Credit Report: The Equifax Service Credit Rating

Similarly, Equifax shows three different points on its corporate credit report. These include:

Equifax Payment Index

Similar to PAYDEX, Equifax’s payment index is a measurement on a scale of 100. It shows how many of your small business’s payments were made on time. Like the others, it uses data from both creditors and vendors. However, it’s not meant to anticipate future behavior. That is what the other two scores are for.

Equifax Credit Risk Score

This score shows the likelihood of your company becoming severely delinquent on payments. Scores range from 101 to 992 and include an evaluation of:

Available credit limit on revolving credit accounts, including credit cards

Company size

Proof of any non-financial transactions (like merchant invoices) which are late or were charged off for two or more billing cycles

Length of time since the opening of the earliest financial account

Equifax Business Failure Score

Equifax’s business failure score takes a look at therisk of your business shutting down. It runs from 1,000 to 1,600 and bases its scoring on these factors:

Total balance to total current credit limit in the past three months

The amount of time since the opening of the oldest financial account

Your small business’s worst payment status on all trades in the last 24 months

Proof of any non-financial transactions (like merchant invoices) which are late or are on a charge off for two or more billing cycles

For the credit risk and the business failure scores, a rating of 0 means bankruptcy.

Equifax Scores

A positive Equifax score for your business is as follows:

Payment Index 0 to 10

Credit Risk score 892 to 992

Business Failure score 1400 to 1600

Are These the Only Agencies Where You Can Get a Corporate Credit Report?

In short, no. In fact, there are multiple other agencies that will issue a corporate credit report. These, however, are known as the big three. They are the most commonly used. Still, there has been an increase in the use of another option recently. It’s the FICO SBSS.

So, the FICO SBSS is the business variation of your personal FICO credit report. Unlike your personal FICO, the SBSS reports on a scale of 0 to 300. The higher the score the better. However, the majority of loan providers demand a rating of least 160.

Exactly how is the FICO SBSS Scored?

Surprisingly, it is significantly different from other business credit scoring designs. The SBSS utilizes your corporate credit score and individual credit rating. It also makes use of monetary details like business assets and income. As you can see, the goal is to give an overall financial picture rolled into one rating.

Business owners cannot access their FICO SBSS by themselves. There is a proprietary formula for score computations. FICO does not make that info public. The result is, you go into lending institutions blind as to what your FICO SBSS credit rating might be.

Furthermore, lenders can choose how certain factors are weighted in the computation of your score. This means your FICO SBSS could actually be different from one lender to the next. For example, one lender could put more weight on your business payment history, while another could lean more on your personal credit score.

Corporate Credit Reports: What Can You Do?

Now that you know who issues them, how they are calculated, and what information lenders may see, you can begin to figure out how you can ensure your corporate credit report contains as must positive information as possible. The number one thing you can do is make your payments on time. Regardless of what report they look at from which agency, the thing all lenders care about most is that you pay your bills.

In addition, you can monitor your credit reports to ensure all information is complete and accurate. If you see a mistake, contest it. Do so in writing, and be sure to send copies of any backup documentation. If you see old information, get it updated. You don’t want old addresses or closed accounts causing problems. Monitor your corporate credit for a fraction of what it costs with the reporting agencies directly here.

In the end, the most important thing you can do for your corporate credit report is to make your payments consistently on-time. The rest is important, but this is the number one thing lenders look for when it comes to making credit decisions.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.