Bill and his guests – Jelani Cobb, Chelsea Handler, Ted Lieu, Evan McMullin, and Ana Navarro – answer viewer questions after the show. (Originally aired 4/7/17)

Private Blog Networks(PBNs) claim to work because they generate backlinks – and that much is true.

What about their other claims, though?

We know backlinks work to improve SEO and therefore visibility in the SERPs, but do PBNs work?

And if so, do they work well?

Howdo they even work?

Well, let’s answer those questions.

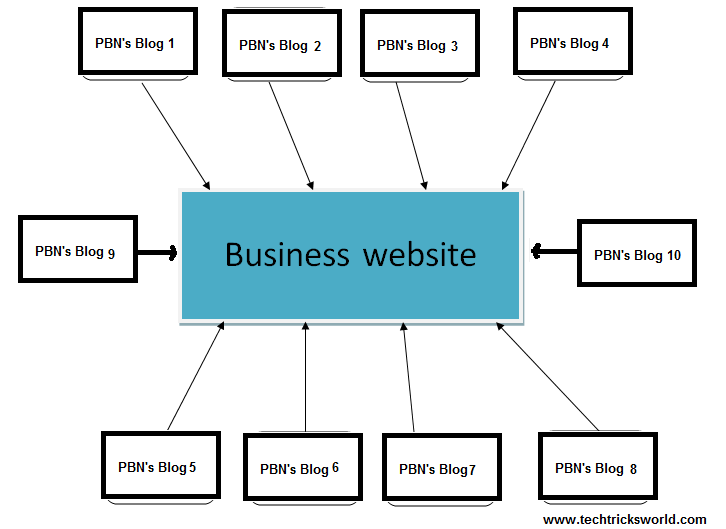

What Is a Private Blog Network?

Luckily, private blog networks are actually quite simple to understand.

At some point in the era of SEO, someone figured out how to build a massive amount of backlinks from high-domain authority websites without much effort.

They did it by purchasing expired domain names that had already established domain authority.

Then, after collecting quite a large portion of these domains, they posted basic content to each website and included a backlink to their primary website in all of the content.

And voilá! They immediately generated loads of backlinks from high-domain authority websites.

At that moment, private blog networks were born.

Think of PBNs like a database of websites that, when you pay, all give your website backlinks.

And with all of those backlinks your website’s domain authority, SEO, and rankings all benefit.

It sounds great, right?

Why wouldn’t you want to pay a little bit of money to increase your rankings and generate passive traffic to your website?

That’s the dream of most SEO experts, after all.

Well, not so fast.

To help you determine whether you should leverage PBNs, we’re going to first talk about the benefits that they have to offer. Then, we’ll discuss why they are a bit risky.

With that knowledge, you’ll be better prepared to make an informed decision for yourself.

Pros: The Benefits of Private Blog Networks

While you might have heard that PBNs are scams that won’t help your SEO, that claim is only partly true.

PBNs offer legitimate benefits.

But before I get much further, let me mention a quick disclaimer:

I’ve never used a PBN for my own website and I don’t recommend using them for your website either.

I’ll explain why a little bit later, but I wanted to get that out in the open, so you know where I stand.

For now, though, let’s discuss why PBNs entice many marketers.

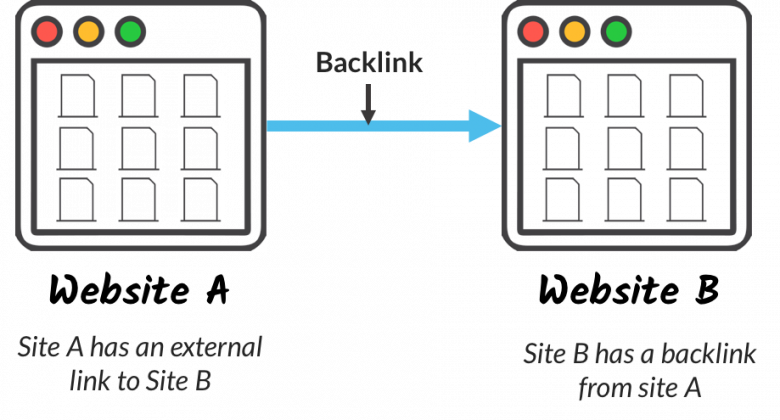

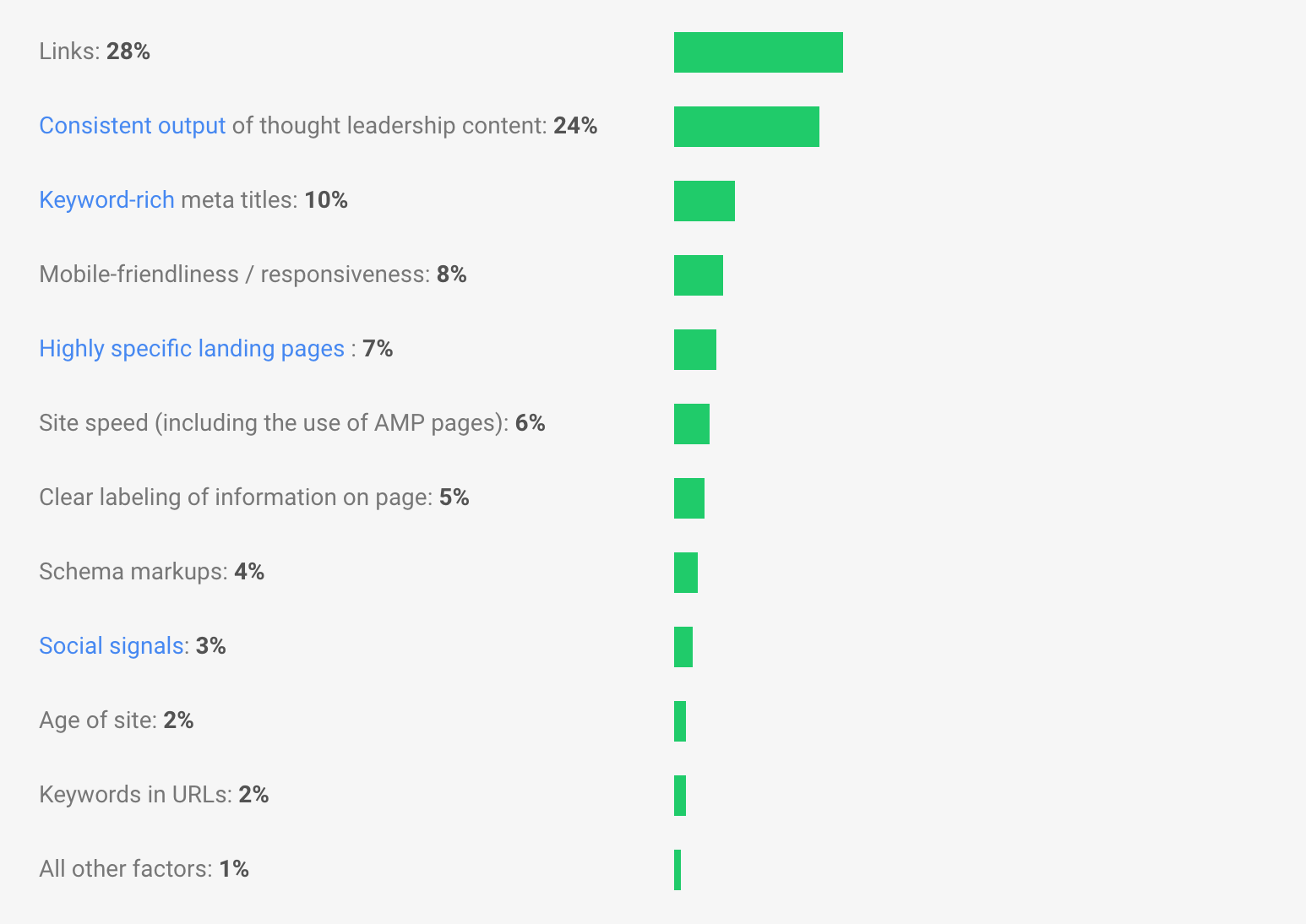

As I already mentioned, backlinks fuel the success of private blog networks.

And what exactly is a backlink?

A backlink is a hyperlink that leads from an external website to your own website. And these little beauties massively help your SEO.

Backlinks communicate to search engines that the linking website trusts your website enough to associate itself with your domain.

That means that the search engines will trust your website as well.

It’s kind of the same thing as playing with the cool kids on the playground.

When you’re hanging with the cool kids, that makes you cool.

Similarly, to figure out which websites are worth trusting, search engines look at which websites are linking to each other.

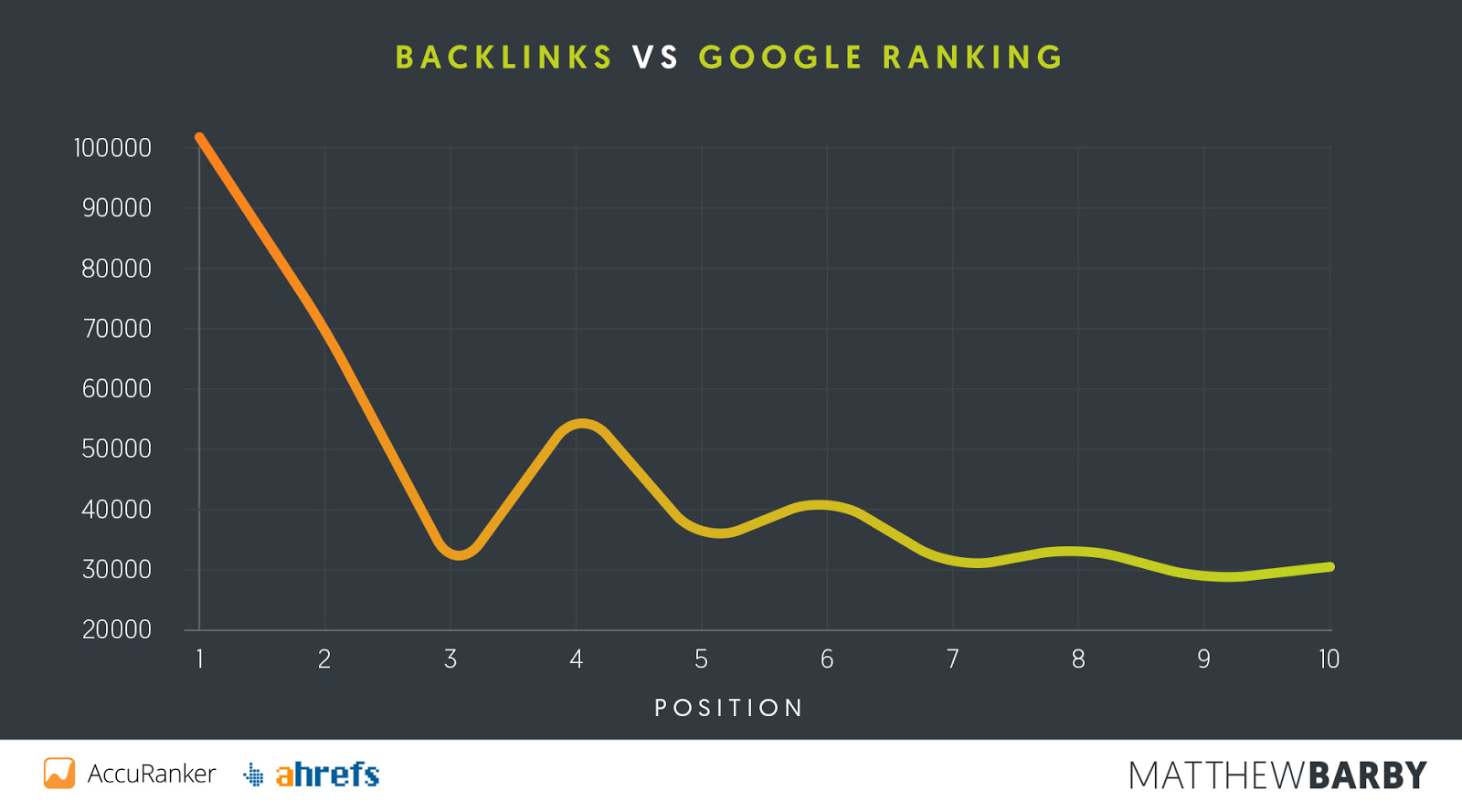

For that reason, link building is the top factor contributing to the rankings of a website.

PBNs can be so effective at building these backlinks that one company experienced this difference in its rankings after working with a private blog network.

That’s why so many marketers use them at some point. It’s why they have stuck around for so long, and it’s the reason that certain SEO firms make loads of money.

But what’s the dark side?

After all, everything that goes up must come down. Everything that sounds too good to be true is too good to be true.

Here are the cons you need to be aware of.

Cons: The Risks of Private Blog Networks

PBNs sound great.

That is until you find out about the risks involved with using them.

Yes, they can increase your SEO and help generate passive traffic and leads to your website.

However, that entire marketing strategy can quickly become a disaster if Google catches you.

So, in case you’re wondering, yes: Google hates PBNs and intentionally tries to penalize people who use them.

But how? How does Google penalize websites that use PBNs to boost their SEO?

How would they know what you’re doing?

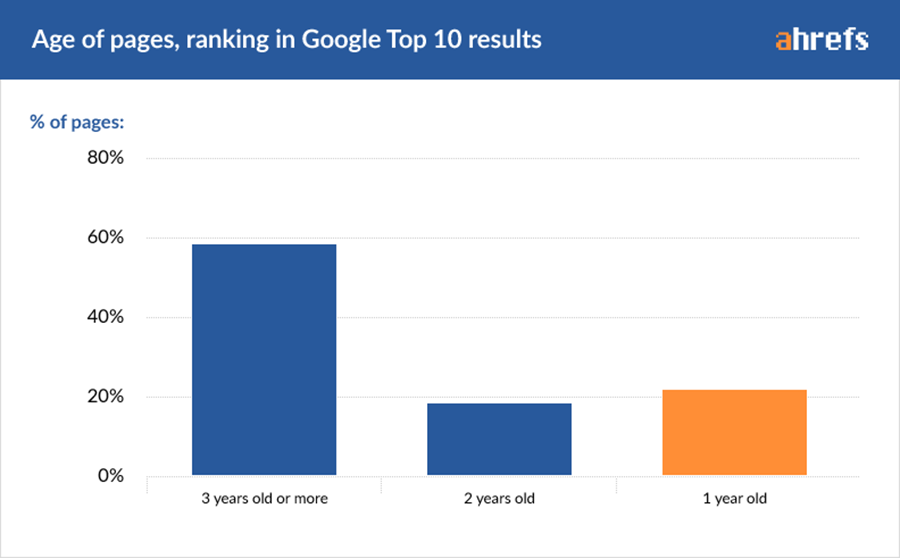

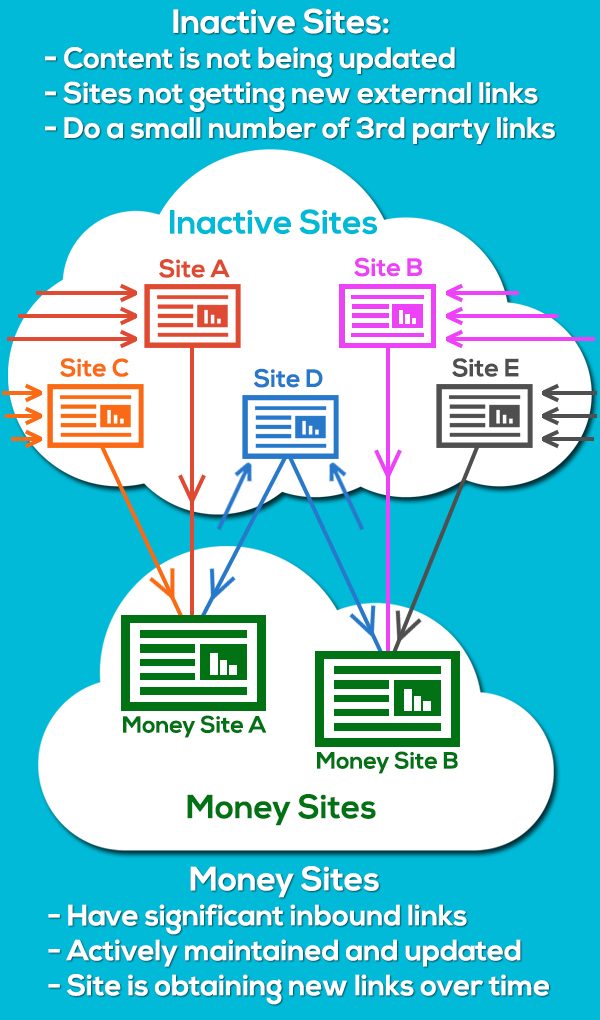

Well, if all of the websites that you’ve received backlinks from are websites with very little activity, few updates, and almost no internal linking, then Google gets suspicious.

That makes it easy for most search engines to spot them.

In the end, if you decide to use PBNs, know that you run the risk of hurting your website’s SEO.

Legitimate pros exist, but only under a cloud of potential penalization by search engines.

You might generate some quick domain authority with PBNs. While traditional strategies take longer, they aren’t nearly as risky.

But if you want to rise through the rankings the right way, then here are five risk-proof strategies you can use instead.

1. Guest Blogging

Guest blogging gives you an opportunity to provide value for someone else’s website while also getting a backlink.

If you do it right, this strategy will be a win for the website you write for and a win for your own website as well.

For that reason, SEO agencies and experts alike use guest blogging as one of their link-building strategies.

You can do the same thing.

Just find blogs within your industry and pitch the editors an article over email. If they accept your pitch, you can run off to write and include a backlink to your own website.

But before you do, make sure that you ask the editor what their policy is regarding backlinks.

They might not want you to include a backlink to your website within the article itself, but they’ll let you put it in your bio.

Either way, you win a backlink, and they win a valuable piece of content for their audience.

Now, you might be nervous that editors won’t respond to your emails.

Always include these two specific things in your testimonial.

Provide a number that shows the success you experienced from using their product or service (traffic or lead generation numbers, revenue numbers, or the number of opt-ins, for example).

Talk about one concern you had when buying the service that the excellence of your experience quickly dispelled. (For example, “The price point seemed a little high at first, but now I realize that every single penny was worth it! I’d even spend more for this service, but don’t tell them I said that.”)

With that start, you’ll be off and writing testimonials for your partners in no time, generating backlinks with every reference.

3. Creating Share-Worthy Content

If you don’t create content worth sharing, then you can probably guess what will happen: No one will share it.

Your goal when you write that blog post or film that video or design that infographic is to generate attention for your brand.

You want to increase brand awareness, drive traffic to your website, and use the content to generate leads.

You even want to generate social backlinks to your website.

But, of course, you can’t do that if you create bad content.

If you’re going to create the content anyway, then take the time to make it great. Make it share-worthy.

Another strategy that works is spying on your competitors to understand what’s performing best on social media. Here’s an easy way to do so:

Step #1: Visit Ubersuggest, Type Your Keyword and Click “Search”

Step #2: Click “Content Ideas” in the Left Sidebar

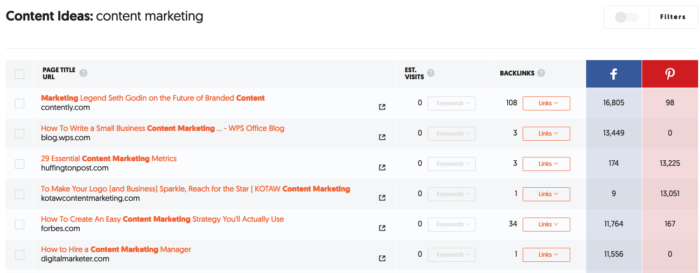

Step #3: Analyze the Results

What you end up with is a long list of top-performing content related to your keyword.

For example, the top listing, “Marketing Legend Seth Godin on the Future of Branded Content,” has been shared 16,805 times on Facebook and nearly 100 times on Pinterest. That gives you a pretty good idea that the content is share-worthy. Now, you can craft your content in a similar manner, with the goal of achieving the same results.

However you do it, take the time to create amazing, share-worthy content. You’ll generate far more social backlinks, drive more traffic, and build better brand awareness.

You’re creating the content, so do the best that you can with it.

4. Leveraging Your Social Platforms

Social signals play a massive part in SEO.

Websites that stay active on their social media accounts, update their information, and generate more content shares tend to rank better than websites that don’t.

Why does Google rank websites that have an active and updated social media presence better than those that don’t?

The short answer is that search engines want to know your website is active and relevant.

If you’re generating lots of shares and social signals, then that tells Google to rank you better.

This means that just staying active on your social media accounts can help your SEO. It really is that simple.

And the more engagement you get on your social media pages, the better.

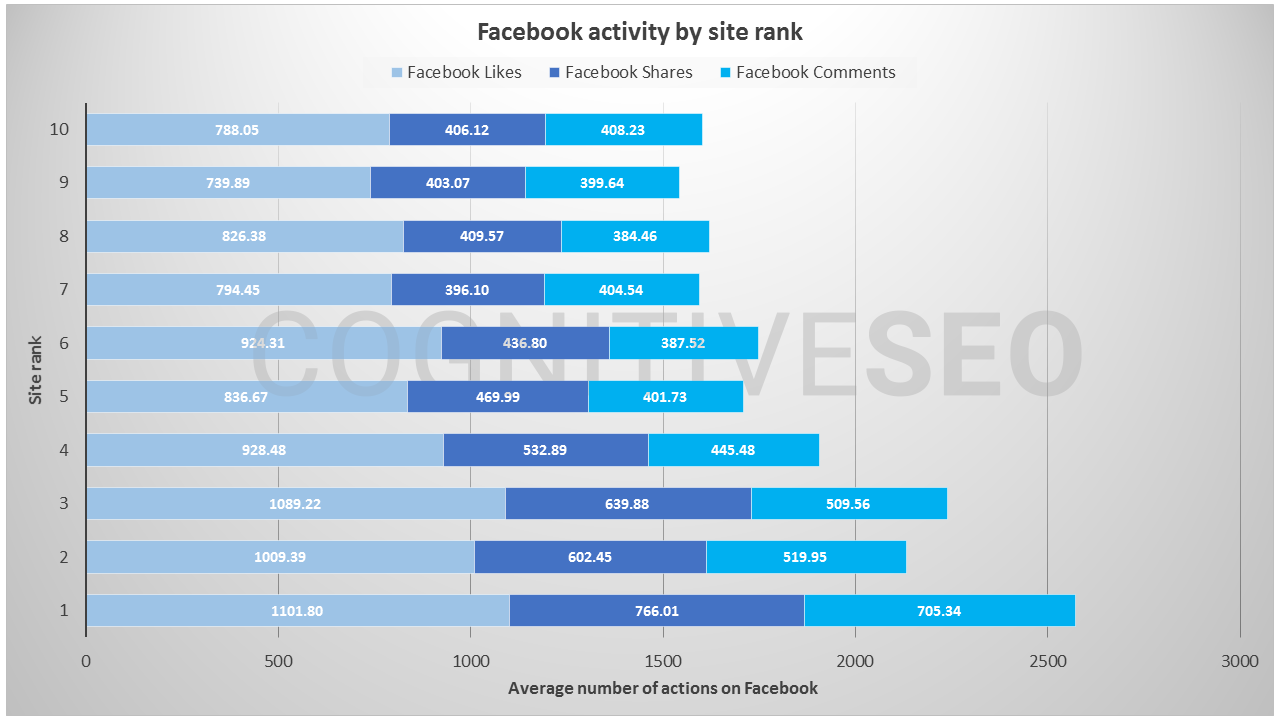

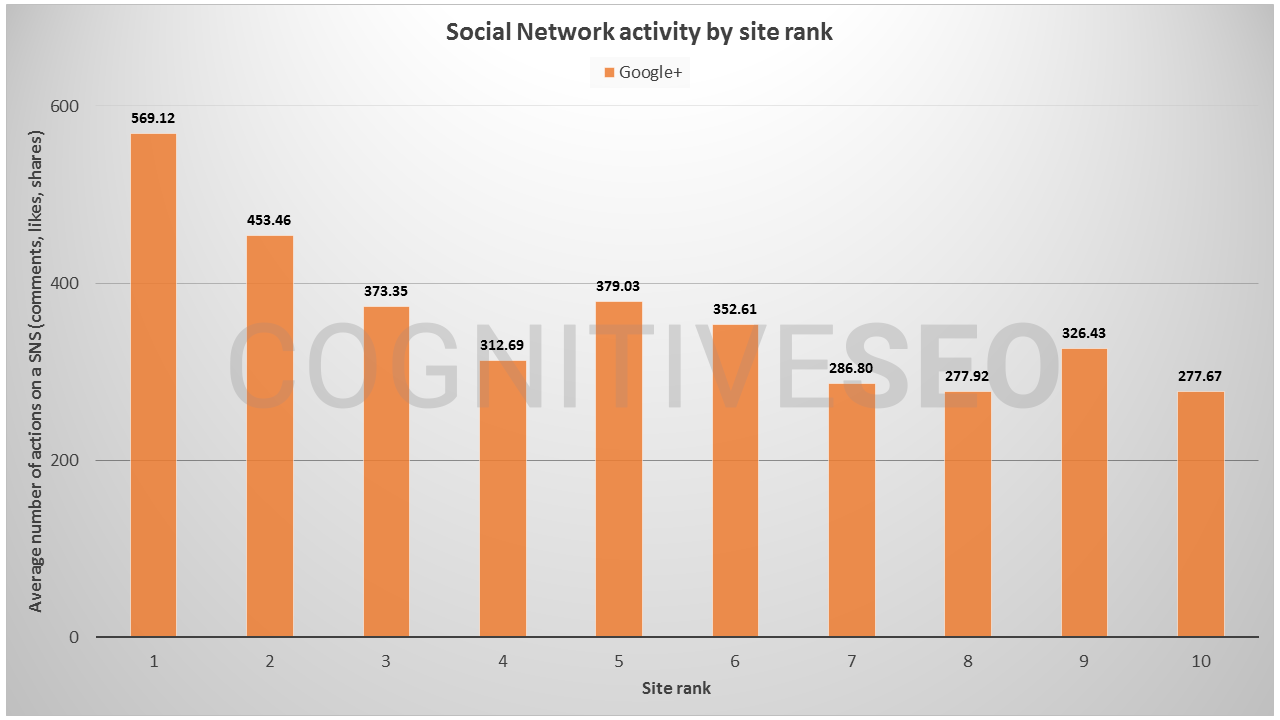

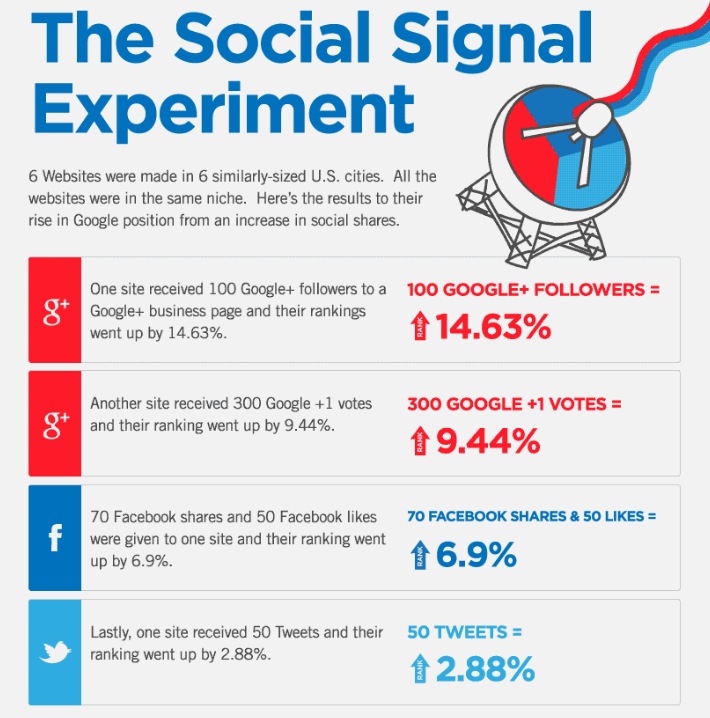

A 2016 experiment tried to discover the impact that social media can have on your website’s SEO.

In the study, one website with an increase in social shares experienced a 14.64% increase in rankings, and another website received a 6.9% SEO boost.

But if that’s not enough motivation for you to stay active on your social media accounts, just consider the additional traffic you’ll drive to your website with each post.

You won’t only win social backlinks. You’ll also generate traffic, leads, and even conversions.

5. Building a Loyal Audience

You’ve stuck with me this far.

But now you’re wondering, “How does building a loyal audience help your SEO?”

And that’s a great question.

Unfortunately, the answer isn’t as direct as you might like.

This means that just posting on your website’s blog regularly will benefit your SEO.

After all, the more people who search for your website and the more popular you become, the higher your domain authority will surge.

In other words, with a loyal audience comes a better ranking.

And, in turn, that’s good for growing your audience.

You see, it’s kind of like a self-sustaining, perpetual cycle.

With a larger audience comes better SEO, and with better SEO comes a larger audience. And with a larger audience comes better SEO, and on it goes. You get the point.

Plus, the bigger your audience, the more shares you’ll generate on social media, further helping your link-building strategy.

Of course, Rome wasn’t built in a day, and you won’t build your audience overnight.

Building a loyal group of followers is a process of posting consistent content over a long period of time.

You’ll cross times of discouragement and tribulation.

In other words, all of that time and energy you dedicate to pleasing your existing audience will pay off when you’re trying to market to them.

Plus, you’ll generate more attention and better SEO from a loyal customer base than you will from new and fleeting customers.

Private Blog Networks Frequently Asked Questions

Can you be penalized for using a Private Blog Network?

Yes, you can be penalized for doing this.

Why are PBNs bad?

Google considers them scammy.

How do I find PBN sites?

Look for sites with high authority and links that you can buy – but this strategy is not recommended.

Are PBNs considered Black Hat SEO?

They aren’t considered black hat, but they are penalized by Google.

{

“@context”: “https://schema.org”,

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “Can you be penalized for using a Private Blog Network?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: ”

”

}

}

, {

“@type”: “Question”,

“name”: “How do I find PBN sites?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: ”

Look for sites with high authority and links that you can buy – but this strategy is not recommended.

”

}

}

, {

“@type”: “Question”,

“name”: “Are PBNs considered Black Hat SEO?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: ”

They aren’t considered black hat, but they are penalized by Google.

”

}

}

]

}

Private Blog Networks Conclusion

So, should you use private blog networks?

As I explained, they can help your SEO, and they can do it fast. But the entire time you use them, you run the unfortunate risk of destroying your website’s ranking potential in one fell swoop.

Is the risk worth it?

I hope that you’ll answer that question with a “no.”

The better option is to build your backlinks over time by guest blogging, writing testimonials, creating share-worthy content, leveraging your social platforms, and building a loyal audience.

Even though it might feel like it takes a long time to rise through the rankings using those strategies, that’s time well spent.

You’ll have peace of mind knowing that no one can penalize you for shady methods.

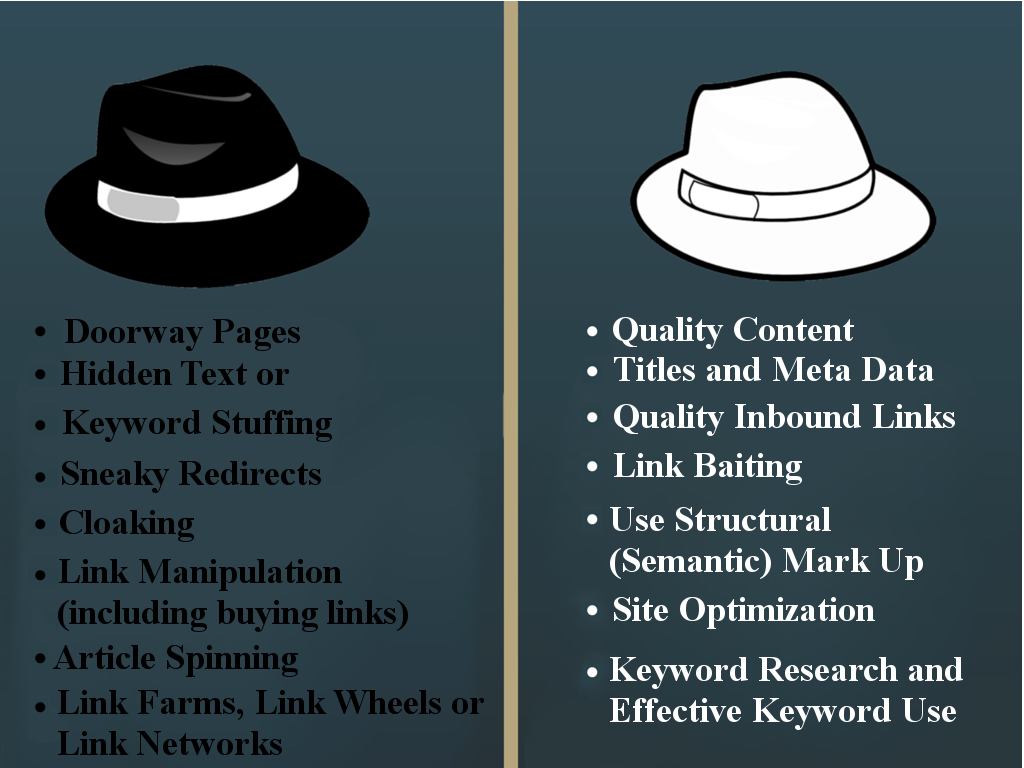

Private blog networks aren’t black hat. But they certainly aren’t white hat, either.

They are gray hat. And that’s a hat you shouldn’t be willing to wear.

Do you think private blog networks are a penalty waiting to happen or a great SEO hack?

What are Private Business Lenders and Private Business Funding?

Real estate investing is big money. But not every entrepreneur qualifies for loans from big banks, and other traditional sources. Not to worry, there are private lenders out there, willing to lend money. Private money business loans just might be the solution you’re looking for – from private business lenders.

What are Private Business Lenders?

Private business lenders are generally funded by investors, or by banks, or both. Private lenders are in the business of taking funds from private investors. They make private business purpose loans with those funds.

Investors expect a decent return from their investments, and interest rates from money borrowed from banks is significantly higher, than the banks are being charged for the funds. These factors raise the private lender’s expenses. Those expenses are then passed on to the ultimate borrower. Unlike with angel investing or venture capital, the borrower isn’t giving away a percentage of ownership.

Why Work with Private Business Lenders?

Apart from possibly not qualifying for traditional lending, there are other reasons why it may be better to work with a private lender. Banks are often tougher to deal with than private lenders. Banks are subject to significant state and federal regulations. They must work within governmental and quasi-governmental agency programs, like Fannie Mae, Freddie Mac, the VA, and HUD. These regulations often dictate which businesses a bank can lend to, and what borrower profiles should look like.

Private business lenders, while still subject to state and federal laws, are significantly less regulated. They can be more flexible in the types of loans they make, and who their customers are.

Hence is it generally easier to get approval from a private lender, versus a traditional bank. Private lenders can customize each loan based on a set of internally set criteria, like credit scores, loan to value ratio, and debt to income levels.

In contrast, bank approvals are program or computer driven. The lender only has a little discretion. Private lenders tend to take a more common sense approach, to understanding borrower issues and overcoming them.

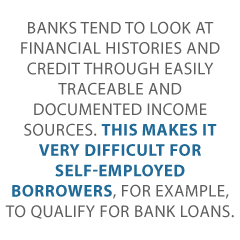

Banks tend to look at financial histories and credit through easily traceable and documented income sources. This makes it very difficult for self-employed borrowers, for example, to qualify for bank loans.

A hard money loan is a type of real estate loan. It is issued by a private lender for non-owner occupied property. Hard money loans are usually short term. They tend to be between six and 36 months. They have a higher interest rate than traditional bank loans.

Let’s look at Hard Money Loan Approvals

You get approval for hard money loans based on the value of the real estate, rather than the creditworthiness of the borrower. These loans are often used because they have an exceptionally fast approval time. They are often closed within two to four weeks.

What is the Difference Between Hard Money Loans and Bank Loans?

The main difference is the lender. Hard money loans are almost always given by a private lender. This is so whether that’s an individual or a private lending company. These loans are used for non-owner occupied real estate. So they aren’t regulated like consumer mortgages. As a result, hard money lenders can charge higher interest rates and fees, and they can get away with terms that wouldn’t be allowed with traditional loans.

The Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA) don’t often apply to commercial mortgages. But there are still regulations traditional financial institutions must follow. Federally insured banks are still regulated by the FDIC. Credit unions are regulated by the National Credit Union Administration (NCUA). But hard money lenders don’t have any regulations placed on them.

What Sorts of Real Estate is Covered by Private Money Financing?

A hard money lender may loan on any type of non-owner occupied real estate. This includes all sorts of real estate investments. But they’re often looking for situations with a fairly quick exit strategy, so they know they’ll get paid by the end of the loan term.

Let’s look at Private Small Business Loans for Fix and Flip Properties

Hard money loans are very common with fix and flip properties. In fact, many lenders will even finance the repairs. These types of deals are ideal for the lender because flips tend to be completed within six months.

If the lender is also financing the repairs, they will estimate the cost of the repairs, and issue draws as the borrower needs them to pay for the work being done. This ensures the funds are being used for the repairs. It also limits the lender’s exposure, since they’re only giving out a small amount of money at a time.

Many hard money lenders prefer to finance the repairs. This way, they know the project will be completed. If the borrower gets through the demolition and runs out of money, the value may become less than the purchase price. By financing the project, they don’t have to worry about the borrower not being able to finish the job due to a lack of funds.

Consider Hard Money for Rentals

Hard money lenders will also provide short-term loans for residential real estate investment properties. The goal here is often to refinance the property in 12 to 36 months, to be able to pay off the hard money loan. Investors may use a hard money loan for a rental property if they need to be able to close the deal quickly, and don’t have the time to go to a bank. Or they may need a private loan if the rental property needs repairs before a bank will finance the deal.

Let’s look at Hard Money for Multifamily Properties

Like loans for rental properties, investors may need capital quickly to close on a multifamily property. This is the case if there’s not enough time to go through the traditional lending process. Private money lending is just plain faster.

An investor may also be buying a multifamily property with little to no tenants that needs a lot of repairs. This type of property would be hard to get financed with a bank, so they may seek out a hard money loan. Investors can get the necessary work done. And they can lease the property before refinancing it with a long term loan.

Consider Hard Money for Commercial Real Estate

A common situation with commercial real estate is an investor having a tenant to lease space to, but no property to put them in. The investor will find a vacant property that the tenant will lease out, but they have to buy the property and get it ready for the tenant first.

A bank may not want to finance a vacant property intended for use as an investment if the borrower doesn’t have the assets to secure the loan. A hard money loan can be useful in this situation to get the deal done. The investors can accomplish the tenant improvements and get the property leased. Once the tenant is in place and paying rent, a bank will be more willing to finance the real estate.

Check out Interest and Fees on Hard Money Loans

The convenience and easy approval with a hard money loan comes at a cost. Lenders will charge higher interest on hard money loans. This is because they are higher risk loans. It is also because these loans are short term.

Longer term loans will earn interest for several years from processing one loan. But the money invested in hard money loans must be reinvested every six to 36 months. There’s added cost and new risks each time that money is invested in a loan. Interest rates for these loans tend to be a few percentage points higher than traditional bank loans.

The lender will charge upfront fees to cover the cost of processing the loan, plus any commissions being paid. This also ensures they still earn a profit; in case the borrower pays off the loan before the end of the term.

Common fees for a hard money loan include origination fee, broker fee, application fee, underwriting fee, document prep fee, processing fee, and funding fee. These fees can add up to thousands of dollars.

Consider Credit Checks and Property Values

In general, private lenders are going to be all right with average credit. Their main concern is the value of the property. Plus a lender wants to know the market the property is in. This is due to higher risk. The lender wants to be able to recover their costs in case of foreclosure. See fool.com/millionacres/real-estate-financing/hard-money-loans/5-best-hard-money-lenders.

More Details on Private Small Business Loans and Hard Money Loans

There is a balloon payment at the end of the short term. For fix and flip, the lender knows the borrower can afford the balloon payment. But in the case of a borrower looking to refinance the property by the end of the term, the may not be as willing to lend to someone with bad credit. They will look closer at the borrower’s credit and personal finances in this case. The lender may also require a higher down payment to limit their risk in case the borrower can’t pay the lender off at the end of the term.

Private lenders for business loans will look into a borrower’s experience. For a fix and flip, private business lenders will want borrowers who have completed at least a few other deals. Smaller lenders usually stick to markets they know and states that have a strong real estate market. They often don’t like rural properties and provide a lower loan to value for them.

Private Money Financing: Takeaways

Private money financing is a way for real estate investors and house flippers to get funding. Also called hard money loans, private money financing tends to have fast approvals, but higher interest rates and no regulation to speak of. Experienced flippers in urban areas with good real estate markets are more likely to get approval.

How Private Business Loans Can Help Build or Improve Business Credit The concepts of business credit and private business loans are new to many business owners. The terms are discussed more often now than they were 10 years ago. Still, many are unfamiliar with what they are and how they can play into the success … Continue reading Build or Improve Business Credit with Private Business Loans

How Private Business Loans Can Help Build or Improve Business Credit

The concepts of business credit and private business loans are new to many business owners. The terms are discussed more often now than they were 10 years ago. Still, many are unfamiliar with what they are and how they can play into the success of your business.

For many looking to start a business, they know no other way than to get started with personal loans on their personal credit. Others understand the concept of business credit, but are unsure how to get it. Then there are those that have found private loans, but aren’t sure how to best utilize them to build or improve business credit.

We hope to answer all these questions and more, specifically those relating to using private loans to build and improve business credit.

What Is Business Credit?

Business credit is credit that is in the name of your business. It isn’t connected to the business owner in any way. It is in the business name, the business contact information, and the business EIN rather than the owner’s SSN.

If you have business credit, you can use it to apply for funding for your business. The debt and the payments will not be on your personal credit report at all. The problem is, most traditional lenders rely on the personal credit score most heavily, even if a business does have business credit. This is where private business loans can be helpful.

What are Private Business Loans?

Private business loans are loans from companies other than banks, also called alternative lenders. Many of these have popped up in the past decade as entrepreneurship has become more prevalent. The need for a financing option from institutions other than traditional banks has encouraged this increase.

There a few benefits to using private business loans over traditional loans. The first is that they often have more flexible credit score minimums. Even though they still rely on your personal credit, they will often accept a score much lower than what traditional lenders require. Another benefit it that they will often report to the business credit reporting agencies, which helps build or improve business credit.

The trade off is that private business loans often have higher interest rates and less favorable terms. In the end though, the ability to get funding and the potential increase in business credit score can make it well worth it.

How Can You Use Private Business Loans to Improve or Build Business Credit?

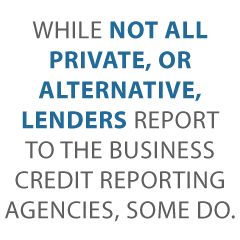

While not all private, or alternative, lenders report to the business credit reporting agencies, some do. These are the ones you want to work with. As they report your on-time payments, your credit will grow. They must report to Dun & Bradstreet, Experian Business, Equifax Business, or some other agency that reports business credit. Otherwise it won’t work. Not all private lenders will do this. You have to ask.

There are some lenders that are known to report to the business credit agencies however.

Which Private Lenders Report?

As a general rule, you simply have to research lenders to determine whether or not they report to the business credit reporting agencies. Sometimes this is as simple as asking them who they report payments to. Here are a few that we know oft to get you started.

Fundation

Fundation offers an automated process that is super-fast. Originally, they only had invoice financing. Then they added the line of credit service. Repayments are automatic, meaning they draft them electronically. This happens on a weekly basis. One thing to remember is that you could have a repayment as high as 5 to 7% of the amount you have drawn, as the repayment period is comparatively short.

You can get loans for as little as $100 and as high as up to $100,000, but the max initial draw is $50,000. They do have some products that go up to $500,000. Though there is no minimum credit score requirement, they do require at least 3 months in business, $50,000 or more in annual revenue, and a business checking account with a minimum balance of $500.

Fundation reports to Dun & Bradstreet, Equifax, SBFE, PayNet, and Experian, making them a great option if you are looking to build or improve business credit.

BlueVine

The minimum loan amount available from BlueVine is $5,000 and the maximum is $100,000. Annual revenue must be $120,000 or more and the borrower must be in business for at least 6 months. Personal credit score has to be at least 600. It is also important to know that BlueVine does not offer a line of credit in all states. You can find out more in our review here.

They report to Experian. They are one of the few invoice factoring companies that will report any business credit bureau.

OnDeck

With OnDeck, applying for financing is quick and easy. Apply online, and you will receive your decision once application processing is complete. Loan funds will go directly to your bank account. The minimum loan amount is $5,000 and the maximum is $500,000.

There is a personal credit score requirement of 600 or more. Also, you must be in business for at least one year. There is an annual revenue requirement of at least $100,000 as well. In addition, there can be no bankruptcy on file in the past 2 years and no unresolved liens or judgements.

OnDeck reports to the standard business credit bureaus.

The Business Backer

The Business Backer offers a product they call FlexFund Line of Credit. Funds range in amount from $5,000 to $240,000, and draws can be repaid on either a daily or weekly basis.

They report to Dun & Bradstreet and Equifax.

What Are Some Other Ways to Build Business Credit?

There are other ways to get accounts reporting on your business credit as well. One option is to look at the regular payments you make already. Do you pay rent? Do you pay telephone, internet, or utility bills? Ask your landlord and utility providers to report your payments to the business credit reporting agencies. Of course, they do not have too. However, some will if you ask. This is a way to get accounts reporting without taking on new debt.

Another option is to talk to merchants you already do business with. If you have been working with them for a while, there is a chance they will extend credit. Ask them if they will extend credit and report to the business credit agencies. Again, they may not do it, and they do not have to. It never hurts to ask though. You’ll never know until you do.

These two options are quick and easy ways to start to build business credit in addition to private business loans. There is another way however, and you can utilize it at the same time as you do the private business loan avenue. It’s called the vendor credit tier.

How to Use the Vendor Credit Tier and Private Business Loans Together to Build Credit Faster

The vendor credit tier is made up of starter vendors that will offer invoices with net terms, and then report payments on those invoices to the business credit reporting agencies. These vendors sell things most businesses use every day. This means all you have to do is buy the things you already need, pay the invoice, and watch you score grow.

Not all vendors are starter vendors. True starter vendors will offer net terms without a credit check so that you can get started with them before you have any business credit to speak of. Instead, they look at things like time in business and annual revenue to determine eligibility. Some of the easiest vendors to get started with include:

● Grainger Industrial Supply

Grainger sells power tools, pumps, hardware and other things. In addition, they can handle maintenance of your auto fleet. You need a business license and EIN number to qualify, as well as a D-U-N-S number from Dun & Bradstreet.

You can apply by fax or over the phone. If you need less than $1,000 in credit, you only have to have a business license for approval. For over $1,000, you will need trade and bank references.

If you are just starting out and do not have references, the $1,000 is plenty to get you started building your business credit.

● Uline Shipping Supplies

Uline reports to Dun & Bradstreet and carries shipping boxes, trucks, dollies, janitorial supplies, and more. Since they report to D&B, you have to have a D-U-N-S number before you get started with them. They will also ask you for a bank reference and two other references. Initially, you may need to prepay. After that, they are likely to approve you for Net 30 terms.

Quill is the ultimate starter vendor and a mainstay in the vender credit tier. They sell office supplies as well as cleaning and packaging supplies. Products range from office supplies to office furniture, and even janitorial supplies.

They report to D&B. If you do not already have a D&B score, you will have to place an initial order first. Generally speaking, they establish a 90-day prepay schedule, and if you order each month for three months, they will most often approve you for a Net 30 account.

Once you have a private business loan or two, as well as some starter vendors and other merchants reporting, you need to keep an eye on your credit report. Credit monitoring is vital to the process of building business credit. Mistakes on your report can slow progress significantly. By looking at your credit regularly, you can see which accounts are reporting and ensure that the information being reported is accurate.

There are a few options when it comes to monitoring your business credit. Unlike personal credit monitoring, it isn’t free. However, we can show you how to do it for cheaper than what the credit agencies themselves will offer.

Credit Monitoring with the Big Three

D & B provides Credit Signal, which is a means to track your credit score by having the reports come directly to you, for a price.

Equifax offers a risk monitoring service as well. It is convenient as it enables reports to come directly to you. If you don’t wish to pay for continual reports, you can submit an alternative request for a one-time Equifax report.

Experian provides similar services, with options for continual monitoring or one-time reports.

Prices for individual reports from each vary, with Experian and Equifax costing about $19.99 each. D&B ranges from $49.99 to $99.99.

Save money by monitoring your credit on a regular basis with Credit Suite. We can help you monitor business credit at Experian and D&B for only $24/month. See: www.creditsuite.com/monitoring.

If there are inaccuracies in the credit information, you need to dispute them. Errors in your credit report(s) can be fixed. However, credit agencies normally want you to dispute in a particular way.

Disputing credit report mistakes generally means you send a paper letter with duplicates of any supporting documents like receipts or cancelled checks. Never mail the original copies.

You Can Build and Improve Business Credit with Private Business Loans

Private business loans can definitely help you build business credit. However, you must choose lenders that will report your payments to at least one business credit agency. There are more that what we have listed. Be sure to do your own research to find the best options for your business.

Private business loans are just one tool to help you build business credit. There are many tools that you can stick in your tool box that will help you along the way. The vendor credit tier is one, but you can also ask those providers that you already make payments to if they will report. This can help you build business credit even faster.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.