How to Open a Successful Business in the Digital Age

Are you looking to open a business but don’t know where to start? The digital age has changed the entire scope of doing business, from getting licenses, getting clients, and selling products or services, all of which happens online. Regardless of the type of business you wish to open, having a digital presence is the key to survival. Here are some tips on how to open a successful business in the digital age.

You Cannot Ignore Technology When Looking at How to Open a Successful Business

Even if you run a convenience store where people will find you no matter what, you still have to embrace the digital era. While opening a business may be a straightforward thing, not all are able to do it correctly.

You may have all the relevant tools and software to help run the business at your disposal, but still fail to get it right. So how does one become successful in this digital era? This post will take you through all that you need to know on how to open a successful business.

Things to Know About How to Open a Successful Business Before You Start

So, have you settled on starting a business? That’s great, but as you know, things have changed over the last couple of years. If you want a smooth entry, there are a few things that you ought to know beforehand about how to open a successful business.

Demolish your funding problems with 27 killer ways to get cash for your business.

Everything is Now on the InternetThe internet is much more important to how to open a successful business than it used to be. Approximately 53% of shoppers will research on Google to find more information regarding the product or services that they wish to purchase. This includes finding more about the vendor by looking for reviews online.

These numbers are a great eye-opener; hence, the need to have an online presence if you wish to be found by prospects.

The best way around this is to invest in a good website, have an active social media presence, and a good PR strategy.

There’s a crucial aspect you must consider when it comes to websites: Search Engine Optimization (SEO). This is a way of making your website search engine-friendly, making it easier to be found online by ranking higher in the Search Engine Result Pages (SERPs). There are many factors to consider when it comes to SEO, such as technical SEO, On-page SEO, and off-page SEO. In a nutshell, once you have a business website, you are not there yet. You still need to optimize it for search engines.

The other crucial thing to know is that almost everyone is now on social media, and you can leverage this platform to boost your business. Some of the ways to effectively utilize social media include:

- Create brand awareness

- Engage with your audience

- Respond much faster to customer inquiries and concerns

- Promote your products or services

- Instil trust about your brand in your target audience.

You need to choose social media platform that resonates best with your business and invest more resources to help grow your audience and engage the current ones.

Digital PR involves getting reviews from third-party websites, independent reviewers, and get featured on local listings. This is a great way to boost your online visibility, and people will gain more trust in your business.

Getting Funding

Any business needs starting capital, regardless of how big or small the venture is. You need to conduct extensive research on your business to identify how much you need to be operational. Apart the materials and equipment required, you also need to factor in the labor cost and any unforeseeable miscellaneous expenditure.

Furthermore, depending on where you live, you may need certain licenses so as not to get into trouble with authorities.

Furthermore, you need to factor in a marketing budget. While creating a website and social media pages might not seem expensive, it can be costly. This is especially true when you get a professional to help you manage them. For instance, you may need to hire a web developer, an SEO specialist, and a social media manager who will increase your audience and engagement levels.

One way to reduce these is to learn the trade yourself. You can easily register with some of the best online learning platforms to increase your knowledge.

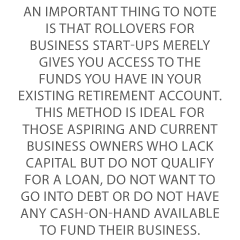

Once you know how much in total you may require for your project, the next step is to identify where to get the funding.

Some of the most effective ways of funding your business are:

Bootstrapping

According to Investopedia, bootstrapping is the act of starting a business with nothing else other than your personal savings. Before you start, have some money in your savings account to get you started. For this to happen, you may plan and save for a while.

Demolish your funding problems with 27 killer ways to get cash for your business.

Venture capitalists

Venture capitalists are individuals that invest in businesses that have potential. You need to reach out to them with a proposal of your venture, indicating the scope of business, the predicted results, and what you need to get the business up and running.

Crowdfunding

Crowdfunding has grown as a popular funding method for upcoming businesses. One can get assistance in various ways, such as getting a loan to start the business, investors, grants, or other people would assure you to purchase your product once ready, to give you enough money to take it to the larger market.

Have Financial Discipline

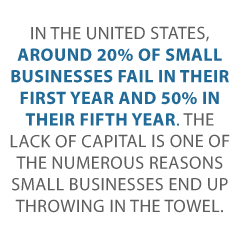

Many businesses fail within their first few months due to mismanagement. This is often a result of financial indiscipline. Before you start making any money, you should have a system in place that will help you take control of your finances and identify business trends. Accounting and bookkeeping are some of the most crucial parts of running a business. This shouldn’t be an afterthought.

With these three tips in mind, you are ready to open up your business. But under the current circumstances with the digital age, you are still not there yet. What’s missing? Here are a few pointers to help you navigate the ever-competitive digital market.

How to Open a Successful Business in the Digital Age

-

Research Your Market

The first thing to do is conduct market research to determine whether your business would make any financial sense. Are the people you wish to sell ready for your product? Have they shown any signs of interest in that particular service? What is the competition like? Are there any businesses of the same type in your area?

Before you settle on any business, you need to find out what other people have to say about it. Do not only rely on the responses of your friends and family. Talk to others also.

-

Identify Your Target Audience

Never get into the market hoping to attract the right people into your business without having pinpointed who you wish to target. What is your product or service? What type of people are likely to purchase more from you? Which group are you likely to convince to buy from you? That is what we call a target audience.

You need to point out the exact type of people you wish to target, as this will help you curate the right products or services. Furthermore, when it comes to digital marketing, you will save yourself a lot of resources when you target a specific group of people rather than generalized marketing. You have better chances at an increased return on investment (ROI) when you take on this route.

-

Conduct Competitor Analysis

Getting into the market without conducting an in-depth competitor analysis is simply gambling with your business. Find out what other companies like yours exist and how they are performing. If they’re doing well, identify their key strengths and see what you can bring to the market to outdo them.

Moreover, if your competition is struggling, find out what you can do differently to ensure that people come to you. Are the people getting valuable services from the competition? Are you willing to offer discounts as you start in a bid to lure more customers? How is the competition handling their online marketing strategies?

Always strive to be better.

Demolish your funding problems with 27 killer ways to get cash for your business.

-

Have a Business Plan

A business plan includes all the details necessary to help you run your business, incorporating every aspect of marketing, sales, and customer retention. You need to highlight what your objectives and goals are beforehand and work towards achieving them.

You also need to set up key performance indicators (KPIs) to help you understand the trends and identify if your business is headed in the right direction. This will help you tweak and change the strategies and your approach towards the business.

-

Embrace Technology

We have already talked about getting a website and an active social media presence to increase your brand visibility online. Still, there are many other ways to embrace technology that will make your operations seamless.

Business automation is the way to go in this digital era, and if you’re stuck handling most of your work manually, then you may sacrifice the revenue. Different businesses require different automation tools and software. Look for any manual tasks that could otherwise get automated to boost your work.

Final words

We hope that our complete guide on how to open a successful business in the digital age will help you get your venture on its feet. Remember that for you to succeed in the digital era, you need to be tech-savvy, understand who your audience is, know what your clients need, keep a close eye on the competition, and of course, have an online presence.

Lidia S. Hovhan is a part of Content and Marketing team at OmnicoreAgency. She contributes articles about how to integrate digital marketing strategy with traditional marketing to help business owners to meet their online goals. You can find really professional insights in her writings.

The post How to Open a Successful Business in the Digital Age appeared first on Credit Suite.