Article URL: https://jobs.lever.co/FinleyTechnologies/70462b30-c31a-4db3-932a-0abb96ec5566

Comments URL: https://news.ycombinator.com/item?id=38355502

Points: 0

# Comments: 0

Article URL: https://jobs.lever.co/FinleyTechnologies/70462b30-c31a-4db3-932a-0abb96ec5566

Comments URL: https://news.ycombinator.com/item?id=38355502

Points: 0

# Comments: 0

Imagine running a retail business without knowing how much you’re paying your wholesaler for goods. Or running a restaurant without looking at the price of your ingredients. Or constructing homes without looking at the price of raw materials… you get the idea. That lack of transparency would be frightening, but hey, things could still work … Continue reading Finley (YC W21) is hiring across all teams to build capital markets software

Imagine running a retail business without knowing how much you’re paying your wholesaler for goods. Or running a restaurant without looking at the price of your ingredients. Or constructing homes without looking at the price of raw materials… you get the idea.

That lack of transparency would be frightening, but hey, things could still work out, right?

Well, let’s up the stakes.

Imagine that, on top of not knowing exactly how much you were paying for your *inputs*, you also didn’t know if you would have consistent and continued *access* to your wholesaler, your food supplier, or your building materials. That would almost certainly induce high blood pressure, stomach ulcers, and mild insomnia.

In the world of private credit (this is basically business credit for *all* companies that aren’t publicly traded behemoths or small businesses), it’s not only normal but *expected* that getting and maintaining access to debt capital (one of the key inputs for running any business!) will be opaque, error-prone, and hard to operationalize. In other words, supply chain uncertainty is the dismal reality in middle-market finance.

Private credit is enormous (add up all the VC dollars spent last year and you’d still be short of the amount of private credit issued over the same period), unavoidable, and broken.

That means credit access–the fuel or primary *financial input* for most medium-sized businesses–is hard to price, access, report on, and predict.

And yet it doesn’t have to be that way; the data and operational issues of private credit have been solved in other domains (e.g., CRMs for Sales, infrastructure tooling for devs, EMRs for hospitals). What’s missing is a software layer for business finance.

Finley has built the system of record for private credit. We plug into all borrower source systems and automate reporting and analysis for private credit lenders. The result is full transparency into the *cost* and *availability* of capital.

We’re a team of builders, designers, finance experts, engineers, and systems thinkers from top companies in finance and technology, and we’re backed by leading investors like Y Combinator and Bain Capital Ventures.

We’re two years into our journey and our software helps companies manage over $3 billion in private credit, but it’s still Day 1.

The challenges we’re taking on will reshape the economy over the next decade, and we’d love to partner with team members who share our passion for innovation and company-building.

To learn more, check out our Careers page here: https://www.finleycms.com/careers/

Comments URL: https://news.ycombinator.com/item?id=33707952

Points: 1

# Comments: 0

Digital Currency Group, the cryptocurrency conglomerate that owns Genesis Global Trading, is the biggest creditor of the beleaguered hedge fund, according to court documents. The post Genesis Lent $2.4 Billion to Hedge Fund Three Arrows Capital first appeared on Online Web Store Site.

Article URL: https://www.finleycms.com/careers/ Comments URL: https://news.ycombinator.com/item?id=28229152 Points: 1 # Comments: 0 The post Finley (YC W21) is hiring fintech experts to transform debt capital management appeared first on Get Funding For Your Business And Ventures. The post Finley (YC W21) is hiring fintech experts to transform debt capital management appeared first on Buy It At … Continue reading Finley (YC W21) is hiring fintech experts to transform debt capital management

The world of business involves many risk-taking attempts. Business owners experience numerous obstacles from the moment they plan and start their business to maintain it and make sure it grows. From developing your business ideas to looking for qualified people to hop on board your venture, starting a business takes a lot of courage, patience, and knowledge. Financing via a 401k could be an avenue you haven’t thought of.

All businesses face different kinds of hurdles and challenges in the process of starting and growing their venture. The Small Business and Trade Alliance conducted the Small Business Trends survey on over 2,400 current and aspiring business owners in the United States. This survey included questions about their current biggest obstacles as business owners.

Although the pandemic, without a doubt, can be considered one of the greatest challenges of 2020, the survey also contained questions about non-pandemic-related challenges. Among these top challenges include recruiting and retaining employees, marketing and advertising, time management, administrative work, and managing and providing benefits. The number one challenge, at 23%, however, is the lack of capital or cash flow.

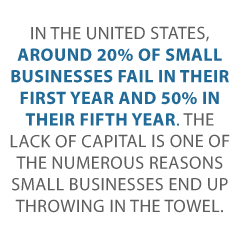

In the United States, around 20% of small businesses fail in their first year and 50% in their fifth year. The lack of capital is one of the numerous reasons small businesses end up throwing in the towel.

Business owners are usually thoroughly aware of and keep a close watch on how much money is needed to keep the company or the business going. It includes expenses such as daily spending, payroll funding, paying fixed and varied overhead expenses like rent and utilities, and payments for external vendors or suppliers. They also make sure to explore various and alternative investment strategies as a way to increase their funds.

On the other hand, business owners who do not closely monitor expenses and revenue generated from sales of products or services are more likely to fail than succeed. In addition, it can lead to inadequate funding, which could ultimately put the business out of operation.

With this, it is critical for aspiring and current business owners to be in tune with the financial state of their business. Financial challenges and hurdles are inevitable and are part of the business process. However, business owners must explore various ways to fund their venture. There are several ways to get financing for your business. Getting business loans is one of the most common methods to do this.

Another way to solve your business’ lack of capital is to consider 401(k) financing. What is 401(k) financing? First, this article will discuss what 401(k) financing is and how it works. Next, it will tell you more about how 401(k) financing can solve your business’ lack of capital and, lastly, the benefits and possible risks that come with it.

Demolish your funding problems with 27 killer ways to get cash for your business.

401(k) business financing is one way your small business can solve its lack of capital. Also referred to as Rollovers for Business Start-Ups (ROBS), 401(k) business financing is a small business financing method. This method allows you to withdraw money from your retirement account to start or fund your business without having to pay a tax penalty or an early withdrawal fee.

401(k) business financing is one way your small business can solve its lack of capital. Also referred to as Rollovers for Business Start-Ups (ROBS), 401(k) business financing is a small business financing method. This method allows you to withdraw money from your retirement account to start or fund your business without having to pay a tax penalty or an early withdrawal fee.

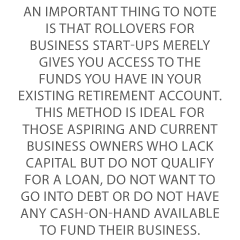

An important thing to note is that Rollovers for Business Start-Ups merely gives you access to the funds you have in your existing retirement account. This method is ideal for those aspiring and current business owners who lack capital but do not qualify for a loan, do not want to go into debt or do not have any cash-on-hand available to fund their business. This method does not consider your credit score, on-hand collateral, or past experiences to qualify for it. The main components of this method would be the retirement account you have. Such as a 401(k) or an Individual Retirement Account (IRA), and the amount of money you have in it.

Demolish your funding problems with 27 killer ways to get cash for your business.

In 401(k) business financing, your retirement plan serves as your investor. To access these funds without having to pay a tax penalty for early withdrawal fees, it is critical to, first and foremost, establish a ROBS (Rollover Business Start-Ups). This structure consists of several components which must adhere to certain requirements for compliance with the Internal Revenue Service, or IRS—the federal agency responsible for overseeing, administering, and collecting taxes.

The first step would be to establish a C corporation, also known as a regular corporation. It is the only entity type allowed to sell shares to a retirement account and within the ROBS structure. In this way, it will help release your business’s funds.

Next, put together a retirement plan for your new business. Although there are other options such as profit sharing and defined benefits, most business owners opt for the standard 401k. You will need a custodian to manage the investments in the plan and have the responsibility to keep records, administer the plan, and modify its investments the way you deem fit.

After this, roll your existing retirement funds from your plan into the new retirement plan under the C corporation. Since the funds have already been rolled over to the company retirement plan, the plan then buys stock in the C corporation through a QES transaction or a Qualified Employer Securities transaction. Thus, it is the step wherein the money is rolled over and made available for the business to use.

The first step is essential since you would not be able to do a QES transaction without it. Finally, once the QES transaction is finished, your retirement funds can now be accessed by the corporation. You can use them to solve your business’s lack of capital. Or you can pay off the pending expenses you may have.

401(k) financing, also known as ROBS or Rollover Business Start-Ups, offers numerous benefits for aspiring and current business owners alike. This financing technique may come off as complex. Still, it is one of the ways to solve your business’ lack of capital. Here are some of the benefits of 401(k) business financing:

In 401(k) financing, you have control over your retirement funds. It allows you to support your business and make it grow financially. Through this, your business has the potential to earn a significant return with tax-deferred growth.

Most loans require monthly payments, which may eventually turn into debt. Unlike most loans, 401(k) financing gives you the ability to use the funds you already have. In addition, since 401(k) financing does not require you to pay interest, it helps reduce your day-to-day costs and other operating expenses you may have.

The only requirement of 401(k) financing is a qualified retirement account. You will not need to put up a down payment or sign over a property to receive the funds. This is unlike most financing methods that will require you to do so.

Since 401(k) financing is not considered a loan, a credit check is not included in its requirements. With this, no evaluation will occur, and you can proceed with 401(k) business financing even if you have a low credit score, as long as you have a retirement plan.

The funds in your 401(k) plan may also be used as a down payment for your small business loan (SBA). Reducing debt is considered to be one of the top benefits of 401(k) business financing.

Demolish your funding problems with 27 killer ways to get cash for your business.

Aspiring and current business owners are no strangers to the challenges and obstacles of starting up and growing a business. Although these hurdles may be intimidating and sometimes overwhelming, you can overcome them.

One of the top challenges small business owners face, aside from the impact and effects of the pandemic, is the lack of capital. However, this is a matter that you can solve through 401(k) business financing. When done correctly, it helps business owners fund their venture. And it does so without worrying about tax penalties, early withdrawal fees, and falling into debt.

Navigating 401k business financing and how it can help solve your business’ lack of capital can seem intimidating if it is new and unfamiliar to you. However, finding the right company that offers a 401(k) financing program can help ease your worries.

Let Credit Suite help you with that! Credit Suite offers a wide range of programs, from their 401(k) financing program to other business loans and business credit programs. So whether it be a 401(k) financing plan or other business loan and credit programs, Credit Suite has got you and your business covered!

Jill Santos is an early childhood educator and a freelance content writer for The Stock Dork. She is passionate about serving others through research, education, and the arts.

The post How to Solve Your Business’s Lack of Capital with 401k Business Financing appeared first on Credit Suite.

Yellowstone Capital no longer exists! They are now Fundry Capital. We reviewed Fundry Capital, one of several lenders in the online space. They are an ISO (independent sales organization).

We look at the specifics and drill down into the details.

Fundry Capital is located online here: https://fundrycap.com. Their physical address is in Jersey City, NJ. The firm’s location is nowhere on their website. And it was a chore to find it on LinkedIn.

You can call them at: (877) 237-2297. Also, you can contact them at: info@fundrycap.com.

Their About page is simply a part of their home page – and it is none too informative.

In 2015, their predecessor Yellowstone Capital had in a $1.5 million deal which, at the time, was their largest ever deal.

Fundry is also related to Green Capital Credit. See: https://greencapitalcredit.com. There’s not a lot of information on the Green Capital site, and their blog stopped being updated in September. Of which year? It is impossible to tell from that website.

Fundry offers loans for what is called B-F credit. These appear to be sub-prime loans. Appear? It is frustratingly tough to find specifics on Fundry Capital’s offerings.

These are types of alternative, or non-conforming, loans, often for borrowers with poor credit.

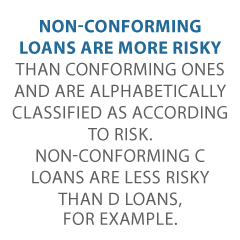

Non-conforming loans are more risky than conforming ones and are alphabetically classified as according to risk. So non-conforming C loans are less risky than D loans, for example.

There are far fewer lenders who want to make non-conforming loans. Hence there is less competition for these borrowers.

This causes interest rates to be higher. Also, most lenders view these borrowers as being riskier and more desperate.

That perception also, understandably, pushes up the interest rates.

Sometimes alternative loans can be seen as predatory. Borrowers in such a situation should always be careful that there are no significant prepayment penalties. Those are common with non-conforming loans, and they can prevent you from refinancing.

This online lender offers merchant cash advances – if you dig deeply into their LinkedIn profile. MCAs are not mentioned anywhere on the Fundry Capital website. They will handle high-risk borrowers. You can get same-day funding for approved merchant cash advances.

Fundry’s fees are nowhere to be found, either on their website or LinkedIn. In addition, the origination fee and APR are not known. This is because their website is not highly informative.

Find out why so many companies use our proven methods to get business loans.

Advantages include fast approvals and acceptance of high-risk borrowers. The company boasts that:

We fund thousands of deals for companies with B-F credit. Found a deal that others say is unfundable? Fundry will get it done.

Disadvantages include a lack of transparency regarding fees, or really anything else. Their website has extraordinarily little information. However, a high-risk borrower may have few other options. Also, any borrowers in these categorizes should know the interest rates will be high.

And this is by definition. So don’t blame Fundry for that.

Given that corporate credit is separate from consumer, it helps to secure an entrepreneur’s personal assets, in case of litigation or business insolvency. Also, with two separate credit scores, a small business owner can get two different cards from the same merchant. This effectively doubles purchasing power.

Another benefit is that even startups can do this. Visiting a bank for a business loan can be a formula for disappointment. But building corporate credit, when done properly, is a plan for success.

Personal credit scores depend on payments but also various other factors like credit utilization percentages. But for company credit, the scores truly just depend on whether a company pays its bills promptly.

Building business credit is a process, and it does not occur automatically. A small business has to actively work to develop company credit. Nevertheless, it can be done readily and quickly, and it is much faster than building individual credit scores.

Merchants are a big component of this process.

Performing the steps out of order will lead to repetitive denials. Nobody can start at the top with small business credit. For instance, you can’t start with store or cash credit from your bank. If you do, you’ll get a denial 100% of the time.

A business has to be genuine to loan providers and merchants. That is why, a small business will need a professional-looking web site and email address, with website hosting from a company such as GoDaddy.

Also business telephone and fax numbers ought to have a listing on ListYourself.net.

Likewise the company phone number should be toll-free (800 exchange or similar).

A business will also need a bank account dedicated solely to it, and it has to have all of the licenses essential for running. These licenses all have to be in the perfect, appropriate name of the corporation, with the same company address and telephone numbers.

So note that this means not just state licenses, but possibly also city licenses.

Visit the IRS website and acquire an EIN for the corporation. They’re totally free. Select a business entity like corporation, LLC, etc.

A small business can begin as a sole proprietor. But they will more than likely want to change to a variety of corporation or partnership to lessen risk and optimize tax benefits.

A business entity will matter when it pertains to taxes and liability in case of litigation. A sole proprietorship means the entrepreneur is it when it comes to liability and tax obligations. No one else is responsible.

If you run a company as a sole proprietor, then at the very least be sure to file for a DBA (‘doing business as’) status.

If you do not, then your personal name is the same as the small business name. Hence, you can end up being directly liable for all business debts.

Additionally, according to the IRS, by having this arrangement there is a 1 in 7 probability of an IRS audit. There is a 1 in 50 possibility for corporations! Prevent confusion and substantially reduce the odds of an IRS audit at the same time.

Find out why so many companies use our proven methods to get business loans.

Begin at the D&B website and get a totally free DUNS number. A DUNS number is how D&B gets a small business into their system, to produce a PAYDEX score. If there is no DUNS number, then there is no record and no PAYDEX score.

Once in D&B’s system, search Equifax and Experian’s websites for the company. You can do this at https://www.creditsuite.com/reports. If there is a record with them, check it for correctness and completeness. If there are no records with them, go to the next step in the process.

In this manner, Experian and Equifax will have something to report on.

First you ought to build trade lines that report. This is also referred to as vendor accounts. Then you’ll have an established credit profile, and you’ll get a business credit score.

And with an established business credit profile and score you can begin obtaining revolving store and cash credit.

These varieties of accounts often tend to be for the things bought all the time, like shipping boxes, outdoor work wear, ink and toner, and office furniture.

But to start with, what is trade credit? These trade lines are credit issuers who will give you starter credit when you have none now. Terms are ordinarily Net 30, instead of revolving.

Hence if you get an approval for $1,000 in vendor credit and use all of it, you need to pay that money back in a set term, such as within 30 days on a Net 30 account.

Net 30 accounts must be paid in full within 30 days. 60 accounts have to be paid in full within 60 days. In comparison with revolving accounts, you have a set time when you have to pay back what you borrowed or the credit you used.

To kick off your business credit profile the right way, you should get approval for vendor accounts that report to the business credit reporting bureaus. As soon as that’s done, you can then make use of the credit.

Then pay back what you used, and the account is on report to Dun & Bradstreet, Experian, or Equifax.

Not every vendor can help like true starter credit can. These are vendors that will grant an approval with hardly any effort. You also want them to be reporting to one or more of the big three CRAs: Dun & Bradstreet, Equifax, and Experian.

Once there are 3 or more vendor trade accounts reporting to at least one of the CRAs, progress to revolving store credit. These are service providers which include Office Depot and Staples.

Use the corporation’s EIN on these credit applications.

Are there more accounts reporting? Then move onto fleet credit. These are businesses such as BP and Conoco. Use this credit to purchase fuel, and repair and maintain vehicles. Make sure to apply using the small business’s EIN.

Have you been responsibly handling the credit you’ve up to this point? Then move to more universal cash credit. These are businesses such as Visa and MasterCard. Keep your SSN off these applications; use your EIN instead.

If you have more trade accounts reporting, then these are doable.

Know what is happening with your credit. Make certain it is being reported and take care of any inaccuracies as soon as possible. Get in the practice of taking a look at credit reports. Dig into the particulars, not just the scores.

We can help you monitor business credit at Experian and D&B for 90% less, here. And update the details if there are mistakes or the details is incomplete.

So, what’s all this monitoring for? It’s to dispute any inaccuracies in your records. Errors in your credit report(s) can be taken care of. But the CRAs generally want you to dispute in a particular way.

Disputing credit report errors normally means you mail a paper letter with duplicates of any proof of payment with it. These are documents like receipts and cancelled checks. Never mail the original copies. Always mail copies and keep the original copies.

Disputing credit report mistakes also means you precisely detail any charges you dispute. Make your dispute letter as crystal clear as possible. Be specific about the issues with your report. Use certified mail so that you will have proof that you sent in your dispute.

Always use credit smartly! Don’t borrow beyond what you can pay off. Monitor balances and deadlines for repayments. Paying off in a timely manner and in full is vital. It will do more to boost business credit scores than nearly anything else.

Building corporate credit pays. Great business credit scores help a small business get loans. Your loan provider knows the business can pay its debts. They recognize the company is authentic.

The small business’s EIN links to high scores. And loan providers won’t feel the need to call for a personal guarantee.

Find out why so many companies use our proven methods to get business loans.

Any business owner should always be wary of funding sources which are not transparent with their fees. Maybe Fundry Capital online lending reveals all once you apply. But why should any business owner have to wait?

Companies which will work best with Fundry are high-risk borrowers. This is because they may have few other options for any loans or other funding.

However, other borrowers should press for more transparency. Or they should be ready to look elsewhere if Fundry is not forthcoming.

Because this should always be basic and easy to find information. No prospective borrower should ever have to glean through a ton of LinkedIn profiles to find the tiniest nugget of information.

And finally, as with every other lender, always read the fine print and do the math. Go over the details with care. Better yet, work with a financial professional with no affiliation with the lender. Decide if this option will be good for you and your company.

In addition, consider alternative financing options that go beyond lending. These are options such as building business credit.

However, only you can best decide how to get the money you need to help your business grow.

The post Fundry Capital Review appeared first on Credit Suite.

Asking questions can be scary. It makes us feel vulnerable. Some feel it’s a sign of weakness. The truth is, you don’t know what you don’t know. What you don’t know, really can hurt you, and the only way to get in the know, is to ask. Here are some things you need to know about capital loans.

This type of loan is a mainstay in the business lending world. However, if you are new to running your own business, you may be confused by some of the terms commonly thrown around.

In the simplest terms, capital refers to the assets of the business that go on the balance sheet. So, capital loans are loans for funds that are to be used to either start a business or be reinvested in a business. This could be for expansion, improvements, and more. Basically, this is money you would spend on those things that go under long-term assets on the balance sheet. It’s money that is to be reinvested in the business, or used to buy an existing business or start a new business.

Working capital is money you use to run your business from day to day. It is still money that is reinvested in the business, but it isn’t used on long-term assets. Rather, the funds go toward the daily ins and outs of running a business, like payroll, utilities expense, and more.

Credit Line Hybrid Financing: Get up to $150,000 in financing so your business can thrive.

Now that you understand the difference, you may be asking yourself which you need. Do you need capital loans or working capital? I imagine the gears are turning in your head right now trying to figure it out. If you want startup capital, or if you need to invest in something big, you need capital loans. If you need funds to handle regular expenses, that means you need working capital. Sometimes this is easy to determine, but sometimes it isn’t so cut and dry.

That depends on how bad your credit is. If it’s above 680, Small Business Administration loan programs may be an option. Try these to start:

Here are some options The Small Business Administration offers for capital loans and working capital.

This is arguably the most popular of the SBA loan programs out there. Mainly, this is because it offers federally funded term loans up to $5 million. The funds can be used for a number of things including expansion, purchasing equipment, working capital and more. Banks, credit unions, and other specialized institutions, in partnership with the SBA, process these loans and disburse the funds.

The minimum credit score to qualify is 680. That’s not exactly a bad credit score, but is it less than what you need to get most traditional loans without an SBA guarantee. Also, there is a required down payment of at least 10% for the purchase of a business, commercial real estate, or equipment. Lastly, the minimum time in business is 2 years. In the case of startups, business experience equivalent to two years will do the trick.

Funds are available for a wide variety of projects, including capital projects.

These loans are available up to $5 million. They can be used to buy machinery, facilities, or land. These are all capital projects. Private sector lenders or nonprofits process and disburse these loans. They especially work well for commercial real estate purchases.

Terms for 504 Loans range from 10 to 20 years. Unfortunately, funding can take from 30 to 90 days. They require a minimum credit score of 680, and collateral is the asset the loan is financing. Furthermore, there is a down payment requirement of 10%, which can increase to 15% for a new business.

Also, you be in business for at least 2 years, or management must have equivalent experience if the business is a startup.

There are 4 distinct CAPLine programs offered by the SBA. They differ mostly in the expenses they can fund. These CAPLInes are designed to help businesses meet short-term or cyclical working capital needs. Each of them goes up to $5 million. Furthermore, the interest rate for each ranges from 7% to 10%. Again, funding can take 45 to 90 days.

The four different programs are:

This is financing for businesses preparing for a seasonal increase in sales.

Financing for businesses that need funding to fill a contract.

Financing for businesses taking on a real estate or construction project.

Financing for businesses that are struggling with a short-term slump in sales.

The minimum credit score to qualify for these is also 680. However, there is no minimum time in business requirement unless you are getting a seasonal CAPLine. You have to be in business at least one year to get that one.

Private lenders are another option for capital loans and working capital if your credit isn’t the best.

Upstart is an innovative online lender. The company itself questions the ability of financial information and FICO on their own to determine the true risk of lending to a specific borrower. Instead, they choose to use a combination of artificial intelligence (AI) and machine learning to gather alternative data. They then use this data to help them make credit decisions.

This alternative data can include such things as mobile phone bills, rent, deposits, withdrawals, and even other information less directly tied to finances. The software they use learns and improves on its own. You can use their online quote tool to play with different amounts and terms to see the various interest rate possibilities. Typically, business loans are available ranging from $1,000 to $50,000.

To be eligible for a loan with Upstart, you must meet the following qualifications:

Founded in 2008 by college roommates, online lender Fora Financial now funds more than $1.3 million in working capital around the United States. There is no minimum credit score, and there is an early repayment discount if you qualify.

The minimum loan amount is $5,000 and the maximum is $500,000. The business must be at least 6 months in operation and the monthly revenue has to be $12,000 or more. There can be no open bankruptcies.

Popular online lender Lending Club offers term loans. Business loans from $5,000 to $300,000. The loan terms are 1 to 5 years. You can get a quote in less than 5 minutes. Funds are available in as little as 48 hours if approved. There are no prepayment penalties. Annual Revenue must be $75,000 or more, and you must be in business for at least 2 years. Also, a personal FICO score of at least 620 is necessary.

Quarter Spot is an online lender that offers short term loans. $5,000 to $150,000 is available.

Your company must have annual revenue of $200,000 or more, and there is no fee to apply.

The minimum time in business is 12 months. There is a required minimum average bank balance of $20,000, and you have to show a minimum of $16,000 in monthly sales. The borrower must own at least 50% of the business as well.

OnDeck offers short term loans and lines of credit. For short term loans, amounts are available from $5,000 to $250,000 with terms of 3 to 24 months.

Credit Line Hybrid Financing: Get up to $150,000 in financing so your business can thrive.

You must have annual revenue of $100,000 or more. In addition, your personal FICO Score has to be 600 or better. In addition, there is a time in business requirement of at least 3 years.

Kiva

Kiva is an online lender that is a little different. For example, the interest rate is 0%, so even though you have to pay it back it is absolutely free money. They don’t even check your credit. However, there is one catch. You have to get at least 5 family members or friends to throw some money in the pot as well. In addition, you have to pitch in a $25 loan to another business on the platform.

Yes, there are. One of the newest options out there today is the credit line hybrid. A credit line hybrid is basically revolving, unsecured financing. It allows you to fund your business without putting up collateral, and you only pay back what you use.

You do need good personal credit. Your personal credit score should be at least 685. This is lower than what is required for many traditional loans, especially for the lower interest rate options.

In addition, you can’t have any liens, judgments, bankruptcies or late payments. Furthermore, in the past 6 months you should have less than 5 credit inquiries, and you should have less than a 45% balance on all business and personal credit cards. It’s also preferred that you have established business credit as well as personal credit.

If you do not meet all of the requirements, don’t sweat it. You can take on a credit partner that meets each of these requirements. Many business owners work with a friend or relative to fund their business. If a relative or a friend meets all of these requirements, they can partner with you to allow you to tap into their credit to access funding.

There are many benefits to using a credit line hybrid. First, it is unsecured, meaning you do not have to have any collateral to put up. Next, the funding is “no-doc.” This means you do not have to provide any bank statements or financials.

Not only that, but typically approval is up to 5x that of the highest credit limit on the personal credit report. Additionally, often you can get interest rates as low as 0% for the first few months, allowing you to put that savings back into your business.

The process is quick, especially with an expert guide to walk you through it. One other benefit is, with the approval for multiple credit cards, competition is created. This makes it easier, and likely even if you handle the credit responsibly, that you can get interest rates lowered and limits raised every few months.

A credit line hybrid can work well as either a straight capital loan or for working capital. Once you have it, you can use it as needed for whatever opportunities come your way.

There is more to eligibility than credit score. The key to eligibility for capital loans is to have overall fundability. What’s that? In short, it’s the ability of your business to get funding. It encompasses so many things however, it can be hard to get your arms around.

One thing that doesn’t change is, the first step in having a fundable business is in how you set that business up. For example, you shouldn’t use your own phone number and address. Your business needs a separate phone number and address. You also need to get an EIN to use on credit applications rather than using your SSN to apply for credit.

Credit Line Hybrid Financing: Get up to $150,000 in financing so your business can thrive.

A separate, dedicated bank account is another must when it comes to fundability. Even more important, you must incorporate. That’s non-negotiable. It is necessary to separate your business from yourself personally and it helps your business gain more credibility with lenders as one that is legitimate. This is just a taste of what can affect fundability. There is so much more.

Sometimes, you don’t know what you don’t know. Maybe some of these are questions you never thought to ask. Applying for loans can be daunting, especially when you feel like you will never qualify. These options for capital loans can help, and in the meantime, work on fundability. With strong fundability, your business will never be without the funding it needs to survive and thrive.

The post Everything You Wanted to Know About Capital Loans and Were Too Embarrassed to Ask appeared first on Credit Suite.

PayPal Working Capital is a funding option offered through the PayPal online payment service. What do they offer? Are they a good option for you? Let’s find out.

If it is a good fit, PayPal Working Capital can help you run and grow your business. However, it isn’t right for everyone. The product is solid, but there are some major drawbacks that make it perfect for some, and not so much for others.

PayPal Working Capital has a physical address at:

2211 North First Street

San Jose, California 95131.

San Jose is the home of PayPal Working Capital’s corporate headquarters.

You can call them at: (888) 221-1161. Their contact page is here: https://www.paypal.com/us/selfhelp/home. They have been in business since 1998 but that is actually how long PayPal itself has been in business.

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

PayPal offers flexible payments with a fixed fee and no credit check. The reason they can offer no credit check is that they use your PayPal business transactions as the basis for approval. The amount of your loan and fees are all dependent on the amount of you take in each year through PayPal. In addition, your loan is repaid as an automatic deduction of collections through PayPal, so as long as you are collecting money through PayPal, they will get their money.

The maximum loan amount can be up to 30% of annual PayPal sales, and no more than $97,000 for a first loan. The third loan can be up to $125,000. Your business can get funding in minutes and there is no early payment penalty.

You must have a PayPal Business or Premier account for 3 months or longer to qualify. You also have to process more than $20,000 in annual PayPal sales if you have a Premier PayPal account. A regular business PayPal account only requires $15,000 annually to be eligible.

Automatic repayments are deducted as a percentage of each PayPal sale. The fee is based on your business’s PayPal sales history, your loan amount, and the repayment percentage chosen. A higher payment percentage will lower the fee.

You can use their calculator tool to get an idea of what fees might look like with different repayment percentages. It can also help you get a feel for how everything works. You do have to pay a minimum amount over a 90-day period, which PayPal claims is easily met by most out of the daily sales percentage. However, if there were a 90-day period where you were not able to hit the minimum out of sales, you can log on and make a payment.

Keep in mind, you get to choose what percentage of sales is taken as repayment. The calculator will show you several options, but the larger the percentage the lower the fees. The website offers these examples:

For those with steady, reliable PayPal sales, this is a great option. Keep in mind however, the amount you are eligible to borrow will be limited by your PayPal sales amounts. If you make sales via other platforms, that revenue will not be included in the decisions making process.

One of the top reasons why business owners use PayPal Working Capital is that there is no credit check. If credit is an issue, it’s time to get to work so you can have more funding options. Credit isn’t the only thing you have to work on however. It is possible the complete fundability of your business needs work.

Fundability is the ability of your business to get funding. It is affected by many variables, only one of which is business credit. The better your fundability, the more funding options you will have.

What affects the fundability of your business? The answer isn’t hard, but it is kind of long. Sure, a great business credit score is important, but there are so many more pieces to the puzzle.

The key is, a potential creditor needs to see that your business is legitimate and profitable. Many loan applications are denied approval due to fraud concerns. Others, simply because something didn’t match up and threw up a red flag. Maybe the addresses or phone numbers didn’t match on a couple of reports and it just looks unprofessional. Business credit just isn’t the whole story.

If you understand what fundability is and how to get it, you can open up a world of funding options you never had before.

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

The foundation of fundability is in how your business is set up. It has to be set up to appear to be a fundable entity separate from you, the owner. How do you accomplish this? Well, like any foundation, it is best to start at the beginning. It will be faster and easier if you do. However, if your business is already up and running, then you may not have that option. That’s okay, it’s never too late to start, but start now. For several reasons, the longer you wait the harder it will be. Here is what it takes to build a fundable foundation.

The first step in setting up a foundation of fundability is to ensure your business has its own phone number, fax number, and address. That doesn’t mean you have to get a separate phone line, or even a separate location. You can still run your business from your home or on your computer.

You can get a business phone number and fax number easily that will work over the internet instead of phone lines. Also, the phone number will forward to any phone you want it too so you can simply use your personal cell phone or landline if you want. Whenever someone calls your business number it will ring straight to you.

The next thing you need to do is get an EIN for your business. This is an identifying number that works in a way similar to how your SSN works for you personally. You can get one for free from the IRS.

Incorporating your business as an LLC, S-corp, or corporation is necessary to fundability. It lends credence to your business as one that is legitimate. It also offers some protection from liability.

Which option you choose does not matter as much for fundability as it does for your budget and needs for liability protection. The best thing to do is talk to your attorney or a tax professional. What is going to happen is that you are going to lose the time in business that you have. When you incorporate, you become a new entity. You basically have to start over. You’ll also lose any positive payment history you may have accumulated, so the sooner you incorporate, the better.

You have to open a separate, dedicated business bank account. There are a few reasons for this. First, it will help you keep track of business finances. It will also help you keep them separate from personal finances for tax purposes.

However, there are also several types of funding you cannot get without a business bank account. Many lenders and credit cards want to see one with a minimum average balance. In addition, you cannot get a merchant account without a business account at a bank. That means, you cannot take credit card payments. Studies show consumers tend to spend more when they can pay by credit card.

Fundability also includes being a legitimate business. For a business to be legitimate it has to have all of the necessary licenses it needs to run. If it doesn’t, red flags will go up. Do the research you need to do to make sure you have all of the licenses necessary to legitimately run your business at the federal, state, and local levels.

A business website can affect your ability to get funding. These days, you do not exist if you do not have a website.

Spend the time and money necessary to ensure your website is professionally designed and works well. Pay for hosting also. Don’t use a free hosting service. Along these same lines, your business needs a dedicated business email address. Make sure it has the same URL as your Website. Don’t use a free service such as Yahoo or Gmail.

In addition to having a fundable foundation, you need these pieces to complete the fundability puzzle and have the complete picture.

Your business credit report also affects fundability. That is the credit report, much like your consumer credit report, that details the credit history of your business. It is a tool to help lenders determine how credit worthy your business is.

Where do business credit reports come from? There are a lot of different places, but the main ones are Dun & Bradstreet, Experian, Equifax, and FICO SBSS. Since you have no way of knowing which one your lender will choose, you need to make sure all of these reports are up to date and accurate.

In addition to the business credit reporting agencies that directly calculate and issue credit reports, there are other business data agencies that affect those reports indirectly. Two examples of this are LexisNexis and The Small Business Finance Exchange. These two agencies gather data from a variety of sources, including public records. This means they could even have access to information relating to automobile accidents and liens. While you may not be able to access or change the data the agencies have on your business, you can ensure that any new information they receive is positive. Enough positive information can help counteract any negative information from the past.

In addition to the EIN, there are identifying numbers that go along with your business credit reports. You need to be aware that these numbers exist. Some of them are simply assigned by the agency, like the Experian BIN. One, however, you have to apply to get. It is absolutely necessary that you do this.

Dun & Bradstreet is the largest and most commonly used business credit reporting agency. Every credit file in their database has a D-U-N-S number. To get a D-U-N-S number, you have to apply for one through the D&B website.

Your credit history has everything to do with everything related to your credit score, which is a huge factor in the fundability of your business.

Your credit history consists of a number of things including:

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

The more accounts you have reporting on-time payments, the stronger your credit score will be.

On the surface, it seems obvious that all of your business information should be the same across the board everywhere you use it. However, when you start changing things up, like adding a business phone number and address or incorporating, you may find that some things slip through the cracks.

This is a problem because a ton of loan applications are turned down each year due to fraud concerns simply because things do not match up. Maybe your business licenses have your personal address but now you have a business address. You have to change it. Perhaps some of your credit accounts have a slightly different name or a different phone number listed than what is on your loan application. Do your insurances all have the correct information?

The key to this piece of the business fundability is to monitor your reports frequently.

This encompasses a broad spectrum of things. First, there is the obvious. Both your personal and business tax returns need to be in order. Not only that, but you need to be paying your taxes, both business and personal.

It is best to have an accounting professional prepare regular financial statements for your business. Having an accountant’s name on financial statements lends credence to the legitimacy of your business. If you cannot afford this monthly or quarterly, at least have professional statements prepared annually. Then, they are at the ready whenever you need to apply for a loan.

Often tax returns for the previous three years will suffice. Get a tax professional to prepare them. This is the bare minimum you will need. Other information lenders may ask for include check stubs and bank statements, among other things.

Bureaus

There are several other agencies that hold information related to your personal finances that you need to know about. Everyone knows about FICO. Your personal FICO score needs to be as strong as possible. It really can affect business fundability and almost all traditional lenders will look at personal credit in addition to business credit.

In addition to FICO reporting personal credit, you have ChexSystems. In the simplest terms, this keeps up with bad check activity and makes a difference when it comes to your bank score. If you have too many bad checks, you will not be able to open a bank account. That will cause serious fundability issues.

For this point, everything comes into play. Have you ever been convicted of a crime? Do you have a bankruptcy or short sell on your record? How about liens or UCC filings? All of this can and will play into the fundability of your business.

Your personal credit score from Experian, Equifax, and Transunion all make a difference. You have to have your personal credit in order because it will definitely affect the fundability of your business. If it isn’t great right now, get to work on it. The number one way to get a strong personal credit score or improve a weak one is to make payments consistently on time.

Also, make sure you monitor your personal credit regularly to ensure mistakes are corrected and that there are no fraudulent accounts being reported.

So much plays into this that you may not even think about. First, consider the timing of the application. Is your business currently fundable? If not, do some work first to increase fundability. Next, ensure that your business name, business address, and ownership status are all verifiable. Lenders will check into it. Lastly, make sure you choose the right lending product for your business and your needs. Do you need a traditional loan or a line of credit? Would a working capital loan or expansion loan work best for your needs? Choosing the right product can make all the difference.

The more options you have, the better. If you do a ton of business on PayPal, then PayPal Working Capital is a completely legitimate option. However, regardless, it is best to ensure your overall fundability is in order so you can have as many funding options as possible.

The post PayPal Working Capital Review: Will It Work for You? appeared first on Credit Suite.

The COVID-19 pandemic caught the world by surprise and turned the economy upside down. If you are a business trying to make it during this time, we can help. The Federal government has approved funding through The CARES Act, including the Paycheck Protection Plan. In addition, many states and local organizations are offering their own COVID-19 relief options. If you need funds fast, keep reading for ways to get fast working capital in a recession.

If you are drowning, you need help fast. There is no time to learn how to swim if you don’t already know. You can’t learn how to float in a heartbeat. You need a life preserver. The same is true if you find yourself in need of fast working capital in a recession. You can’t learn to swim at that point. You need immediate help, and once you are safe, then you can focus on longer term solutions.

However, fast working capital in a recession isn’t easy to come by. In fact, it can seem nearly impossible. There is hope though. You can escape from the recession storm, but it is going to take a lot of work. If you move in the right direction and grab the life preserver, I am about to toss you, survival is possible.

While the goal is to never get back into that kind of danger again, you have to actually get out of the water alive first. Here’s how.

Not only is invoice factoring the fastest way to cash, it is also an option that depends very little on your credit, personal or business. In fact, sometimes there isn’t even a minimum credit requirement. They may pull a credit score, but they make decisions based more upon the strength of your invoices.

The lender will gather information to help them determine the likelihood of the invoices being repaid. If they find that the invoices are strong, they will lend money based on the total amount of the invoices minus a premium. The borrower can usually either repay the loan or the lender can keep the invoices and collect from them.

Hit the jackpot and weather any recession with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

Here are a couple of options for creditors that offer invoice factoring without a minimum credit score or despite a low credit score.

Fundbox offers invoice financing for amounts less than $100,000. There is no minimum credit score, and there are options for a 12- week or 24-week repayment term.

If you have a larger amount in open invoices, like up to $5 million, you can get invoice financing from BlueVine.

This is very similar to invoice factoring, but the funds are based on average credit card sales. For example, if you average $20,000 in credit card sales per year, a merchant cash advance would allow you to access that cash at a premium.

Here is how it works. If $20,000 is the average, you would get maybe $16,000 of that up from the creditor. Then, they would take a percentage of your credit card sales, usually weekly, until the whole $20,000 was paid off.

It isn’t perfect, but it is definitely fast, and therefore an option for fast working capital in a recession.

If you need really working capital in a recession, invoice factoring or a merchant cash advance is your best bet. Of course, that only works if you have credit cards sales or invoices to factor. Another option, which takes a little more time, is to apply for a working capital loan from an alternative lender.

Some alternative lenders pull a credit report, but they have a low minimum score requirement. For example, Fundbox offers working capital loans to businesses that have been in operation for at least 3 months and have at least $50,000 in revenue. They lend amounts up to $100,000, and there is no credit check

Kabbage offers something similar if you have been in business for at least 1 year and have $50,000 in revenue. They will lend up to $250,000. There is no minimum credit score here either, but most approvals have over 500. You also have to have either a business checking account or use and online payment platform.

Quaterspot will lend up to $250,000 if you have been in business for at least one year and have at least $200,000 in annual revenue. They will do a soft credit pull, but it does not affect your credit. The minimum score is 550.

Even if your personal credit isn’t fabulous, you can get fast working capital in a recession with business credit cards. How? You can do it with your business credit. That is, your business credit score. It is totally separate from your personal credit score.

If you have business credit you can access those cards for fast working capital in a recession if needed. Of course, credit cards are not an ideal source of working capital, but if you need a way out of the waves, they work well as a life preserver.

Hit the jackpot and weather any recession with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

A credit line hybrid is revolving, unsecured financing. It allows you to fund your business without putting up collateral, and you only pay back what you use. It even works for startups.

How hard is it to qualify? It’s probably easier than you think. You do need good personal credit. That is, your personal credit score should be at least 685. In addition, you can’t have any liens, judgments, bankruptcies or late payments. Also, in the past 6 months, you should have less than 5 credit inquiries, and you should have less than a 45% balance on all business and personal credit cards. It’s also preferred that you have established business credit as well as personal credit.

If you do not meet all of the requirements, all is not lost. You can take on a credit partner that meets each of these requirements. Many business owners work with a friend or relative to fund their business. If a relative or a friend meets all of these requirements, they can partner with you to allow you to tap into their credit to access funding.

If you are not in trouble yet, start now establishing and building business credit so that when hard times come, are ready to meet them head on. Even if you are already in trouble, find one of the other options for fast working capital in a recession and go ahead and get busy working on your business credit. You can start at any time, even if you are in the middle of a recession storm. Here’s how.

The first step in getting business credit is to establish your business as a separate entity from yourself. This isn’t hard at any point, but it is a lot easier if you start at the beginning. Start by ensuring your business has its own contact information. It cannot have the same address, telephone number, or email address as you. The telephone number needs to be toll-free, and the email address should have the same URL as your business website. Yes, you need a website. More on that later.

Next, set up your business as a formal corporation. It needs to be either a corporation, S-corp, or LLC. Operating as a sole proprietor or partnership will not suffice for business credit purposes.

After this, you need to apply for two different identifying numbers. The first is an EIN. This is similar to a social security number, but for your business. You can apply for free on the IRS website. After that, you need a DUNS number. This is a number assigned by Dun & Bradstreet, the largest and most often used business credit reporting agency. Apply for it for free on their website.

This not only helps to separate your business from yourself, but it also helps keep business and personal finances separated. It will be easier to track business expenses and income, which is a huge time saver come tax time.

These are vendors that will extend net 30 terms on invoices and report payments to the credit agencies without checking your credit. You may have to make a few initial purchases, and some have a minimum time in business or revenue requirement. Companies in that will do this are the best place to start when it comes to getting payments reporting to establish business credit.

Once you have a few starter vendor accounts reporting you will be able to apply and get approval for other credit cards, which can be a source of fast working capital in a recession. The store cards are the next step. These include credit cards connected to specific retail stores such as Amazon, Best Buy, and Office Depot.

After enough of these are reporting to the credit agencies, you can apply for fleet credit cards. They include cards from Fuelman, WEX, and others that can be used for fuel as well as vehicle repair and maintenance.

Eventually, you will have enough accounts reporting that you can apply for, and get approval for, cards general use credit cards. This is where you can really access significant fast working capital in a recession if necessary. Cards in the cash credit tier include MasterCard and Visa cards that are not attached to a specific store or limited by the type or location of purchase.

Like I said, even if you do not have business credit in place before the recession hits, this process will still work. You can use it at any time, but if you already have business credit in place, it will be easier and faster to use it to access fast working capital in a recession.

Once you are out of the water, don’t get back in until you know how to handle yourself. Learn how to swim, take a survival class, and be prepared.

The way you do this is by establishing and building strong business credit. Not only will this keep you out of choppy water, but it can turn that same churning nightmare into beautifying, relaxing, calm waters.

Here is how you start.

Did you fall overboard or were you pushed? If hard times just sent you flying over the rails and into the churning waves, don’t sweat it. It happens. Just grab a hold of the first floating object you can find, hold on for dear life, and make it through. Use the fast working capital in a recession and you will come out on the other side.

If, however, your peril was caused by foolish decisions, poor planning, or some undiscovered fraud, you are going to have some work to do when you get out. Damage control is in order. Figure out what happened and take steps to ensure it doesn’t happen again.

Hit the jackpot and weather any recession with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

The best way to stay on top of your finances is to understand your financial statements. There is more to it that just revenue, expenses, and assets. Of course you need to understand profit, but learn to look closer. Figure out the real story your financial statements are telling you.

There is a lot to this, but the easiest and quickest way to start is to do a comparison. Take a look at what sales, profit, and expenses looked like at the same time last year, last quarter, and last month. If you see a significant change, look into it. You may find something easily explained, such as an increase in cost or a decline in sales that is standard at that time of the year.

You may, however, find something that is causing a problem. Has a cost increased significantly enough that you need to shop around for a better price? Is there a cash leak that you cannot get your hands around? It could be fraud.

Maybe receivables haven’t turned over at all in a significant amount of time. Consider increasing collection efforts or revisiting the credit policy. Learning how to read your financial statements and understand what they are telling you will help you stay out of the deep end.

Look at your processes. Is there a more efficient way to do things? It isn’t uncommon to find that you need to make some changes during an economic downturn. Maybe you need to adjust the hours you are open or make some staffing changes. Take a fresh look at your pricing model and make any decisions that need to be made.

Whether you turn to invoice factoring, merchant cash advances, working capital loans, or business credit cards, you need to handle the working capital you access during a recession wisely. Make payments consistently on-time, and don’t blow it. It is best to have a plan and a budget in place for the funds before you have it in hand.

The post 4 Lifesaving Ways to Get Fast Working Capital in a Recession appeared first on Credit Suite.