The Top 3 Secured Business Credit Cards

Got Bad Personal Credit or No Business Credit? Secured Business Credit Cards Could be the Answer You’re Looking For

But be aware of what secured business credit cards really are – and what’s a much better alternative to kickstarting a business credit profile.

What Are Secured Business Credit Cards?

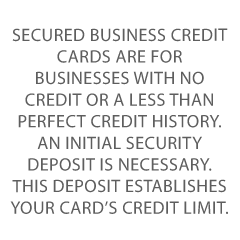

Secured business credit cards are for businesses with no credit or a less than perfect credit history. An initial security deposit is necessary. This deposit establishes your card’s credit limit. Often a minimum deposit of $500 is necessary. Once you start making purchases you get invoices like a regular credit card. But this begs the question: what does it mean when a business credit card is unsecured?

Unsecured Business Credit Cards

An unsecured business credit card works like an unsecured consumer credit card. Credit limits are calculated from many factors, this depends on the card issuer. Factors in deciding credit limit can include personal credit and/or your company’s business credit scores. They can also include time in business, annual revenues, etc. These credit cards can give your business the opportunity to earn incentives and rewards.

What Aren’t Secured Business Credit Cards?

There are a number of types of business credit cards. Some aren’t too different from secured cards. Or they may have some of the same results, where you can get credit when you normally couldn’t, and you may even have the opportunity to build business credit with such cards.

Prepaid Business Credit Cards

A prepaid business card works as a convenient alternative to carrying cash. In this way, it works a lot like a secured credit card. You add funds to your account. And then whatever amount you add is available for purchases. Sounds like a debit card, right?

Business Debit Cards

But, a business debit card is a card that works a lot like a business checkbook. The limit is the amount of funds you currently have in your business checking account. Every time you use it to make a purchase, the amount you charge comes from your account as a deduction

The Difference Between Prepaid and Debit Cards

Prepaid cards and debit cards are both widely accepted at merchants worldwide, but one is preloaded and the other is not. Debit cards are linked to a checking account, while prepaid cards aren’t and instead require you to load money onto the card

Prepaid Cards Versus Secured Credit Cards for Business

Not exactly. The salient difference between secured credit cards and prepaid debit cards has to do with whose money you’re spending when you use the card. With secured credit cards, you spend money borrowed from the credit card company. You pay that money back after the purchase. With prepaid debit cards, you’re spending your (or your business’s) own money. You load money onto the card before the purchase.

Because it involves borrowing and repaying money, a secured credit card can help someone (or a business) build their credit. It can also harm their credit if they don’t use the card responsibly. Prepaid debit cards have no effect on a credit score.

Business Charge Cards

Another, similar-sounding card is a business charge card. A business charge card has all the convenience of a credit card. But it’s without the high price of interest. When using this card you must pay your balance in full each billing cycle.

Since you can’t carry a balance, a charge card doesn’t have a periodic or annual percentage rate. Hence there is no rate for a charge card issuer to disclose. Let’s look at some secured cards for business.

FNBO Business Edition® Secured Visa® Card

With this card, you can, “take control of your credit history and help rebuild your credit”. Request your own credit limit between $2,000 and $100,000, in multiples of $50, when you apply. Your credit limit is subject to credit approval and a security deposit.

Your security deposit is 110% of the amount of your credit limit. And you will earn interest on your security deposit. But there is a $39 annual fee. Pay a variable 20.24% APR on purchases and balance transfers based on the Prime Rate.

Get it here: https://www.fnbo.com/small-business/credit-cards/

Union Bank® Business Secured Visa® Credit Card

With this card, you can, “start building credit for your business”. Get up to a $25,000 secured credit limit. You will pay a 13.99% variable APR on purchases and balance transfers. And pay a 5% balance transfer fee on each transfer, with a minimum of $10.

There is a 25.25% APR for cash advances. And there is a $30 annual fee. Also, Union Bank will demand immediate payment in full, if you use this business credit card for personal, family, or household purposes.

Get it here: https://www.unionbank.com/business/visa-credit-cards-all

Score the best business credit cards for your business. Check out our professional research.

Wells Fargo Business Secured Credit Card

A Wells Fargo business checking or savings account must be open before applying. Upon approval, your funds will be transferred from the deposit account to fund the credit line

Get a $500 to $25,000 credit line, based on the amount of funds deposited by you as security in a collateral account. Pay no annual fee, and no foreign transaction fee.

You can get up to 10 employee cards. Pay prime + 11.90% APR on purchases. And pay prime + 20.74% APR on cash advances. Cash advance or balance transfer fees may apply.

Perks

Choose between Cash Back or Rewards Points. There is no annual rewards program fee. And there are no required spending categories or caps. Earn 1.5% cash back for every $1 spent on net purchases. You can receive cash back automatically as a credit to your account or to your eligible checking or savings account each quarter.

If you choose rewards points, you will earn 1 point for every $1 spent on net purchases. Get 1,000 bonus points when your company spends $1,000 or more in any monthly billing period. Redeem points for gift cards, merchandise, airline tickets and more. Get a 10% points credit when you redeem points online. And you can earn extra bonus points or discounts from Earn More Mall® retailers.

Business Credit Building with the Wells Fargo Business Secured Credit Card

Wells Fargo reports your payment and usage behavior to the Small Business Financial Exchange. Payment and usage activity of the Wells Fargo Business Secured card is not reported to the consumer credit bureaus, therefore it will not help build or rebuild personal credit history.

Wells Fargo will periodically review your account and recent credit history for an opportunity to upgrade to an unsecured business credit card. You may become eligible with responsible use over time. Being able to upgrade to an unsecured business credit card also depends on your FICO score, payment history and ratio of credit card usage to credit limit.

Get it here: https://www.wellsfargo.com/biz/business-credit/credit-cards/secured-card/

Score the best business credit cards for your business. Check out our professional research.

Choosing the Best Secured Business Credit Cards for Your Circumstances

Wells Fargo is the best when it comes to annual fees (it’s hard to beat $0). For the highest possible credit limit, the FNBO Business Edition® Secured Visa® Card comes out on top,

with a $100,000 maximum.

For the best balance transfer rate, it looks like Union Bank® Business Secured Visa® Credit Card is the best. But keep in mind, they do charge a 5% balance transfer fee on each transfer,

with a minimum of $10.

Building Business Credit is a Viable Alternative to Getting Secured Credit Cards for Business

New businesses can get credit from starter vendors, and often there’s no need to pay money to secure a card. Consider CEO Creative and Grainger Industrial Supply. Neither of them require a deposit to secure a card.

Supply Works

Let’s focus on another starter vendor: Supply Works. They are a part of Home Depot, and offer integrated facility maintenance supplies. But they will not accept virtual addresses. They will report to Experian. Terms are Net 30. You can apply online or over the phone.

Qualifying for Supply Works

You will need:

- An entity in good standing with Secretary of State

- EIN number with IRS

- Business address (matching everywhere)

- D-U-N-S number

- Business License (if applicable)

- Business Bank account

- Trade/Bank references

But at least there is no minimal time in business requirement.

Score the best business credit cards for your business. Check out our professional research.

Secured Business Credit Cards: Takeaways

For entrepreneurs just starting out, getting secured business credit cards may seem to be one of the only ways they feel they can get credit. But you can build business credit with starter vendors. Even if you start with lower limits, you often don’t have to secure those cards with a deposit. As a result, starter vendor credit is nearly always a superior alternative to getting secured business credit cards.

The post The Top 3 Secured Business Credit Cards appeared first on Credit Suite.

Mastercard®

Mastercard®