President Biden is preparing to deliver a State of the Union address before a joint session of Congress after again missing his deadline to present spending and national security plans to Congress.

Some Republicans in Congress want to hold Biden and future presidents accountable to the deadline with a simple penalty. No plans on time, no grand speech under a proposal titled the SUBMIT IT Act, short for Send Us Budget Materials & International Tactics In Time.

The Budget and Accounting Act of 1921 – updated several times – requires a president to submit his budget request to Congress no later than the first Monday in February. The National Security Act of 1947 requires the president to submit a national security proposal for the same day. But there is no enforcement mechanism for either, which is where the SUBMIT IT Act could come in.

“President Biden’s budget was due on Feb. 5, yet Congress has seen nothing,” Rep. Buddy Carter, R-Ga., who sponsored the bill, told Fox News Digital.

“This is irresponsible. Until Congress receives the president’s national security strategy and budget, he has no business delivering a State of the Union address,” Carter added.

The SUBMIT IT Act would prohibit House or Senate leadership from inviting the president to address a joint session of Congress until Congress gets both plans.

If passed, the bill would affect the State of the Union going into 2025 and onward. This won’t have any impact on Biden’s State of the Union address this year, scheduled for March 7.

Biden’s tardiness is not unique, as his four immediate predecessors from both parties were also late in getting their plans to Congress – including his likely 2024 Republican opponent, Donald Trump. So, rather than a partisan problem, it’s largely a long-running issue between two branches of government.

Sen. Joni Ernst, R-Iowa, introduced a Senate version.

“If the president is going to be allowed the opportunity to address Congress and the entire nation, he should actually have a plan in place,” Ernst said in a public statement when announcing the Senate version. “At a time when Americans are facing skyrocketing inflation and the world is on fire, we deserve more than just empty rhetoric.”

Biden’s budget proposals in the past three years missed the deadline by 115, 49, and 31 days, respectively, noted Kurt Couchman, a senior fellow in fiscal policy at Americans for Prosperity.

“Over the past several decades, presidents’ budget and defense proposals have been delayed more and more as missed deadlines have become an ever-more common symptom of the breakdown of the budget process,” Couchman said in a public statement supporting the legislation. “Congress and the American people deserve the opportunity to see and evaluate the president’s requests in a timely manner.”

Trump, who was 38 days late in his first year, and his three immediate predecessors missed the budget deadline as well, according to Roll Call. President Barack Obama was late by 98 days in submitting his first budget proposal in 2009, according to a Congressional Research Service report. President George W. Bush was 63 days in his fiscal 2003 plan. In 1993, President Bill Clinton was 66 days late.

The Congressional Research Service report noted the deadline was changed several times. Previously required in January, the most recent adjustment was in 1990, when the deadline was changed to say, “on or after the first Monday in January but not later than the first Monday in February of each year.”

The Constitution requires the president to submit a State of the Union update to Congress, but nothing requires that message to be a speech to a joint session. Every president from Thomas Jefferson through William Howard Taft submitted a written annual message to Congress. In 1913, President Woodrow Wilson broke that tradition with a speech to a joint session of Congress.

The speech to a joint session requires an invitation from congressional leadership, which has typically been a formality.

But in 2019, House Speaker Nancy Pelosi, D-Calif., threatened to withhold an invitation Trump to speak until the partial government shutdown ended. Trump suggested he would deliver the address at an alternative location. The shutdown ended, and Pelosi invited him to speak.

People always ask me the same question about AdWords:

“What’s a ‘good’ cost per click?”

My response back to them is always the same:

“Why do you care?”

See, most people have AdWords wrong. They obsess over the costs.

They know that more and more competitors are advertising on the platform, which drives up prices.

So they’re zeroed-in on how much they’re going to have to spend.

That’s the wrong approach.

Instead, they should be concerned with what they’re going to get back in return.

I know this sounds counterintuitive. However, I almost never worry about the Cost Per Click for keywords.

In fact, I almost always ignore them.

I’m going to show you why CPC’s don’t matter in many cases. I’ll show you how worrying about keyword costs can mislead you time and time again.

Then, I’ll show what you should be analyzing to make sure you’re not leaving tons of money on the table.

Why Cost Per Click Doesn’t Matter (and What to Analyze Instead)

Each year, companies analyze the most expensive keywords in the country.

These are typically competitive phrases in law or insurance and can cost as much $50 for just a single click.

The insane thing is almost none of those clicks will turn into customers immediately.

Instead, they’ll usually opt-into a form, first.

That means you might have to front the bill for 50 or 100 clicks before someone ever converts.

We’re talking thousands of dollars for a single customer.

It makes sense on the surface; CPC ultimately determines how much you need to spend.

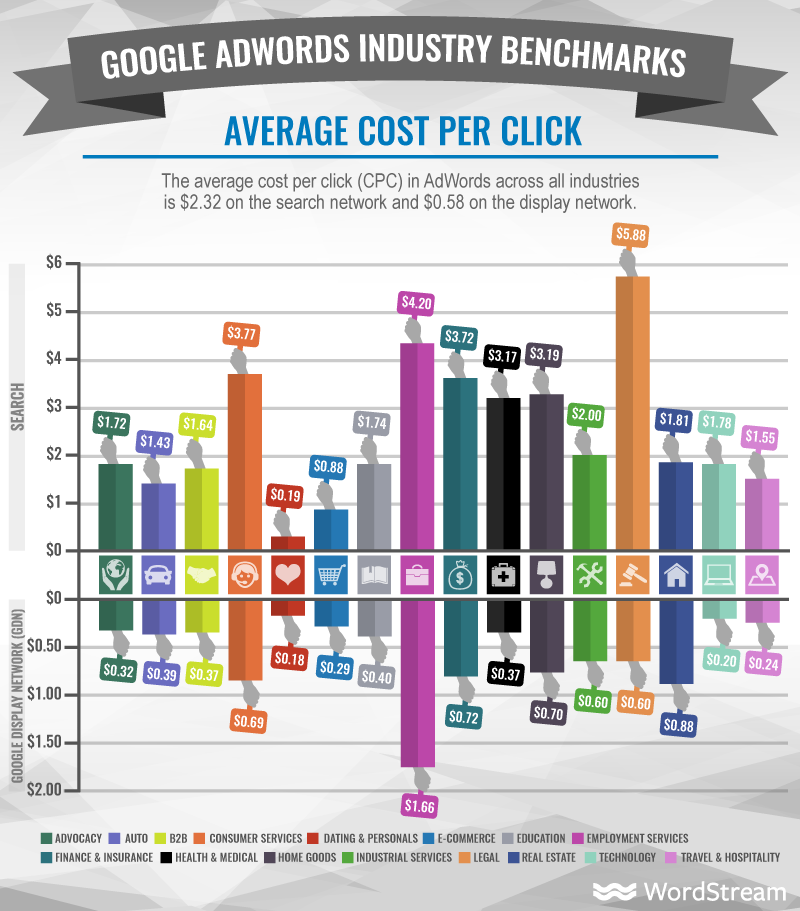

WordStream, for example, always releases an annual update on Cost Per Click benchmarks across industries.

The businesses I own are all software-related. But we work with clients across different industries. So it’s always interesting to look at these cost breakdowns.

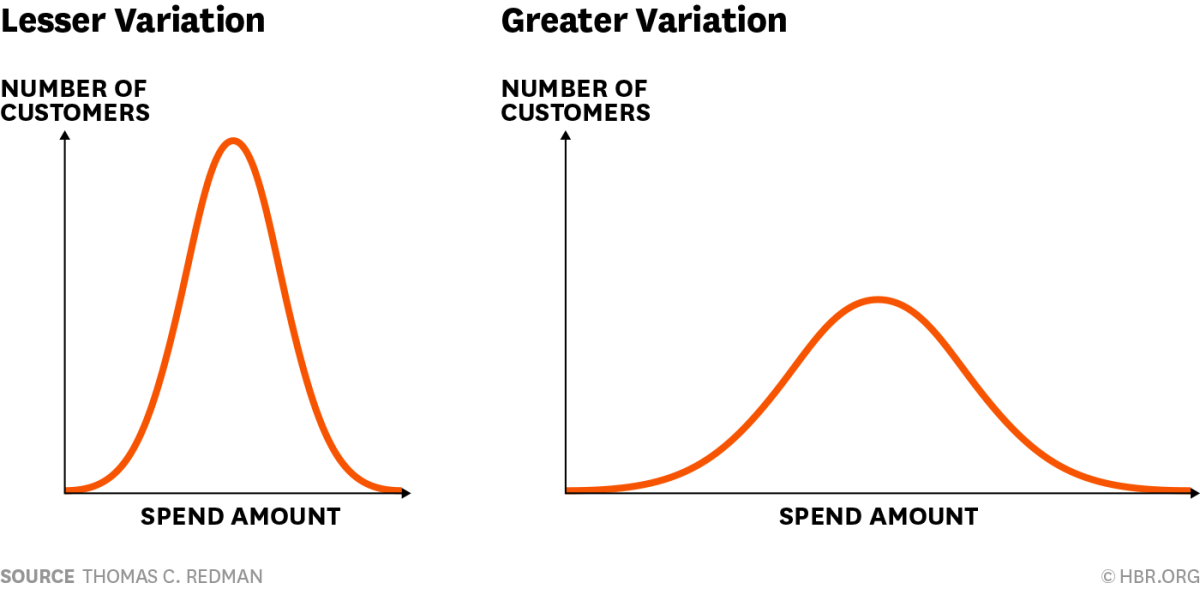

Average ecommerce CPC’s might only be around a dollar, while law might run up to around six dollars (these are higher than most Bing Shopping campaigns, which should be considered for e-commerce businesses as well).

To be honest, though, I don’t obsess over costs, alone.

The first reason comes down to what the study says at the top: Averages.

Average CPCs don’t really mean all that much.

Popular, generic terms aren’t usually all that expensive.

Only a tiny percentage of the people who ever click on those will convert. Whereas, a more commercial long-tail keyword will be incredibly expensive.

Just compare the difference in costs between “tax” and “file back taxes”:

See? It’s not even close.

That makes it hard to use a standard, “industry average benchmark” for any in-depth analysis.

There’s another reason why I don’t like to just look at costs — because you’re often forgetting the other side of the equation.

Conversions ultimately have a much bigger impact than costs.

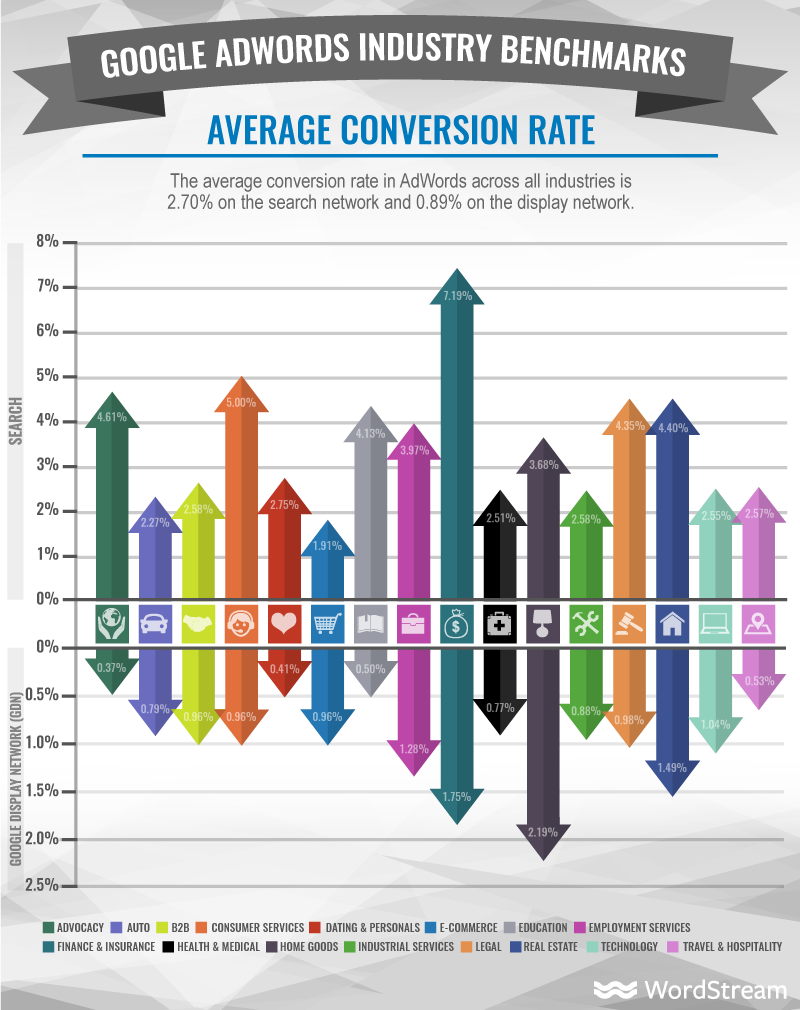

If you remember, the industry average CPC for ecommerce was only around a dollar. In fact, it was one of cheapest CPC’s on the entire list.

But if you now look at the average conversion rates, you’ll see why.

Their conversion rates are also among the lowest.

What does it matter if CPCs are ‘inexpensive’ if the conversions are equally low?

That’s why you often want to look at the Cost Per Action (or Acquisition) when putting together advertising estimates.

This is the effective price you pay to generate a lead, for instance.

It’s a performance ratio. It starts to take into account things like costs vs. conversions to help you determine a much better figure: ROI.

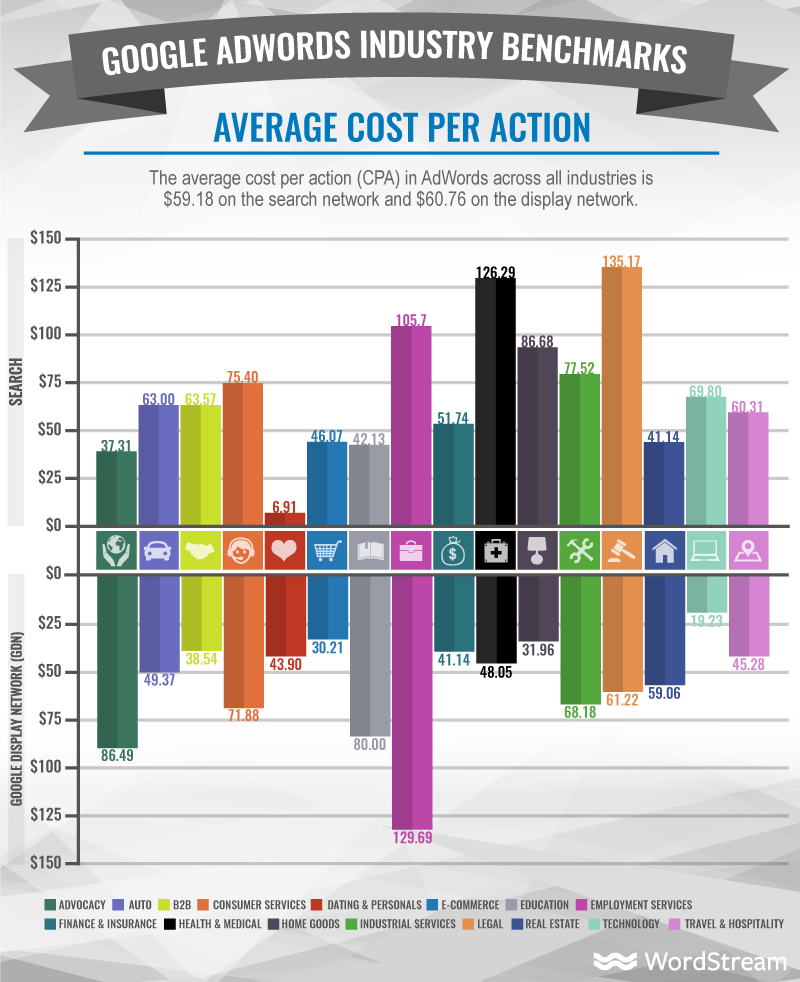

The industry average Cost Per Action for ecommerce lines up with education on the search network.

So from an ROI standpoint, there’s almost no difference.

This is why CPC is almost meaningless.

Yes, it’s important to a point because it drives things like your Cost Per Action.

However, what’s ultimately more important is the revenue you can generate.

It doesn’t matter whether we’re talking about Google AdWords, Facebook, or even Twitter ads. The message is still the same.

Digital Marketer once ran a Twitter Lead Gen campaign, testing the effective Cost Per Action (or Lead).

One campaign was able to see a $7.81 cost per lead.

They then ran the same study with the same ad and audience targeting. But this time, they optimized the campaigns to increase conversions.

It generated a $1.38 Cost Per Lead, which came out to a five time lead increase on the same ad budget.

They were able to 5X conversions simply by focusing on conversions and Cost Per Lead. They didn’t even have to touch the CPC.

You can see this time and time again.

Jacob Baadsgaard of Disruptive Advertising confirms that the best PPC metrics are revenue-focused. They track lead data all the way through to closed sales.

Then, and only then, will they make a decision about which ad campaign is best.

It’s not that costs don’t matter. They do, of course. But they only matter in context to how much revenue you can generate from it.

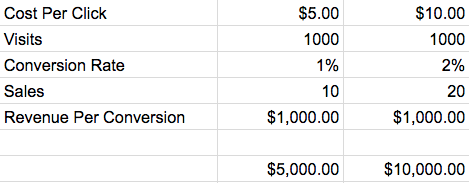

Here’s a very simple example to illustrate.

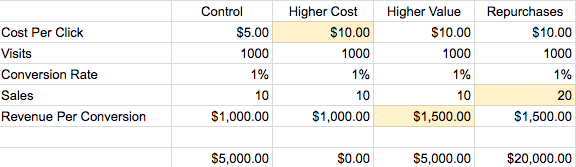

Let’s say you run two ad campaigns side-by-side.

The Cost Per Click for the second campaign is twice as much as the first. But because the conversion rate is 2% instead of 1%, you’re able to double revenue.

Would you pay twice as high a Cost Per Click to generate twice as much revenue? Of course you would!

This is after reducing revenue by your ad costs. So it’s already accounting for the higher ad budget.

At the end of the day, you’re still doubling revenue. It’s totally worth it!

Obsessing over CPC doesn’t just leave money on the table. It can also make you waste a ton of what you’re already spending.

Here are a few examples.

Obsessing Over CPCs Can Make You Pull The Plug Too Early (or Too Late)

There are many things that separate big companies from small ones.

But here’s one of the biggest: Big companies spend more on advertising than small ones do.

Duh, right? Of course big companies have bigger budgets.

We’re not just talking about dollars spent, but percentage of revenue

Because you still might leave a lot of money on the table.

If your CPCs start edging up, the campaigns will back off or stop.

Then your lead flow will stop, too.

That’s why I like using CPAs as targets if possible, instead of CPCs.

Watch CPA Instead of CPC

Cost Per Action is a better performance than Cost Per Click.

It’s not as good as Revenue, though–and there’s the problem.

CPAs can still be subjective.

Is a ‘high’ CPA bad? Maybe, maybe not.

If your CPA is over $100 in ecommerce, that might be bad.

Almost every single campaign CPA will be over $100 in law, for example. So it’s not bad at all.

Its still a much better metric to control ad campaign performance, though.

You can still figure out an upper range that starts to make ad campaigns unprofitable. You’ll base this on your average sale per customer. (More on this later.)

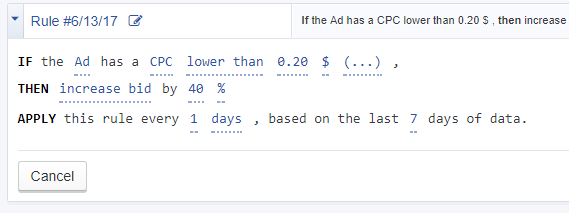

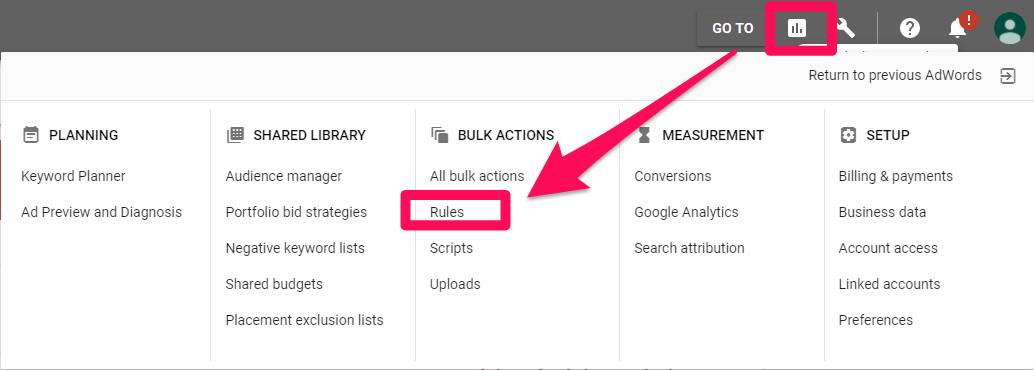

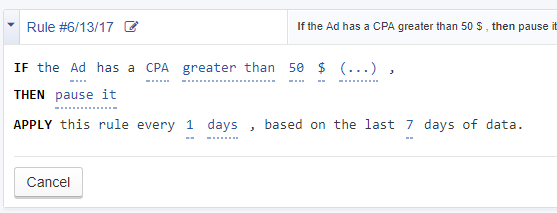

For starters, you can set automated rules to increase or decrease the total budget based on your CPA.

Inside AdWords, you can go to “Bulk Actions” and create new “Rules” for these ranges:

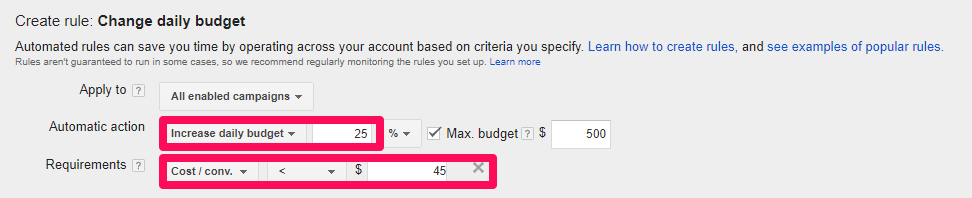

Under “Change budgets,” you can set an automated rule to either increase or decrease budgets based on cost per conversion numbers.

This tells AdWords to automatically increase your daily budget 25 percent if the CPA is within a certain dollar range.

You can do this same exact strategy inside Facebook, too.

You’ll set a rule to increase, decrease, or stop a campaign if the CPA hits a certain threshold.

Managing ad campaigns by CPA can net you more customers and revenue.

There’s still one big section we’re forgetting.

Keyword pricing or competitive pressure aren’t the only factors to worry about.

Many times, your customer base could be going through their own issues, and that’s not something you can change.

That’s why focusing on revenue is always the best approach.

Increase the Revenue-Side of the Equation to Overcome Outside Factors

Spearmint Love is one my favorite success stories.

The craziest part is that it almost didn’t happen.

They were growing like a weed, until…everything just stopped.

Results were declining across the board and they couldn’t figure out why.

Until, one day while on a walk, it dawned on one of the co-founders.

Parents will buy baby clothes until that baby grows up. In other words, their customers were kind of ‘moving on’ from the company.

The ad campaign decline had nothing to do with costs or his ad campaigns per se.

It had everything to do with their customer base.

How on Earth do you solve this problem?

By focusing on increasing revenue — not touching costs.

If the CPA is ‘too high’ to make your numbers work, start by increasing average order values.

Upsells are easy, for example, when you bundle similar products.

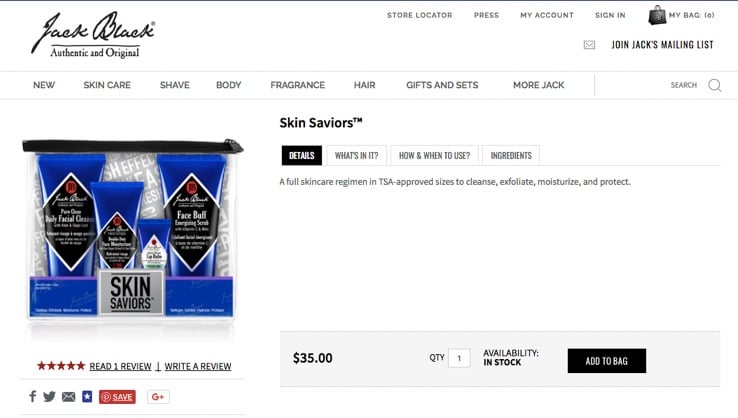

Think about the last time you flew somewhere. Chances are, you bought a travel-sized product at a store before going through TSA.

But that product probably only cost a few bucks, right?

Check out what Jack Black does here, bundling several travel products together.

You arguably need all of these products if you’re flying somewhere.

Instead of only charging you a few bucks each, they’re charging you $35 for the whole pack!

Simply bundling similar products allows them to charge 10x more. Which means you can afford a much higher initial advertising cost now, too.

You can also cross-sell products to try and raise the average order value.

For example, right underneath this travel bundle, Jack Black offers a few related products to take with you:

One interesting thing to note is the price of all three items. They’re all slightly less than the initial $35 purchase.

Why?

They’re using price anchoring effect to make these additional products seem less expensive.

The Economist included a middle pricing tier for a print-only subscription. It was the same exact price as the ‘big’ plan for both the print and web editions.

Most people chose the combined third option because it seemed like the best deal.

There’s only one reason to spend money on ads at the end of the day: to make money.

Chasing the keywords with the lowest CPC is a losing proposition.

If anything, you should be spending more money. You should actually search out the highest CPC’s in your industry.

Why?

Often, they offer the most potential. You want to maximize the most sales per dollar spent.

So you know all those “industry benchmark CPC” numbers? Don’t worry about them.

Instead, start focusing on CPA. That’s the number it costs for you to acquire each new customer.

It’s not perfect by any stretch. But it’s a better number to optimize around than CPC.

From there, try to dig into revenue numbers.

Can you bundle a few products to raise the average order value? Can you cross-sell recommended products and use price anchoring to lower their perceived cost?

Then, figure out how you can keep customers around longer.

That might mean introducing new, related product lines. Or it might mean introducing ‘consumable’ products that people need to repurchase again and again and again.

Mobile advertising works, but only if your message makes it to the consumer’s inbox, and only if your ad is mobile-optimized.

It’s the only way to steer clear of the noise and get a positive return on investment.

Most online marketers laugh at the idea of SMS marketing because they think it’s more regulated than email marketing. But that’s a myth.

Watered-down, mobile-targeting tactics are costing you conversions, clients, and revenue.

Meanwhile, SMS marketing is lurking in the background, waiting for you to capitalize on it.

Here’s why (and how) you should revisit SMS marketing to generate revenue.

The Many Advantages of SMS Marketing

Do you think Instagram has good engagement numbers?

Wait until you see what text messages get.

SMS Marketing Advantage #1.Texting Has The Best Engagement Rate of Any Marketing Medium

Emails can sit unread for days, phone calls can go unanswered, but text messages are almost always read immediately after they’re sent.

We already talked about the comparatively dismal open rates for email. The average CTR for PPC ads is even worse at 2%.

The point is that SMS marketing is underrated and underappreciated.

But nothing great comes without its catch.

It’s neither ethical nor legal to send unsolicited messages with text-message marketing.

You need a written opt-in.

Fortunately, customers have an easy way to opt themselves in — or out — straight from their mobile phones with most text-marketing services.

Using Attentive’s patent-pending “two-tap” technology, customers can opt-in to a brand’s text messaging subscriber list seamlessly from their mobile website, social media, or other digital channels.

With one tap, a message will populate in their message inbox. They simply press send on the pre-populated text message to opt-in and receive a welcome message.

Here are some of the advantages of mobile text messaging.

SMS Marketing Advantage #2. It’s Trackable

There are countless texting platforms that allow you to manage your campaign all from your desktop.

Find a solution that will give you access to detailed analytics that lets you track each step in the conversion process, starting with the initial delivery and opening.

Mobile messaging makes it possible to get feedback from your recipients quickly via a quick tap on the ‘reply’ button or a click on your link.

You can deliver quick, simple messages that direct subscribers back to your site.

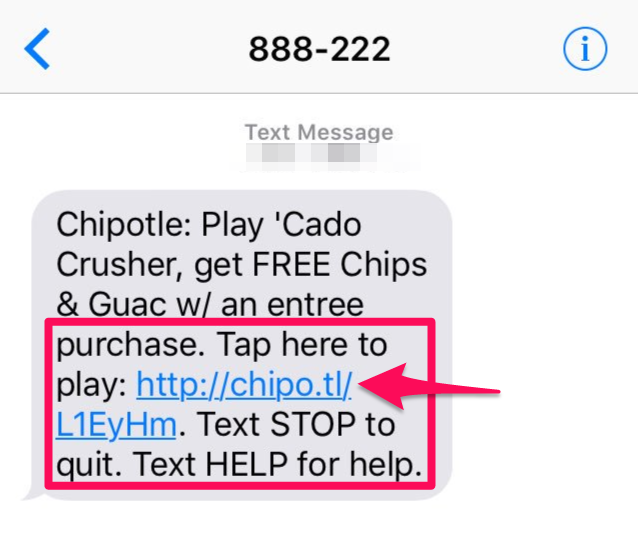

For example, Chipotle excels at using mobile messaging to drive sales.

It’s short and sweet. It gets straight to the point with “free chips and guac” if you play their game.

Not a bad deal, right?

Especially since they have queso now, too.

Get creative with your text-marketing campaigns and take a page out of the Chipotle playbook.

SMS Marketing Advantage #4. Immediate Delivery

Overall, mobile marketing is fast. Once you press “send,” your message goes out instantly.

You can set up a campaign and have hundreds of clicks within minutes.

SMS Marketing Advantage #5. Add a Personal Touch

Sending a text message via your mobile device gives you an informal opportunity to personalize the message.

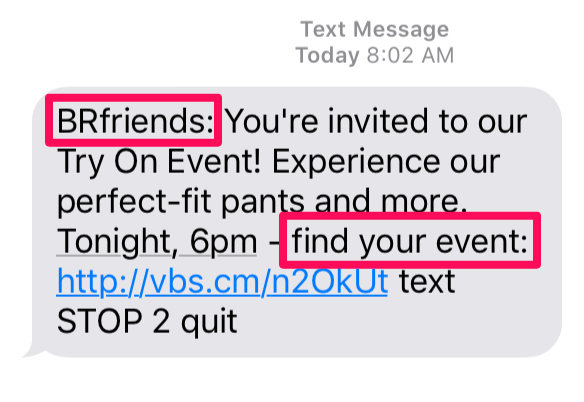

For example, the Banana Republic often sends text messages that include words like “friends” and “your.”

Using words like “you” and “I” is one of my favorite techniques for driving engagement.

The Banana Republic also does an excellent job of tapping into local events that are relevant to the recipient.

See? The opportunities with SMS are endless.

You can personalize your message, direct users to fun games where they can win coupons, and track every step of the conversion process.

Here’s how it works.

The Basic Components of SMS Marketing

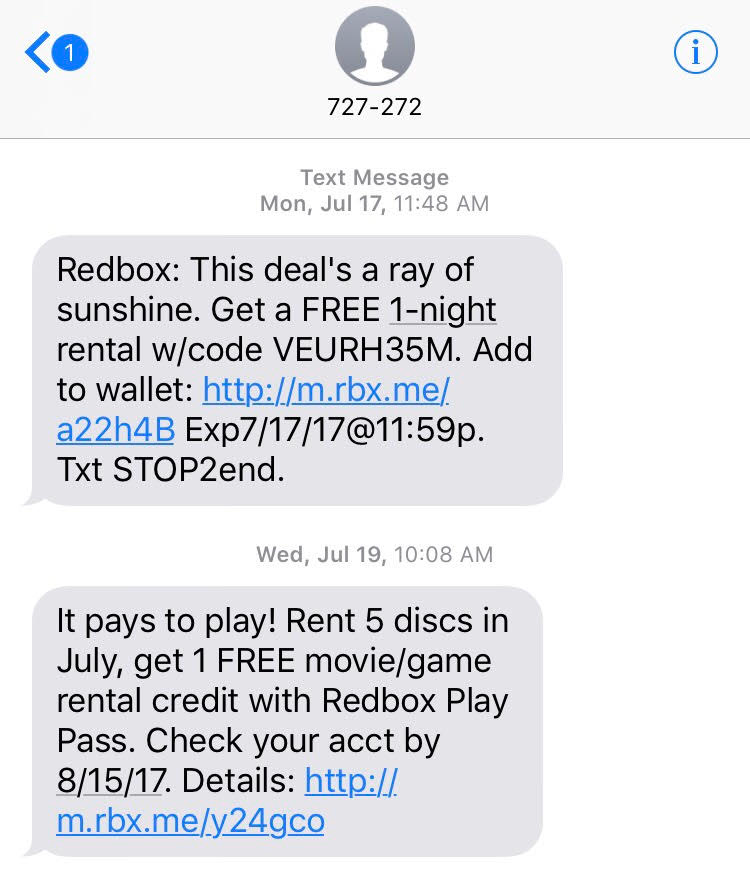

The two basic components of a typical SMS-marketing campaign are the keyword and the shortcode. Here’s an example:

Text “POPCORN” to 555555 for our weekly list of flavors!

“POPCORN” is the keyword that gets placed in the body of the message.

“555555” is the shortcode that gets put in the recipient box.

When a customer sends that message, they’re “opting in” to your campaign. It’s as easy as that.

From there you can do a few different things.

Go ahead and send them a single, automated response to follow up and let them know what to expect next. Or you can just add them to a list that will send additional texts over time.

Numbers received this last way have to be confirmed, however, since a customer could always enter a number incorrectly.

So before you add them to a campaign, you’ll have to confirm their participation with another message.

For example, you could send. “Text ‘YES’ to receive weekly coupons.”

Once they’ve opted in, customers can also respond to your messages with sub-keywords.

For example, sending the phrase “Hours” could trigger an automated text to send business hours, and “Stop” could remove the subscriber from the list.

Allowing customers to use sub-keywords gives them a way to interact with your business. It also enables them to opt-out of your campaign if they wish to stop receiving messages.

Once you’ve got the basics down, you can tap into creative ideas — like Chipotle’s game, which we covered earlier.

It’s giving you a simple one-click option to hook up your phone’s payment system with its offer.

Plus, the subscriber gets an extra incentive for taking this additional step. Customers don’t have to take an extra step to pay when they want to rent movies.

SMS Marketing Tip #2. Use Drip Campaigns

Drip campaigns are automated messages sent based on specific factors, such as how long someone has been a customer.

You can create triggers or tailored responses depending on each individual’s status.

In the context of coupons, for example, you could send a 5 percent off coupon right after the subscriber signs up, a 10 percent coupon after three weeks, and a 20 percent off coupon after two months.

The longer they stick around, the bigger the potential bonus. So you’re incentivizing the action you want.

Best of all, you can schedule these to run automatically.

One will be sent as soon as a customer signs up or opts in. That way, you don’t need to keep sending individual messages.

SMS Marketing Tip #3. Poll Your Customers

Polls let your customers text different keywords to cast a vote.

With most services, you can run polls to collect responses over a period of time and graph the responses from your online dashboard.

These are relatively simple when you think about it.

However, they offer an interesting content piece.

You can use the results internally to improve your operations.

Or you can reuse the results in both blog and social content to leverage your unique, proprietary information.

The people who left an answer will also be more eager to find out what the eventual results were and even help you share them.

SMS Marketing Tip #4.Run a Sweepstakes Contest

You can have customers sign themselves up for sweepstakes by texting a particular keyword.

Once again, this is a standard promotion tactic.

You can select some winners from everyone who opts in. Or you can also give away a smaller prize to every person who texts your keyword.

You can even use it as an opportunity for cross-promotions.

Sterling Vineyards and Uber did that to give away free rides to Sterling’s customer base.

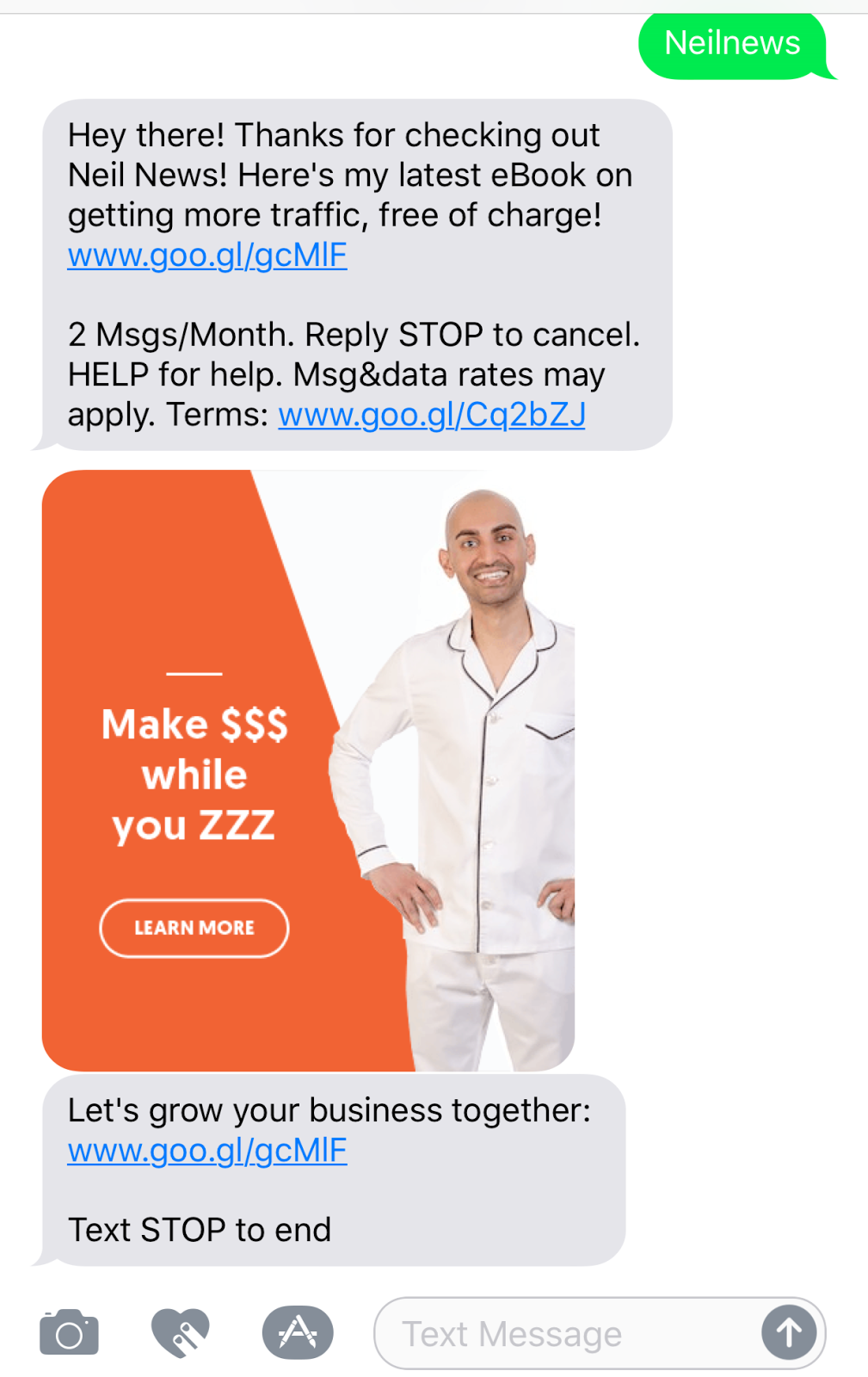

SMS Marketing Tip #5. Send Photos and Videos

In addition to actual text SMS messaging, you can also send photos and videos.

Here’s what I mean.

Let’s say you wanted to send an eBook preview or another image-style CTA.

Check out this example I created to see what’s possible with just a few minutes worth of work.

Want to create this type of marketing message? I’ll show you how a bit later in this piece.

Use Facebook to Grow Your SMS List

Instead of putting all of your eggs in one basket, use multiple channels to segment subscribers.

SMS and Facebook Ads are excellent on their own. But they can be even better when you use them together.

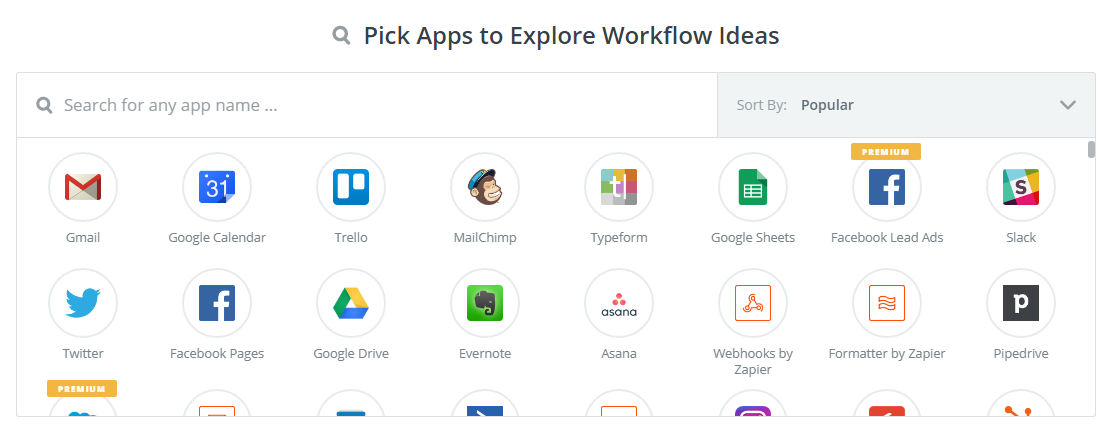

I recommend checking out Facebook’s lead ads to integrate with your SMS campaigns.

Lead ads are great for collecting data and information to build up a large subscriber base.

Here’s how to get started.

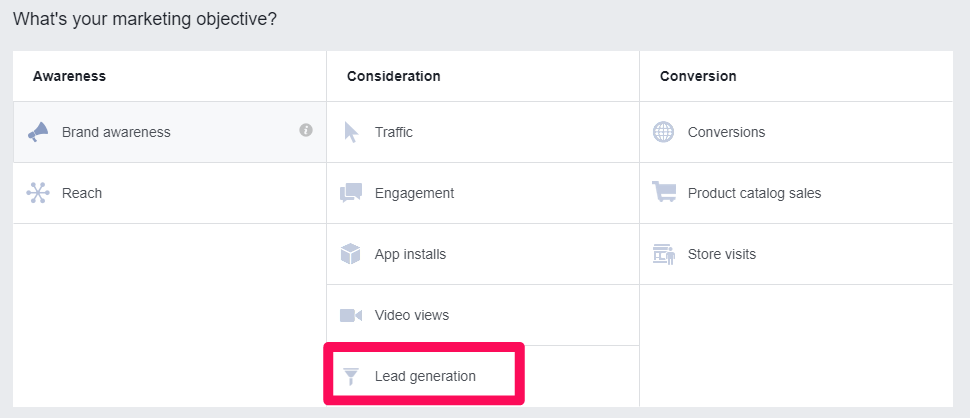

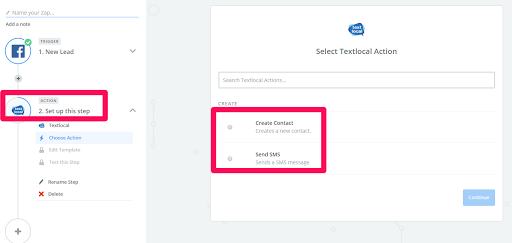

Head to the Facebook Ads Manager and create a new ad, selecting lead generation as your objective.

After you’ve set your target audience, budget, and placements, head down to the lead form option to set up your ad and collect phone numbers.

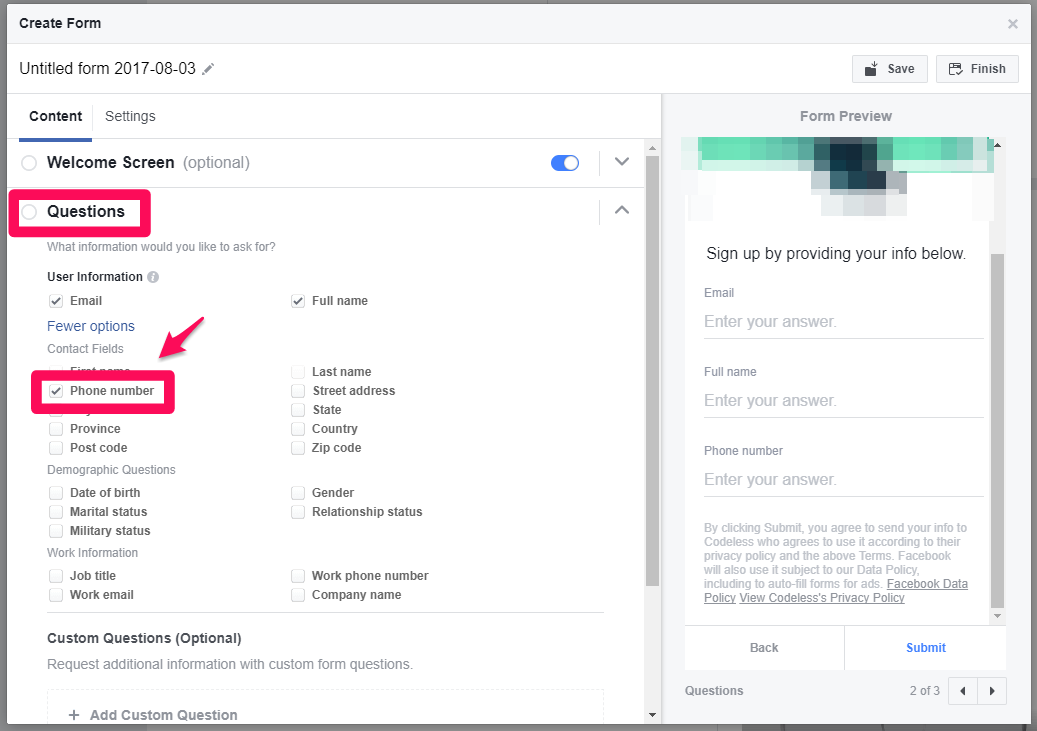

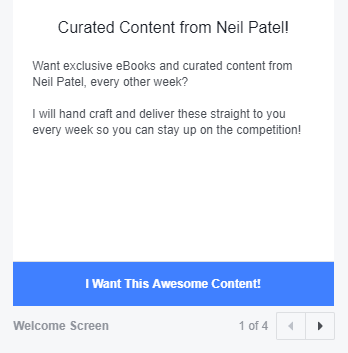

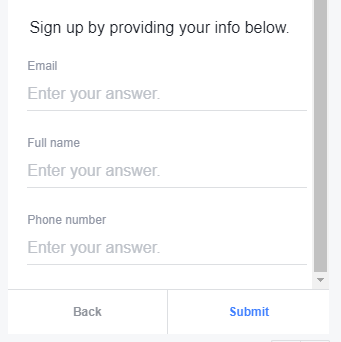

Here’s what the finished product should look like.

Now you get a multi-step form that doesn’t bombard the user with an instant information grab.

Instead, it uses multiple steps to warm them up to your offer.

Pretty cool, right?

Here’s what the second step of the form looks like.

Once you’ve configured your settings, you’ve got a simple way to collect phone numbers immediately.

That means you’re almost ready to start getting your first SMS campaign off the ground.

How to Automate SMS Marketing

Since we’re into the idea of working smarter and not harder, I suggest automating the SMSM marketing process.

Let’s face it: Marketing automation saves precious time you can spend growing your business.

For example, you don’t have to manually export and import lead data. Instead, you can use a tool like Zapier to quickly build out an automated process.

Zapier connects with just about every marketing software you can think of, including MailChimp, Gmail, Facebook Ads, Slack, and many of the biggest CRMs on the market.

So if you get a few people submitting phone numbers in your Facebook lead ads, you can send them directly to your CRM, your messaging platform, and even various SMS marketing platforms. All at the same time!

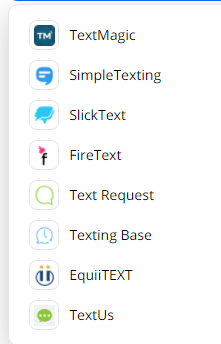

Here’s a few of the texting apps they work with, or you can search here.

Let’s dive straight in, shall we?

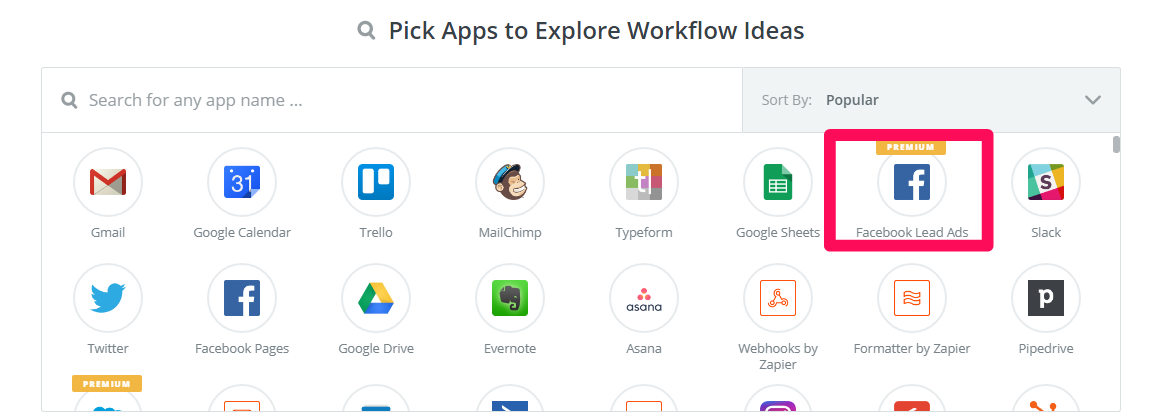

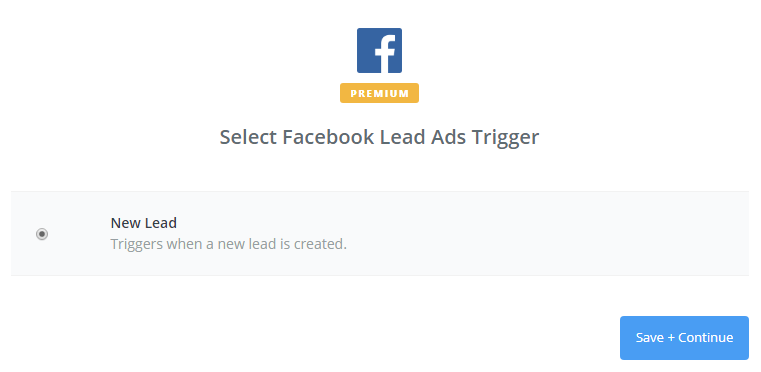

First, select Facebook Lead Ads from the workflow ideas list.

Next, select it as your trigger.

So whenever a lead fills out your lead capture form, it will trigger the following action that you want to set.

I’ll show you how to set that up in one second. But it could be anything from sending that lead form information to your CRM to connecting it to your SMS marketing software.

Now, let’s select this action once you’ve connected your Facebook account to Zapier’s workflow.

The action determines what happens with the data from your lead forms.

For example, you can instantly add a new lead to your SMS app of choice. Then you can even automate the first message that will go out to them after they’re added.

All of this automation saves you countless hours of manually transferring data and information.

Conclusion

Let’s be honest: SMS marketing can be kinda spammy.

It has evolved a lot over the past few years, though.

People are attached to their phones more than ever, and SMS marketing allows you to get direct access to your customers.

If you can get them to opt-in, they’re never going to miss an update or offer from your company ever again.

Are you looking for a business credit card that doesn’t require personal guarantee?

Get a Business Credit Card That Doesn’t Require a Personal Guarantee

We researched a ton of company credit cards for you. So, here are our top picks.

Per the SBA, business credit card limits are a whopping 10 – 100 times that of consumer credit cards!

This shows you can get a lot more funds with business credit. And it also shows you can have personal credit cards at retail stores. So, you would now have an additional card at the same shops for your small business.

And you will not need collateral, cash flow, or financial data to get small business credit.

Business Credit Card That Doesn’t Require a Personal Guarantee: Advantages

Benefits can differ. So, make certain to choose the benefit you would prefer from this choice of options.

Business Credit Card That Doesn’t Require a Personal Guarantee: 0% APR – Pay Nothing!

Bank of America® Business Advantage Travel Rewards World Mastercard® Credit Card

The Bank of America® Business Advantage Travel Rewards World Mastercard® credit card has no annual fee and comes with a 0% introductory APR on purchases for the initial nine months. Afterwards, the card has a 13.24 – 23.24% variable APR

Earn 3 points/dollar spent when you book travel via the Bank of America Travel Center and 1.5 points/dollar on all other purchases. You can get unlimited points and points never expire.

Details

There is a 25,000-point sign-up bonus when you spend $1,000 in the initial 60 days of starting the account. Cardholders get travel accident insurance, and lost luggage reimbursement.

They additionally get trip cancellation coverage, trip delay reimbursement and other benefits.

There is no introductory rate for balance transfers. Also, bonus categories are limited.

Consider the JetBlue Plus Card for an additional offer of a 0% introductory APR

Earn six points/dollar on JetBlue purchases, two points/dollar at restaurants and grocery stores. And get one point/dollar on all other purchases.

Details

Spend $1,000 in the first 90 days and pay the annual fee. So, then you can earn 40,000 bonus points. New cardholders receive a 12-month, 0% initial APR on balance transfers made within 45 days of account opening.

Thereafter, the variable APR on purchases and balance transfers is 17.99%, 21.99% or 26.99%, based on creditworthiness. Benefits include a free first checked bag and 50% savings on in-flight purchases.

Outstanding Business Credit Cards with No Annual Fee

Uber Visa Card

Check out the Uber Visa Card. Uber is the very first ride-sharing service to offer a credit card, in a partnership with Visa and Barclays.

The card offers 4% back per dollar spent at restaurants, takeout and bars, including UberEATS. Also, earn 3% back on hotel, airfare and vacation home rentals. And get 2% back on online purchases.

So, this includes retailers and subscription services such as Uber and Netflix. And earn 1% back on all other purchases. Each percent/point has a value of 1 cent. Redeem points for cash back, gift cards or Uber credits directly in the app.

By spending a minimum of $500 in the initial 90 days, users can earn a $100 sign-up bonus. Cardholders spending a minimum of $5,000 per year are eligible to receive a $50 credit toward online subscription services.

Details

If you pay your cellphone bill with this card, you are insured up to $600 for cellphone damage or theft.

Cardholders are eligible for exclusive access to specific events and offers. Uber expects most of these offers to be available in major cities like New York, San Francisco, Los Angeles, Chicago and DC. There is no foreign transaction fee.

But there is no introductory rate. So the APR is a variable 16.99%, 22.74% or 25.74%, based on your creditworthiness. Cardholders with less than stellar credit will be on the higher end of the range.

Also, there are restrictions on Uber credits. To redeem points as credits within the Uber app, accumulate a minimum of 500 points, or $5. Cardholders can convert a maximum of 50,000 points, or $500, per day.

Not taking Uber? Then you’ll need to fill your gas tank someway. Why not do so with the Costco Anywhere Visa® Business Card by Citi?

This credit card earns cash back with every purchase. Get 4% cash back on the first $7,000 spent on eligible gas purchases annually (1% after that). Get 3% cash back at restaurants and on eligible travel purchases. Also, get 2% cash back at Costco and Costco.com. And earn 1% cash back on all other purchases.

So keep in mind: the $0 annual fee is only for Costco members. And an active Costco membership is required. Cardholders will get access to damage and theft purchase protection, extended warranty coverage and travel accident insurance.

Also, there is no sign-up bonus available with this card.

Check out the Ink Business Cash ℠ Credit Card. Companies can get cash back with every purchase. Spend $3,000 in the first three months from account opening. And you’ll earn a $500 bonus cash back.

There is a $0 annual fee with a 0% introductory APR for 12 months on purchases and balance transfers. Thereafter, the APR is a 15.24 – 21.24% variable.

The card comes with travel and purchase coverage benefits. So, this includes an auto rental collision damage waiver and extended warranty protection.

Details

Earn extra cash back on business categories. So, these include office supply stores, telecommunications, gas stations and restaurants.

Note: this credit card has a balance transfer fee. Pay 5% of the amount transferred or $5, whichever is greater. Also, there is a foreign transaction fee of 3%.

Get a good look at the United MileagePlus Explorer Business Card.

Earn 2 miles/dollar with United and at restaurants, gas stations and office supply stores. All other purchases get 1 mile/dollar. Earn a 50,000-mile sign-up bonus after spending $3,000 in the initial three months from account opening.

Benefits include priority boarding, a free first checked bag for you and a companion on the same reservation.

Details

Also, get two United Club passes annually. And get hotel and resort perks including upgrades. Additionally, get early check-in and late checkout. And get an auto rental collision damage waiver.

Also, get baggage delay insurance, lost luggage reimbursement, trip cancellation and interruption insurance. Finally, get trip delay reimbursement, purchase protection, price protection and concierge service.

After the first year, the card has an annual fee of $95. APR of 17.99% – 24.99%, based on creditworthiness.

Starwood Preferred Guest® Business Credit Card from American Express

Another alternative is the Starwood Preferred Guest Business Credit Card from American Express.

This credit card is for those who stay at Starwood Preferred Guest and Marriott hotels often. Get six points per dollar of eligible purchases at participating SPG and Marriott Rewards hotels.

And get four points per dollar at American restaurants, American filling stations, and on US purchases for shipping.

Also, earn four points to the dollar on wireless telephone services purchased directly from US service providers. For all other eligible purchases, get two points per dollar.

Details

Get 75,000 bonus points when you spend $3,000 in the initial three months of account opening. Benefits include free in-room premium internet access, Sheraton Club lounge access, and purchase protection.

Plus, you get car rental loss and damage insurance. And you get baggage insurance. There is also a global assistance hotline. And there is a roadside assistance hotline. And get travel accident insurance and extended warranty coverage.

The most significant issue is the annual fee. There is a $0 introductory annual fee for the first year, then it’s $95 thereafter. Plus, there is no 0% introductory APR. Instead, there is a 17.74 – 26.74% variable APR

Get Business Credit Card That Doesn’t Require a Personal Guarantee for Average Credit

Capital One® Spark® Classic for Business

For fair credit, we like the Capital One Spark Classic for Business. It has no yearly fee. There are cash-back rewards. The card earns an unlimited 1% cash back on all purchases. There is an annual fee of $0.

With this card, you will get benefits including an auto rental collision damage waiver, and purchase security. And you also get extended warranty coverage. And you get travel and emergency assistance services.

But KEEP IN MIND: the ongoing APR is 24.74% variable APR. And the penalty APR is even higher, 31.15%. Also, there is no sign-up bonus. In addition, this card reports monthly to personal credit. It does report to business credit as well, but they generally require a personal credit check and will always report to personal credit.

Get a Business Credit Card That Doesn’t Require a Personal Guarantee for Luxurious Travel Points

IHG ® Rewards Club Premier Credit Card

Have a look at the IHG ® Rewards Club Premier Credit Card. it earns hotel rewards worldwide. For every dollar spent at participating IHG hotels, get 10 points. Get two points per dollar spent at gas stations, grocery stores and restaurants.

Plus, all other purchases earn one point. New cardholders can earn an 80,000-point sign-up bonus when they spend $2,000 in the first three months of account opening.

Details

This card offers a free one-night hotel stay each year. Plus, there is a variety of benefits like travel and purchase coverage and an upgrade to Platinum Elite status with the IHG Rewards Club. The club offers complimentary room upgrades when available and guaranteed room availability.

The most significant issue is that the card does not offer a zero percent APR introductory rate. And the standard APR is 17.99 – 24.99% variable. Also, the annual fee is $89.

This credit card earns six points/dollar spent at participating Marriott and SPG hotels. And get two points/dollar on all other purchases.

Spend $3,000 in the initial three months from account opening and get two free night awards (each valued up to 35,000 points).

Cardholders get access to perks including a free one-night stay yearly after account anniversary. Also get travel and purchase protection. So, this includes free standard in-room Wi-Fi and priority late checkout.

Details

Perks include baggage delay reimbursement, and lost luggage reimbursement. There is also trip delay reimbursement. And there is purchase protection. Additionally, there are concierge service and automatic Silver Elite status, which includes a 20% bonus on points.

Spend $35,000 each account year and get an upgrade to Gold Elite status. So, that includes a complimentary room upgrade, free daily breakfast and 4 PM late checkout.

There is an annual fee of $95. The APR is a 17.99– 24.99% variable.

Get a Low APR/Balance Transfer Business Credit Card That Doesn’t Require a Personal Guarantee

Discover it® Cash Back

Have a look at the Discover it® Cash Back card. There is a 10.99% introductory APR for six months from date of first transfer. So, this is for transfers under this offer which post to your account by January 10, 2019.

After the introductory APR expires, your APR will be 14.99% to 23.99%. So, this is based on your creditworthiness. Your APR will vary with the market, which is based upon the Prime Rate.

Details

You can get 5% cash back at different places every quarter. So, these are places like gas stations, grocery stores, restaurants, Amazon.com, or wholesale clubs. But this is up to the quarterly maximum each time you activate. Additionally, automatically get unlimited 1% cash back on all other purchases.

You will earn an unlimited dollar-for-dollar match of all the cash back you have gotten at the end of your first year, automatically.

Get a Business Credit Card That Doesn’t Require a Personal Guarantee With a Credit Builder Option

Discover it® Student Cash Back

Make sure to have a look at the Discover it® Student Cash Back card. It has no annual fee. The credit card also has a six-month introductory period of 0% APR on purchases. And there is an APR of 14.99 – 23.99% variable on all purchases after that period.

One distinct feature is that it provides an incentive for students to maintain good grades with a $20 statement credit. If students earn a GPA of 3.0 or better each school year, the card will award the $20 statement credit annually. So, this is for up to five years.

Details

Use this card to build personal credit. While this is a personal credit card versus a company card, for new credit users, their FICO scores will be vital. And this credit card offers an outstanding way to raise FICO. This is while also getting rewards. Better personal credit can also, often, be the key to unlocking online lending.

You can earn 5% cash back at different places each quarter like grocery stores, gas stations, restaurants or Amazon.com. So, that’s up to the quarterly maximum. After that, this credit card offers unlimited 1% cash back on all purchases.

In the first year, all cash back rewards are matched 100%.

Downsides include a cash advance fee of either $10 or 5% of the amount of each cash advance, whichever is more. And even though they waive the first late payment fee, a fee of up to $37 applies on all other late payments. There is also a returned payment fee of up to $37.

Get a Business Credit Card That Doesn’t Require a Personal Guarantee for Cash Back

SimplyCash Plus Business Credit Card from American Express

Consider the SimplyCash Plus Business Credit Card from American Express. There is a $0 annual fee. And there is a 0% APR on purchases. So this is for the first 15 months an account is open.

But when the introductory period ends, the APR for purchases is 14.24 to 21.24%. So, this is variable and based on creditworthiness.

Details

This credit card has several benefits. These include purchase protection, car rental loss and damage insurance. And they also include a baggage insurance plan, extended warranty coverage and a global assist hotline.

Also, earn 5% cash back at US office supply stores and on wireless phone services. So, these must be bought from American service providers. But this applies to the initial $50,000 of yearly spending. Then, you earn 1% cash back.

You also get 3% cash back on spending category of your choice. So, this is from eight distinct categories. They include airfare, gas, advertising and computer purchases. But it applies to the first $50,000 of annual spending. Then, you earn 1% cash back.

Cash-back bonuses are automatically credited to the customer’s billing statement.

Note: you cannot use this credit card for balance transfers. There is a foreign transaction fee of 2.7%. The credit card charges up to $38 in late fees. And the returned check fee is also $38. The penalty APR is 29.99%.

And, it applies if you have two or more late payments within 12 months. It can also apply if you fail to make the minimum payment on time or have a returned payment.

Look at the Capital One® Quicksilver® Card. It offers flat-rate rewards of 1.5% on all purchases. There are no limits to the amount of cash back rewards which cardholders can earn. Also, the card has a $0 yearly fee.

New cardholders have a 0% APR on purchases and balance transfers for the first 15 months after opening the account. Then afterwards they have a 14.74 – 24.74% (variable) APR after that.

A cash bonus of $150 is on offer for those who make at least $500 in purchases within 3 months of account opening.

Details

Also, cash back rewards do not expire for the life of the account. And there is no limit to how much you can earn.

This card also offers travel accident insurance. And you get an auto rental collision damage waiver. There are no foreign transaction fees. And there is extended warranty coverage.

Downsides are the flat reward rate, not allowing for any more than that. And the higher APR after the first 15 months.

Get a Secured Business Credit Card That Doesn’t Require a Personal Guarantee

Wells Fargo Business Secured Credit Card

Have a look at the Wells Fargo Business Secured Credit Card. It charges a $25 yearly fee per credit card (up to 10 employee cards). It also requires a minimum security deposit of $500 (up to $25,000). And it is designed to help cardholders set up or rebuild their credit.

Select this credit card if you wish to get 1.5% per dollar in purchases without any limits. Or earn one point for every dollar in purchases. You also earn 1,000 bonus points for every month your company makes $1,000 in purchases on the card.

Details

Also, you get free FICO scores every month. There are no foreign transaction fees. It is possible to upgrade to unsecured credit. Your account is regularly reviewed. And you may become eligible for an upgrade to an unsecured card with responsible use over time. Approval is not guaranteed and depends on factors including how you manage this and your other accounts.

APR is the current prime rate plus 11.90%. There is no introductory APR period and no sign-up bonus. This is not a credit card for balance transfers.

Grab a Business Credit Card That Doesn’t Require a Personal Guarantee for Jackpot Rewards

Ink Business Preferred ℠ Credit Card

Get a look at the Ink Business Preferred Credit Card from Chase. Cardholders earn 3 points for every dollar spent on travel, shipping, internet, cable, phone and qualifying advertising with the card. So, this is up to $150,000 each year. And all other purchases earn an unlimited one point per dollar spent.

This is a Visa card.

Cardholders get benefits like purchase protection, trip cancellation or interruption insurance. They also get cellphone protection. And they get extended warranty coverage. And they get an auto rental collision damage waiver.

Details

Earn 80,000 bonus points when you spend $5,000 in the initial 3 months from account opening. There is an annual fee of $95. You can add employee cards at no additional cost.

This credit card only offers 3 points per dollar to a limit of $150,000 a year. So, this is for travel, shipping, internet, cable, phone and qualifying advertising. All other purchases earn an unlimited flat rate of one point per dollar. And there is no introductory APR

The Best Business Credit Card That Doesn’t Require a Personal Guarantee for You

Your absolute best business credit card that doesn’t require a personal guarantee will hinge on your credit history and scores.

Only you can select which features you want and need. So, be sure to do your homework. What is outstanding for you could be catastrophic for other people.

And, as always, be sure to develop credit in the recommended order for the best, quickest benefits.

Most agree, when you start wondering how to qualify for a business loan, the waters can become muddied with things that do not really matter. As a result, it can be hard to distinguish between what really matters, and what doesn’t. In fact, many factors affect whether or not you qualify for a business loan.

How to Qualify for a Business Loan: What Really Matters?

Truly, there is a lot of conflicting information out there on how to qualify for a business loan. Is it business credit? Is it personal credit? What else makes a difference? Can you get a loan without business credit? Do you really need a business plan? What reports are they looking at? Let’s clear some of this up.

How to Qualify for a Business Loan: What You Don’t Know Can Hurt You

First, you need to know that there are probably a lot of things that make a difference in how to qualify for a business loan that you don’t even realize. At first glance, a lender is going to consider fundability. Usually, most borrowers think this has only to do with your credit score. However, there are many layers to fundability. Together, they can all make a difference in whether or not you are approved.

Find out why so many companies use our proven methods to get business loans.

How to Qualify for a Business Loan: Understanding Fundability

Not surprisingly, one of the main things about fundability that most business owners do not realize is that it actually starts with how your business is set up. For example, even the address and telephone number you use for your business can affect fundability.

Set Your Business Up to Be Fundable

To help, here are some things to consider when setting up your business to appear fundable.

Contact Information

It has to be separate from your personal contact information.

EIN

If you don’t know, this is the equivalent of an SSN for your business.

Incorporate

It’s true, you have to incorporate as either an LLC, and S-corp, or a corporation.

Business Bank Account

A dedicated business bank account is vital to fundability.

Licenses

Make sure you have all the licenses you need to operate your business.

Website

You need a professionally designed website and an email address with the same URL.

Honestly, this is a super simple summary. Get more details on how to set up your business to be fundable here.

Other Things that Affect Fundability

In addition to how your business is set up, there are about a million other things that can affect the fundability of your business. They can all be broken down into the following categories.

Business Credit Report

This is the credit report, much like your consumer credit report, that details the credit history of your business. It is a tool to help lenders determine how credit worthy your business is.

Where do business credit reports come from? There are a lot of different places. Still, the main ones are Dun & Bradstreet, Experian, Equifax, and FICO SBSS. Consequently, you have no way of knowing which one your lender will choose. As a result, you have to make sure all of these reports are up to date and accurate.

Other Business Data Agencies

There are other business data agencies that affect those reports indirectly. This is in addition to the business credit reporting agencies that directly calculate and issue your credit reports. Two examples of other agencies include LexisNexus and The Small Business Finance Exchange. They gather data from a variety of sources, including public records. What does this mean for you? It may surprise you, but they could have access to information relating to automobile accidents and liens, among other things. You cannot access or change the data the agencies have on your business. However, you can ensure that any new information they receive is positive. Enough positive information can help counteract any negative information from the past.

Identification Numbers

In addition to the EIN, there are identifying numbers that go along with your business credit reports. You need to be aware that these numbers exists. Some of them are simply assigned by the agency. One, however, you have to apply to get. It is absolutely necessary that you do this.

Dun & Bradstreet is the largest and most commonly used business credit reporting agency. Every credit file in their database has a D-U-N-S number. To get a D-U-N-S number, you have to apply for one through the D&B website.

Business Credit History

Your credit history has everything to do with all things related to your credit score. Of course, this is a huge factor in the fundability of your business.

Credit history consists of a number of things including:

How many accounts are reporting payments?

How long have you had each account?

What type of accounts are they?

How much credit are you using on each account versus how much is available?

Are you making your payments on these accounts consistently on-time?

Of course, the more accounts you have reporting on-time payments, the stronger your credit score will be.

Business Information

On the surface, it seems obvious that all of your business information should be the same across the board everywhere you use it. However, when you start changing things up like adding a business phone number and address and incorporating, you may find that some things get missed.

Find out why so many companies use our proven methods to get business loans.

This is a problem. A lot of loan applications are turned down each year due to fraud concerns simply because things don’t match up. For example, maybe your business licenses have your personal address but now you have a business address. That needs to be changed. Maybe some of your credit accounts have a slightly different name or a different phone number listed than what is on your loan application. Do your insurances all have the correct information?

The key to this piece of the business fundability is to monitor your reports often. When it comes to business credit reports, you can monitor through the reporting agencies directly, or save money here.

Financial Statements

First, both your personal and business tax returns need to be in order. Not only that, but you need to be paying your taxes, but business and personal.

Business Financials

Typically, it is best to have an accounting professional prepare regular financial statements. Having an accountant’s name on financial statements helps your business look more credible and legitimate. If you cannot afford it monthly or quarterly, then at least have professional statements prepared annually. Then, they will be there whenever you need them.

Personal Financials

Usually, this is just tax returns for the previous three years. That is the bare minimum you will need. Other information lenders may ask for include check stubs and bank statements.

Bureaus

There are other agencies that hold information related to your personal finances that you need to know about. Everyone knows about FICO. Your personal FICO score needs to be as strong as possible. It really can affect business fundability and almost all traditional lenders will look at personal credit in addition to business credit.

Other than that, there is also ChexSystems. They monitor bad check activity, and that can affect your bank score. If you have too many bad checks, you will not be able to open a bank account. That will cause serious fundability issues.

For this point, everything comes into play. Have you ever been convicted of a crime? Do you have a bankruptcy or short sell on your record? How about liens or UCC filings? This all affects fundability.

Personal Credit History

Your personal credit score from Experian, Equifax, and Transunion affects fundability as well. If it isn’t great right now, get to work on it. The number one way to get a strong personal credit score or improve a weak one is to make payments consistently on time.

Also, make sure you monitor your personal credit regularly to make sure mistakes get corrected and that there are no fraudulent accounts reporting.

Application Process

So much plays into this that you may not even think about. First, consider the timing of the application. Is your business currently fundable? If not, do some work first to increase fundability. Next, ensure that your business name, business address, and ownership status are all verifiable. Lenders will check that. Lastly, make sure you choose the right lending product for your business and your needs. Do you need a traditional loan or a line of credit? Would a working capital loan or expansion loan work best for your needs?

How to Qualify for a Business Loan: Choose the Right Product and the Right Lender

This falls into that application process section of fundability. You have to know what you need, what you are eligible for, and what type of lender will work best for your needs. This will help you know where to apply and what to apply for, so that you can have the best possible chance of qualifying.

How to Qualify for a Business Loan: Choose the Right Type Business Loan

When it comes to business loans, these are the general types of products available.

Traditional Loans

These are the standard loans that disperse as a set amount of funds, with the borrower repaying with equal payments over a certain period of time. These can be secured or unsecured.

Line of Credit

This is revolving debt similar to credit cards. Borrowers are given a maximum limit of the amount of funds they can use, but only pay back the amount that they actually use.

Invoice Factoring

Factoring invoices is an option if you have receivables. The lender basically buys unpaid invoices from you at a premium, meaning you do not get full value. However, you do get fast cash.

Merchant Cash Advance

If you accept credit card payments, a merchant cash advance can help you out in a cash pinch. It is basically just what is says. It’s a cash advance on predicted credit card sales. They base the amount of the loan on average daily credit card sales, and then take payment from future credit card sales.

Find out why so many companies use our proven methods to get business loans.

How to Qualify for a Business Loan: Choose the Right Type of Lender

A lot of business owners think that a bank is their only option. There are a few different types of lenders to consider however.

Large Commercial Banks

Community Banks

Credit Unions

Private Lenders

Of course, which one of these you use will depend on your specific needs and qualifications.

How to Qualify for a Business Loan: You Need an Awesome Business Plan

While there are forms available from most lenders for you to simply write in information related to your business plan, that’s not the best way to do it. A professionally written, complete business plan makes a far better impression on a lender. This is true even if you are an established business applying for a loan. The only difference is, you will write a plan for how you will use the funds in relation to your current business rather than a business you intend to start. In general, a complete and professional business plan contains the following.

Opening

First comes the opening. It includes an executive summary, a more detailed description of the business, and your strategy for getting started.

Market Research

Next, there is a section for market research. As you might guess, this section consists of market analyses including an analysis of your audience and an analysis of any existing competition. It will tell what need exists, how you will fill it, and how you will fill it better than the competition.

How to Qualify for a Business Loan: The Plan

This can also be broken down into two parts.

Plan for Design and Development

This is your plan from start to finish. It discusses what steps are you going to take. In comparison, this is more detailed than your strategies section.

Plan for Operation and Management

This is where a number of questions are answered in relation to the management of the business. For example, who will own or does own the business? Furthermore, who will run or currently runs it from day to day? It could be as easy as stating that you are the sole owner and operator. In contrast, it could be as complicated as laying out a complete partnership plan or board or directors’ format. Truthfully, it just depends on your specific business.

Financials

Lastly, this section includes current financials, projections, and a budget plan for the loan funds you are applying for. As you can imagine, lenders want to see that you know how to handle and funds you get. Furthermore, they want to know that you have a plan for paying them back.

Take note, if you are not a great writer, you may need to hire a writer to help you with this. If you have no clue how to do market research, you may need to outsource that piece as well. Thankfully, most small business development centers offer help with business plans also. Go here to find an SBDC near you.

How to Qualify for a Business Loan: Wrap Up

Hands down, the absolute first step in the process has to be to do an analysis of fundability. Then, you will know where you stand. As a result, you will have a better idea of what you may need to do to increase fundability. Also, you will have a better understanding of what type of lender you need to go with and which type of product will best fit your needs. Then, you can get to work on your business plan. Remember, while nothing is guaranteed, following these steps can help increase your chances of loan approval immensely.

Most agree, when you start wondering how to qualify for a business loan, the waters can become muddied with things that do not really matter. As a result, it can be hard to distinguish between what really matters, and what doesn’t. In fact, many factors affect whether or not you qualify for a business loan.

How to Qualify for a Business Loan: What Really Matters?

Truly, there is a lot of conflicting information out there on how to qualify for a business loan. Is it business credit? Is it personal credit? What else makes a difference? Can you get a loan without business credit? Do you really need a business plan? What reports are they looking at? Let’s clear some of this up.

How to Qualify for a Business Loan: What You Don’t Know Can Hurt You

First, you need to know that there are probably a lot of things that make a difference in how to qualify for a business loan that you don’t even realize. At first glance, a lender is going to consider fundability. Usually, most borrowers think this has only to do with your credit score. However, there are many layers to fundability. Together, they can all make a difference in whether or not you are approved.

Find out why so many companies use our proven methods to get business loans.

How to Qualify for a Business Loan: Understanding Fundability

Not surprisingly, one of the main things about fundability that most business owners do not realize is that it actually starts with how your business is set up. For example, even the address and telephone number you use for your business can affect fundability.

Set Your Business Up to Be Fundable

To help, here are some things to consider when setting up your business to appear fundable.

Contact Information

It has to be separate from your personal contact information.

EIN

If you don’t know, this is the equivalent of an SSN for your business.

Incorporate

It’s true, you have to incorporate as either an LLC, and S-corp, or a corporation.

Business Bank Account

A dedicated business bank account is vital to fundability.

Licenses

Make sure you have all the licenses you need to operate your business.

Website

You need a professionally designed website and an email address with the same URL.

Honestly, this is a super simple summary. Get more details on how to set up your business to be fundable here.

Other Things that Affect Fundability

In addition to how your business is set up, there are about a million other things that can affect the fundability of your business. They can all be broken down into the following categories.

Business Credit Report

This is the credit report, much like your consumer credit report, that details the credit history of your business. It is a tool to help lenders determine how credit worthy your business is.

Where do business credit reports come from? There are a lot of different places. Still, the main ones are Dun & Bradstreet, Experian, Equifax, and FICO SBSS. Consequently, you have no way of knowing which one your lender will choose. As a result, you have to make sure all of these reports are up to date and accurate.

Other Business Data Agencies

There are other business data agencies that affect those reports indirectly. This is in addition to the business credit reporting agencies that directly calculate and issue your credit reports. Two examples of other agencies include LexisNexus and The Small Business Finance Exchange. They gather data from a variety of sources, including public records. What does this mean for you? It may surprise you, but they could have access to information relating to automobile accidents and liens, among other things. You cannot access or change the data the agencies have on your business. However, you can ensure that any new information they receive is positive. Enough positive information can help counteract any negative information from the past.

Identification Numbers

In addition to the EIN, there are identifying numbers that go along with your business credit reports. You need to be aware that these numbers exists. Some of them are simply assigned by the agency. One, however, you have to apply to get. It is absolutely necessary that you do this.

Dun & Bradstreet is the largest and most commonly used business credit reporting agency. Every credit file in their database has a D-U-N-S number. To get a D-U-N-S number, you have to apply for one through the D&B website.

Business Credit History

Your credit history has everything to do with all things related to your credit score. Of course, this is a huge factor in the fundability of your business.

Credit history consists of a number of things including:

How many accounts are reporting payments?

How long have you had each account?

What type of accounts are they?

How much credit are you using on each account versus how much is available?

Are you making your payments on these accounts consistently on-time?

Of course, the more accounts you have reporting on-time payments, the stronger your credit score will be.

Business Information

On the surface, it seems obvious that all of your business information should be the same across the board everywhere you use it. However, when you start changing things up like adding a business phone number and address and incorporating, you may find that some things get missed.

Find out why so many companies use our proven methods to get business loans.

This is a problem. A lot of loan applications are turned down each year due to fraud concerns simply because things don’t match up. For example, maybe your business licenses have your personal address but now you have a business address. That needs to be changed. Maybe some of your credit accounts have a slightly different name or a different phone number listed than what is on your loan application. Do your insurances all have the correct information?

The key to this piece of the business fundability is to monitor your reports often. When it comes to business credit reports, you can monitor through the reporting agencies directly, or save money here.

Financial Statements

First, both your personal and business tax returns need to be in order. Not only that, but you need to be paying your taxes, but business and personal.

Business Financials

Typically, it is best to have an accounting professional prepare regular financial statements. Having an accountant’s name on financial statements helps your business look more credible and legitimate. If you cannot afford it monthly or quarterly, then at least have professional statements prepared annually. Then, they will be there whenever you need them.

Personal Financials

Usually, this is just tax returns for the previous three years. That is the bare minimum you will need. Other information lenders may ask for include check stubs and bank statements.

Bureaus

There are other agencies that hold information related to your personal finances that you need to know about. Everyone knows about FICO. Your personal FICO score needs to be as strong as possible. It really can affect business fundability and almost all traditional lenders will look at personal credit in addition to business credit.

Other than that, there is also ChexSystems. They monitor bad check activity, and that can affect your bank score. If you have too many bad checks, you will not be able to open a bank account. That will cause serious fundability issues.

For this point, everything comes into play. Have you ever been convicted of a crime? Do you have a bankruptcy or short sell on your record? How about liens or UCC filings? This all affects fundability.

Personal Credit History

Your personal credit score from Experian, Equifax, and Transunion affects fundability as well. If it isn’t great right now, get to work on it. The number one way to get a strong personal credit score or improve a weak one is to make payments consistently on time.

Also, make sure you monitor your personal credit regularly to make sure mistakes get corrected and that there are no fraudulent accounts reporting.

Application Process

So much plays into this that you may not even think about. First, consider the timing of the application. Is your business currently fundable? If not, do some work first to increase fundability. Next, ensure that your business name, business address, and ownership status are all verifiable. Lenders will check that. Lastly, make sure you choose the right lending product for your business and your needs. Do you need a traditional loan or a line of credit? Would a working capital loan or expansion loan work best for your needs?

How to Qualify for a Business Loan: Choose the Right Product and the Right Lender

This falls into that application process section of fundability. You have to know what you need, what you are eligible for, and what type of lender will work best for your needs. This will help you know where to apply and what to apply for, so that you can have the best possible chance of qualifying.

How to Qualify for a Business Loan: Choose the Right Type Business Loan

When it comes to business loans, these are the general types of products available.

Traditional Loans

These are the standard loans that disperse as a set amount of funds, with the borrower repaying with equal payments over a certain period of time. These can be secured or unsecured.

Line of Credit

This is revolving debt similar to credit cards. Borrowers are given a maximum limit of the amount of funds they can use, but only pay back the amount that they actually use.

Invoice Factoring

Factoring invoices is an option if you have receivables. The lender basically buys unpaid invoices from you at a premium, meaning you do not get full value. However, you do get fast cash.

Merchant Cash Advance

If you accept credit card payments, a merchant cash advance can help you out in a cash pinch. It is basically just what is says. It’s a cash advance on predicted credit card sales. They base the amount of the loan on average daily credit card sales, and then take payment from future credit card sales.

Find out why so many companies use our proven methods to get business loans.

How to Qualify for a Business Loan: Choose the Right Type of Lender

A lot of business owners think that a bank is their only option. There are a few different types of lenders to consider however.

Large Commercial Banks

Community Banks

Credit Unions

Private Lenders

Of course, which one of these you use will depend on your specific needs and qualifications.

How to Qualify for a Business Loan: You Need an Awesome Business Plan

While there are forms available from most lenders for you to simply write in information related to your business plan, that’s not the best way to do it. A professionally written, complete business plan makes a far better impression on a lender. This is true even if you are an established business applying for a loan. The only difference is, you will write a plan for how you will use the funds in relation to your current business rather than a business you intend to start. In general, a complete and professional business plan contains the following.

Opening

First comes the opening. It includes an executive summary, a more detailed description of the business, and your strategy for getting started.

Market Research

Next, there is a section for market research. As you might guess, this section consists of market analyses including an analysis of your audience and an analysis of any existing competition. It will tell what need exists, how you will fill it, and how you will fill it better than the competition.

How to Qualify for a Business Loan: The Plan

This can also be broken down into two parts.

Plan for Design and Development

This is your plan from start to finish. It discusses what steps are you going to take. In comparison, this is more detailed than your strategies section.

Plan for Operation and Management

This is where a number of questions are answered in relation to the management of the business. For example, who will own or does own the business? Furthermore, who will run or currently runs it from day to day? It could be as easy as stating that you are the sole owner and operator. In contrast, it could be as complicated as laying out a complete partnership plan or board or directors’ format. Truthfully, it just depends on your specific business.

Financials

Lastly, this section includes current financials, projections, and a budget plan for the loan funds you are applying for. As you can imagine, lenders want to see that you know how to handle and funds you get. Furthermore, they want to know that you have a plan for paying them back.

Take note, if you are not a great writer, you may need to hire a writer to help you with this. If you have no clue how to do market research, you may need to outsource that piece as well. Thankfully, most small business development centers offer help with business plans also. Go here to find an SBDC near you.

How to Qualify for a Business Loan: Wrap Up

Hands down, the absolute first step in the process has to be to do an analysis of fundability. Then, you will know where you stand. As a result, you will have a better idea of what you may need to do to increase fundability. Also, you will have a better understanding of what type of lender you need to go with and which type of product will best fit your needs. Then, you can get to work on your business plan. Remember, while nothing is guaranteed, following these steps can help increase your chances of loan approval immensely.

Everyone thinks SEO is a long-term game… that you have to wait months if not years to see results. And, maybe that was the case a few years ago when content was still king.

With Google making 3200 algorithm changes in just one year, their goal isn’t to make a website wait a year or two before they are able to achieve a top spot.

Instead, they want to show the user the right site as quick as possible. It doesn’t matter if the site has been around for 10 years, or 10 days.

How SEO has changed

It used to be that if you want to rank well, you would have to create tons of long-form content and build links.

Or have a really aged domain with history. But as Google has clearly stated, having an older domain or even a new domain won’t affect your rankings.

In other words, there are other tactics that produce quick results.

For example, a few weeks I wrote a blog post about FAQ schema and how you can see the difference with your Google listing in 30 minutes.

Literally, 30 minutes.

That kind of stuff wasn’t possible before.

And SEO is no longer just a game of ranking on Google. There are tons of popular search engines like YouTube, in which you can get results in 24 hours.

Their algorithm is a bit different than Google’s in which if a video does really well in the first 24 hours of it being released, it will get shown more and rank higher.

In essence, you can take a top spot on YouTube in just days, no matter how competitive the term maybe.

You are full of it Neil?

Look, I’m not trying to say you can rank for “auto insurance” on Google within 24 hours or achieve unrealistic results, but you can drastically grow your search traffic in a reasonable time if you follow the right tactics.

It doesn’t matter if you have a new website or an old one.

So how do you get results faster? What’s the secret?

Well, I have a Master Class that will teach you how to double your traffic, but you’ll have to wait till Thursday.

I’m going to be introducing something new in which you can get more search traffic in 30 days.

All you have to do is take one simple action each day. And the action is so simple that it shouldn’t take you more than 30 minutes.

Stay tuned!

PS: Don’t forget to add the Master Class to your calendar. That way you’ll get notified on Thursday when it comes out.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

{kind=link}