Ecommerce Business Inventory Financing

How Can Ecommerce Business Inventory Financing Help Your Business?

Selling goods online? Then you might need Ecommerce business inventory financing.

Our World Has Changed – and It’s Gone Even More Online

While there was already a lot of online commerce, in March of 2020, due to COVID-19, a good 42% of Americans bought groceries online at least once per week. Orders for grocers from Amazon increased 50 fold!

Statista says about 227.5 million Americans were buying online in 2020, so with 330.7 American citizens, that’s just under 69% of all Americans. They are buying a lot more than groceries online. And that’s only continuing in 2021.

What is Ecommerce Business Inventory Financing?

According to Investopedia, “Inventory financing is a revolving line of credit or a short-term loan that is acquired by a company so it can purchase products for sale later. The products serve as the collateral for the loan.”

Why Can Ecommerce Business Inventory Financing Work Right Now?

Online businesses are doing relatively well right now. You already have experience with doing all of your commerce online. With a lot of brick and mortar businesses closed right now, or only tentatively reopening, ecommerce businesses can continue to do well.

Consider Ecommerce Business Inventory Financing

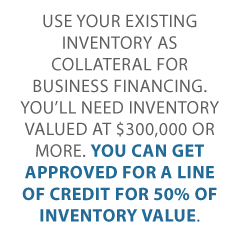

Use your existing inventory as collateral for business financing. You’ll need inventory valued at $300,000 or more. You can get approved for a line of credit for 50% of inventory value. Rates are usually 5 – 15% depending on type of inventory. Get funding within 3 weeks or less. It can’t be lumped together inventory, like office equipment.

But there may be restrictions on the type of inventory you can use. This can include not allowing cannabis, alcohol, firearms, etc., or perishable goods. There can be revenue requirements. There may also be minimum FICO score requirements.

Alternatives to Inventory Financing

There are a number of other ways to get financing for your online business. Your business – and you – have assets beyond inventory. You can tap these assets as collateral. You can use: a 401(k) or IRA, accounts receivable, or stocks or bonds. The 401(k), stocks, or bonds don’t have to be yours. You can work with a partner with these kinds of assets.

Securities-Based Financing

Use existing stocks as leverage to get business financing. Borrow as much as 90% of their value. You continue to earn interest on the stocks pledged as collateral. Closing and funding takes less than 3 weeks.

Rates can be as low as 1.6%. This is a working capital line of credit. You will have challenged personal credit.

Demolish your funding problems with 27 killer ways to get cash for your business.

401(k) Financing

Use your existing 401(k), or IRA as collateral for business financing. This program uses IRS proven strategies. You will pay no tax penalties.

You still earn interest on your 401(k). pay low rates, often less than 5%. Close and fund in less than 3 weeks. You can usually get up to 100% of what’s “rollable” within your 401(k).

Follow these steps. A new corporation is formed; a retirement plan is created to allow for investment into the corporation; funds are rolled over into the new plan. Then the new plan purchases stock in corporation and holds it. The corporation becomes debt free and cash rich.

Accounts Receivable Financing

Use your outstanding account receivables for financing. Get as much as 80% of receivables advanced ongoing in less than 24 hours. The remainder of the accounts receivable are released once the invoice is paid in full. Closing takes 2 weeks or less. Factor rates as low as 1.33%. Accounts receivable credit line with rates of less than 1% with no consumer credit requirement

Receivables should be with the government or another business. If you also have purchase orders, you can get financing to have those filled. You won’t need to use your cash flow to do so.

Amazon Corporate Credit Line

Get revolving or pay in full. You can authorize multiple buyers on a single account and download order history reports and pay by purchase order.

With the pay in full credit line, you get net 55-day billing terms to pay in full with no interest. You can set up primary and secondary accounts for multiple purchasers. And you will get a Dedicated Account Manager.

For the revolving credit line, you can make minimum payments or pay in full monthly. Pay 12.99% purchase APR (the minimum interest charge is $1). You get an option to apply as a personal guarantor to build business credit. And enjoy 24/7 Customer Service.

Amazon Lines of Credit and Working Capital Loans

If your business is eligible, you will see funding options when you log into Seller Central. Currently, lines of credit are offered by Marcus by Goldman Sachs. Loans come from Amazon Lending – specific terms are tailored to the business. Get access to loan funds within 5 days.

Kickfurther

You can finance your next inventory purchase with financing from customers and brand supporters and fundraise directly to them. The way it works is, customers buy through what’s called a Consignment Opportunity. Customers own the products they helped fund until they are sold by the brand. As soon as the products sell, the customer earns payments. Kickfurther also offers an online store for businesses to market and sell their products.

Shopify Capital

With Shopify Capital, you can get 12-month terms. Pay back with a percentage of daily sales. Borrow between $200 and $1 million. The total owed and daily repayment rate depend on risk profile.

OnDeck

OnDeck offers inventory loans and business lines of credit. Term loans runs $5,000 to $250,000, with 12-month terms paid back daily or weekly. Lines of credit run from $6,000 to $100,000. Pay back over 12 months, with automatic weekly payments.

Demolish your funding problems with 27 killer ways to get cash for your business.

Get to know Our Hybrid Credit Line Program

Check out this form of unsecured funding. Unsecured funding does not require collateral, but the lender’s risk is mitigated by higher interest rates. Our credit line hybrid has an even better interest rate than a secured loan. Yet you can get the money faster and easier than any type of traditional funding. Get business funding without having to supply bank statements or credit stubs. You can get funding in a few days rather than weeks without supplying any collateral or documents.

You can get some of the highest loan amounts and credit lines for businesses. Get 0% business credit cards with stated income. No financials required. These report to business CRAs. You can build business credit at the same time. This will get you access to even more cash with no personal guarantee.

You can often get a loan of 5 times the amount of current highest revolving credit limit account. This is up to $150,000. Easily five times what you could get on your own when applying for cards. Get cash out on this program as well.

Advantages

There will be NO impact on your personal credit with this type of financing. You need a good credit score or a guarantor with good credit to get an approval. With good personal credit, get unsecured credit cards with a personal guarantee. And with good business credit, get unsecured credit cards without a personal guarantee.

Check out business credit. It should be your goal to build business credit, even if you can get funding elsewhere. Business credit will help your company for years to come. Business credit is credit linked to your EIN and not your SSN.

This credit is available without a personal guarantee. It is available regardless of personal credit. You can get business credit immediately. Business credit is the only way to get money for a business when you don’t have collateral, cash flow, good personal credit, or a guarantor.

Demolish your funding problems with 27 killer ways to get cash for your business.

Ecommerce Business Inventory Financing: Takeaways

Due to current circumstances, online businesses are doing relatively well. You can get inventory financing for your ecommerce business. Or use personal or business assets as collateral for business loans. Amazon and Kickfurther offer even more options. Our hybrid credit line is a stellar choice if you or a guarantor have good personal credit. And don’t forget to build business credit, for even more money for your ecommerce business.

The post Ecommerce Business Inventory Financing appeared first on Credit Suite.