COVID-19 got you down? It’s not going to last forever. In the meantime, you can build recession business credit. Get a jump on then competition and use this pause in our lives to get ahead. Recession Business Credit for Residential Real Estate Agents and the Rest of Us! Every entrepreneur asks this same question: how … Continue reading Here’s a Great Question from Residential Real Estate Agents: How Do I Build Recession Business Credit

Tag: Great

Get Great Startup Business Credit Cards with No Credit

Are you looking for startup business credit cards with no credit? Check out our top choices.

The Absolute Best Startup Business Credit Cards with No Credit

We researched a lot of business credit cards for you. So, here are our top picks.

Per the SBA, company credit card limits are a whopping 10 — 100 times that of consumer cards!

This shows you can get a lot more funds with small business credit. And it also means you can have personal credit cards at retailers. So, you would now have an additional card at the same shops for your company.

And you will not need collateral, cash flow, or financials to get business credit.

Startup Business Credit Cards with No Credit: Benefits

Perks can differ. So, make sure to choose the perk you prefer from this array of alternatives.

Startup Business Credit Cards with No Credit with 0% APR – Pay Zero!

Bank of America® Business Advantage Travel Rewards World Mastercard® Credit Card

The Bank of America® Business Advantage Travel Rewards World Mastercard® credit card has no annual fee and comes with a 0% introductory APR on purchases for the initial nine months. Thereafter, the card has a 13.24 – 23.24% variable APR

Earn 3 points/dollar spent when you book travel through the Bank of America Travel Center and 1.5 points/dollar on all other purchases. You can get unlimited points and points never expire.

Details

There is a 25,000-point sign-up bonus when you spend $1,000 in the initial 60 days of opening the account. Cardholders get travel accident insurance, and lost luggage reimbursement.

They also get trip cancellation coverage, trip delay reimbursement and other advantages.

There is no introductory rate for balance transfers. Also, bonus categories are limited.

Get it here: https://www.bankofamerica.com/smallbusiness/credit-cards/products/travel-rewards-business-credit-card/

JetBlue Plus Card

Check out the JetBlue Plus Card for yet another offer of a 0% introductory APR

Earn six points/dollar on JetBlue purchases, two points/dollar at dining establishments and grocery stores. And get one point/dollar on all other purchases.

Details

Spend $1,000 in the initial 90 days and pay the annual fee. So, then you can earn 40,000 bonus points. New cardholders get a 12-month, 0% introductory APR on balance transfers made in 45 days of account opening.

Afterwards, the variable APR on purchases and balance transfers is 17.99%, 21.99% or 26.99%, based on creditworthiness. Benefits include a free first checked bag and 50% savings on in-flight purchases.

There is a $99 annual fee for this card.

Get it here: https://cards.barclaycardus.com/cards/jetblue-card/

Startup Business Credit Cards with No Credit for Low APR and Balance Transfers

Discover it® Cash Back

Have a look at the Discover it® Cash Back card. There is a 10.99% introductory APR for six months from date of first transfer. So, this is for transfers under this offer which post to your account by January 10, 2019.

After the introductory APR expires, your APR will be 14.99% to 23.99%. So, this is based on your creditworthiness. Your APR will vary with the market, which is based on the Prime Rate.

Details

You can get 5% cash back at different places each quarter. So, these are places like gas stations, grocery stores, restaurants, Amazon.com, or wholesale clubs. But this is up to the quarterly maximum each time you activate. Plus, automatically get unlimited 1% cash back on all other purchases.

You will get an unlimited dollar-for-dollar match of all the cash back you have gotten at the end of your first year, automatically.

Get it here: https://www.discover.com/credit-cards/cash-back/it-card.html

Startup Business Credit Cards with No Credit with No Annual Fee

Uber Visa Card

Check out the Uber Visa Card. Uber is the very first ride-sharing service to offer a credit card, in a partnership with Visa and Barclays.

The card offers 4% back per dollar spent at restaurants, takeout and bars, including UberEATS. Also, get 3% back on hotel, airfare and vacation home rentals. And get 2% back on online purchases.

So, this includes retailers and subscription services like Uber and Netflix. And get 1% back on all other purchases. Each percent/point has a value of 1 cent. Redeem points for cash back, gift cards or Uber credits directly in the app.

By spending at least $500 in the first 90 days, users can earn a $100 sign-up bonus. Cardholders spending at least $5,000 per year are eligible to receive a $50 credit toward online subscription services.

Details

If you pay your cellular phone bill with this card, you are insured up to $600 for cellphone damage or theft.

Cardholders are eligible for exclusive access to specific events and offers. Uber anticipates the majority of these offers to be available in major cities like New York, San Francisco, Los Angeles, Chicago and DC. There is no foreign transaction fee.

But there is no introductory rate. So, the APR is a variable 16.99%, 22.74% or 25.74%, based on your creditworthiness. Cardholders with less than stellar credit will be on the higher end of the range.

Also, there are restrictions on Uber credits. To redeem points as credits within the Uber app, accrue a minimum of 500 points, or $5. Cardholders can convert a maximum of 50,000 points, or $500, per day.

Get it here: https://www.uber.com/c/uber-credit-card/

Costco Anywhere Visa® Business Card by Citi

Not taking Uber? Then you’ll need to fill your gas tank somehow. Why not do so with the Costco Anywhere Visa® Business Card by Citi?

This card earns cash back with every purchase. Earn 4% cash back on the first $7,000 spent on eligible gas purchases annually (1% after that). Get 3% cash back at restaurants and on eligible travel purchases. Also, get 2% cash back at Costco and Costco.com. And earn 1% cash back on all other purchases.

So, note: the $0 yearly fee is only for Costco members. And an active Costco membership is required. Cardholders will get access to damage and theft purchase protection, extended warranty coverage and travel accident insurance.

Also, there is no sign-up bonus offered with this card.

Get it here: https://www.citi.com/credit-cards/credit-card-details/citi.action?ID=Citi-costco-anywhere-visa-business-credit-card

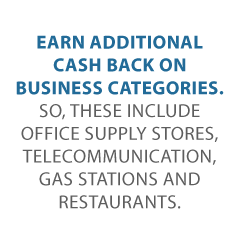

Ink Business Cash℠ Credit Card

Consider the Ink Business Cash ℠ Credit Card. Companies can get cash back with each purchase. Spend $3,000 in the initial three months from account opening. And you’ll earn a $500 bonus cash back.

There is a $0 yearly fee with a 0% introductory APR for 12 months on purchases and balance transfers. Thereafter, the APR is a 15.24 – 21.24% variable.

The credit card comes with travel and purchase coverage benefits. So, this includes an auto rental collision damage waiver and extended warranty protection.

Details

Earn additional cash back on business categories. So, these include office supply stores, telecommunications, gas stations and restaurants.

Note: this credit card has a balance transfer fee. Pay 5% of the amount transferred or $5, whichever is greater. Also, there is a foreign transaction fee of 3%.

Get it here: https://creditcards.chase.com/small-business-credit-cards/ink-cash

United MileagePlus Explorer Business Card

Get a good look at the United MileagePlus Explorer Business Card.

Earn 2 miles/dollar with United and at restaurants, filling stations and office supply stores. All other purchases earn 1 mile/dollar. Earn a 50,000-mile sign-up bonus after spending $3,000 in the initial three months from account opening.

Benefits include priority boarding, a free first checked bag for you and a companion on the same reservation.

Details

Also, get two United Club passes annually. And get hotel and resort perks including upgrades. In addition, get early check-in and late checkout. And get an auto rental collision damage waiver.

Plus, get baggage delay insurance, lost luggage reimbursement, trip cancellation and interruption insurance. Finally, get trip delay reimbursement, purchase protection, price protection and concierge service.

After the first year, the card has an annual fee of $95. APR of 17.99% – 24.99%, based on creditworthiness.

Get it here: https://creditcards.chase.com/small-business-credit-cards/united-mileageplus-explorer-business

Starwood Preferred Guest® Business Credit Card from American Express

Another choice is the Starwood Preferred Guest Business Credit Card from American Express.

This card is for those who stay at Starwood Preferred Guest and Marriott hotels often. Earn six points per dollar of eligible purchases at participating SPG and Marriott Rewards hotels.

And get four points per dollar at US restaurants, American gas stations, and on American purchases for shipping.

Also, earn four points to the dollar on wireless telephone services purchased directly from US service providers. For all other eligible purchases, get two points per dollar.

Details

Earn 75,000 bonus points when you spend $3,000 in the first three months of account opening. Benefits include free in-room premium internet access, Sheraton Club lounge access, and purchase protection.

Plus, you get car rental loss and damage insurance. And you get baggage insurance. There is also a global assistance hotline. And there is a roadside assistance hotline. And get travel accident insurance and extended warranty coverage.

The most significant issue is the annual fee. There is a $0 introductory annual fee for the first year, then it’s $95 afterwards. Plus, there is no 0% introductory APR. Instead, there is a 17.74 – 26.74% variable APR

Get it here: https://www.americanexpress.com/us/credit-cards/business/business-credit-cards/spg-amex-starwood-credit-card

Startup Business Credit Cards with No Credit for Average Credit

Capital One® Spark® Classic for Business

For average credit, we like the Capital One Spark Classic for Business. It has no annual fee. There are cash-back rewards. The card earns an unlimited 1% cash back on all purchases. There is an annual fee of $0.

With this card, you will get benefits including an auto rental collision damage waiver, and purchase security. And you also get extended warranty coverage. And you get travel and emergency assistance services.

But KEEP IN MIND: the ongoing APR is 24.74% variable APR. And the penalty APR is even higher, 31.15%. Also, there is no sign-up bonus. In addition, this card reports monthly to personal credit. It does report to business credit as well, but they generally require a personal credit check and will always report to personal credit.

Get it here: https://www.capitalone.com/small-business/credit-cards/spark-classic/

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

Startup Business Credit Cards with No Credit for Luxurious Travel Points

Capital One® Spark® Miles for Business

Be sure to check out the Capital One® Spark® Miles for Business card. With this card, you can earn 2 miles per dollar on all purchases. When you spend $4,500 within the first 3 months of opening an account, you can earn 50,000 miles. So, that is worth $500 in travel.

Benefits for cardholders include an auto rental collision damage waiver, and purchase security. And they also include extended warranty coverage. And you get travel and emergency assistance services.

Cardholders will pay $0 introductory for first year. But they will pay $95 after that for the annual fee.

There is no 0% APR for purchases or balance transfers with this card. The APR is 18.74% (variable).

Get it here: https://www.capitalone.com/small-business/credit-cards/spark-miles/

IHG ® Rewards Club Premier Credit Card

Have a look at the IHG ® Rewards Club Premier Credit Card. it earns hotel rewards worldwide. For every dollar spent at participating IHG hotels, get 10 points. Get two points per dollar spent at gas stations, grocery stores and restaurants.

And all, other purchases earn one point. New cardholders can earn an 80,000-point sign-up bonus when they spend $2,000 in the first three months of account opening.

Details

This card provides a free one-night hotel stay annually. Plus, there is a variety of benefits like travel and purchase coverage and an upgrade to Platinum Elite status with the IHG Rewards Club. The club offers complimentary room upgrades when available and guaranteed room availability.

The biggest issue is that the card does not offer a zero percent APR introductory rate. And the standard APR is 17.99 – 24.99% variable. Also, the annual fee is $89.

Get it here: https://creditcards.chase.com/a1/ihg/premiernaep

Marriott Rewards® Premier Plus Credit Card

This card earns six points/dollar spent at participating Marriott and SPG hotels. And get two points/dollar on all other purchases.

Spend $3,000 in the initial three months from account opening and get two free night awards (each valued up to 35,000 points).

Cardholders get access to perks including a free one-night stay every year after account anniversary. Also get travel and purchase protection. So, this includes free standard in-room Wi-Fi and priority late checkout.

Details

Perks include baggage delay reimbursement, and lost luggage reimbursement. There is also trip delay reimbursement. And there is purchase protection. Plus, there are concierge service and automatic Silver Elite status, which includes a 20% bonus on points.

Spend $35,000 each account year and get an upgrade to Gold Elite status. So, that includes a complimentary room upgrade, free daily breakfast and 4 PM late checkout.

There is an annual fee of $95. The APR is a 17.99– 24.99% variable.

Get it here: https://creditcards.chase.com/marriott/apply

Startup Business Credit Cards with No Credit to Build Credit

Discover it® Student Cash Back

Make sure to have a look at the Discover it® Student Cash Back card. It has no yearly fee. The credit card also offers a six-month introductory period of 0% APR on purchases. And there is an APR of 14.99 – 23.99% variable on all purchases after that period.

One special feature is that it provides an incentive for scholars to maintain good grades with a $20 statement credit. If students earn a GPA of 3.0 or higher each school year, the card will award the $20 statement credit every year for up to five years.

Details

Use this credit card to build personal credit. While this is a personal credit card versus a company card, for new credit users, their FICO scores will be vital. And this credit card provides an outstanding way to raise FICO while also getting rewards. Better personal credit can also, often, be the key to unlocking online lending.

You can earn 5% cash back at different places each quarter like grocery stores, gas stations, restaurants or Amazon.com up to the quarterly maximum. After that, this card offers unlimited 1% cash back on all purchases.

In the first year, all cash back rewards are matched 100%.

Downsides include a cash advance fee of either $10 or 5% of the amount of each cash advance, whichever is more. And even though they waive the first late payment fee, a fee of up to $37 applies on all other late payments. There is also a returned payment fee of up to $37.

Get it here: https://www.discover.com/credit-cards/cash-back/it-card.html

Startup Business Credit Cards with No Credit for Cash Back

SimplyCash Plus Business Credit Card from American Express

Check out the SimplyCash Plus Business Credit Card from American Express. There is a $0 yearly fee. And there is a 0% APR on purchases. So this is for the initial 15 months an account is open.

But when the introductory period expires, the APR for purchases is 14.24 to 21.24%. So, this is variable and based on creditworthiness.

Details

This credit card has several benefits. These include purchase protection, car rental loss and damage insurance. And they also include a baggage insurance plan, extended warranty coverage and a global assist hotline.

Also, earn 5% cash back at US office supply stores and on wireless phone services. So, these must be bought from United States providers. But this pertains to the initial $50,000 of yearly spending. Then, you earn 1% cash back.

You also get 3% cash back on spending category of your choice. So, this is from eight distinct categories. They include airfare, gas, advertising and computer purchases. But it applies to the first $50,000 of yearly spending. Then, you earn 1% cash back.

Cash-back bonuses are automatically credited to the customer’s billing statement.

Note: you cannot use this credit card for balance transfers. There is a foreign transaction fee of 2.7%. The card charges up to $38 in late fees. And the returned check fee is also $38. The penalty APR is 29.99%.

And, it kicks in if you have two or more late payments within 12 months. It can also apply if you fail to make the minimum payment on time or have a returned payment.

Get it here: https://www.americanexpress.com/us/small-business/credit-cards/simply-cash-plus-business-credit-card/44279

Capital One® Quicksilver® Card

Look at the Capital One® Quicksilver® Card. It offers flat-rate rewards of 1.5% on all purchases. There are no limits to the amount of cash back rewards that cardholders can earn. Also, the card has a $0 yearly fee.

New cardholders have a 0% APR on purchases and balance transfers for the first 15 months after opening the account. And after that they have a 14.74 – 24.74% (variable) APR after that.

A cash bonus of $150 is available for those who make at the very least $500 in purchases in 3 months of account opening.

Details

Also, cash back rewards do not expire for the life of the account. And there is no limit to how much you can earn.

This credit card also offers travel accident insurance. And you get an auto rental collision damage waiver. There are no foreign transaction fees. And there is extended warranty coverage.

Downsides are the flat reward rate, not allowing for any more than that. And the higher APR after the first 15 months.

Get it here: https://www.capitalone.com/credit-cards/quicksilver/

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

Startup Business Credit Cards with No Credit (Secured)

Wells Fargo Business Secured Credit Card

Check out the Wells Fargo Business Secured Credit Card. It charges a $25 annual fee per card (up to 10 employee cards). It also requires a minimum security deposit of $500 (up to $25,000) and it is meant to help cardholders set up or rebuild their credit.

Pick this credit card if you want to get 1.5% per dollar in purchases with no limits or earn one point for every dollar in purchases. You also earn 1,000 bonus points for every month your company makes $1,000 in purchases on the card.

Details

Also, you get free FICO scores every month. There are no foreign transaction fees. It is possible to upgrade to unsecured credit. Your account is regularly reviewed. And you may become eligible for an upgrade to an unsecured card with responsible use over time. Approval is not guaranteed and depends on factors including how you manage this and your other accounts.

APR is the current prime rate plus 11.90%. There is no introductory APR period and no sign-up bonus. This is not a card for balance transfers.

Get it here: https://www.wellsfargo.com/biz/business-credit/credit-cards/secured-card/

Startup Business Credit Cards with No Credit for Jackpot Rewards

Chase Sapphire Preferred® Card

Have a look at the Chase Sapphire Preferred® Card for travel points.

You can earn two points to the dollar spent on travel and dining at restaurants. And you can get one point per dollar on all other purchases. Points can be redeemed for cash back, gift cards, or travel.

The card’s benefits include trip cancellation insurance, travel and emergency assistance services. They also include an auto rental collision damage waiver, purchase protection and extended warranty protection.

When you spend $4,000 in the initial 3 months from account opening, you will get 50,000 bonus points. These points are worth $625 if you redeem them for travel through Chase Ultimate Rewards.

Details

You can earn an unlimited two points per dollar for travel and dining at restaurants. Then afterwards get one point per dollar for all other purchases. Points will transfer equally to 13 leading frequent travel programs with partners. So, these include British Airways, Southwest Airlines, United, and Marriott.

There is no 0% introductory APR on purchases or balance transfers. The card’s standard APR is 17.74 – 24.74% variable. Also, the card has an annual fee of $0 introductory for the first year. And then it skyrockets to $95.

Get it here: https://creditcards.chase.com/rewards-credit-cards/chase-sapphire-preferred

Ink Business Preferred ℠ Credit Card

Get a look at the Ink Business Preferred Credit Card from Chase. Cardholders earn 3 points for every dollar spent on travel, shipping, internet, cable, phone and qualifying advertising with the card. So, this is up to $150,000 each year. And all other purchases earn an unlimited one point per dollar spent.

This is a Visa card.

Cardholders get benefits like purchase protection, trip cancellation or interruption insurance. They also get cellphone protection. And they get extended warranty coverage. And they get an auto rental collision damage waiver.

Details

Earn 80,000 bonus points when you spend $5,000 in the initial 3 months from account opening. There is an annual fee of $95. You can add employee cards at no additional cost.

This card only offers 3 points per dollar to a limit of $150,000 a year. So, this is for travel, shipping, internet, cable, phone and qualifying advertising. All other purchases earn an unlimited flat rate of one point per dollar. And there is no introductory APR

Get it here: https://creditcards.chase.com/small-business-credit-cards/ink-business-preferred

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

The Perfect Startup Business Credit Cards with No Credit for You

Your absolute best company credit cards hinge on your credit history and scores.

Only you can pick which features you want and need. So, make sure to do your homework. What is excellent for you could be disastrous for other people.

And, as always, make certain to establish credit in the recommended order for the best, quickest benefits.

The post Get Great Startup Business Credit Cards with No Credit appeared first on Credit Suite.

Get Great Startup Business Credit Cards with No Credit

Are you looking for startup business credit cards with no credit? Check out our top choices. The Absolute Best Startup Business Credit Cards with No Credit We researched a lot of business credit cards for you. So, here are our top picks. Per the SBA, company credit card limits are a whopping 10 — 100 … Continue reading Get Great Startup Business Credit Cards with No Credit

Great Generation Z Marketing and More –10 Brilliant Business Tips of the Week

Looking for Generation Z marketing tips? We’ve got those and more this week for our ten brilliant business tips of the week. Find out how to reach the generation after the millennials.

The Hottest and Most Brilliant Business Tips for YOU – Grab Some Great Generation Z Marketing Tips and More

Our research ninjas at Credit Suite smuggled out ten amazing business tips for you! Be fierce and score in business with the best tips around the web. You can use them today and see fast results. You can take that to the bank – these are foolproof! Take your Generation Z marketing to the next level – and more!

Stop making stupid decisions and start powering up your business. Demolish your business nightmares and start celebrating as your business fulfills its promise.

And these brilliant business tips are all here for free! So, settle in and scoop up these tantalizing goodies before your competition does!

#10. Better Bonuses? Yes, Please!

Our first jaw-dropping tip is all about building an effective bonus plan. Because who doesn’t love bonuses? Great Game says bonuses need to have a connection to the goals of the business. And the time for being secretive and mysterious about them is over.

Here’s our fave tip.

Rally Everyone Around a Common Goal

So, how many times have you worked for (or heard of) a company where the only bonuses went out to people who made sales? Or who could prove their contributions cost less than what they brought in?

Good golly, that’s unfair. But why?

Because there are plenty of disciplines which are fully important to business operations. But they are cost rather than profit centers. After all, where can human resources show a profit? What about loss prevention?

And the clerical staff or the front-line factory workers? Fuggeddabout it. They will never see a bonus under these circumstances. By definition, they can’t.

So, where’s the incentive for them?

Communications Are Key

Now, this is true under most circumstances, anyway. But if a person who did really well for the company can’t get a little public recognition, then who can? Or should?

And in particular, if your employees need to meet some sort of quota or goal, let them know how they’re doing. How close are they? And how much further do they have to go? Is it possible for them to meet their goal, or not? Knowing they’re close might help some workers work just that much harder to meet their goal. And if you keep them informed early and often, some might not get discouraged if they are a little behind.

So, don’t just leave the feedback to the last minute.

#9. Grab Your Advantage and Become a Market Leader

The next awesome tip is about lower risk innovation which can help you become a market leader. Entrepreneurs’ Organization notes you should get started with ‘jobs to do’. That is, understand what your product actually does for your customers.

This gets into a bigger theme we’ve noticed for a while.

Let Your Customers Take the Reins

The biggest thing we have learned while writing these marketing posts is to listen to your customers.

Listen to your customers.

Let’s repeat that.

Listen to your customers. They know what they want. And it may not be what you think they should want.

It’s time for a true story. And it’s a new one. As in, this just happened this morning.

Please Don’t Treat Me Like Everyone Else

So, I am not in Generation Z. Heck, there are plenty of places which say I’m not even Gen X, although I tend to act and consume like that cohort. For the record, I’m ‘officially’ a late boomer. Birth date in 1962, yo’.

But I digress. I am on Twitter, and I tend to follow fellow writers. This morning, a profile I recently filed sent me a generic DM with their links and all. At least they had the foresight to call me by name. But it was my full name on Twitter.

Anyone who thinks their program scraped my name from the appropriate Twitter field, give yourself a cookie.

That was the sole attempt at personalization.

So, I sent them a return PM. And I told them in no uncertain terms that their DM was tone-deaf, generic, and clearly mass-produced. I also told them that if they didn’t have the time to get more personal with their intended audience, then they either need an assistant or they’re trying to be all things to all people.

And, let’s face it. I am most likely not in their target audience. The writing community reads, yes. But our Holy Grail is to find readers.

The person who DM’d me was savvy and gracious enough to thank me for my thoughts. And so, in return, I apologized for being harsh.

Smart Move on the Part of the Marketer

The kicker is that the writer, in this case, absolutely salvaged the situation. Will this person change their ways? Maybe. I have no idea. But they were wise enough to acknowledge my opinion and, dare I say, treat me like an individual.

By listening to your audience, your customers and your prospects, you are treating them like people and not a monolith. And that’s not just good for marketing to the post-millennial generation.

If you are as passionate about succeeding in business as we are, please help us spread the word about how to take the plunge and save time and money – and your sanity! Start Generation Z marketing today, and more!

#8. Up with Productivity; Down with Stress!

Our following life-changing tip concerns lowering your stress levels. Score lays it all out for us. And be sure to check tip #7, which is also about combatting stress.

But first, let’s tackle productivity. After all, it can be extremely stressful when you don’t seem to be able to get everything done on time. And beyond that, if you’re constantly getting everything done after hours, that will take a lot out of you physically. Not to mention, it could interfere with parenting or even threaten your marriage.

There were some great tips here, but we’ll just focus on one.

Om Shanti – Meditate Your Way to Less Stress

You don’t need to climb a mountain and meet a yogi. Rather, you can just download a meditation app onto your phone or computer. The main point of meditation is to train your mind to essentially go to a ‘happy place’, even if everything else around you is going to hell in a handbasket.

This doesn’t mean you ignore your problems. It’s more that you are able to approach them more dispassionately. That can make it easier to solve them.

Consider this. It’s a lot like listening to your friend’s problems with their love life, and you have the solution on the spot. But when it comes to your own issues, you’re stumped. Well, sure, because you’re too close to those problems.

Stepping back could be the key to seeing solutions all the more clearly – and faster. What better way to increase productivity than to lessen the amount of time you spend fixing stuff?

#7. Banish Your Financial Stress in 2020

For our next sensational tip, we looked at financial stress in your business, and how to minimize if not outright omit it. Small Biz Club says that over half of all entrepreneurs say debt is a problem.

But you may be asking, don’t you advocate carrying debt here at Credit Suite?

Not exactly.

In reality, we advocate building and leveraging credit. But we also feel you should never bite off more credit you can ‘chew’. Being incapable of paying your business debts is hardly the definition of success.

While this article is mainly about personal finances, we suggest checking it out anyway. Many issues with personal financial stressors are similar to business finance stressors.

In particular, if there’s more than one owner of your company, be open and honest with each other about money. Your business’s survival will depend on your open communications in this area, so don’t clam up about business cash.

#6. Soothe Those Ruffled Feathers

This tip is so helpful, and it works! Inc tells us all about dealing with difficult customers.

Talk about your stressors!

We highly recommend reading the entire article, as it offers a good framework for this inevitable issue. Hence, let’s talk about one tip which really stands you in good stead with difficult customers. Heck, it should help you in your relationships.

Seriously.

Own Up, Apologize, Address, and Resolve

These are actually two separate tips, but we feel they’re related closely enough to talk about them together.

For any issue in life, you can cover it up and deny it. Or you can own up to it. So, if you did it – whatever it is – say you did. Of course, we all have egos. And we don’t necessarily enjoy or want to confess to our mistakes. But they are going to come out, sooner or later.

Admit to them and you’ll be able to control at least a small part of the narrative.

And then apologize.

“I took the last cookie. I’m sorry.”

Then address the issue. It’s not just an admission of guilt that’s necessary. You should also be working to prevent a recurrence.

“I took the last cookie. I’m sorry. I’ll make sure we keep cookies permanently on our shopping list, so we don’t run low again.”

Finally, resolve the issue, as soon as you can.

“I took the last cookie. I’m sorry. I’ll make sure we keep cookies permanently on our shopping list, so we don’t run low again. This afternoon, I’ll go to the store and get more.”

There, now, that wasn’t so bad, now.

#5. Learn All About Generation Z Marketing

Grab this mind-blowing tip while it’s hot!

Go beyond the millennial generation and get into Generation Z marketing!

Manta says this generation is going to become 40% of all consumers by year 2020.

Wait a second – that’s this year.

Now, you may be saying to yourself – Generation Snowflake is still a bunch of kids. They aren’t interested in my widgets. Not so fast. Per Wikipedia, the post-millennial generation was born between the mid- to late-90s to, well, they’re not sure when. 2010 seems to come up a lot as the endpoint. But so do 2012 and 2014.

And no, we don’t know what the post-Generation Z cohort is going to be called, either.

That means the eldest among them are turning 25 this year. So, these are people who can drive, vote, drink, join the armed forces, and marry. They’re already done with their bachelor’s degrees (if they have them). They may even be past a master’s degree by now. And they may be parents by now – more than once.

For Generation Z Marketing, Find Out What They’re All About

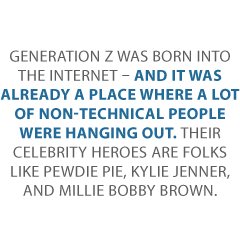

Generation Z was born into the internet – and it was already a place where a lot of non-technical people were hanging out. Their celebrity heroes are folks like Pewdie Pie, Kylie Jenner, and Millie Bobby Brown.

How Do You Get Started with Generation Z Marketing?

Start with shareworthy content. That’s easier said than done, though.

Catchy information with a high level of expertise is a great place to start.

Another tip we really liked was to share your content in bits. For one thing, this cohort has an average attention span of – gulp – 8 seconds. Perfect for Twitter, eh?

So, instead of sharing the entire article (like this one), a better tactic for Generation Z marketing is to just refer to tip #5 in one tweet. And then tip #10 in another tweet. Then, feature tip #3 in an Instagram post. You get the idea.

Oh, and share user-generated content. And if you can convert your content to video, do so.

Is this perfect for Generation Z marketing? Maybe not. But it’s a dang fine start.

If you are as passionate about succeeding in business as we are, please help us spread the word about how to take the plunge and save time and money – and your sanity! Start Generation Z marketing today, and more!

#4. Up Your Business Growth with Terrific Online Listings

Check out this spectacular tip, all about leveraging your online listings to help your business grows. Succeed as Your Own Boss notes that how you list products and services online can make a difference when it comes to sales.

And, we might add, when it comes to search.

As is often the case, we highly recommend reading this article in its entirety. But one tip really stood out to us.

Tell Your Product’s (or Service’s) Backstory

What does that mean?

In fiction, it’s the history of your character, before the book or series started. In fiction writing and presentation on TV and film, the backstory is generally better told in pieces. Otherwise, it rightfully feels like an information dump.

But in your online sales listings, you kind of have to. So, our suggestion is to do this, but also to edit the heck out of it. Consider your Generation Z customers and, really, all of us. After all, everyone is busy, and we are all bombarded with information all day long.

Hence, you probably shouldn’t be writing about how your widgets are locally sourced, unless you can spread that story out across several pages. Maybe the first bit of the production process can be a part of the online listing for one product, and then the second step can end up on the online listing for another.

Experiment!

#3. You Can Lead a Prospect to Your Business…

It’s not your imagination: this winning tip can help you with lead generation. United Capital Source tells us that generating low-quality leads is a surefire way to basically just waste money and time. And, probably, the goodwill and energy of your sales staff.

Hence the article is devoted to various forms of lead generation. We recommend reading it in its entirety as one or the other of their strategies may work for you. Hence, we’re only going to zero in on one of their tactics.

Swap Leads with a Partner

This makes so much sense, and we are kind of surprised we haven’t seen anything like this before!

That is, get to know noncompeting businesses which serve the same demographic niche(s) you do. Their leads could work as your leads, and vice versa.

So, let’s say you have a nail salon, but you don’t do hair. There’s nothing wrong – and a lot right – with talking with nearby hair salon owners and seeing if you can do a lead trade. It will probably be beneficial to both of you.

And you’re not left out if you offer services! If you have a long-haul trucking company, there may be freight companies with a similar lead profile. After all, if a business knows it needs shipping of some form, it may start with air or rail. But then they would quickly realize that there also has to be good, reliable, and fast ground transportation to complement those methods.

So, look for the jam to your peanut butter. And you might just create a partnership in other areas, like sponsoring a local Little League team or running a conference together or – whatever!

#2. Go and Get More Done

Our second to last unbeatable tip can give you a new perspective on multitasking while on the go. Addicted to Success reveals all about stretching the hour, almost like some people stretch a dollar.

Now, multitasking gets a bad rap at times, because it’s sometimes a not so efficient way to get things done. So, we’d like to concentrate on one tip which just might help save the planet.

Rethink Your Commute

Unfortunately, not every area allows for this. But for those that do, why not use public transportation to get to the office? Yes, the bus is probably not as fast as your car – and you’re beholden to their schedule.

But if you can make it work, having someone else do the driving means your time can be spent on something else. And, it just may be less stressful. Commuting time will never come back to you, so you may as well make the most of it.

Plus, we think there are a few things you can do which the article didn’t go into.

First, could you carpool? Maybe just one day per week to start. Save gas and spend time with someone, maybe someone on your team. You can meet, after a fashion. Or just spend time together quietly sitting or even having some fun. Getting to know your colleagues better is probably not a bad thing.

And another idea is, if it’s safe and feasible, how about bicycling to work? We all know that more aerobic exercise is good for us. You may even live longer. Bring a change of clothes – don’t wear your good clothes to bike. No good bike paths or bus routes by you? Then talk to your local government.

Because you may not be the only person who wants to change their commute.

#1. Hire the Right People, the First Time – and Keep Them

We saved the best for last. For our favorite remarkable tip, we focused on developing and keeping top talent. HBR says keeping top talent is an ongoing process. You don’t just offer (for example) a company gym. You give your best people a chance to better develop themselves.

This kind of individual treatment is what we’ve been advocating for customers and prospects, too.

Treat people like they were the only person in the world. What a concept.

So, which one of our brilliant business tips was your favorite? And which one will you be implementing now?

If you are as passionate about succeeding in business as we are, please help us spread the word about how to take the plunge and save time and money – and your sanity! Start Generation Z marketing today, and more!

The post Great Generation Z Marketing and More –10 Brilliant Business Tips of the Week appeared first on Credit Suite.

Get Small Loans For Your Business the Easy Way With a Great Bank Rating

Even small loans can be challenging without a great bank rating. Learn why this little-known number matters, and how you can improve yours.

Need Small Loans for Your Business?

Even the search for small loans can be a recipe for frustration if you aren’t ready and don’t take the time to build your bank credit score. But what’s a bank credit rating, anyway?

Your Bank Credit Score – What’s it All About?

Do you know the distinction between bank credit scores and small business credit?

Company credit is the full and complete amount of money that your business can get from all manner of creditors. That means the banking system, credit unions, credit card companies, and also leasing firms. And it also means providers, under what’s called trade credit or vendor credit or trade lines. That is, the vendor credit tier.

A bank credit rating, on the other hand, is a measure of the full amount of borrowing capacity which a business can get from the banking system only.

Bank Credit Scores Clarified

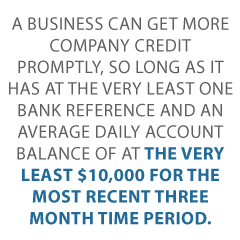

A business can get more company credit promptly, so long as it has at the very least one bank reference and an average daily account balance of at the very least $10,000 for the most recent three month time period. This setup will generate a bank credit score of a Low-5. So this means it is an Adjusted Debt Balance of from $5,000 to $30,000.

A lower rating, like a High-4, or balance of $7,000 to $9,999 will not instantly turn down the small business’s loan application. Nevertheless, it will slow down the approval process.

What is a Bank Score?

A bank rating is a measure of the average minimum balance as kept in a business bank account over a 3 month long period. Hence a $10,000 balance| will rank as a Low-5, a $5,000 balance will rank as a Mid-4. So a $999 balance will rate as a High-3, etc.

A company’s chief objective should always be to maintain a minimum Low-5 bank rating (or, an average $10,000 balance) for at least three months. This is because, without a minimum of a Low-5 score, most banks will operate under the assumption that the business has little to no capacity to pay off a loan or a business line of credit.

But there is one thing to remember: you will never actually see this number. The financial institution will simply keep this number in its back pocket.

The Bank Score Ranges

The numbers work out to the following ranges:

To get a High-5 score, your company will need to have an account balance of $70,000 to $99,999. For a Mid-5 score, your business must have an account balance of $40,000 to $69,999. And for a Low-5 rating, your business needs to hold onto an account balance of $10,000 to $39,000. So your company needs this level bank score or better to get a bank loan.

For a High-4 score, your company has to have an account balance of $7,000 to $9,999. And for a Mid-4 rating, your small business must maintain an account balance of $4,000 to $6,999. So for a Low-4 score, your small business will need to have an account balance of $1,000 to $3,999.

Ruining Your Bank Score

Unfortunately, there are a lot of ways to really destroy your bank rating. Here are 7 – and how you can fix them in order to get small loans or really any level of financing.

7th Way to Ruin Your Bank Credit Score and Lose Out on Small Loans

Do not maintain a minimum balance for a minimum of three months. Given that every bank rating cycle is based on the previous 3 months, a continuously seesawing balance ought to damage your bank score.

6th Way to Destroy Your Bank Credit

Don’t bother to ensure that your business bank accounts are reported precisely the same way as all of your small business documents are, as well as with the exact same physical address (no post office box) and telephone number. Sow confusion here by editing one and not another, or not remedying an error if there is one.

Small Loans

Check out our professional research on bank ratings, the little-known reason why you will – or won’t – get a get a bank loan for your business.

5th Way to Destroy Your Bank Credit and Lose Out on Small Loans

To accompany #6, do not see to it that each and every credit agency and trade credit supplier also lists the business name and address the precise same way. This is every keeper of financial documents, earnings and sales taxes, internet addresses and e-mail addresses, directory assistance, and so on.

No loan provider is going to stop to consider the myriad manners in which a business might be listed, when they explore the business’s creditworthiness. For this reason if they are not able to locate what they need quickly, they will either deny an application or it won’t be reported to a business credit reporting agency such as Experian, Equifax or Dun & Bradstreet.

Therefore, if they are not able to discover what they need quickly, they will just reject the application. So see to it your records are a mess!

4th Way to Damage Your Bank Credit Score

Never manage your bank account responsibly. This means that your small business must not avoid writing non-sufficient funds (NSF) checks at all costs, because those annihilate bank ratings. Non-sufficient-funds checks are something which no business can afford to let happen.

Balancing checkbooks and accounts is so dull anyway. You’ve got adequate money without even making sure, right?

3rd Way to Destroy Your Bank Credit Rating and Lose Out on Small Loans

To add to #4, do not include overdraft protection to your bank account ASAP, in order to avoid NSFs. Why bother thinking in advance or preparing for the future? Everything is going to be fantastic forever, right?

Writing checks insufficient funds (NSFs) is a sure way to destroy your bank score.

2nd Way to Damage Your Bank Credit Score

Do not let your small business show a positive cash flow. The cash coming in and leaving your business’s bank account must show a positive free cash flow.

A positive free cash flow is the quantity of profits left over after a business has paid every one of its expenses. According to Investopedia, it “represents the cash a company can generate after required investment to maintain or expand its asset base. It is a measurement of a company’s financial performance and health.”

When an account shows a positive cash flow it indicates your small business is producing more earnings than is used to run the business. That means the financial institution will feel your company can pay its expenses.

So if you actually intend to trash your bank score, get whatever’s expensive for your business so your expenses overtake your profits. Doesn’t every manufacturing facility deserve plush carpeting in the loading dock?

Small Loans

Check out our professional research on bank ratings, the little-known reason why you will – or won’t – get a get a bank loan for your business.

1st Way to Ruin Your Bank Credit and Lose Out on Small Loans

Financial institutions are extremely motivated to lend to a company with consistent deposits. And a business owner should also make regular deposits in order to preserve a positive bank score. The business owner needs to make several regular deposits, greater than the withdrawals they are making, in order to have and preserve a good bank rating. If they can do that, then they will have a great bank credit rating.

Consistency is the hobgoblin of little minds, right? So be a free spirit!

Damage Your Business’s Bank Score and Losing Out on Small Loans – Even Though You Will Never See This Number

You, the entrepreneur must never make regular deposits. And these deposits ought to never be more than the withdrawals you are making, in order to ruin your bank credit rating.

If you can do these things, then your company will have a dreadful bank credit rating. And, subsequently, a bad bank credit rating means your firm is far less likely to get small business loans.

Just Kidding: Obviously We Do Not Really Want You to Miss Out on Small Loans!

So, where do you go from here?

The First Great Way to Rescue Your Bank Credit Score

Possibly the most convenient way to attain and maintain a good bank credit is to deposit at least $10,000 into your small business bank account and maintain it there for as much as a half year. While you will still have to make consistent deposits, this one straightforward step will aid in 3 ways.

One, you will have maintained an excellent minimum balance for at the very least three months. Two, you will probably not overdraw with such an excellent balance. And three, you will get to the magic minimum for a Low-5 bank credit rating. Hence you will be dealing with our #4 and #7, above.

And you might even have the ability to get around our #3. But we still highly recommend overdraft protection.

The Second Wonderful Way to Rescue Your Bank Credit Rating

A 2nd need is to make sure your small business account details are consistent across the board, all over. While it might take some work order to ensure everything is right, you will be taking care of #5 and #6, above.

The Third Great Way to Rescue Your Bank Credit

A third necessity is to make regular deposits. And make certain they are more than the quantities you are withdrawing every month. This will take care of our #1 and #2 smoothly.

Takeaways for Your Bank Credit Rating and Small Loans

Your bank rating is not to be trifled with. Although the financial institutions maintain a secret regarding them, failing to keep your bank credit rating high will make it a great deal harder to do well in business. You might not even get small loans, so be diligent!

Check out our professional research on bank ratings, the little-known reason why you will – or won’t – get a get a bank loan for your business.

The post Get Small Loans For Your Business the Easy Way With a Great Bank Rating appeared first on Credit Suite.

Mux is hiring great people to keep building the best dang video infra on the web

Article URL: https://mux.com/jobs?a=1

Comments URL: https://news.ycombinator.com/item?id=20660005

Points: 1

# Comments: 0

Check Out This Great Question from Residential Real Estate Agents: How Do I Build My Business Credit?

How Do I Build My Business Credit? Residential Real Estate Agents Ask This Question All the Time

Every entrepreneur asks this same question: how do I build my business credit?

Business credit is credit in a company’s name. It doesn’t link to a business owner’s consumer credit, not even when the owner is a sole proprietor and the sole employee of the company.

As such, a business owner’s business and consumer credit scores can be very different.

How Do I Build My Business Credit and Get The Advantages?

Due to the fact that business credit is separate from individual, it helps to safeguard a business owner’s personal assets, in the event of a lawsuit or business insolvency.

Also, with two distinct credit scores, a small business owner can get two separate cards from the same merchant. This effectively doubles purchasing power.

Another advantage is that even new ventures can do this. Going to a bank for a business loan can be a recipe for disappointment. But building small business credit, when done properly, is a plan for success.

Consumer credit scores rely on payments but also other components like credit utilization percentages.

But for company credit, the scores actually only hinge on if a business pays its invoices on time.

How Do I Build My Business Credit and Start The Process?

Growing company credit is a process, and it does not occur automatically. A small business has to proactively work to establish business credit.

However, it can be done readily and quickly, and it is much swifter than establishing consumer credit scores.

Merchants are a big part of this process.

Doing the steps out of order will lead to repetitive rejections. Nobody can start at the top with company credit. For example, you can’t start with retail or cash credit from your bank. If you do, you’ll get a rejection 100% of the time.

How Do I Build My Business Credit and Get Started with Small Business Fundability?

A small business needs to be fundable to lenders and vendors.

Hence, a business will need a professional-looking website and e-mail address. And it needs to have site hosting bought from a supplier like GoDaddy.

And also, company phone and fax numbers ought to have a listing on 411.com.

At the same time, the company phone number should be toll-free (800 exchange or comparable).

A business will also need a bank account dedicated solely to it, and it has to have all of the licenses essential for running.

Licenses

These licenses all have to be in the particular, accurate name of the small business. And they must have the same small business address and phone numbers.

So keep in mind, that this means not just state licenses, but potentially also city licenses.

Learn more here and get started toward establishing small business credit.

How Do I Build My Business Credit and Start Credibly Dealing with the Internal Revenue Service?

Visit the IRS web site and acquire an EIN for the small business. They’re totally free. Choose a business entity such as corporation, LLC, etc.

A business can begin as a sole proprietor. But they will most likely want to switch to a variety of corporation or an LLC.

This is in order to limit risk. And it will take full advantage of tax benefits.

A business entity will matter when it involves taxes and liability in case of a lawsuit. A sole proprietorship means the business owner is it when it comes to liability and taxes. No one else is responsible.

Sole Proprietors Take Note

If you run a company as a sole proprietor, then at the very least be sure to file for a DBA. This is ‘doing business as’ status.

If you do not, then your personal name is the same as the small business name. Consequently, you can end up being directly accountable for all small business debts.

In addition, according to the Internal Revenue Service, by having this structure there is a 1 in 7 chance of an IRS audit. There is a 1 in 50 possibility for corporations! Prevent confusion and significantly reduce the odds of an IRS audit at the same time.

How Do I Build My Business Credit and Set off the Business Credit Reporting Process?

Start at the D&B web site and obtain a totally free D-U-N-S number. A D-U-N-S number is how D&B gets a company in their system, to generate a PAYDEX score. If there is no D-U-N-S number, then there is no record and no PAYDEX score.

Once in D&B’s system, search Equifax and Experian’s sites for the business. You can do this at www.creditsuite.com/reports. If there is a record with them, check it for correctness and completeness. If there are no records with them, go to the next step in the process.

This way, Experian and Equifax will have activity to report on.

Vendor Credit Tier

First you must establish trade lines that report. This is also called the vendor credit tier. Then you’ll have an established credit profile, and you’ll get a business credit score.

And with an established business credit profile and score you can start to obtain credit in the retail and cash credit tiers.

These kinds of accounts often tend to be for the things bought all the time, like marketing materials, shipping boxes, outdoor work wear, ink and toner, and office furniture. This furniture could be particularly helpful to residential real estate agents.

But to start with, what is trade credit? These trade lines are credit issuers who will give you preliminary credit when you have none now. Terms are usually Net 30, rather than revolving.

Hence, if you get an approval for $1,000 in vendor credit and use all of it, you will need to pay that money back in a set term, such as within 30 days on a Net 30 account.

Details

Net 30 accounts need to be paid in full within 30 days. 60 accounts must be paid in full within 60 days. In contrast to with revolving accounts, you have a set time when you have to pay back what you borrowed or the credit you used.

To launch your business credit profile the right way, you should get approval for vendor accounts that report to the business credit reporting bureaus. Once that’s done, you can then make use of the credit.

Then repay what you used, and the account is on report to Dun & Bradstreet, Experian, or Equifax.

Vendor Credit Tier – It Helps

Not every vendor can help like true starter credit can. These are vendors that will grant an approval with a minimum of effort. You also need them to be reporting to one or more of the big three CRAs: Dun & Bradstreet, Equifax, and Experian.

You want 5 to 8 of these to move onto the next step, which is the retail credit tier. But you may need to apply more than one time to these vendors. So, this is to demonstrate you are responsible and will pay timely. Here are some stellar choices from us: https://www.creditsuite.com/blog/5-vendor-accounts-that-build-your-business-credit/

How Do I Build My Business Credit and Get Benefits from Accounts That Don’t Report?

Non-Reporting Trade Accounts can also be helpful. While you do want trade accounts to report to a minimum of one of the CRAs, a trade account which does not report can still be of some worth.

You can always ask non-reporting accounts for trade references. And credit accounts of any sort will help you to better even out business expenditures, thereby making budgeting simpler. These are companies like PayPal Credit, T-Mobile, and Best Buy.

Retail Credit Tier

Once there are 5 to 8 or more vendor trade accounts reporting to at least one of the CRAs, then move onto the retail credit tier. These are companies like Office Depot and Staples, both of which have plenty of goods for sale which will help residential real estate agents.

Just use your Social Security Number and date of birth on these applications for verification purposes. For credit checks and guarantees, use the small business’s EIN on these credit applications.

One instance is Lowe’s. They report to D&B, Equifax and Business Experian. They want to see a D-U-N-S and a PAYDEX score of 78 or more.

Fleet Credit Tier

Are there 8 to 10 accounts reporting? Then move to the fleet credit tier. These are companies such as BP and Conoco. Use this credit to buy fuel, and to fix, and maintain vehicles. Only use your Social Security Number and date of birth on these applications for verification purposes. For credit checks and guarantees, make certain to apply using the company’s EIN.

One such example is Shell. They report to D&B and Business Experian. They need to see a PAYDEX Score of 78 or more and a 411 business phone listing.

Shell might say they want a specific amount of time in business or profits. But if you already have adequate vendor accounts, that won’t be necessary. And you can still get an approval.

Learn more here and get started toward establishing small business credit.

Cash Credit Tier

Have you been sensibly managing the credit you’ve gotten up to this point? Then move to the cash credit tier. These are companies like Visa and MasterCard. Only use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, use your EIN instead.

One example is the Fuelman MasterCard. They report to D&B and Equifax Business. They need to see a PAYDEX Score of 78 or higher. And they also want you to have 10 trade lines reporting on your D&B report.

Plus, they want to see a $10,000 high credit limit reporting on your D&B report (other account reporting).

Also, they want you to have an established business.

These are businesses such as Walmart and Dell, and also Home Depot, BP, and Racetrac. These are commonly MasterCard credit cards. If you have 14 trade accounts reporting, then these are in reach.

And there are tons of ways the business credit cards in the cash credit tier can help residential real estate agents.

Learn more here and get started toward establishing small business credit.

How Do I Build My Business Credit and Monitor My Business Credit?

Know what is happening with your credit. Make certain it is being reported and take care of any mistakes ASAP. Get in the practice of taking a look at credit reports and digging into the details, and not just the scores.

We can help you monitor business credit at Experian and D&B for 90% less than it would cost you at the CRAs. See: www.creditsuite.com/monitoring.

At Equifax, you can monitor your account at: www.equifax.com/business/business-credit-monitor-small-business. Equifax costs about $19.99.

Update Your Data

Update the relevant information if there are inaccuracies or the information is incomplete. At D&B, you can do this at: https://iupdate.dnb.com/iUpdate/viewiUpdateHome.htm. For Experian, go here: www.experian.com/small-business/business-credit-information.jsp. So for Equifax, go here: www.equifax.com/business/small-business.

How Do I Build My Business Credit and Fix My Business Credit?

So, what’s all this monitoring for? It’s to dispute any inaccuracies in your records. Mistakes in your credit report(s) can be fixed. But the CRAs often want you to dispute in a particular way.

Disputes

Disputing credit report errors typically means you mail a paper letter with copies of any evidence of payment with it. These are documents like receipts and cancelled checks. Never send the originals. Always mail copies and retain the originals.

Fixing credit report inaccuracies also means you specifically itemize any charges you dispute. Make your dispute letter as crystal clear as possible. Be specific about the concerns with your report. Use certified mail so that you will have proof that you sent in your dispute.

How Do I Build My Business Credit? A Word to the Wise

Always use credit smartly! Don’t borrow more than what you can pay back. Keep track of balances and deadlines for payments. Paying off on schedule and fully will do more to elevate business credit scores than nearly anything else.

Establishing small business credit pays off. Great business credit scores help a business get loans. Your lender knows the small business can pay its debts. They understand the company is bona fide.

The business’s EIN attaches to high scores and credit issuers won’t feel the need to demand a personal guarantee.

How Do I Build My Business Credit: Takeaways

Business credit is an asset which can help your small business for years to come. Learn more here and get started toward establishing small business credit.

The post Check Out This Great Question from Residential Real Estate Agents: How Do I Build My Business Credit? appeared first on Credit Suite.