FIRST ON FOX: A federal judge on Saturday announced its “preliminary intent to appoint a special master” to review records seized by the FBI during its unprecedented raid of his Mar-a-Lago home earlier this month, at the request of former President Trump and his legal team, citing the “exceptional circumstances.”

Trump and his legal team filed a motion Monday evening seeking an independent review of the records seized by the FBI during its raid of Mar-a-Lago earlier this month, saying the decision to search his private residence just months before the 2022 midterm elections “involved political calculations aimed at diminishing the leading voice in the Republican Party, President Trump.”

U.S. District Judge from the Southern District of Florida Judge Aileen M. Cannon on Saturday afternoon said that the decision was made upon the review of Trump’s submissions and “the exceptional circumstances presented.”

“Pursuant to Rule 53(b) (1) of the Federal Rules of Civil Procedure and the Court’s inherent authority, and without prejudice to the parties’ objections, the Court hereby provides notice of its preliminary intent to appoint a special master in this case,” Cannon wrote in a filing Saturday.

A hearing is set for Sept. 1 at 1:00 p.m. in West Palm Beach, Fla. Cannon also ordered the Justice Department to file a response by Aug. 30 and provide, “under seal,” a “more detailed Receipt for Property specifying all property seized pursuant to the search warrant executed on August 8, 2022.”

The current property receipt shows that FBI agents took approximately 20 boxes of items from the premises, including one set of documents marked as “Various classified/TS/SCI documents,” which refers to top secret/sensitive compartmented information.

Records covered by that government classification level could potentially include human intelligence and information that, if disclosed, could jeopardize relations between the U.S. and other nations, as well as the lives of intelligence operatives abroad. However, the classification also encompasses national security information related to the daily operations of the president of the United States.

The property receipt also showed that FBI agents collected four sets of top secret documents, three sets of secret documents and three sets of confidential documents, but the document does not reveal any details about any of those records.

The government initiated the search in response to what it believed to be a violation of federal laws: 18 USC 793 — gathering, transmitting or losing defense information; 18 USC 2071 — concealment, removal or mutilation; and 18 USC 1519 — destruction, alteration or falsification of records in federal investigations.

The allegation of “gathering, transmitting or losing defense information” falls under the Espionage Act.

Trump and his team are disputing the classification and say they believe the information and records to have been declassified.

Cannon also ordered the Justice Department to file under seal a “particularized notice indicating the status” of its review of the seized property, “including any filter review conducted by the privilege review team and any dissemination of materials beyond the privilege review team.”

Cannon also said that the Justice Department should include in its filings its “respective and particularized positions on the duties and responsibilities of a prospective special master, along with any other considerations pertinent to the appointment of a special master in this case.”

Trump’s motion for a special master filed Monday evening, requested that the Justice Department halt its ongoing review of the material seized by the FBI during the raid — some labeled classified, and others covered by attorney-client privilege — until an independent review could be conducted.

At this point, a Department of Justice “taint” or “filter” team has been reviewing documents seized by the FBI during its raid.

A senior law enforcement official familiar with the process told Fox News that the review began soon after the search warrant was executed on Aug. 8.

The official told Fox News that it is standard procedure for the Justice Department to use a “taint” or “filter” team to go through documents obtained during a search — in part, to identify records that may be protected by attorney-client privilege.

Fox News first reported earlier this month that FBI agents seized boxes containing records covered by attorney-client privilege and potentially executive privilege during the raid.

Sources familiar with the investigation told Fox News Saturday that the former president’s team was informed that boxes labeled A-14, A-26, A-43, A-13, A-33, and a set of documents — all seen on the final page of the FBI’s property receipt — contained information covered by attorney-client privilege.

Attorney-client privilege refers to a legal privilege that keeps communications between an attorney and their client confidential. It is unclear, at this point, if the records include communications between the former president and his private attorneys, White House counsel during the Trump administration or a combination.

The ruling Saturday comes after another federal judge, U.S. Magistrate Judge Bruce Reinhart, released a redacted version of the affidavit used to justify the FBI’s raid.

The FBI, in the heavily-redacted affidavit, said it had “probable cause to believe” that additional records containing classified information, including National Defense Information, would be found on the premises of Mar-a-Lago, beyond what he had previously turned over to the National Archives and Records Administration.

Reinhart signed the FBI’s warrant for the raid on Mar-a-Lago on Aug. 5, giving the FBI authority to conduct its search–a document Reinhart unsealed, along with the property receipt from the raid earlier this month.

Disclosure: This content is reader-supported, which means if you click on some of our links that we may earn a commission.

Wix is an exceptional website builder, allowing you to create a highly functional and professional website with zero coding experience. Even web developers have access to numerous tools to enhance their site’s customization and functionality.

In my opinion, Wix is the best website builder for general use, whether you are a photographer, musician, restaurateur, blogger, or just setting up a small ecommerce business.

Wix Compared To The Best Website Builders

While most website builders tend to focus on niche markets like ecommerce or content management, Wix is a jack of all trades. This website builder casts a wide net, making it attractive to all kinds of people who need professional-looking websites quickly and cheaply.

Whether you are a seasoned restaurateur looking to promote your business, a startup venturing into your first online enterprise, or an experienced web developer without the time or resources to create a website from scratch, Wix will work for you.

Be sure to see all of my top picks for the best website builders before you decide Wix is the best option for you. There, I review three more services in separate categories and include an in-depth guide focusing on different types of website builders, what criteria you should consider when choosing the best website builder, and more.

Who Is Wix Best For?

While it is easy to be transfixed by Wix’s marketing and features, the truth is this website builder targets a particular audience.

Wix works exceptionally well for individuals or small businesses that want a professional website but don’t want to bother with hiring a web developer, registering a domain name, finding a web hosting company, and all that goes into setting up a professional website.

Wix does a great job of making an online presence more accessible to small businesses and individuals.

Wix websites are attractive, relatively cheap, and quick to set up. Wix also caters to diverse niches, including blogging, photography, ecommerce, music, events, hospitality, bookings, restaurants, forums, and much more.

Wix’s industry-specific themes, design templates, tools, and resources often feel like the company had you in mind when creating its platform. However, this all-inclusive take on website building is also Wix’s Achilles heel.

The platform simply doesn’t offer sufficient functionality and scalability for larger businesses and bigger ecommerce websites. For this, Shopify would be a much better option.

Wix: The Pros and Cons

One of Wix’s best-defining features is the freedom it offers. You can create your ideal site, down to your preferred pixelation.

While freedom is a good thing, newbies may find the design potential slightly overwhelming. Wix remedies this by offering extensive resources, including step-by-step tutorials, videos, articles, and a wealth of information to help you grasp the editor.

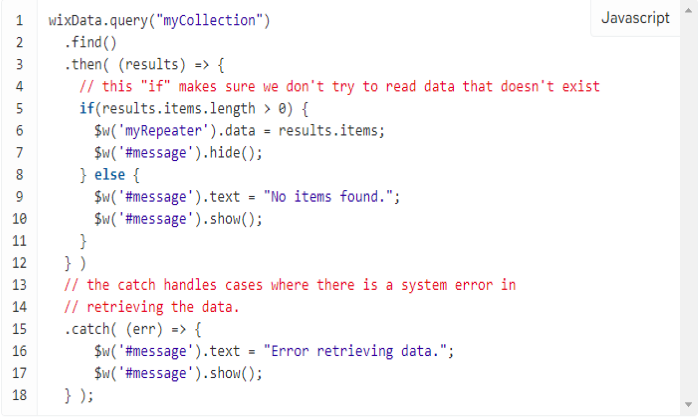

Wix also has unique elements that you don’t see very often with website builders. For example, the Repeater feature allows you to easily replicate elements for list items with a similar layout and design but different content.

One major challenge when using a website builder is differentiating your website from competitors using the same themes and templates. Wix offers far more customization options than Weebly and certain other competitors.

You can tell that Wix prioritizes the user’s ability to create unique websites. The design possibilities are endless, especially in the hands of a seasoned developer.

Pros

Intuitive Interface: While the drag-and-drop feature is hardly a revolutionary concept among website builders, Wix succeeds in this regard. You have unbridled freedom to move elements around with few restrictions. Additionally, the platform offers guidelines to help you get the hang of the tools and templates. Wix also lets you preview your mobile site rather than cross your fingers that the mobile site will be just as good as the desktop version.

Robust App Market: Wix has plenty of built-in tools to get started, but you might need more functionality in your site. Wix has a highly populated app market that offers apps and widgets for almost any functionality you can think of, including events bookings, live chat, newsletter, blogging, opt-in forms, pop-ups, online ads, forums, and much more. The app market offers more than 250 integrations covering almost every conceivable area of your online presence.

Built-In SEO: It’s one thing to create a beautiful website, but an entirely different territory getting your site in front of eyeballs. You can fill in metadata and keyword tags related to your niche, and Wix will help you rank in the search engines. Additionally, Wix lets you edit your URL format for each page to boost your site’s Google ranking. If you aren’t quite ready to invest in SEO, Wix is a good start and requires minimal effort on your part.

Exceptional Security: Something few people think about when building their website is how to protect the data of your site and that of your site’s visitors. Good thing is, with Wix, you don’t even have to. Their managed security elements, including built-in TLS 1.3 encryption and DDoS protection, secure ecommerce payments, and keeping all platform elements compliant with the highest industry standards, mean you won’t have to lift a finger to ensure your site is secure.

A Reliable Platform: Wix puts in the work to make sure the sites their users create are reliably available. Through 24/7 platform monitoring and their powerful array of data centers, you’ll almost certainly never experience downtime for any site you build on Wix. They also offer auto-scaling technology so your site can handle big, sudden rushes of traffic with no degradation of the user experience. Wix even automates backups of your site data, so if anything does go awry, you can restore everything had before and continue along as normal.

Tons of Templates: Wix offers 500+ industry-specific templates to help you build your website. Wix lets you sort and select templates by industry to narrow down your options, including tourism and travel, corporate, photography, ecommerce, music, and more. The templates are all high-quality and designer made. If you are worried about boiler-plate offerings, these templates are highly customizable. You can edit content, change the site name, delete sections, replace images, and tweak the template to make it your own. Wix has one of the largest template libraries of any website builder out there.

Flexible Plans: Wix has an affordable entry-level plan if you need to create a basic personal website. Should you need more functionality, simply upgrade to a premium plan for as low as $4.50 per month. Also, Wix won’t lock you into a contract. Many website builders need you to commit to a 24 or 36-month contract for premium features. With Wix, you can choose to cancel your subscription at any time. This flexibility works particularly well if you aren’t sure about the direction you want to take with your web presence.

All-in-One Solution: With your Wix subscription, you don’t have to worry about web hosting, domain*, SSL certificate, downtime, security, website speed, or any of the practical elements of running a website. Wix takes care of all that for you, included in your monthly subscription. The platform also has a very responsive customer support team to help you with your site’s problems. You can contact customer support via email, chat, or direct phone call.

*Wix offers a free domain voucher valid for one year with most subscriptions. Domain extensions include .com, .org, .net, .biz, .xyz, .space, .pictures, .co.uk, and .info.

Cons

No Unlimited Plans: A sizable number of website builders offer unlimited storage or unlimited bandwidth. Although Wix provides unlimited bandwidth for its Business and Ecommerce plans, there is still a storage limit. This omission reinforces my opinion that Wix is meant for individuals and small businesses rather than large ecommerce enterprises.

Inflexible Templates Once Live: You can customize your Wix’s website templates to your heart’s content, but once you are locked in, that’s it. You cannot change your template once your site goes live. While this might not be such a big problem for a personal website, it can spell trouble down the line for an online business that continues to grow, morph, and evolve over the years.

You Can’t Export Your Website: To piggyback on the con above, Wix can lock you into a long-term commitment even without a contract. Once on the Wix platform, you are locked in for life. You cannot transfer or export your website to another platform. Again, this may not be a big deal for a small business or an individual. However, a fast-growing startup will have problems down the line if Wix can no longer meet its needs.

Wix Pricing

Wix paid plans fall into two categories; Website Plans and Business & Ecommerce Plans. Each category has individual tiers, as you will soon discover.

Before I get to the nitty-gritty of Wix’s pricing structure, there are a couple of things worth mentioning.

First, Wix’s advertised pricing is based on an annual subscription. You have the option of paying month-by-month, but it will cost more. Don’t be surprised if your monthly billing is a little higher than advertised on the website. It’s all in the fine print.

Secondly, your free domain is only available for one year. After that, you have to pay an annual premium. Additionally, you are only eligible for the free domain if you pay for the whole year in advance. You lose out on the offer if you choose the month-to-month payments.

Wix Website Plans

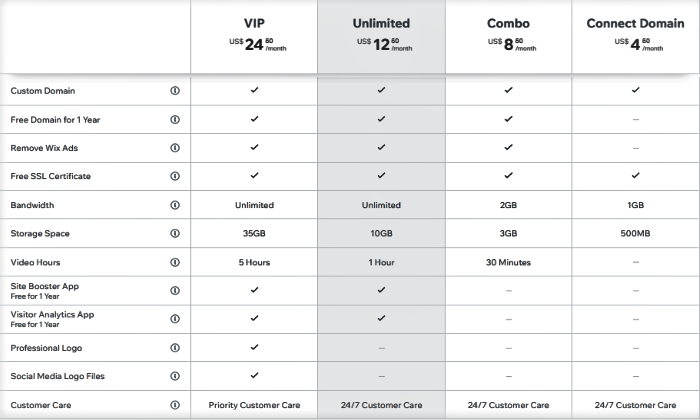

Connect Domain

Starting from the far right, Connect Domain is the most basic plan. This option costs $4.50 per month and doesn’t come with a free domain. Also, your website will display Wix ads. You can still connect your existing or custom domain name to your Wix site. This plan also comes with:

24/7 customer care

Free SSL certificate

500MB storage space

1GB bandwidth

Some of the features you’ll be giving up here include the ability to upload and stream videos on your site, site booster app, social media logo files, and visitor analytics app (SEO tool).

I only recommend this option if you want to put together a simple informational website or portfolio at the lowest possible price. However, considering that you’d have severely limited bandwidth, Wix ads, and a Wix-branded URL, this isn’t the kind of site that could conceivably rank high on Google. There are very limited use-cases for this plan.

Combo

This option costs $8.50 per month and is an excellent alternative to the Connect Domain for a simple personal website. This plan comes with a free domain, or you connect a custom domain.

This option offers 2GB bandwidth, 3GB storage space, 24/7 customer care, and 30 minutes of video. However, you’ll be losing out on social medial logo files, a visitor analytics app, a site booster app, and a professional logo.

Ultimately, you are getting a good deal for a low-traffic but professionally done website. You can always upgrade to a higher plan should your needs change.

Unlimited

This Wix plan targets freelancers and entrepreneurs. It will cost $12.50 per month in exchange for 10 GB of storage space and unlimited bandwidth. You also get a free SSL certificate, no Wix ads, a free domain for one year, one video hour, a visitor analytics app, and a site booster app.

If you want to start a professional website or online business, the unlimited plan will serve your needs better than the Combo plan for a nominal price hike.

VIP

The price shoots up rather drastically with the Wix VIP plan. This one costs $24.50 per month. For the price, you get all the features not included in the other plans and some add-ons. These include:

Free domain for one year

Remove Wix Ads

Unlimited bandwidth

35GB storage space

Free SSL certificate

Social medial logo files

Visitor analytics app

Five video hours

Professional logo

24/7 customer care

I recommend this plan for an established business wanting to make its online presence.

Wix Business & eCommerce Plans

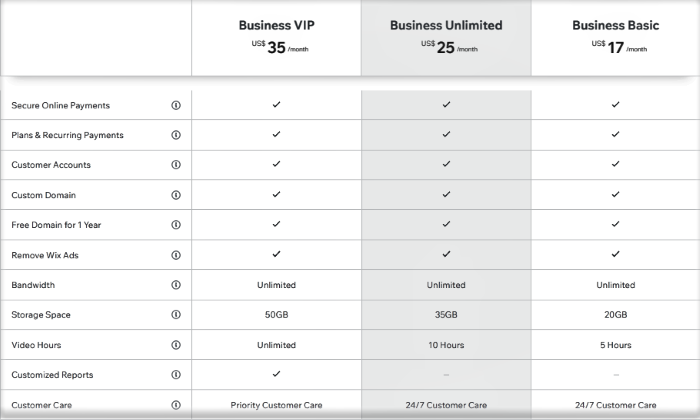

If you plan to accept online payments, Wix offers three tiers under its Business & Ecommerce Plans.

All business and ecommerce subscriptions offer:

Secure online payments

Customer accounts

Plans & recurring payments

Remove Wix ads

Custom domain

Free domain for one year

Video hours

Unlimited bandwidth

Business Basic

This plan costs $17 per month and offers 20GB storage space and five video hours in addition to the above-listed features.

Business Unlimited

You get all the Wix Business Basic features, except this time, you get an additional 15GB (35GB total) storage space. This plan costs $25 per month and guarantees ten video hours instead of five. The distinction between the two plans in terms of offerings is negligible in most cases.

I suggest you start with the Wix Business Basic plan and only upgrade to Business Unlimited if you have good reason to do so.

Business VIP

This tier costs $35 per month. The most prominent upgrade is proprietary customer care. If you value customer support or have nightmares of your site going down at a critical hour, this is the plan for you.

Additionally, Wix Business VIP allows you to create customized reports from the data you collect. This functionality isn’t available on any of the other business and ecommerce plans. Additionally, you get unlimited video hours on this plan.

I recommend Business VIP for established businesses.

Wix Product Offerings

Wix allows people with little to no coding experience to create a website from scratch. To this end, Wix offers all the features you would need to create a professional website.

Wix Editor

The Wix editor is the platform’s main feature, allowing you to create a website from scratch with little or no coding experience. This editor is among the most robust out there, and is intuitive and feature-packed, and can handle just about any kind of website you throw at it.

The Wix editor offers more than 500 designer-made and industry-specific templates. You can browse through the templates based on industry to make things easier. You get total design freedom, including dragging and dropping template elements to get the perfect site.

Suppose you’re worried about your site looking the same as everyone else’s. In that case, Wix allows you to add scroll effects, video backgrounds, animation and display your text and videos. You can also choose from more than 100 fonts with the option to upload your own.

Wix also lets you create a mobile-optimized site independently of your desktop site. Additionally, the Wix Mobile app lets work on your site from a smartphone (hopefully one with a large screen!) or a tablet.

Overall, Wix offers excellent design flexibility without being too overwhelming for newbies. This website builder treads the thin line between being feature-rich and easy to use.

Wix Artificial Design Intelligence (ADI)

If you are pressed for time or the platform’s functionality is proving a little overwhelming, Wix can literally build the site for you.

The ADI offers a hands-off approach to customized website building. Simply enter your social media profiles (Twitter, Facebook, Instagram, etc.) or website. The AI will extract business information from these pages and create the first draft of your website.

You can then tweak and customize the site to fit precisely what you are looking for. To make your job even easier, the ADI feature offers helpful tips and prompts throughout the process to help you create the perfect website.

Wix succeeds at pushing boundaries, and this Wix ADI is a feature you won’t see too often on the market.

Velo by Wix

Although Wix primarily focuses on people with minimal to no experience creating a website, this platform does have something for amateurs and more experienced web developers.

Velo by Wix offers more freedom to create the website just how you want it. Wix lets you use your source control tools and code editors and work in your environment of choice or online.

Additionally, you can use external data sources or use Wix’s integrated databases. Velo by Wix uses an open platform, allowing you to connect to an external data source and third-party data sources.

Wix Professional Suite of Features

Wix has all the tools you would need to create and maintain your website. Most plans offer a free custom domain name with the option to connect your existing domain. You also get free website hosting and a professional mailbox complete with a personalized email to match your brand and domain name.

Additionally, Wix offers contact management to help you collect and manage contacts and subscribers from a single dashboard. Additional features include:

SSL Certificate: Wix offers a free SSL certificate to help you with website security and search engine optimization.

Social Tools: You can easily connect all your social media accounts to your Wix website.

Analytics: Wix keeps track of your web performance, including in-depth stats to help you make data-driven decisions.

Considering that Wix mostly targets small businesses, freelancers, and individuals, it’s hard to fault its feature suit. Its all-in-one approach to website building takes a huge load off your back when creating your online presence.

Wix Business and Ecommerce

Another area where Wix excels is its industry-specific offerings for businesses and ecommerce sites. First, Wix lets you build an online store from scratch. Ecommerce features include a storefront, order-tracking, customized shipping and tax rules, coupons and discounts, and multiple payment methods, among other features.

While these features work well for a small business, Wix isn’t well suited to a large online business that relies primarily on online sales. For starters, Wix only supports a handful of payment methods. There is a good chance a large company will need the help of third-party payment gateways to get around this limitation.

Additionally, its built-in ecommerce features aren’t all that powerful compared to competitors such as Shopify.

On the upside, the industry-specific ecommerce offerings include:

Wix Booking

Wix Stores

Wix Blog

Wix Music

Wix Photography

Wix Events

Wix Videos

Wix Restaurants

With these options, you get industry-specific templates, features, and functionality. This system makes your work so much easier.

For example, Wix Bookings allows you to accept online payments, accept bookings around the clock, and send auto-reminder emails to your clients. Wix Photography lets you tweak your image’s sharpness and quality, secure your photos with built-in watermarks, and display your pictures in over 30 galleries.

You may need a more robust website builder for a large ecommerce store. However, for a small business, professional blog, or freelance business, Wix ticks all the boxes.

The Best Website Builders

To get a more comprehensive view of how Wix stacks up to the competition, please be sure to check out my Top 4 Best Website Builderspost.

Overall, Wix is an exceptional website builder for a select group of people, including small business owners, freelancers, professionals, and bloggers. While Wix also works well for small ecommerce businesses, you may need to look elsewhere if you are creating a sizable online enterprise. Wix is user-friendly, highly functional, and offers excellent value for money.

What is a 2021 Credit Review and Why Should You Do One?

In a time when the economy is tumbling toward a recession, it’s important for small businesses to get their finances in order. Here are tips on how to do that by doing a 2021 credit review.

Also, we’ll show you how this can give your business an advantage over competitors who are not aware of what they’re missing out on. And why financial experts recommend this type of review. So look at the 5 ways a 2021 credit review can help your business. Get more information about what you need to do now so you don’t have any regrets later!

All year, we’ve been talking about building business credit. And we’ve talked about business credit reporting agencies and their reports. But do you know how to read your business credit reports? And do you know what to do with the information you might find?

The Benefits of Doing a 2021 Credit Review

Knowing what’s in your business credit reports can only help you. Learning what the CRAs are scoring you on will help focus your efforts. For example, if on-time payments matter to a CRA more than utilization percentage, then wouldn’t it be a good idea to concentrate on paying your credit bills on time? <Spoiler alert> they do.

Why it is Important for You to Know About Your Business Credit Scores

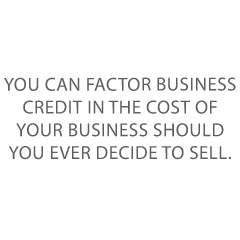

Business credit is an actual asset, and it is worth money! That means you can factor business credit into the cost of your business, should you ever decide to sell. Plus, what you do to build business credit will often help you build a clientele!

Better business credit scores will help you get business financing. They will help you get better financing, with lower interest rates and payback terms. For some entrepreneurs, better business credit scores are the difference between getting some financing….

Or none.

What Information Should be Included in Your Review

You want to be looking at your actual, full business credit reports, which are more than the scores. It’s time to look at the details. These should be reports from:

Dun & Bradstreet

Experian and

Equifax

About the Process

Get your D&B business credit report by signing into the D&B website. You want their CreditMonitor product, which shows the most scores. Get your Experian credit report by running a search for your business. You want their CreditScoreSM Report. To get your Equifax business credit report, you’ll need to contact them. Specify that you want a single Equifax business credit report.

How to Get Started with a 2021 Credit Review Now

If a highly detailed report isn’t in the budget right now, at least a shorter summary report will keep you informed. And it will get you in the habit of checking your credit reports. Today, we’ll look at high level information. This is what you absolutely need to know right now.

#5 Way a 2021 Credit Review Can Benefit Small Businesses: Get to Know Your Dun & Bradstreet Business Credit Report

It always makes sense to start with D&B. They are the biggest business CRA in the world, by far! You need a D-U-N-S number to start building business credit. If you don’t have a D-U-N-S number, you’ll need to get one; they’re free. This number gets your business into their system.

But your business will not get a PAYDEX score, unless there are at least 3 trade lines reporting, and a D-U-N-S number. Your business must have BOTH to get a D&B score or report.

D&B Data

D&B’s database contains hundreds of millions of companies around the world, both active and out of business. So D&B lists over a billion trade experiences. It works to improve its analyses to assure the greatest degree of accuracy possible. To ensure as accurate a report as possible, give D&B your company’s current financial statements.

Predictive Models and Scoring

D&B takes historical information to try to predict future outcomes. This is to identify the risks inherent in a future decision. They take objective and statistically derived data, rather than subjective and intuitive judgments. There are sample reports online available on the D&B website.

D&B Reports

D&B offers database-generated reports. These help their clients decide if your business is a good credit risk. Companies use the reports to make informed business credit decisions and avoid bad debt. Several factors go into creating such a report.

In general when D&B does not have all the information that they need, they will show as much in their reports. But missing information does not necessarily mean your company is a poor credit risk. Instead, the risk is unknown.

Executive Summary

The report starts with basic company information, like:

Number of employees

Year your business was started

Net worth

Sales

D&B Rating

This rating helps companies check your business’s size and composite credit appraisal. Dun & Bradstreet bases this rating on data in your company’s interim or fiscal balance sheet plus an overall evaluation of your business’s creditworthiness. The scale runs 5A—HH. Rating Classifications show your company size based on worth or equity. D&B assigns such a rating only if your company has supplied a current financial statement.

The rating contains a Financial Strength Indicator. It is calculated using the Net Worth or Issued Capital of your company. Plus there’s a Composition Credit Appraisal. This number runs 1 through 4, and it shows D&B’s overall rating of your business’s creditworthiness.

The scores mean:

1—High

2—Good

3—Fair

4—Limited

A D&B rating might look like 3A4.

D&B PAYDEX

This part shows two gauges: an up to 24 month PAYDEX, and an up to 3 month PAYDEX. As a result, you can see recent history and your company’s performance over time.

Both gauges have the same scores:

1 means greater than 120 days slow (when it comes to your business paying bills)

50 means 30 days slow

80 means prompt payments

100 means anticipates

100 is the best PAYDEX score you can get. The PAYDEX score is Dun & Bradstreet’s dollar-weighted numerical rating of how your company has paid the bills over the past year. It shows how well your company pays its bills.

Predictive Analytics

This next section shows the chance of business failure. It also shows how often your business is late in paying its financial obligations. These are comparative analyses: the Financial Stress Class, and the Credit Score Class.

Financial Stress Score

This section shows your Financial Stress Class, and a Financial Stress Score Percentile. The Financial Stress Class runs 1—5, with 5 being the worst score.

Financial Stress Score Percentile

It is a comparison of your business to other businesses. The percentile contains a Financial Stress National Percentile. The Financial Stress National Percentile shows the relative ranking of your company among all scorable companies in D&B’s file. It also contains a Financial Stress Score. The report shows the probability of failure with a particular score.

Financial Stress Score Percentile Comparison

So the idea behind the score is to predict the chances your business will fail over the next 12 months. The average probability of failure comes from businesses in D&B’s database. It is provided for comparative purposes. The Financial Stress Score offers a more precise measure of the level of risk than the Financial Stress Class and Percentile. It is meant for customers using a scorecard approach to determining overall business performance.

Credit Score Class

The Credit Score Class measures how often your company is delinquent in paying bills. Overall numbers run 1—5. 1 is businesses least likely to be late. More granular scores run 101—670. 670 is the highest risk.

Credit Limit Recommendation

It shows a spectrum of risk. Your risk category can be:

Low

Moderate or

High

D&B checks risk using their scoring methods. It is one factor used when creating recommended limits.

D&B Viability Rating

This section contains:

Viability Score— to show risk

Portfolio Comparison—also a demonstration of risk

Data Depth Indicator—descriptive vs. predictive

Company Profile—showing if financial data and other info was available

Credit Capacity Summary

This part repeats the D&B Rating above. It includes financial strength, the composite credit appraisal, and payment activity

Business History and Business Registration

This section contains information on ownership. It also shows where your corporation is filed (i.e. which state). This includes the type of corporation, and the incorporation date

Government Activity Summary and Operations Data

This section gives basic information on if your company works as a contractor for the government. It also shows the kind of industry your company is in. It shows what the facilities are like, including general data on its location.

Industry Data and Family Tree

The section shows your business’s SIC and NAICS codes. It also shows where your branches and subsidiaries are. This list is limited to the first 25 branches, subsidiaries, divisions, and affiliates, both domestic and international. D&B offers a Global Family Linkage Link to view the full listing.

Financial Statements

This section is devoted to financial statements D&B has on your business. It shows assets and liabilities, with specifics like equipment, and even common stock offerings.

Indicators and Full Filings

This part shows public records, like:

Judgments

Liens

Lawsuits

UCC filings

This part also breaks down where filings are venued, like the court or the county recorder of deeds office. It shows if judgments were satisfied (paid). It also shows which equipment is subject to UCC filings.

Commercial Credit Score

This part shows the Credit Score Class again. It also shows a comparison of the incidence of delinquent payments. It also includes key factors to help anyone reading the report interpret these findings. And it explains what the numbers mean.

Credit Score Percentile Norms Comparison

Here, your company is compared to others based on:

Region

Industry

Number of employees and

Time in business

Financial Stress Score and Financial Stress Percentile

This section shows a Financial Stress Class and a Financial Stress Score Percentile. The Financial Stress Class runs 1—5, with 5 being the worst score. he Financial Stress Score Norms calculate:

An average score and percentile for similar firms

The norms benchmark where your business stands

This is in relation to its closest business peers.

Financial Stress Score Percentile and Financial Stress Score Percentile Comparison

These two scores are a repeat of the Financial Stress Score section, above.

The average probability of failure is based on businesses in D&B’s database. t is provided for comparative purposes. The Financial Stress National Percentile shows the relative ranking of your company among all scorable companies in D&B’s file. And the Financial Stress Score offers a more precise measure of the level of risk than the Financial Stress Class and Percentile. It is meant for customers using a scorecard approach to determining overall business performance.

Advanced PAYDEX + CLR

This section repeats the 24 month and 3 month PAYDEX gauges. It also includes a repeat of the Credit Limit Recommendation. There is also a PAYDEX Yearly Trend. It shows the PAYDEX scores of your business compared to the Primary Industry from each of the last four quarters.

PAYDEX Yearly Trend

The PAYDEX Yearly Trend is a graph. It includes detailed payment history, with payment habits and a payment summary. It helps show if your business pays the bigger bills first or last.

Let’s look at an Experian business credit report.

#4 Way a 2021 Credit Review Can Benefit Small Businesses: Explore Your Experian Business Credit Report

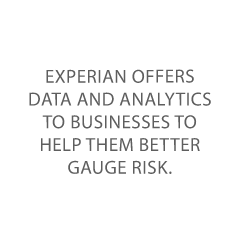

Experian offers data and analytics to businesses to help them better gauge risk. They have a massive consumer and commercial database for checking risk. They have found that blended data and reports work a lot better for them. For troubled businesses, blended scores dropped an average of 30% over the four quarters leading up to a bad event. But the owner’s consumer scores showed no statistically significant decline during the same period. Their best known and most widely used score is Intelliscore Plus℠, a percentile score.

A Typical Experian Business Credit Advantage SM Report

Experian provides a sample report where you can get an idea of what to expect. The best, most accurate and up to date source for this information is the Experian website itself.

Business Background Information

The first part of a report contains:

Basic details like business name, address, and main phone number

Experian BIN (Experian’s BIN is like Dun & Bradstreet’s D-U-N-S number. It’s a unique identifier for each business in the database)

Annual sales

Business type (corporation, etc.)

Date Experian file established

Years in business

Total number of employees

Incorporation date and state

Experian Business Credit Score

Business Credit Scores run 1—100; higher scores mean lower risk. This score predicts the chance of serious credit delinquencies in the next 12 months. It uses tradeline and collections data, public filings as well as other variables to predict future risk.

Key Score Factors:

Number of commercial accts with terms other than Net 1—30 days

The number of commercial accounts that are not current

Number of commercial accounts with high utilization

Length of time on Experian’s file

Experian Financial Stability Risk Rating

Financial Stability Risk Ratings run 1—5; lower ratings mean lower risk. A rating of 1 means a 0.55% potential risk of severe financial distress in the next 12 months. Experian categorizes all businesses to fit within one of the five risk segments. This rating predicts the chance of payment default and/or bankruptcy in the next 12 months.

This rating uses tradeline and collections info, public filings, and other variables to predict future risk. Key Rating Factors:

Number of active commercial accounts

Risk associated with the business type

Risk associated with the company’s industry sector

Employee size of business

Credit Summary

This section contains several counts of various data points. For the most part, details are available further in the report. The info contains:

Current Days Beyond Terms (DBT)

Predicted DBT for a particular date

Average industry DBT

Payment Trend Indicator (stable, or not)

This sector also contains:

Number of payment tradelines

Number of lender consortium experiences

The number of business inquiries

Number of UCC Filings, bankruptcies, and liens

The last part of this section shows:

Number of judgments filed

Number of accounts in collections

Company background (includes founding date, where headquarters are, and what your business does)

Payment Trend Summary

This section shows your company versus your industry on:

Monthly payment trends

Quarterly payment trends

These are the percentages of on-time payments by month and quarter.

Trade Payment Information

This next part shows details on payment experiences (financial trades). There is also data on:

There is also a link to send any missing payment experiences.

Inquiries, Collection Filings, and Collections Summary

The Inquiries part has the industry making the inquiry and a total made during a given month. The Collection Filings sector has the date, name of the agency, and status (open or closed). If a collection is closed, the Collection Filing sector also has the closing date. The Collections Summary shows: status, number of collections, dollar amount in dispute, and amount collected (even if $0).

Commercial Banking, Insurance, Leasing

For leasing, this section shows:

Leasing institution name and address

Product type and lease start date and term

Original and remaining balances

The scheduled amount due

The number of payments per year

And the number of payments which are current, late, or overdue

Judgement Filings

This sector shows:

Date and plaintiff

Filing location

Legal type and action

Document number

Liability amount

It also includes cases where your company in the report is the plaintiff or the defendant.

Tax Lien Filings

This part has:

Date and owner

Filing location

Legal type and action

Document number

Liability amount and description

UCC Filings

This section has:

Date and filing number

Jurisdiction

Secured party

Activity (filed, or not)

UCC Filings Summary

This part shows:

Filing period

Number of cautionary filings

Total filed, released, or continued

Amended/Assigned

Cautionary UCC Filings include one or more of the following collateral:

Accounts

Accounts receivable

Contracts

Hereafter acquired property

Leases

Notes receivable, or

Proceeds

But the Experian Business Credit Advantage SM Report does not have Intelliscore Plus℠. And it does not have the Experian Finance Stability Risk Score.

Experian’s Intelliscore Plus℠

It is a highly predictive score. This score provides detailed and accurate data on your business’s risk. It blends commercial data and consumer data on you, the business owner or guarantor. Reports include trades, legal filings, and more. Business credit scores run 0—100; 0 represents a high risk.

This score shows the percentage of businesses scoring higher or lower than yours. Many large financial institutions use it. So do over half of the top 25 P&C insurers and most major telecommunications and utility firms. Industry leaders in transportation, manufacturing, and technology also use Intelliscore Plus as their main risk indicating model. It has more than 800 aggregates or factors affecting business credit scores. Experian checks the scores of the millions of businesses in their database.

The Experian Financial Stability Risk Score (FSR)

FSR predicts the potential of your business going bankrupt or defaulting on obligations. The score finds highest risk businesses by using payment and public records which include:

Severely delinquent payments of 61+ and 91+ days

High utilization of credit lines

Tax liens

Judgments

Collection accounts

Industry risk

Short time in business, etc.

FSR shows a 1—100 percentile score, plus a 1—5 risk class. The risk class puts businesses into risk categories. The highest risk is in the lowest 10% of accounts. A score of 66—100 and a risk class of 1 means a low risk of default or bankruptcy. But a score of 1—3 and a risk class of 5 means your business has a high risk of default or bankruptcy.

Time to look at Equifax.

#3 Way a 2021 Credit Review Can Benefit Small Businesses: Understand Your Equifax Business Credit Report Better than You Ever Have

You can get a sample Equifax business credit report online. The company gets its data through a data sharing agreement with the Small Business Exchange. And it uses Net 30 type industry trade credit info.

Equifax Business Credit Reports

Equifax will combine financial data with industry trade credit data and add in:

Utility and telephone data

Public record information (bankruptcies, judgments, and tax liens)

Company Identifying Information

The first section shows identifying info, like business name, and address and telephone number. This section will also include your Equifax ID. An Equifax ID is how Equifax can tell your business from similarly-named businesses.

Credit Risk Score

This score runs 101—992. Higher numbers are better. This section also shows key factors. These are positives and negatives about your business. Such as the age of your oldest account, if you have any charge-offs, and the size of your business.

Credit Utilization

This pie chart shows which percent of your available credit line you are using. It also has labels to show how much each percentage is. It is only for your financial accounts.

Payment Index

This score runs 0—100. Higher numbers are better. It also shows Industry Median.

90+ means paid as agreed

1—19 means 120 or more days overdue

Days Beyond Terms

This is a line graph of the average days beyond terms by date reported. It is for nonfinancial accounts only. Plus it shows any recent trends. So if you’ve improved your payment habits, it shows up here.

Business Failure Score/Inquiries

The score runs 1000—1880. It shows key factors like recent balances. The section on inquiries shows the date, and if it was an inquiry on a financial or nonfinancial account.

Bureau Messages

This part seems to be a free form field. Its purpose is to add notes to your profile. These can be notes on the number of your locations, or any business aliases.

Bureau Summary Data

This section shows:

The number of financial and nonfinancial accounts

Date the credit became active

Number of charge offs and total dollars past due

Most severe status in 24 months

Single highest credit extended

Total current card exposure

Median balance and average open balance

It also shows Recent Activity, which includes:

The number of accounts delinquent

New accounts opened

Inquiries and

Accounts updated

Public Records

This section has:

Type Status:

Bankruptcy

Judgments, whether satisfied or not

Liens filed and opened, or released

Number, dollar, and most recent date filed

If there are none reported, then the date field will show that.

Additional Information

The final section appears to contain miscellaneous information, like:

Alternate Company Names and DBAs

Owners and Guarantor Names (name, type, date reported)

Business and Guarantor Comments (seems to be another freeform field) and

Report Details (the date of the report)

#2 Way a 2021 Credit Review Can Benefit Small Businesses: You Can do a 2021 Credit Review on Your Own

Checking your business credit reports in depth is the way to go to do your own credit review. But how do you know if there’s an issue you need to address? The answer is business credit monitoring. Each of the business CRAs has their own plan(s).

D&B Business Credit Monitoring

Pricing is current to September of 2021.

Use D&B Credit Monitor to check your report. It costs $39/month. View recent scores and ratings and benchmark your business versus your industry. It also alerts you to special events like suits, liens, and judgments. It includes dark web monitoring. This means it scans the dark web to help protect your business from possible fraud.

Experian Subscription Plans: The Business Credit Score Pro Subscription Plan

Get 30 reports per month. This plan does not include:

Alert Emails & Monitoring

Dispute Resolution Status Alerts

3 Month Score Trend

Unlimited Access to Your Report

Business Identity Monitoring

Experian Subscription Plans: The Business Credit Score Pro Subscription Plan (Enhanced Version)

Experian also offers an enhanced version of this plan. Get more info, including:

Trade payment detail

UCC detail

Inquiry detail

Currently costs $1,495 per year.

Experian Reports: The Profile Plus Report

Get everything in the Business Credit Score Pro Subscription Plan. Plus (optional with the more expensive report):

Trade Payment Detail

Inquiry Detail

UCC Detail

Corporate Financial Information

Experian Reports: The Credit Score Report

Get everything in the Business Credit Score Pro Subscription Plan, but no optional sections. This one is like a one-time version of the Business Credit Score Pro Subscription Plan. You can use it to decide if you want to subscribe to the more expensive plan.

Equifax Business Credit Monitoring

These prices are current to September 2021. These reports include credit summary, and payment trends and public records. So the idea is to help you identify potential risk of late payments and business failure. Order a single Business Credit Report for $99.95. Or order a Business Credit Report multipack (5 for the price of 4) for $399.95.

Tips for Maintaining Good Credit after Your 2021 Credit Review

Pay your bills on time! It’s the most effective and fastest way to raise and maintain good business credit scores. You should also dispute any material inaccuracies in your reports. Inaccuracies are material (important) if they’re dragging down your scores.

Disputing Issues with Your Reports

The business CRAs will not change your scores without proof. They are starting to accept more online disputes. Include proofs of payment with it. These are documents like receipts and cancelled checks. Be specific about the concerns with your report.

#1 Way a 2021 Credit Review Can Benefit Small Businesses: Monitor Business Credit at D&B, Experian, and Equifax for Less

But all these reports are expensive! You could spend HUNDREDS of dollars trying to keep up with reports from all three of the big business CRAs. But… Did YOU know you can get business credit monitoring for all 3 big business CRAs in one place—for less? Credit Suite offers monitoring through its Business Finance Suite (through Nav). See what credit issuers and lenders see. So you can improve your scores and get the business credit and funding you need.

Your 2021 Credit Review: Takeaways

So there are many reasons to review your business credit reports and understand them.

Business CRAs D&B, Experian, and Equifax all provide reports on businesses like yours. They tend to tap similar info and draw somewhat similar conclusions. Paying on time will help your scores more than anything else. And monitoring your reports will help you find errors fast, before they can do a lot of damage. Monitor with Credit Suite for a lot less than if you monitored your reports and scores at each business CRA.

What’s YOUR business’s biggest benefit from doing a 2021 credit review?

Mercedes has written to motorsport’s governing body, the FIA, to request a review of the incident between Max Verstappen and Lewis Hamilton on lap 48 of the Sao Paulo Grand Prix, which was not investigated by the stewards at the time.

Become.co, once known as Lending Express, claims to help businesses get funding even when they have gotten denials elsewhere. But can they do what they say?

An All In Become.co Review

First as Lending Express, and now as Become, this is a company that claims to be able to help businesses get funding when they have not otherwise been able to do so. What is their secret, and does it really work? We dug deep in order to find out.

Become.co Review: What is Become?

First things first. This is not a lender. Rather, they are more of a lender and borrower dating service. They collect information from potential borrowers and send it to partner lenders. The lenders then decide whether or not they want to make a financing offer to the would-be borrower. The company spins it as lenders competing for the opportunity to fund the borrower’s business. In some cases, this may well be how it turns out.

The lenders that work with Become offer a broad range of lending products. They include:

Startup business loans

Commercial vehicle loans

Asset based loans

SBA loans

Merchant cash advances

Lines of credit

Invoice financing

And unsecured business loans

Become.co Review: How Does it Work?

First, you fill out an application with Become. Then, the company technology analyzes the application and matches you with the best lenders for your business from among their partners.

Application Process

Select how much you need under “loan amount” and then “Get Loan Offer”’

Fill out the information asked for, which includes time in business, industry, revenue etc.

Select up to 3 different lenders.

Then, you will have to connect your business’s checking account to be analyzed.

After that, you wait for the offers to roll in.

After reviewing offers, select the lender you wish to go with.

Funds will be deposited into your business checking account.

The process takes about 15 minutes and involves a soft pull on your credit report. It will not affect your credit.

Rates and Terms

Typically, the minimum amount available from partner lenders is $5,000. The maximum is up to $500,000. Flexible repayment is available based on monthly turnover. Loan terms are from 3 to 36 months.

Also, repayments do not use “interest rates.” Rather, you are given a payback amount, which is agreed on upfront. It is based on your business type and your loan term.

They claim this structure is beneficial for your business cash flow, because you will know your total costs upfront. While not untrue, it would be wise to calculate an effective interest rate for comparison purposes. For example, if your loan amount is $5,000 and your repayment amount is $5,500, your effective interest rate is 10% over the life of the loan.

This is important information to know, so that you can make sure you are getting the best deal possible for your business.

Qualifying

Any business owner can apply. If you do not qualify, you will still be assigned a dashboard explaining the reason why, along with tips to help you improve your chances. At a minimum, you should have an average revenue of $5,000 per month, ideally. You also need to have been in business for at least 3 months if you are a U.S. business and at least 6 months if you are in Australia.

As for credit score, while it is important, some of their partners do not deny based on a low credit score. Instead, their decision is based on the overall health of your business as determined by a number of factors. These may include revenue, time in businesses, average balance in business bank accounts, and more.

Clearly, the more of these factors you have in your favor, the better your chances are going to be for getting funding from Become.

Required Documents

You must have a business checking account. Become will analyze the statements for the past 3 to 6 months. Other document requirements will be up to the lender you end up applying to. Some examples of documents they may require include merchant statements, tax returns, and financing projections. It will never hurt to have a business plan.

Become uses technology and advanced algorithms to help match business borrowers to alternative lenders. The process is free, and unlike others, they do more than just match borrowers to lenders. They also function as a credit profiler.

Their proprietary technology renders a unique LendingScore for each business. This is a financing profile that is intended to help the company improve funding possibilities, access new opportunities, and find the best funding solutions.

They do not seem to have a Better Business Bureau profile, at least not under the name Become. There is a company with the same name that uses the URL “Become.com.” Become.com appears to be an online shopping portal, wholly unrelated to Become. Co. Since both companies are in the state of California, this could be quite confusing.

They do, though, have a very good rating on Trustpilot. The rating is 4.8 stars. There are over 500 reviews, and over 90% of them are excellent.

Become.co Review: Are They All That They Claim to Be?

It seems that they do a great job. They have a lot of happy customers, and Trustpilot is a trusted review source. That said, it’s unfortunate that they chose a name that requires a .co URL. This may make them hard for many to find when looking for small business loans. Alos, the name “Become” doesn’t exactly reflect who they are or what they do, further complicating the ability of business owners to find them. It is a very generic word which most people would not relate to business funding.

Another potential area of concern is the fact that they want access to your business bank account. It sounds as if they want to access it electronically. Still, online lenders are doing this more and more these days. Given the number of great reviews, it may not be an issue. That is a decision you will have to make for yourself.

Is Become the End of the Road if You Do Not Qualify?

If you fill out an application with Become and you do not qualify for funding with any of their lenders, your dashboard will contain the reasons why and ideas to help you qualify in the future. This can be helpful in the long term. But, what if you need funding right now?

A business credit expert can help walk you through the process of building a business credit profile. This is separate from your personal credit profile, and will open up new funding opportunities. They can also analyze the current fundability of your business, and help you find ways to improve it.

There are a lot of companies out there that claim to help you get business funding. It can be hard to tell which ones are legit and which ones are scams. Predatory lending is a big issue in the world of business loans, and you have to be on your toes. You need to research any company before you decide to work with them.

Biz2Credit is one option, and we’ve done the leg work for you in our in-depth review.

An In Depth Look at Biz2Credit

It can be hard to navigate the business loan waters alone. Sometimes, a lifeboat comes along and throws out a life preserver. They can help you get your business safely where it needs to be. Sometimes, however, these businesses are sharks in disguise. How do you tell the difference, and which one is Biz2Credit?

Biz2Credit Review: Background

Biz2Credit has been around since 2007. They are backed by Nexus Business Partners, as well as 225,000 small business customers. The company has helped thousands of small business owners obtain over $2 billion in funding across the United States.

What Does Biz2Credit Do?

They are not a bank. They do not directly fund loans. What they do is accept and process applications for loans, matching small business owners to the best lender and small business financing products to meet their qualifications and needs. How do they do this? Their proprietary platform innovatively matches business to the capital sources that best fit them.

Biz2Credit Review: Products

They offer a number of options for business financing that business owners can apply for. They will help you figure out which option is best for your business needs. Remember, details such as available amounts, rates, terms and requirements can change frequently. Always check with them directly for the most up-to-date information.

Working Capital

You can get working capital loans that range up to $2 million with Biz2Credit. They claim it only takes 4 minutes to apply and 24 hours for approval. Funding happens in as little as 72 hours.

You must have at least $250,000 in annual revenue, be in business at least 6 months, and have a 575 or greater credit score.

Term Loans

They offer term loans of up to $250,000 with rates starting at 8.99%. Final rates depend on many factors, including the borrower’s credit score. The timeline for the term loans is like that of the working capital loans. The application process is fast, taking as little as four minutes. Approval usually happens within 24 hours and funds are available by 72 hours in.

To qualify, your business must have revenue of at least $250,000, you must be in business at least 18 months, and your credit score must be now lower than 660.

Check out our professional research on bank ratings, the little-known reason why you will – or won’t – get a bank loan for your business.

Commercial Real Estate Loans

These loans top out at $6 million. Rates start at 10%. The timeline is a little longer for these, with qualification approval coming in at around 48 hours. Closing times for these loans vary.

The qualification requirements for the commercial real estate loans are the same as for the term loans. You must have at least $250,000 annual revenue, a 660 or above credit score, and be in business at least 18 months. One difference is, you also have to own commercial property.

Biz2Credit PPP

During this past year, over the course of the COVID-19 pandemic, Biz2Credit has also worked with a lender to process applications for the Paycheck Protection Program. Many who applied with them did so because they were one of the last accepting applications. Like many lenders in the midst of the program, there were some definite rough spots, however they very well may be approved to help again if the program continues.

Is Biz2Credit Legit?

They are. They have an A+ grade with the Better Business Bureau and an average of 3.86 starts out of 26 reviews. On Consumer Affairs, they have close to 3.5 stars with 31 ratings. Reading through the reviews on Consumer Affairs, it seems that virtually all of the bad reviews are related to the PPP program. Almost every other review is 5 stars. This definitely appears to be a legit business, and it seems they work with reputable lenders.

How to Find More Legit Lenders Avoid Predatory Lenders

So, Biz2Credit is a great option. Working with them can be a good step in finding the funding you need while avoiding predatory lenders, as it looks like they work with lenders that are reputable. But, what if they will not work for you? What if you do not meet their requirements or you need a different type of funding? How do you find a lender that can help without falling prey to the sharks? You have to know the signs of a predatory lender.

Signs of a Predatory Lender

What are the signs of a predatory lender? There are many, and not all of them are an automatic stop sign. However, some are. All of these are definitely red flags that should cause you to take a closer look.

Focus on Monthly Payment Rather Than Actual Loan Amount

If a lender insists on one large payment at the end of the term, with only interest payments being made each month until that point, proceed with caution.

Unnecessary Extras Without Your Knowledge

Another common practice of predatory lenders is adding unnecessary extras onto the loan. These are usually things the borrower does not needand is not even aware of their inclusion. The most common of these seems to be insurance products that do not offer any benefit.

Confessions of Judgement

If a borrower signs a confession of judgement, they are basically agreeing to lose in a court battle if there is a dispute about repayment. Many cash-advance companies, which make up a large faction of predatory lenders, have their borrowers sign one of these.

New York state law is friendly to this type of contract. Regardless of where a loan takes place, it may include a “New York confession of judgement.”

If you see one of these in your loan documents, do not sign it. It only benefits the lender, not the borrower.

Check out our professional research on bank ratings, the little-known reason why you will – or won’t – get a bank loan for your business.

Punishment for Early Payment

Look closely at loans that have a penalty for prepayment. The bottom line is, early payment is good. Even though the lender may lose some interest, they should not be too opposed to early repayment. Alone, this should not be the reason you do not take a loan as it isn’t uncommon. But, it should make you tread carefully and be on the look out for other red flags.

Seeking the Weak

Business loan companies that specifically seek out underserved populations, such as minorities and immigrants, and those with bad credit are cause for concern. Especially if they are contacting business owners that fit into these types of categories unsolicited, or targeting them with marketing campaigns designed for them specifically. In fact, those that fall into these categories are more likely than others to fall prey, according to a 2015 Center for Responsible Lending Report.

Starting with a Bad Deal

Some lenders try to earn trust by admitting they are offering a bad deal. Then, they promise to fix it in the future. Usually this includes a claim that they will allow for a refinance later that will be better. Don’t fall for it. A bad deal is a bad deal.

Loan Flipping

While flipping a house can be very profitable, loan flipping is actually a classic predatory lending move. When the lender sees that you are struggling, they will offer a refinance. But, you end up paying points and fees again. As a result, before it is over, you could owe more than your original loan.

Check out our professional research on bank ratings, the little-known reason why you will – or won’t – get a bank loan for your business.

The Best Way to Avoid Predatory Lenders Is to Work with a Business Credit Expert

In the end, even knowing all the signs doesn’t guarantee you will avoid the sharks. This is especially true if your credit isn’t great. They can smell blood in the water. Biz2Credit seems to work with reputable lenders, but sometimes that’s not enough.

In addition to researching lenders, reading reviews, and making phone calls, you need someone on your side to ensure you are set up in the best way possible to get the best funding options for you.

Our experts at Credit Suite can not only help you find the funding you need, but so much more. They can help you assess your overall fundability so that you can see where your trouble spots are. Then, they can help you make the necessary changes, including helping you build business credit, so you can get the funding you need to run and grow your business.

There is a lot of talk out there about Accion small business loans. When it comes to this type of alternative lender, it can be hard to know for certain what you are getting into. There are so many predatory lenders in the industry these days, you can never be too careful. You should research any lender before you apply for a loan from them. In this review, we’ve done the work for you to help you make an educated decision.

Is An Accion Business Loan for You?

The thing is, Accion isn’t for everyone. Some of their loans are specific to certain regions. Others are for pretty much anyone nationwide. What’s what, and what’s right for you?

What is Accion?

They are a nonprofit lending network dedicated to helping small businesses. They offer small business loans, some grant opportunities, and other resources designed to help both startups and established small businesses grow and thrive.

Globally they have been working their magic for 55 years across 4 continents. Tens of millions of entrepreneurs have been helped by them. They came to the United States in 1991.

They lend to small business owners in general, from all backgrounds and most industries. However, they specialize in underserved populations. These may include:

Women-owned businesses

Veteran-owned businesses

Businesses owned by Native Americans

Business owners with disabilities

And Minority Owned businesses

They also boast specificallying helping to fund salon owners, green businesses, and those in the restaurant, food, and beverage industries.

What Types of Small Business Loans Do They Offer?

There are a few different types of loans. However, two of them are only available in certain areas of California. These are the Rapid Loans and the COVID-19 Relief Loan program.

Alternatively, they also have SBA Community Advantage loans that are available nationwide. These loans range from $50,000 to $250,000. These are for established businesses with less than 100 employees. It is also available to partially funded startups that need larger loans to scale.

You can also see more options that may be available to you by specifying which area of the country you are in by zip code. Interest rates vary by region and risk factors, ranging from 7% to 34% APR.

What Makes Them Different From Other Lenders?

They do not rely as heavily on credit score in the decision making process as more traditional lenders do. Rather, they look closely at the whole financial picture. If your credit isn’t great, they work with you to help determine your business strengths. Then, they help you determine which products they offer may be a good fit for your business.

The application process is completely online. However, you are not left wondering if you qualify or not, or why you do not if that is the case. Within 2 days you will receive a personal phone call walking you through your approval status. If you are approved, they will work with you on the rest of the process.

If you are not approved, they don’t just say “see you later.” They offer help and resources to improve your situation. You can reapply in 3 to 6 months.

Do You Have to Have Good Credit to Qualify for an Accion Loan?

They do not rely as heavily on credit as traditional lenders. However, they do require a minimum personal credit score of 575. That is, except for the Community Advantage program which requires a minimum of 525. In addition, they have strict requirements related to debt and financing. These include:

You must be current, described by Accion as no more than 30 days late, on all debt and bills.

If you are late, within the 30 days, it must be by less than $3,000.

You can have no bankruptcy in the past year.

There can be no foreclosures in the past 2 years.

There must be at least 2 years worth of revenue.

You must have the cash flow to repay the loan.

For startups, the 2 most recent pay stubs must also be provided, along with a partner referral from an organization such as SCORE or an SBDC. Theremust also be a business plan with a cash flow projection, and the owner must have at least 20% of the total cost invested.

Other restrictions may apply based on a number of factors.

Do They Have a Good Reputation?

As part of a review, it is always good to look at other online reviews and ratings on sites such as the Better Business Bureau and Trust Pilot. The organization is not rated on either of these. In fact, there are not a ton of reviews out there at all. However, their longevity and lack of substantial negative reviews speaks volumes.

Accion Pros and Cons

The major pro of working with Accion is the accessibility to underserved populations. They are a nonprofit organization with a mission to help, not hinder, small businesses.

The big con is that their product options are severely limited if your business is not in California. Also, the interest rates can get high, depending on where you are and what risk factors are present.

What to Do If You Do Not Qualify

What if you do not qualify for a loan with Accion? Well, there are a number of options. However, as mentioned, they will help you understand the reasons why you did not qualify, and help you figure out how to change that.

What they do not do is help you find other funding options, or help you build your business credit. All of their loans are business loans, and therefore guaranteed by the business. Most, however, will also require a personal guarantee. They will offer coaching to help you correct the issues keeping you from loan approval with them, but they do not work on establishing and building a business credit score. This is hugely important to overall company fundability.

This is where the business credit experts at Credit Suite can help. These experts can help you assess your fundability, and walk you through the process of correcting it. In addition, they already work with reputable lenders, and can help you find the lenders and funding options that best fit your needs and eligibility right now.

Conclusion

This is the real deal, and they offer great options for those in underserved populations or that do not have great credit. It’s concerning that they do not list more solid interest rates on their website, but this is for a very good reason. Rates vary widely based on location. However, the online application process is fast. You should know what, if anything, is available to you in a couple of days.

Also, keep in mind that whether or not you can get a loan from Accion, Credit Suite’s experts are available to help you build fundability, increase your business credit score, and make sure your business is in the best position to get the funding it needs at the best rates and terms available.

Disclosure: This content is reader-supported, which means if you click on some of our links that we may earn a commission. For reliable hosting that focuses on speed, A2 Hosting provides plenty of options to get your site up and running. If you’re familiar with SEO and the ranking factors Google uses to decide where …

Disclosure: This content is reader-supported, which means if you click on some of our links that we may earn a commission. For reliable hosting that focuses on speed, A2 Hosting provides plenty of options to get your site up and running. If you’re familiar with SEO and the ranking factors Google uses to decide where …

Disclosure: This content is reader-supported, which means if you click on some of our links that we may earn a commission. For reliable hosting that focuses on speed, A2 Hosting provides plenty of options to get your site up and running. If you’re familiar with SEO and the ranking factors Google uses to decide where …

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

for each business. This is a financing profile that is intended to help the company improve funding possibilities, access new opportunities, and find the best funding solutions.

for each business. This is a financing profile that is intended to help the company improve funding possibilities, access new opportunities, and find the best funding solutions.