One of the inevitable side effects of having a fleet of vehicles is they do nothing for you if they’re idle. In fact, you lose money on them, as you need to pay for parking. Plus, of course, they’re depreciating every single day. Turo is a company that can help you turn idle vehicles into cash cows – no magic wand necessary.

But first, you need to get the vehicles – and here’s how you do ALL that.

Building Your Commercial Fleet While You Build Your Business and Its Credit

Your business doesn’t start off with good business credit already built. In much the same way, you probably didn’t start with any vehicles. Or, at least, not with business vehicles you wanted to keep. And even if you bought your business fully created, you can still build it to greater heights. For all three goals, it pays to work in an orderly fashion. Step by step, it all works together.

Building business credit means getting vendor accounts. Starting with vendor credit accounts is a proven way to start building business credit. But we don’t include vendors just because they report to the business CRAs. We include them because they have quality products you can use, and great customer service. They are more than a means to an end!

Building Business Credit the Right Way

Let’s start with building business credit. You can’t start with high limits. First build starter trade lines that report (vendor credit). Then you’ll have an established credit profile. Then you’ll get a business credit score. With an established business credit profile and score you can start getting high credit limits.

Use your credit. Pay on time, like you should with personal credit. These vendors we’ll show you will report to the business CRAs. And you’ll build a good business credit score.

But Wait: What is Starter Vendor Credit?

These trade lines are creditors who will give you initial credit when you have none now. These vendors often offer terms such as Net 30, instead of revolving. So if you get an approval for $1,000 in vendor credit and use it all, you must pay the money back in a set term. Such as, within 30 days on a Net 30 account. But there are some revolving accounts still considered to be starter vendors.

Vendor Credit Accounts

You must pay net 30 accounts in full within 30 days. And you must pay net 60 accounts in full within 60 days. Unlike with revolving accounts, you have a set time when you must pay back what you borrowed or the credit you used.

To start your business credit profile the RIGHT way, you need approval for vendor accounts that report to the business CRAs. Once that’s done, you can then use the credit, pay back what you used. Then the account is on report to Dun & Bradstreet, Experian, or Equifax, or some combination.

Once it reports, then you have trade lines, an established credit profile, and an established credit score. With an established business credit profile and score, you can then get approval for more credit under your EIN. For vendor credit, you can usually leave your SSN off the application. Because this credit isn’t offered through a bank. Then the credit issuer pulls your EIN credit, sees a solid profile and score, and as a result can approve you for more credit. Keep in mind, credit through a bank will demand your SSN. It’s an anti-money laundering requirement under federal law.

Vendor Credit Cards

Vendor credit cards will kick off business credit building for your business. Once you’ve added payment experiences from three vendors, and they have sent reports to business CRAs like Dun & Bradstreet, you can start qualifying for fleet credit. Make sure business credit cards don’t report on your personal credit.

Every step and every credit provider is designed to help your business. It’s meant to help you qualify for business credit cards you will actually use. This isn’t building for the sake of building, and it isn’t just to increase a number. These credit providers are going to have what your business needs to succeed.

Business Credit

Keep in mind, business credit is independent of personal. Applying for it often won’t harm your personal credit scores, although it can if you offer a PG and then fail to pay. An inquiry will also impact personal credit. Too many inquires can hurt your ability to get an approval. Building this asset can only help your business. You can help your future business right now.

Vendor Credit Benefits

You need 3 or more vendor accounts reporting to move onto more credit with higher limits and better terms. More reporting accounts are even better. It will take 30-90 days for those accounts to report – 60 days on average. Do NOT apply for tier 2 credit without having 3 or more accounts first.

Getting a Vendor to Pull Credit Under your EIN

There is no Social Security requirement for starter vendor credit. This is unlike bank loans and bank cards. So leave the field blank. Don’t fill in any other number. It’s a violation of two Federal laws.

A blank field will force them to pull your business credit under your EIN. But note: some creditors will still want an SSN for verification purposes. You should present your SSN in this situation. But make sure you aren’t agreeing a PG or personal credit check.

Building Business Credit – What You Really Need to Know

You won’t get a Visa or a MasterCard (bank credit cards) right away. You need to have credit to get more credit. Start building trade lines to get the big payoff. Getting initial credit is the hardest part. The vast majority of trade vendors who issue credit don’t report it to the business CRAs. So, you MUST find sources which actually report.

Using Business Credit Vendors

Check out three of our favorite starter vendors:

Wex Fleet

Marathon

76

All three come from Wex.

Wex Fleet

They report to Experian and D&B. They offer universal fleet cards, heavy truck cards, and universally accepted business fleet cards. Their cards have features supporting a small business. This includes a rewards program. Before applying for several accounts with WEX Fleet cards, leave enough time between applying so they don’t red flag your account for fraud.

If you don’t get an approval based on business credit history, or been in business for at least a year, then a $500 deposit is necessary or a PG. Apply online or over the phone. Terms: Net 15 (Wex Fleet Card), Net 22, or revolving (Wex FlexCard).

To qualify, you need:

Entity in good standing with Secretary of State

EIN number with IRS

Business address- matching everywhere.

D-U-N-S number

Business license (if applicable)

And a business bank account

Business phone number with a listing on 411

Marathon

Marathon Petroleum Company provides transportation fuels, asphalt, and specialty products throughout the US. Their product line supports commercial, industrial, and retail operations. This card reports to Dun & Bradstreet and Experian. Remember: before applying for several accounts with WEX Fleet cards, leave enough time between applying so they don’t red-flag your account for fraud.

To qualify, you need:

Entity in good standing with Secretary of State

EIN number with IRS

Business address- matching everywhere.

D-U-N-S number

Business license (if applicable)

And a business bank account

Business phone number with a listing on 411

Your SSN is necessary for informational purposes. If concerned they will pull your personal credit talk to their credit department before applying. You can provide a $500 deposit instead of using a PG if you’ve been in business less than a year. Apply online or over the phone. Terms are Net 15.

76

Phillips 66 Company owns 76. It has more than 1,800 retail fuel sites in the United States. This card reports to: D&B and Experian. Keep in mind: before applying for several accounts with WEX Fleet cards. make sure to leave enough time between applying so they don’t red flag your account for fraud.

To qualify, you need the following:

Corporate entity must be in good standing with the applicable Secretary of State

An EIN

Company address matching everywhere

D-U-N-S number from Dun & Bradstreet

Your business license (if applicable)

A business bank account

Business phone number with a listing on 411

Your SSN is necessary for informational purposes. If concerned they will pull your personal credit talk to their credit department before applying. You can give a $500 deposit instead of using a personal guarantee. if you’ve been in business less than a year. Apply online or over the phone. Terms are Net 15. You can used this card at any P66, 76, or Conoco fueling location. Let’s move onto fleet credit.

Fleet credit comes after starter vendors. It comes from places like Gulf and Exxon. You use it to:

Buy fuel

Maintain vehicles of all sorts

Repair vehicles

Even businesses which don’t have big fleets can still benefit. These are usually gas credit cards.

You may need to have a minimal time in business. If your business doesn’t have enough time in business, you may be able to instead offer a personal guarantee or give a deposit to secure the credit. Now that you’ve got a bunch of cards to support your fleet, it’s time to look at vehicle financing to buy the fleet!

Vehicle Financing

Chances are you didn’t buy personal vehicles outright. In the same way, financing is a great way to get a vehicle now, without having to wait until you can pay cash and drive it off the lot. With a fleet car, your choices are usually buying or leasing. Providers include banks like Bank of America or the financing arm of the manufacturer, like Chrysler Capital.

Using Business Credit for Vehicle Financing

You can even finance a vehicle purchase or lease through our Business Credit Builder. These offers are in Tier 4. So they have certain requirements that business credit neophytes won’t be able to meet. Lenders will want to see you have the income to support the purchase. Consider Ford Commercial Vehicle Financing.

Ford Commercial Vehicle Financing Through Credit Suite

Ford offers several commercial vehicle financing options. These include loans, lines, and leases to actual business entities. This is not for sole proprietorships. You can get a loan or a lease.

Ford may ask for a personal guarantee if you do not get an approval on the merit of your application. Apply at the dealership. Ford will report to D&B, Experian, and Equifax.

To qualify, you need:

Entity in good standing with Secretary of State

EIN number with IRS

Business address- matching everywhere

D-U-N-S number

Business license (if applicable)

And a business bank account

Strong business credit history

Must have a good Experian business credit score

Ally Car Financing Through Credit Suite

Ally provides personal financing. But they will also report to business credit bureaus. If your business qualifies for financing without the owner’s guarantee, you can get financing in the business name only. Ally will report to D&B, Experian, and Equifax.

Ally Car Financing: Ally Commercial Line of Credit

To qualify, you need:

Entity in good standing with Secretary of State

EIN number with IRS

Business address- matching everywhere

D-U-N-S number

Business license (if applicable)

And a business bank account

Bank reference

Fleet financing references

If you use a PG, Ally will not report to the personal credit bureaus unless the account defaults.

Ally Car Financing: Ally Commercial Vehicle Financing

Get a lease or a loan. To qualify, you need the same things as you need for an Ally Commercial Line of Credit. This is except for a bank reference and fleet financing references. There is no time in business requirement. Apply in person only. The dealer will say if you get approval or must provide a PG. Now that you’ve got the cars and the cards, let’s explore Turo.

Turo is a peer-to-peer car sharing marketplace. You can book any car you want, wherever you want it, from a community of trusted hosts across the US, Canada, and the UK. Guests choose from a unique selection of nearby cars. Hosts earn extra cash to offset the costs of car ownership.

How Do Turo, Business Credit, and Business Ownership Work Together?

There are going to be times when some of the vehicles your fleet aren’t in use. This could happen if there’s a personnel change, or if an employee with an older vehicle gets an upgrade to a newer one. This could be a perk accompanying a promotion. Or an employee with a vehicle could be out for parental leave. But no matter how or why any vehicles are idle. you can be making money from them.

Turning the Idle Vehicles in Your Fleet into Moneymakers

Turo says you can make an average of $620 per month per vehicle. This comes from 2019 stats for hosts with twelve or more trips and “at least average quality metrics”. You can set your own price and availability dates. Make 70% of the price, or 80% if you can prove you have your own insurance and waive Turo’s coverage. Turo offers an array of coverage options with different percentages and deductibles. So you can choose what appeals most to you. Liability insurance comes from a policy issued to Turo by Liberty Surplus Insurance Corporation. They’re a member of the Liberty Mutual Group.

Bringing Out the Best in Your Vehicles to Make the Most Money

There are ways to make more money and get your vehicle out there to more riders, more often. Turo offers tips on taking better photographs of your car and listing your car’s options. as riders may be searching for things like all-wheel drive or air conditioning, etc.

Working with Turo

Turo will provide guidance on how to write better descriptions, and otherwise make a vehicle more appealing to riders. There is even a section on writing a business plan. Also – earnings go through Turo so you will get a 1099. And even making a few hundred per month per vehicle is a VAST improvement over letting a vehicle idle while you pay for parking and it depreciates! To end, let’s touch on personal guarantees for financing.

Vehicle Financing

With commercial vehicle financing, business owners may need to personally guarantee vehicle loans. If you are a co-borrower the loan will most likely report to your personal credit report. Starting off by giving a personal guarantee means you can get money, and start building your commercial fleet now instead of later.

PG (Personal Guarantee) Financing

According to Investopedia, a personal guarantee is:

“an individual’s legal promise to repay credit issued to a business for which they serve as an executive or partner. Providing a personal guarantee means that if the business becomes unable to repay the debt, the individual assumes personal responsibility for the balance. Personal guarantees provide an extra level of protection to credit issuers who want to make sure they will be repaid.”

When you provide a PG, you are adding your Social Security number to the application. You should expect a hard inquiry. You’re also adding the details of your personal income to the application.

No PG Financing

With no PG financing, you can get higher limits and better terms. Continue to build exceptional business credit and pay your bills on time. In general, the following you won’t need to provide a personal guarantee for this type of financing if you have:

good business credit

a decent amount of time in business or

good personal credit

Much like with any other kind of business borrowing, the more assurances you can give the lender, the better.

Turo, Business Credit, and Growing Your Business: Takeaways

Use business credit to buy everything you need to run a fleet, from fuel to service. And use auto financing to buy the vehicles. Plus, you can make money with the idle vehicles in your fleet! Turn your fleet into a regular, reliable moneymaker – without having to pull any rabbits out of your hat. Let’s get together and talk about getting started.

Maybe you’re not hitting the kind of figures you want, or maybe you haven’t even made a single sale yet. Either way, you’re not selling as much as you want to be.

But why aren’t you?

There are tons of possible reasons here, but I’m willing to bet it’s your website. Even if you have an expertly designed site, it could still be the culprit that’s stealing all your sales.

I learned this the hard way. My websites used to flat out suck and I barely got any sales. Once I started putting serious effort into my sites, my sales skyrocketed.

I tried everything. Some stuff was a huge waste. Some techniques ticked off my users.

But I was able to find some serious long-term winners.

While there’s no magic formula that will 10x your sales overnight, there are some best practices that will help you optimize your website to pull in the maximum amount of sales possible.

In short, you want to turn your site into an automated sales machine.

And I’m going to show you exactly how to do that.

Ready?

Setting Up Behind the Scenes With a CRM

The first thing you need is great customer relationship management (CRM) software.

A CRM helps you manage all of your current customers and leads in one place. You can communicate, track progress, and oversee all interactions without having to leave the CRM.

The reason you want to use a CRM is that it will help you generate the most amount of money out of your customers. And this is a lot easier to do than it is to acquire new customers.

When my friends at Keap reached out to let me know about their rebranding, I realized it had been a long time since I talked about how important their tool is in my arsenal.

Now, throughout the rest of this article, I’ll show you how I use Keap to grow NeilPatel.com.

But first, let me go into what it does… that way whatever solution you decide to choose, just make sure it has these features.

All-in-one Client Management

A good CRM should provide everything you need to manage your customers. You shouldn’t have to use extra software or apps to fill in the cracks.

That means your CRM should allow you to manage every interaction between you and your customers. You should be able to look at your CRM and know exactly where you are with any given client.

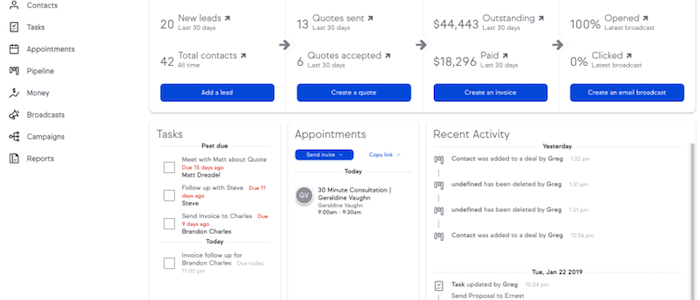

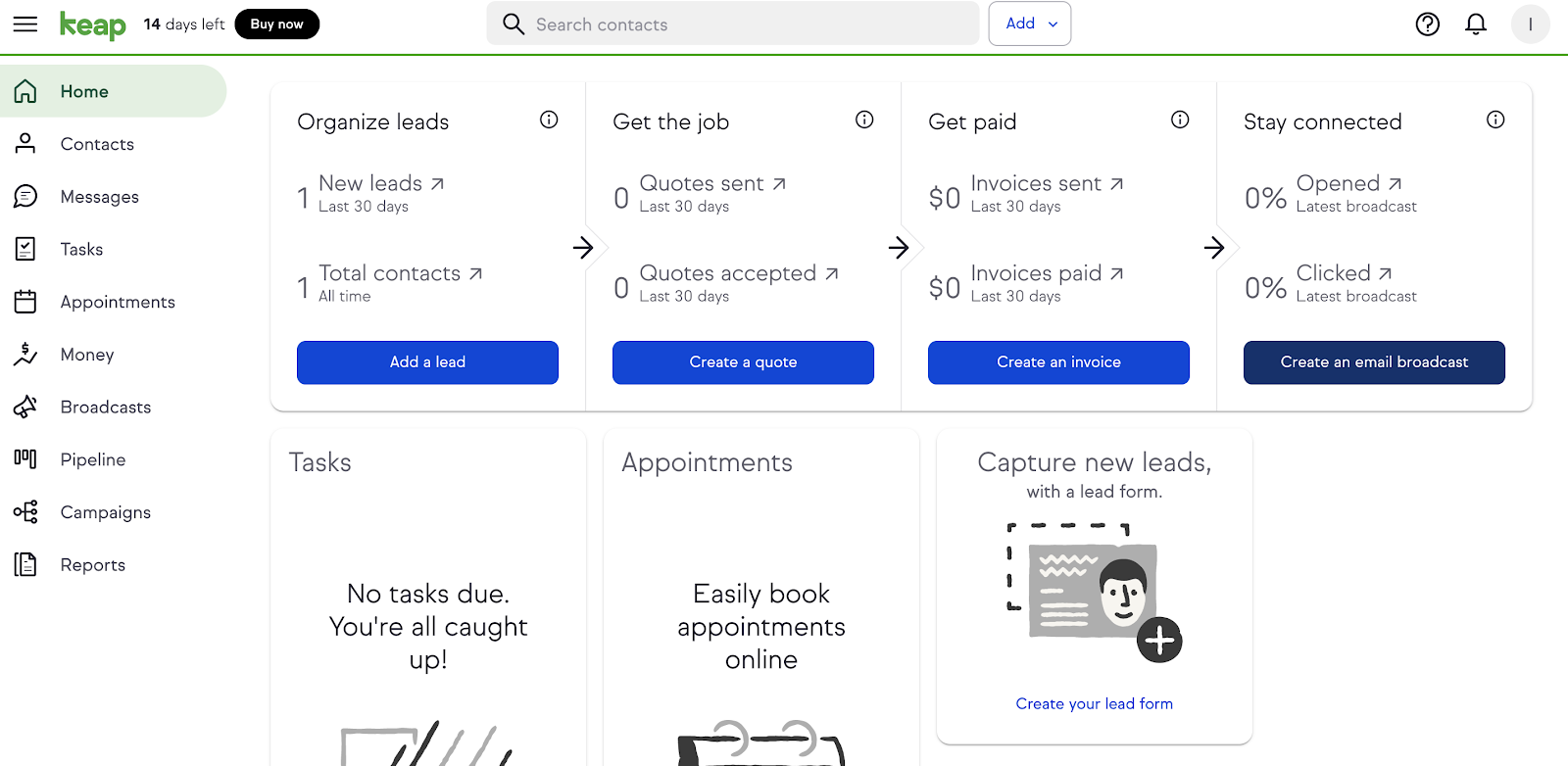

Here’s what it looks like when you first view your dashboard:

Having a simple, minimalistic design like this really helps cut down on the confusion that comes with managing tons of clients. There’s no second-guessing.

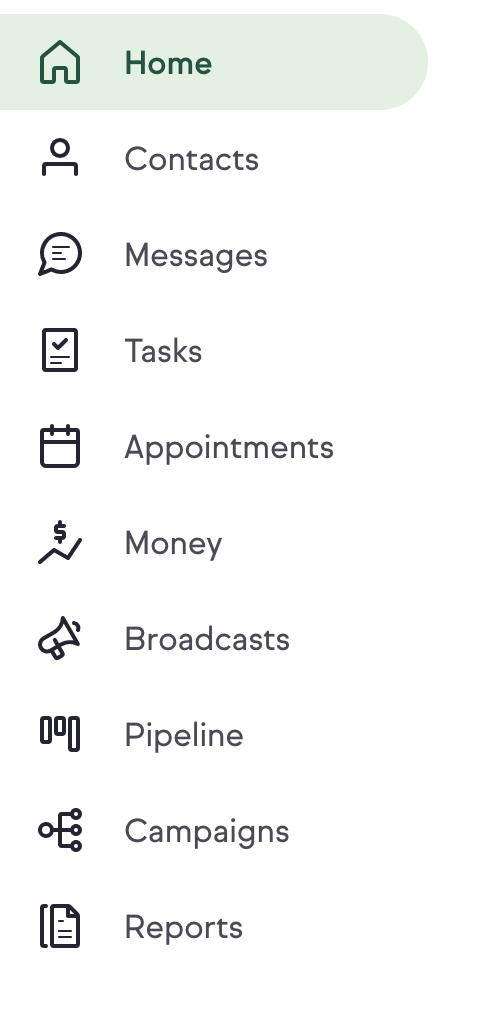

Take a look at the menu on the left-hand side:

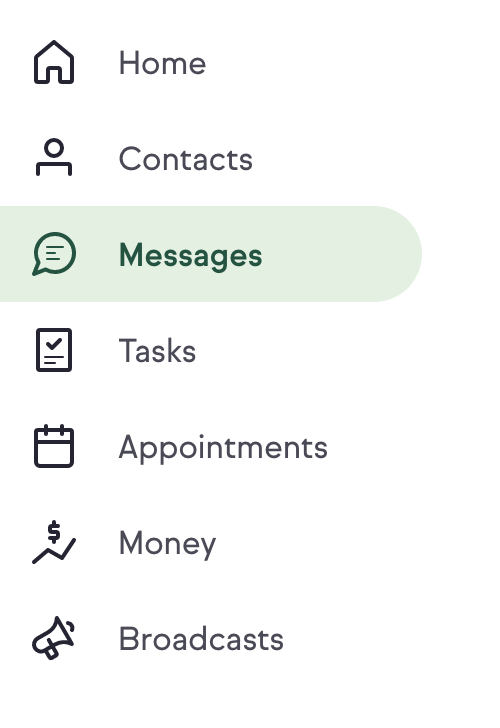

Keap has taken all the ways you interact with your customers and broken them down into nine intuitive categories.

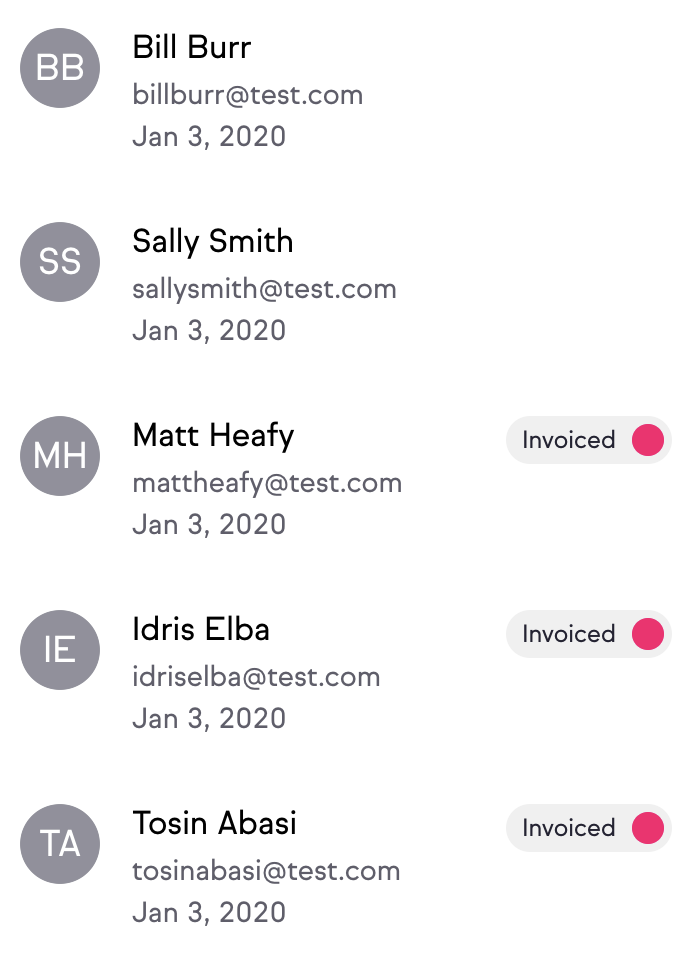

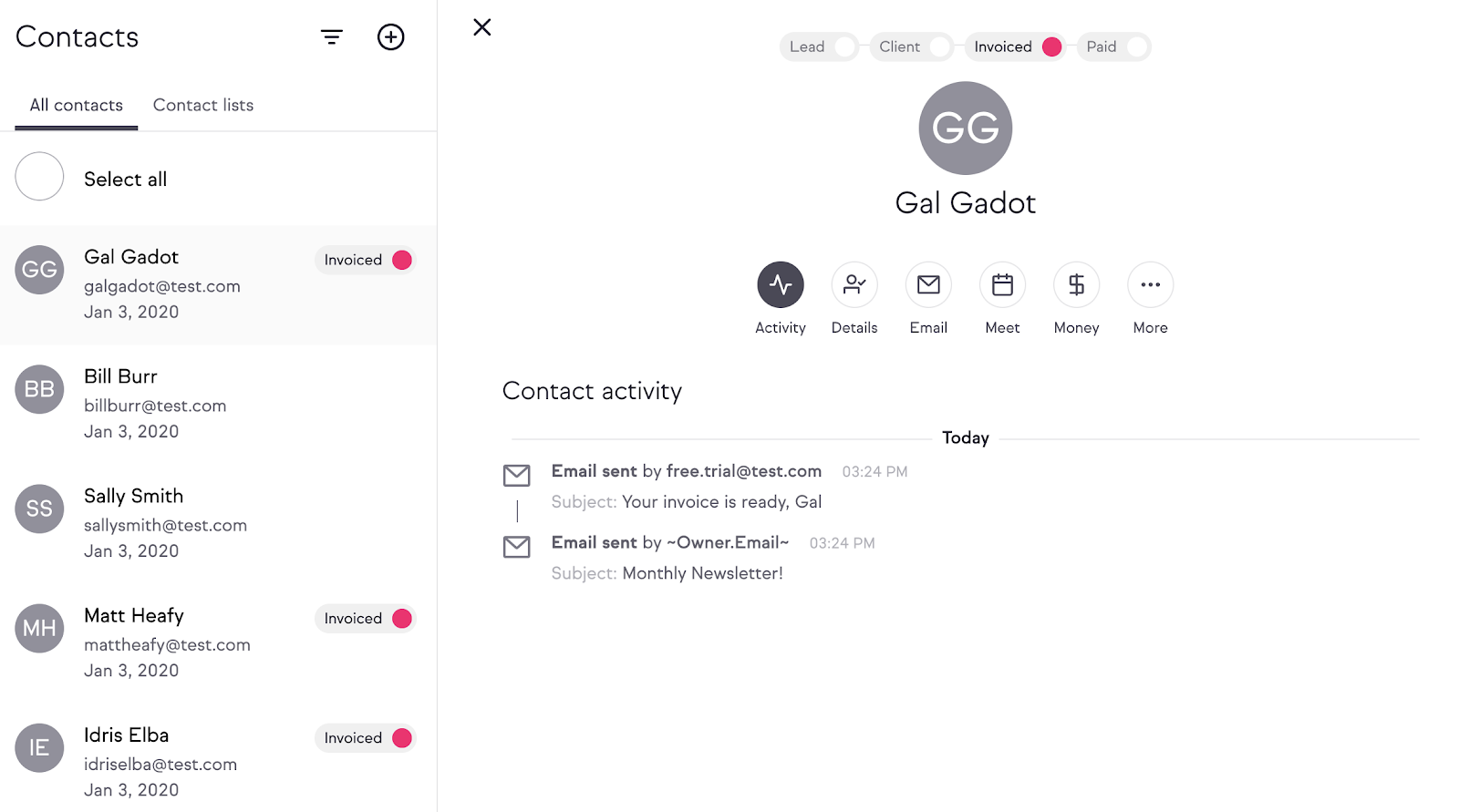

By clicking on the Contacts tab, you can see all of your clients:

By clicking on a particular client, you can see a summary of your activity with that person, including email conversations and invoice history.

This is important for me and my team as we offer multiple products and this view helps us understand where people are.

Remember, by having multiple products you can maximize your lifetime value, which then allows you to spend more money on marketing.

There’s also a separate message function that you can access by clicking on the Messages tab:

Here you can see all of your correspondence with each client. You’ll need to connect your mobile phone with the Keap app. This allows you to seamlessly switch between mobile and desktop for an efficient messaging experience.

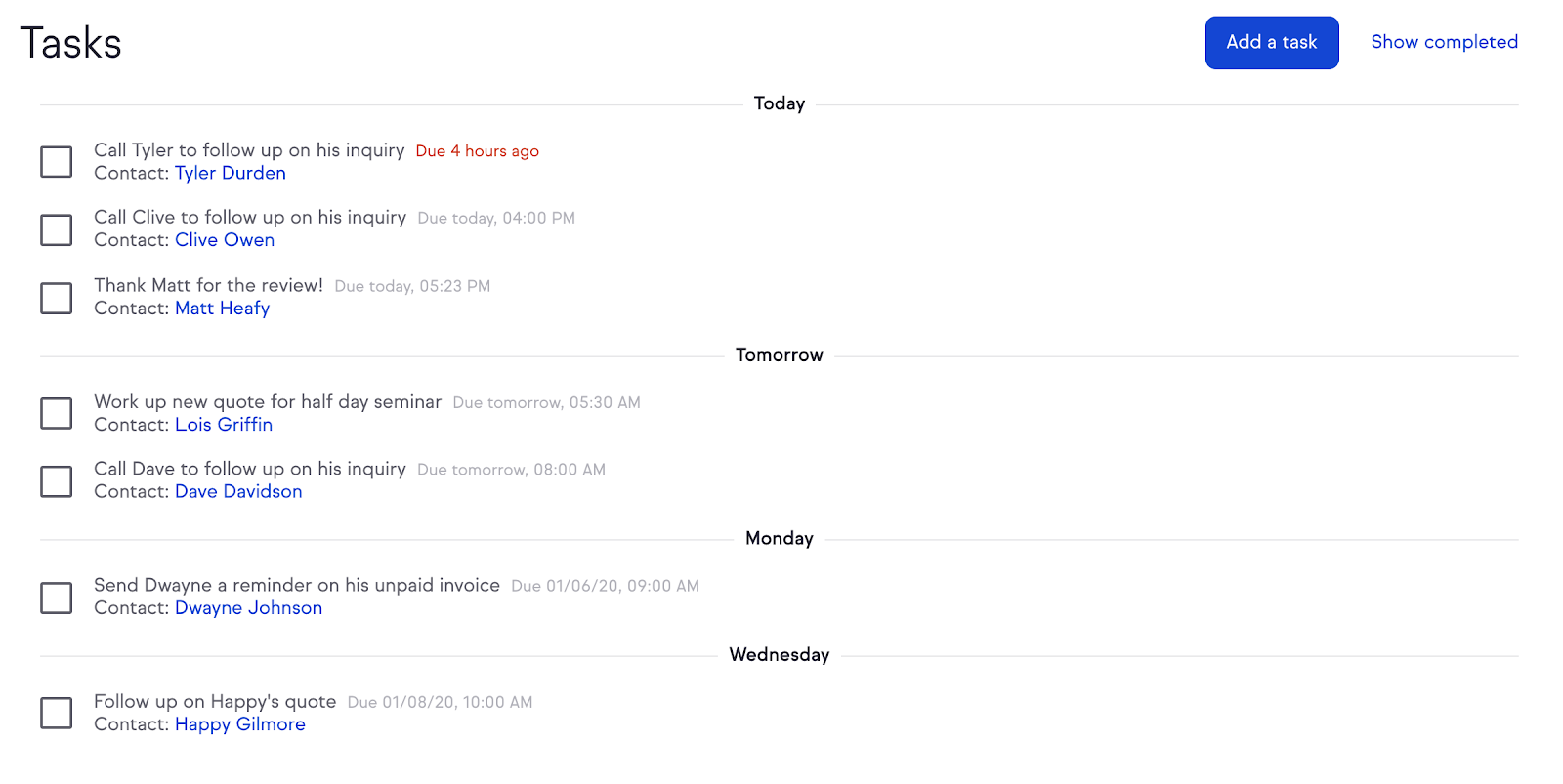

The Tasks tab gives you a rundown of your to-do list for your clients:

You can check off each task here and easily add more by clicking the blue “Add a task” button at the top right. This way, you’ll never lose track of what you need to do.

Next is the Appointments tab, where you can set up a custom booking link to allow clients to schedule appointments with you. You choose your own availability so that clients always choose times that work for you.

This is great if you regularly have face-to-face interactions with your clients for example.

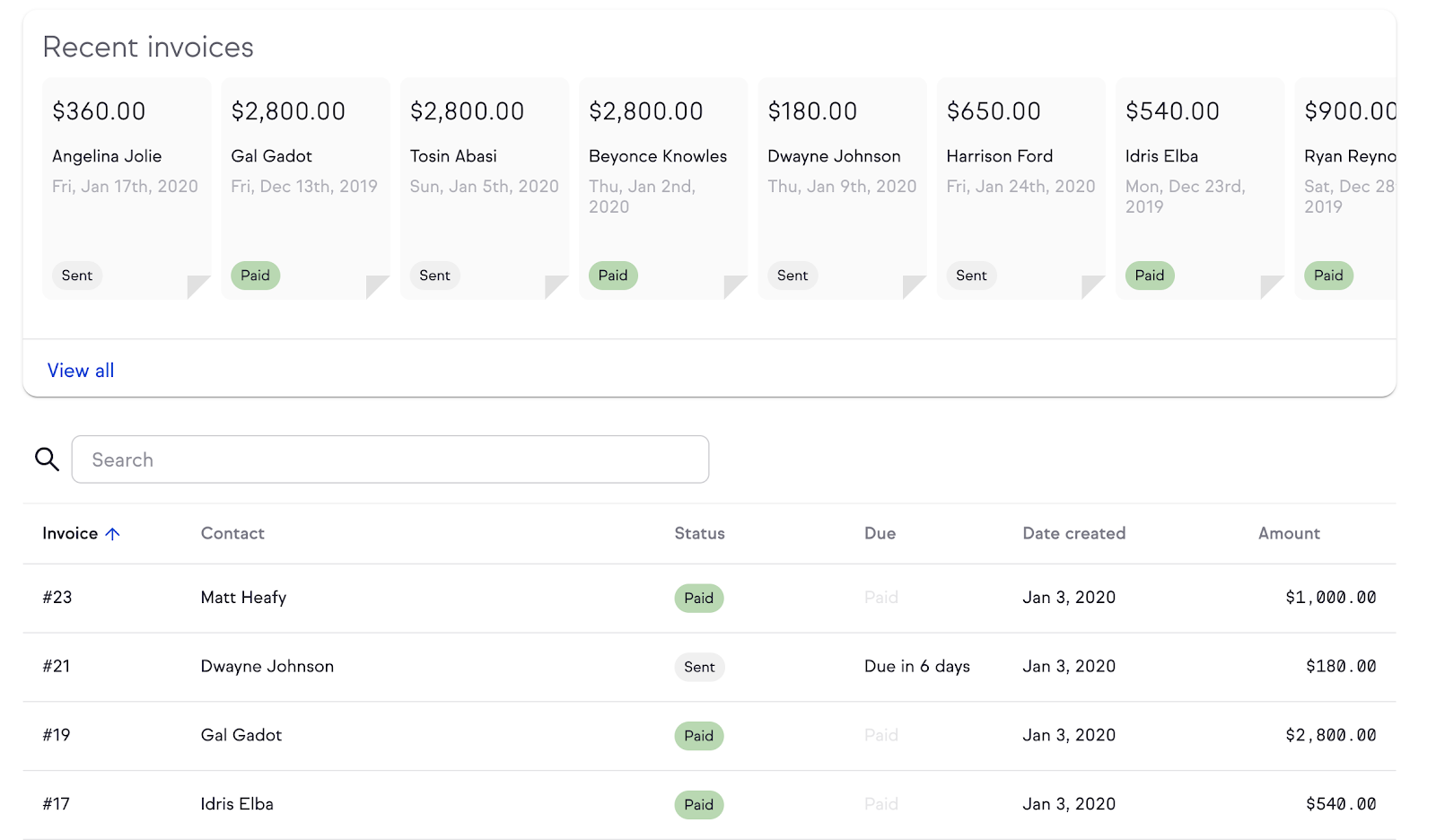

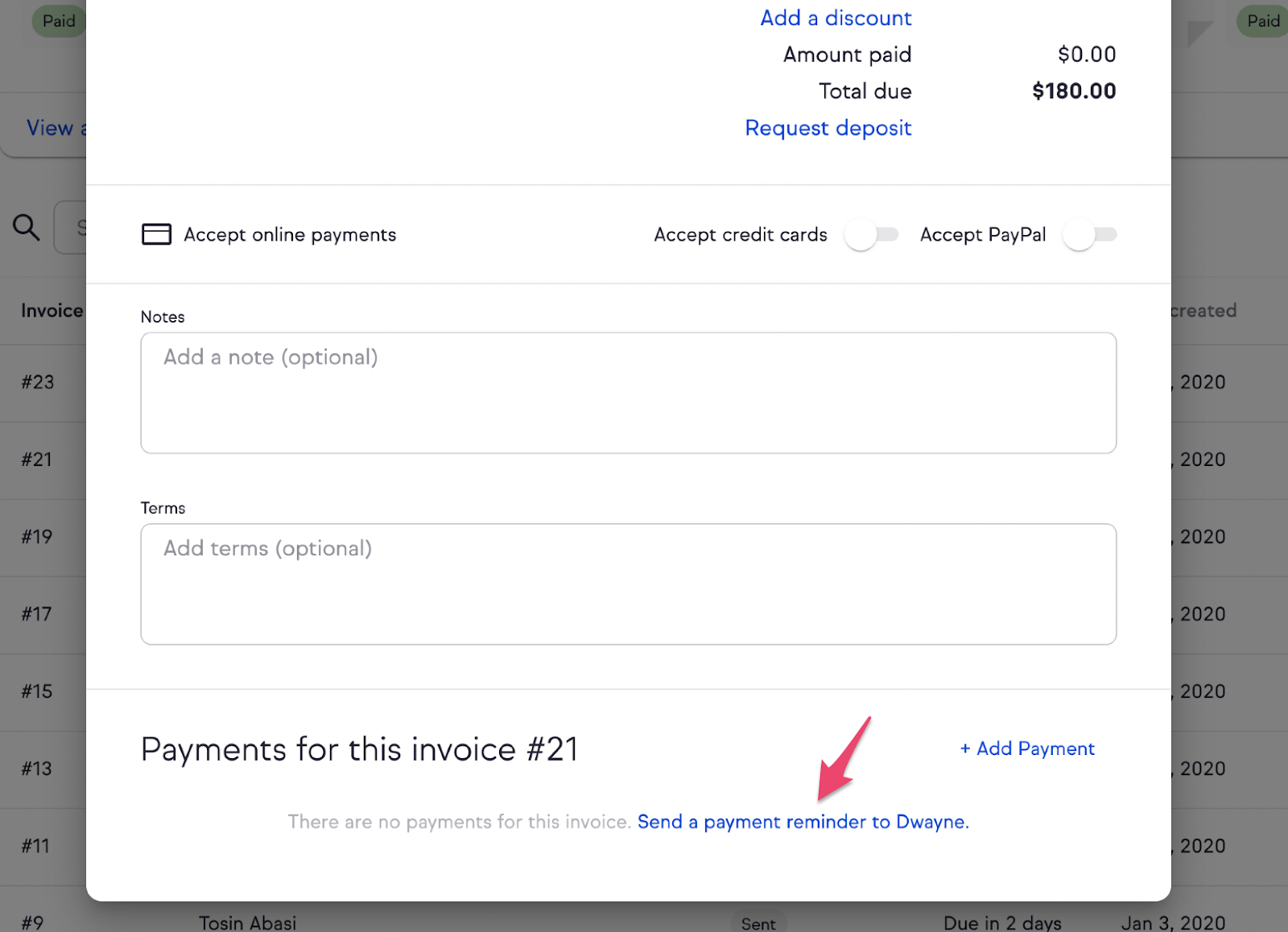

The Money tab is your one-stop-shop for all things finances. You can connect your bank to get paid in a flash and you can also manage all your invoices without any fuss.

You’re always aware of who’s paid and who hasn’t, so you don’t have to go chasing down clients one by one. You can simply send them a reminder within the interface by clicking on the specific invoice and scrolling to the bottom where there’s a reminder option:

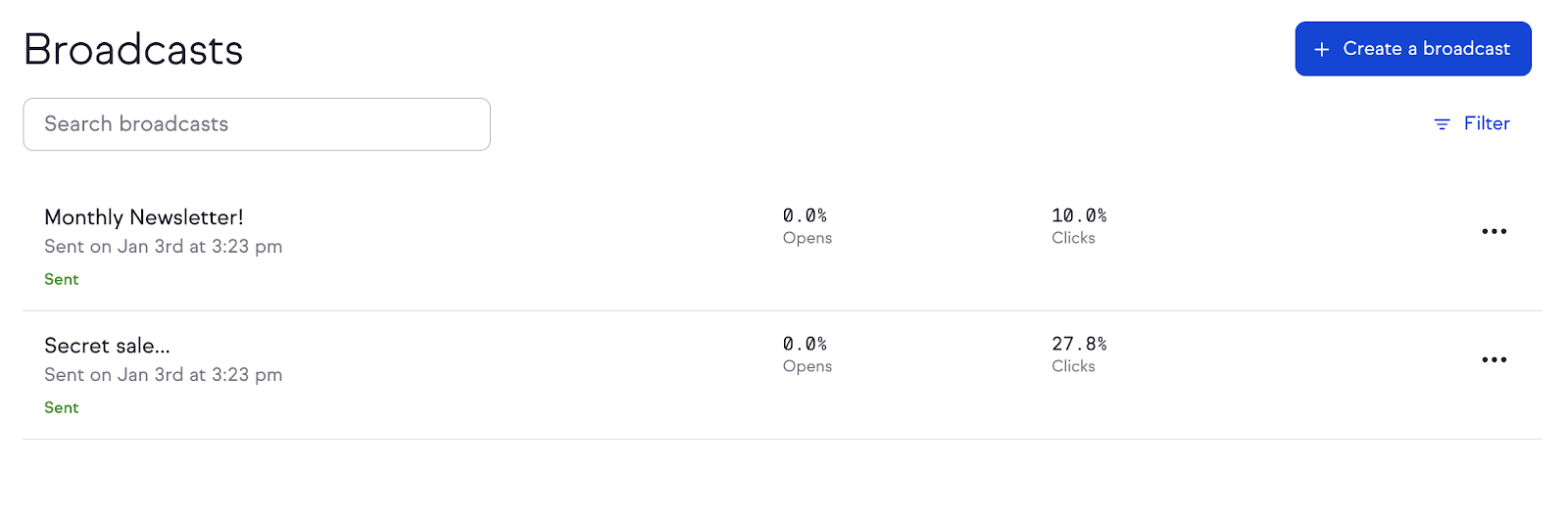

The Broadcasts tab allows you to send out emails to your list.

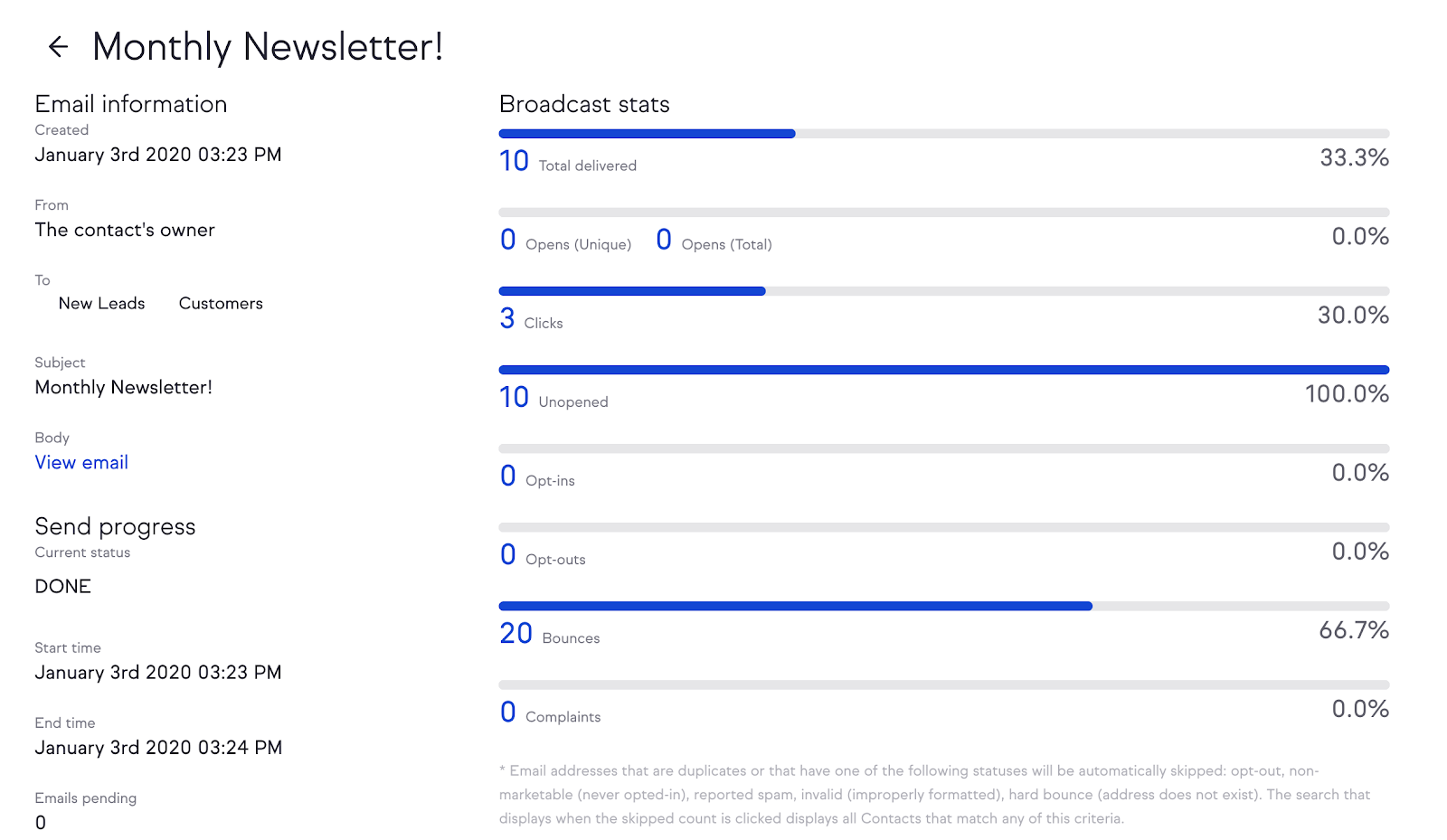

Even though this isn’t standalone email software, you can still see a ton of helpful metrics by clicking on each campaign:

This feature is especially helpful for sending out emails to specific groups, like new leads or existing customers.

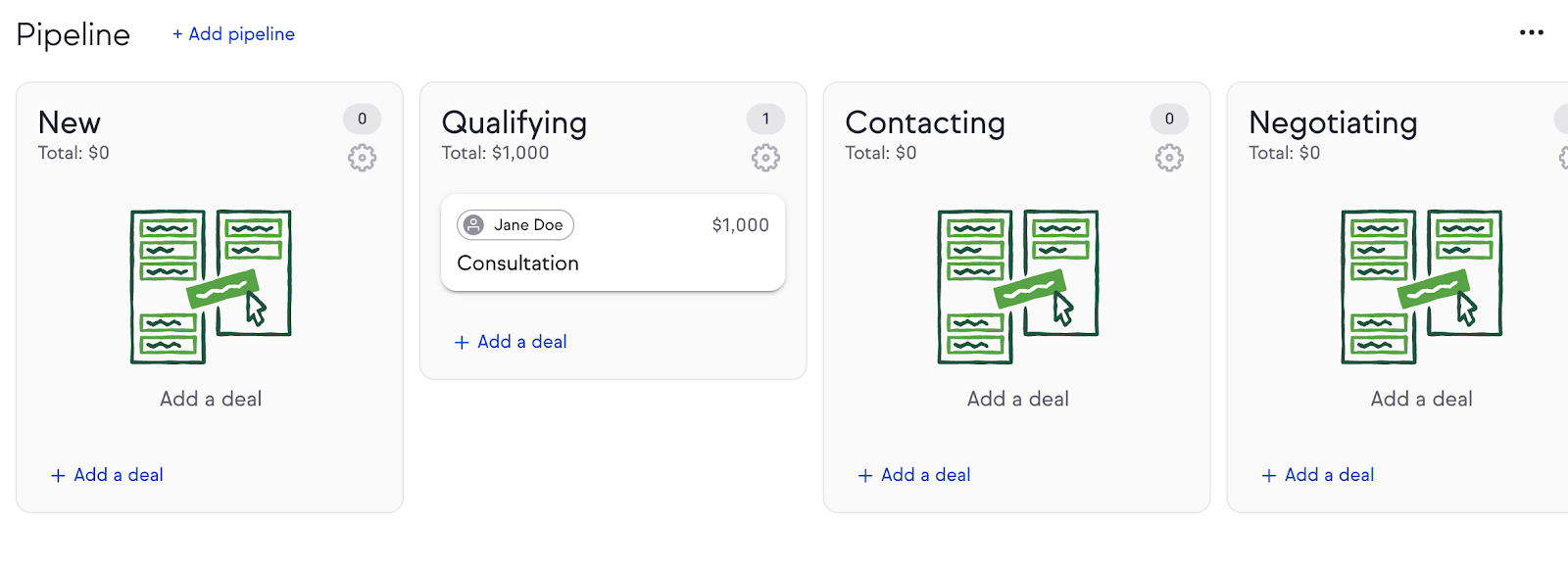

Next, you’ll see the Pipeline tab. This is where you build the core of your customer journey.

Once you click on the Pipeline tab, you’ll see four basic panels: new, qualifying, contacting, and negotiating. These are the stages that you’ll go through when converting a new prospect.

This is also where a lot of the automation happens that will save you tons of time and money. I’ll go into detail on this later on in the article, but for now, just remember this pipeline structure.

The Campaigns tab is a full-featured campaign manager that allows you to follow up with leads, track unpaid invoices, simplify scheduling, and much more. (You can also automate a lot of things here.)

Finally, the Reports tab helps you stay on top of your sales. Here you can also track important metrics like email engagement and campaign progression.

Take another look at all of these features. This is what I mean by all-in-one. A CRM should allow you to interact with your clients in any way you need to. You shouldn’t have to jump from software to software to create a great experience for your clients.

Now that we’ve looked at some basic elements of a good CRM, let’s look at one of the must-haves: automation.

Automation

Automation is hands down one of the most important features I look for in a CRM.

Why?

Because running a business is a lot of work, and the more you can automate, the better.

Automating is usually straightforward, but when it comes to automating client interactions, you have to be careful.

People love personal interactions, and that’s why you should do your best to deliver. If your automation is dry and corporate, your clients will notice.

So what do you do?

The trick is to personalize your automation as much as possible.

In other words, your automation should have a human touch.

If this sounds counterintuitive, I totally understand. “Personalized automation” seems like an oxymoron.

But it’s not. In fact, it works pretty well.

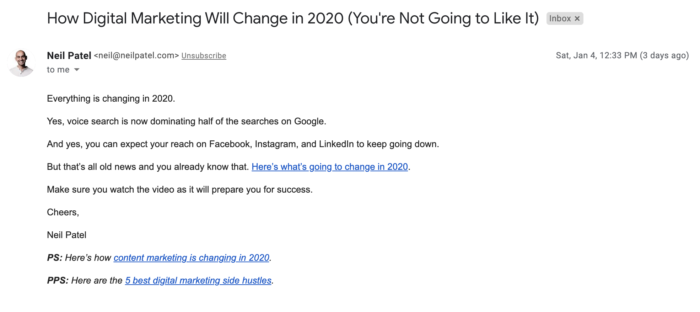

Take a look at this email I recently sent:

Believe it or not, this is a template.

The reason this works so well is that it doesn’t read like a template. It reads like an email I sat down and wrote myself.

Of course, you can automate way more than just emails.

Most automation actually happens behind the scenes, so you need a CRM that’s capable of seamlessly automating everything from client data to scheduling and beyond.

Let’s say I want to email a lead when they move from stage to stage in my pipeline. This is a great technique to keep leads engaged but often you have to do it manually.

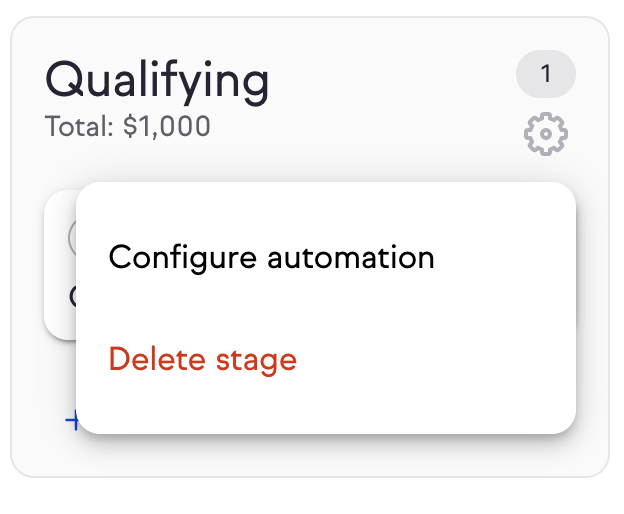

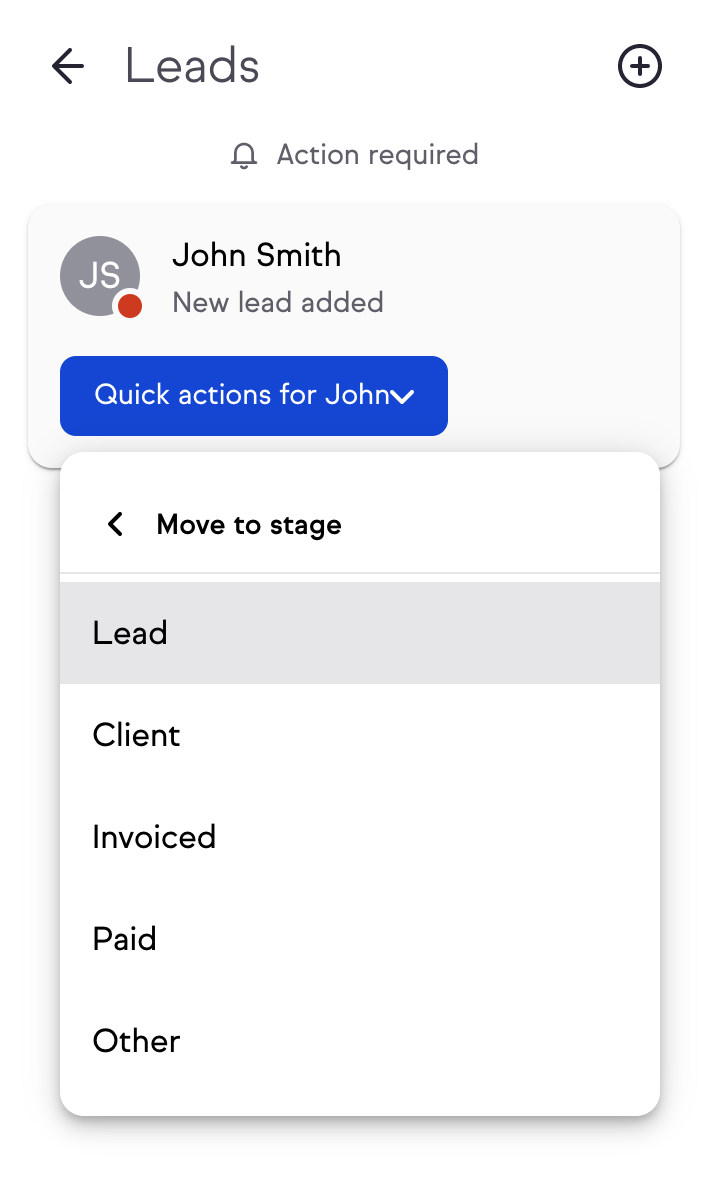

With Keap, it’s simple. First I head to the Pipeline tab and find the specific lead. Then I click the gear icon and select “Configure automation.”

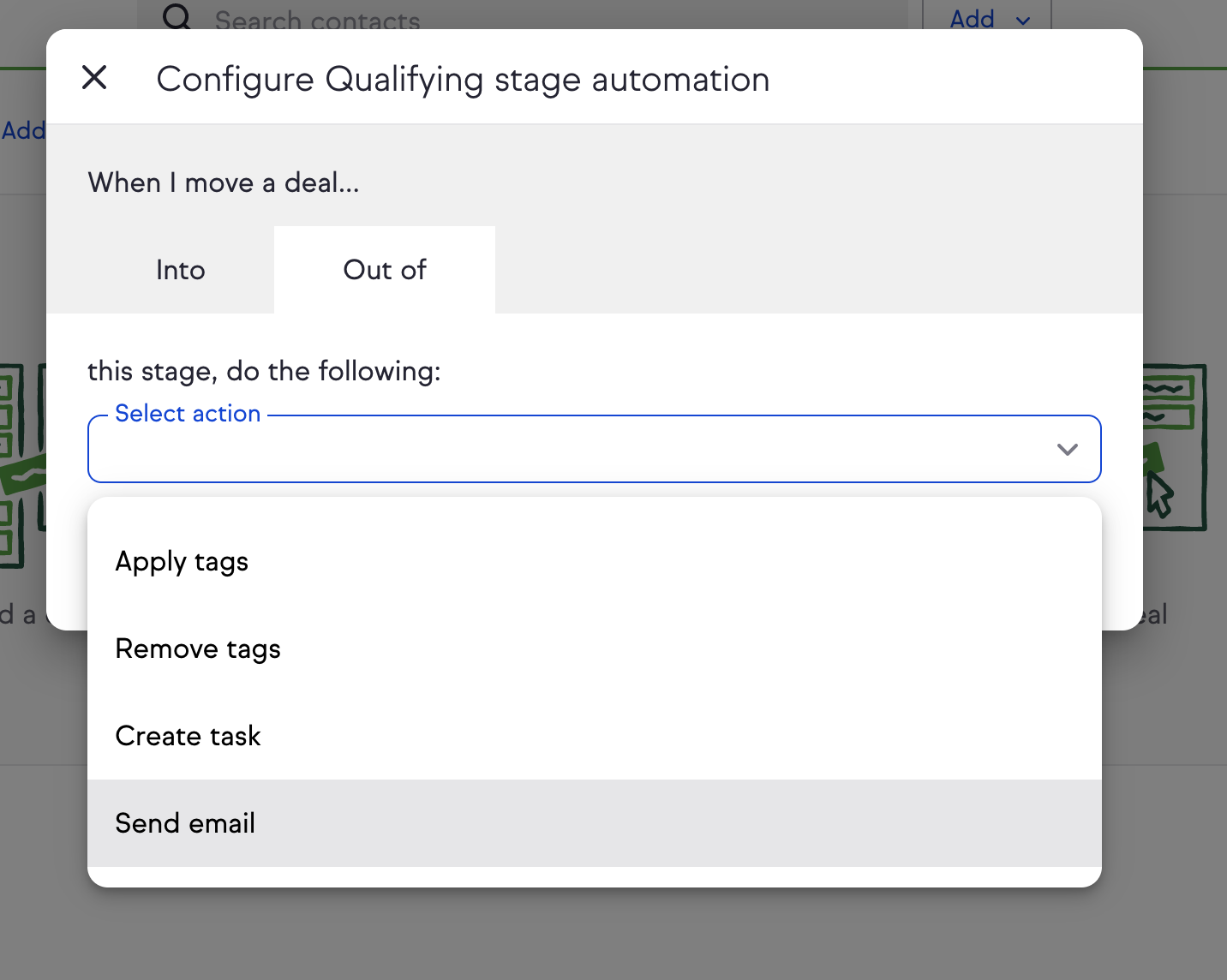

I now select when I want the email to trigger: either moving into or out of a stage. For this example, I’ll have it trigger when the lead moves out of the qualifying stage (where the lead currently is).

Then I select “send email” from the drop-down menu.

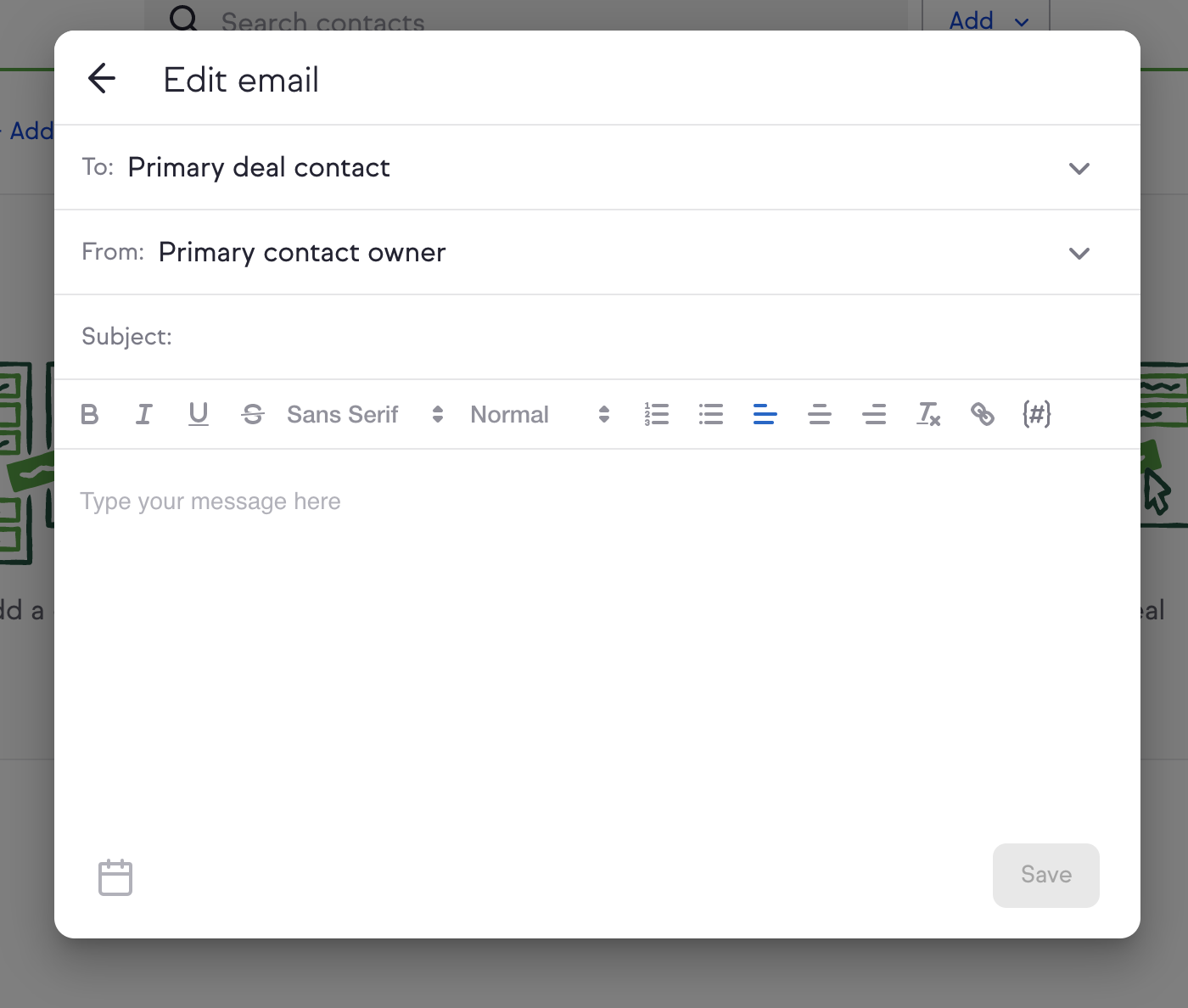

Now all I have to do is write the email.

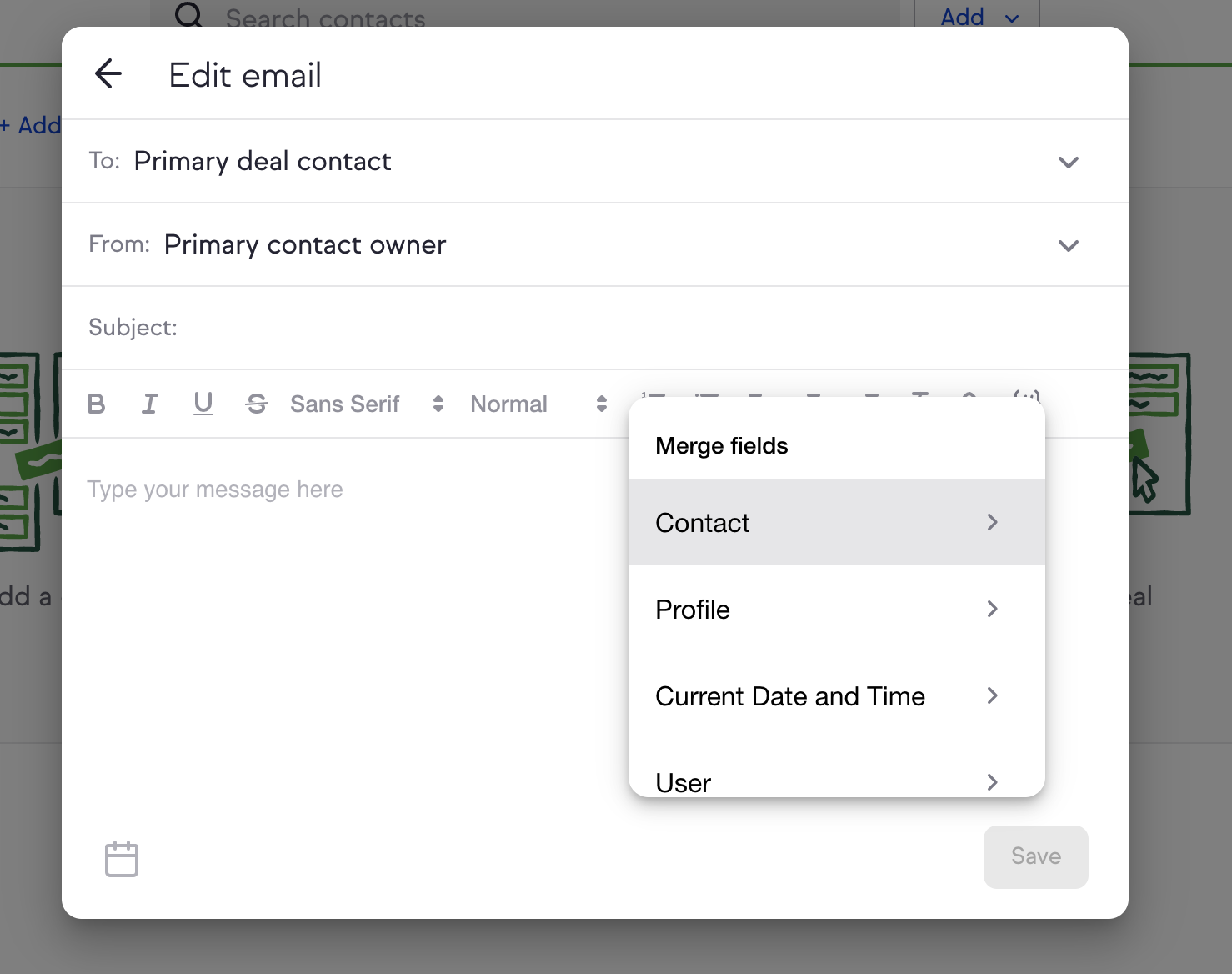

Of course, you can use personalized templates here to maximize your efficiency even more. You can even personalize the email with this form by clicking on the pound sign on the right to open up the merge fields drop-down menu.

This all takes just a couple of minutes and it’s all completely contained within Keap.

See why automation is so important? It’s one of those features I can’t go without.

And I like easy automation. I’m super busy, so the easier something is, the better. I don’t want to have to go through a million menus just to shoot an email.

All of this said, there are definitely right and wrong ways to automate. You want your automation to make your business as efficient as possible and that means creating dependable processes that you can repeat without even thinking about it.

Creating Processes With a CRM

CRMs are useful for a lot of things from qualifying leads to creating entire marketing campaigns.

But there’s a common thread that runs through all of these features: the ability to create processes.

Processes are invaluable because they save you time, effort, and often money.

They also help your business operate more smoothly. Relying on processes is much easier than having to do everything manually.

That begs the question: What kinds of processes should you create?

The short answer is that you should have a process for everything. And I mean everything.

Responding to client emails? Make a process for it. Dealing with new leads? Set up a workflow for qualifying them. You get the picture.

This is critical. If you want to increase your sales, you have to be able to handle increased sales in the first place. Having processes to depend upon will allow you to take on more volume without any unnecessary friction.

As a rule of thumb, if you can automate something in your business, you probably should.

The exception (like I mentioned above) is anything based around human interaction. It’s best to stay as hands-on as possible when it comes to this.

The idea is to make your business run like clockwork so you can pay more attention to your clients and deliver a better experience.

And that’s a win-win for everyone involved.

But let’s get specific and talk about certain processes that you should make sure you have.

Lead Flow

This is a big one.

A lot of marketers focus on lead generation but not enough people talk about what should happen after you’ve got a lead.

If you don’t move your lead forward, your efforts are as good as wasted.

That’s why automating your lead flow process is critical. You don’t want to be doing this by hand––that takes hours.

Instead, let your CRM do it for you.

Create multiple stages along your pipeline and trigger unique email sequences for each stage. This means that you can keep your lead moving forward at all times.

This way, you won’t overlook anything. You don’t have to worry about forgetting to follow up or missing an important email.

So let the CRM do the heavy lifting so you can focus on providing a better service for your customers.

Marketing Emails

With a CRM, it’s possible to automate all of your marketing emails, and in my opinion, this should be one of the first things you automate.

Why? Because emails can take up lots of time without you even noticing.

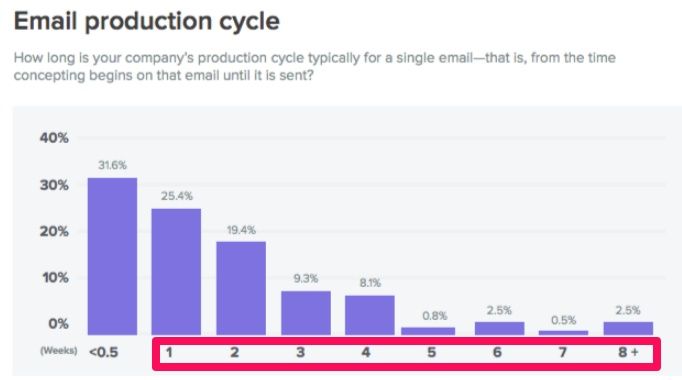

According to the Litmus 2017 State of Email report, more than 68% of businesses spend a week or more on the production of just one email.

Automation allows you to cut back on that time so you’re not working on the same task for days on end. You’re able to spread out your time and attention on other things that need to be handled.

And by automating your email, you’re making your email work for you instead of the other way around.

For example, whenever you get a new lead, you need to take action as swiftly as possible.

With the right CRM, this is a snap. All you need to do is automate it so that a new lead receives an email as soon as they sign up.

That way, you’re able to contact a warm lead immediately and you don’t have to do anything manually.

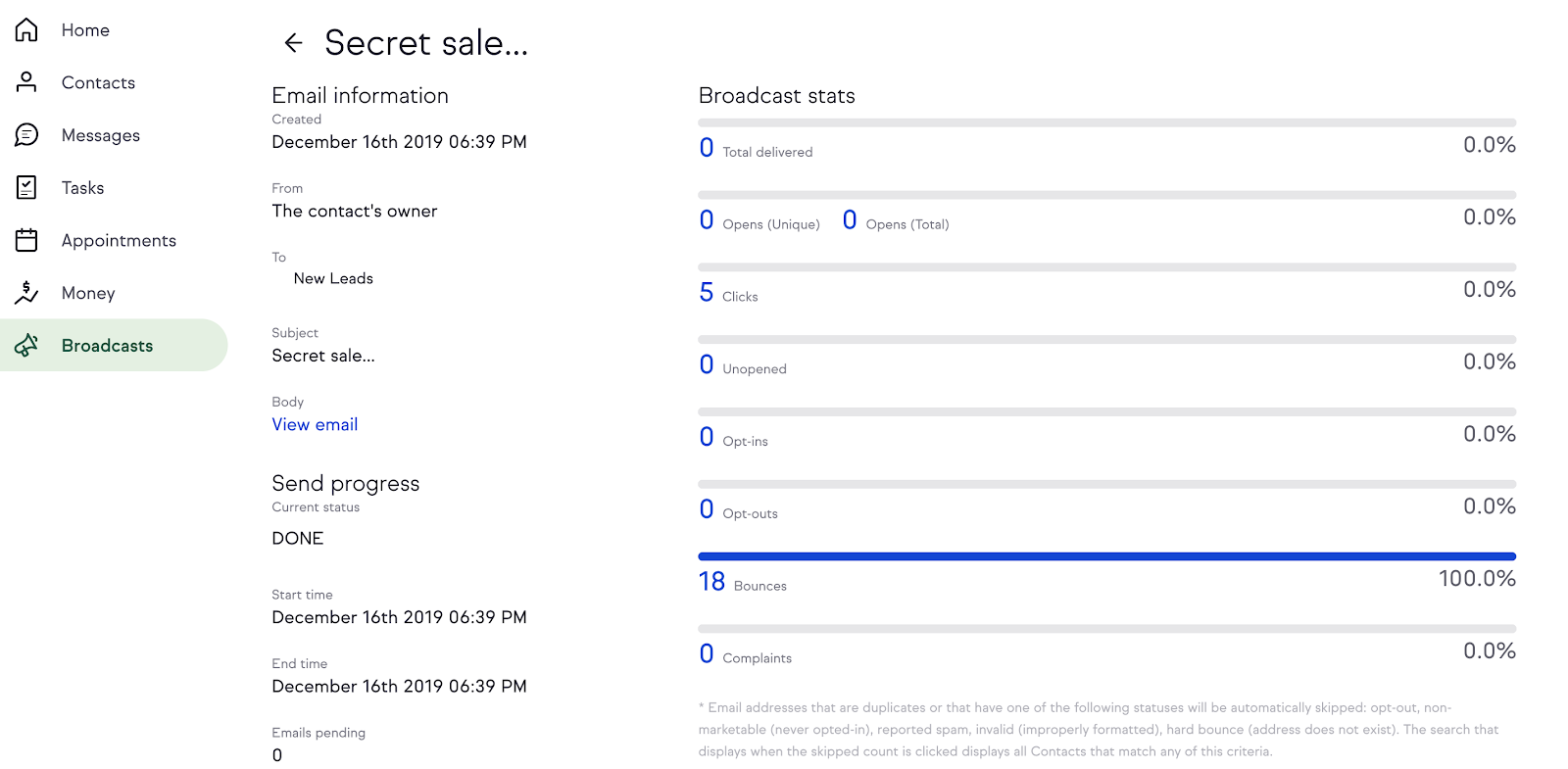

You can track them right from the Broadcasts tab:

This means you can also create autoresponder campaigns to get more clients in the door.

You can then move them down your pipeline, which brings me to the next thing you need to do: build a robust pipeline.

Building a Streamlined Sales Pipeline

If you’ve ever wondered what’s stopping your site from raking in the sales, chances are it’s probably your pipeline.

Now, I could talk for hours about building an effective pipeline, but for the purposes of this article, I’m going to condense the information down to the essentials.

So here’s everything you need to know about pipelines.

Common Pipeline Mistakes

Most pipeline errors that cost you precious time and money are easily preventable, which is why you should take the time now to make sure your pipeline is seamless from start to finish.

Ironically, one of the most common pipeline mistakes is simply not spending enough time on your building it out initially.

Your pipeline is the lifeblood of your business. It’s what helps you turn leads into clients. So if it’s not optimal, your sales won’t be either.

Another mistake is not moving leads quickly enough.

The data shows that the sooner you nurture your leads, the better. Wait too long, and your leads will turn cold, which could cost you a sale.

Did you know that as much as 50% of sales go to the first vendor?

Every second matters when you get a new lead.

By baking automation into your pipeline, you can nurture a new lead immediately. The software will take care of that for you, and you’ll be one step closer to making a sale.

Likewise, it’s important to keep this engagement steady throughout your pipeline. Being present at every step will greatly increase your chances of closing the sale.

The best way to do this? Surprise––it’s CRM automation.

But no matter what CRM you’re using, don’t make these costly mistakes.

Organizing Your Pipeline

Now that I’ve talked about what not to do, I’ll tell you what you should do.

First, make sure you have your priorities right at each touchpoint.

To put it another way, your pipeline needs to be doing the right things at the right time.

For example, when you first get a lead, your top priority should be nurturing that lead. You don’t want to hit them over the head with a big sales pitch––you just want to increase brand awareness.

Also, remember that a pipeline is essentially a bunch of leads going through a sales funnel. Use that framework to create your process and automations.

Your CRM can help you create a cohesive pipeline that keeps leads moving through your funnel and ensures that the appropriate actions are taken when necessary.

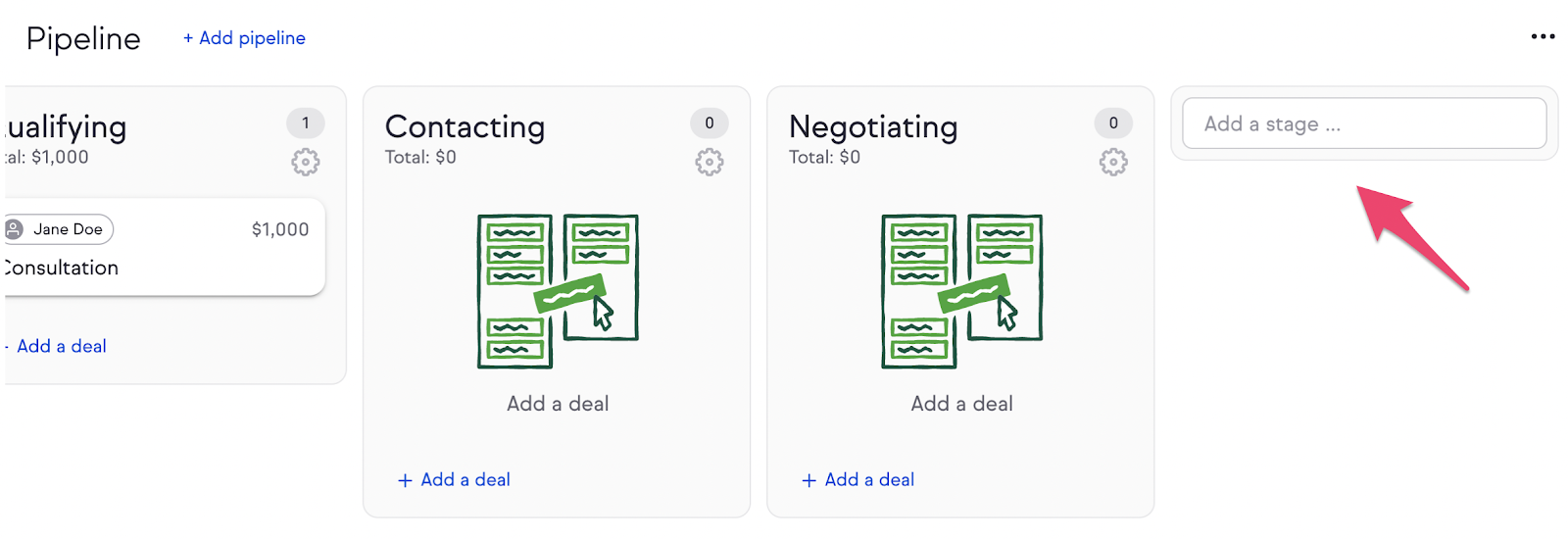

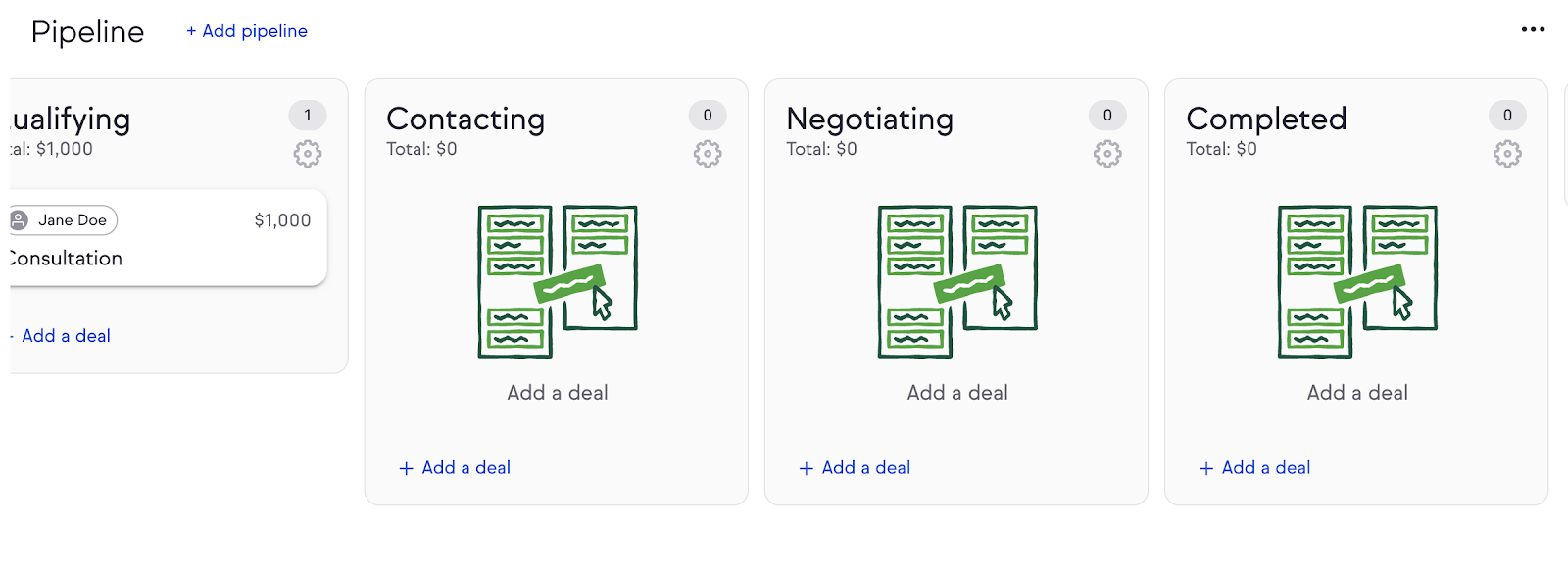

First of all, the four stock categories that Keap starts you out with (new, qualifying, contacting, negotiating) are great, but you can always add more if you need to.

Just scroll all the way to the right and click the “Add a stage” text field:

For instance, you could add a Completed stage for leads that you’ve successfully converted and are moving forward with.

The way you organize your pipeline might take some trial and error, as most companies have unique workflows.

However, I would recommend having at least three different stages so you can engage your lead at the beginning, middle, and end of your pipeline.

Next, the key is to use automation to make your pipeline as hands-off as possible.

Start by automating your email sequences as I showed above to help move your leads from stage to stage and keep them engaged. Again, these emails need to be personalized. There’s no point in using boilerplate templates that are stiff and boring. Take the time to make each email feel personal.

Next, add automation to your campaigns. This will ensure specific actions are taking within your CRM as leads move from stage to stage. These step-by-step tutorials on automation can help you get up and running.

Now, I won’t lie to you––this is going to take some trial and error. You aren’t going to have a perfect pipeline on day one.

So be sure to test your pipeline before you take it out in the real world.

Plug some fake clients and numbers into your CRM and use a few burner emails to test out your CRM’s capabilities. This will give you the chance to identify and remedy problems before you go live.

This extra step goes a long way. Sure, your pipeline still might have some errors once you start using it for actual clients, but you’ll have minimized the risk involved.

Conclusion

You’re almost at the finish line! It won’t be long until you’re putting your shiny new pipeline to good use.

But first, we have to put all the pieces together, so let’s recap what we’ve gone over.

1. The importance of a robust CRM. You want software that will allow you to manage all of your customers in one place, automate your business process, and track important metrics and interactions.

2. Putting processes in place. Having processes to depend upon is crucial for every business. Doing everything by the seat of your pants leads to inconsistency and often costs you.

3. Automation. If you can automate an internal process, you probably should. You can also automate a fair amount of client interactions without losing a human touch.

The final step is to synthesize all of these steps into one unified approach.

Remember, you’re doing all this to optimize your site for sales. You’re building a strong foundation that will support you as you scale.

After all, your site is the sum of its parts, so make those parts awesome.

Choose a CRM that meets your needs and that’s flexible so it will grow with you. Then create processes that will take the weight off your shoulders––and don’t be afraid to change these processes over time as your business evolves.

And there you have it — everything you need to start turning your site into an automation workhorse.

Before you know it, you’ll be seeing some of the amazing effects of automation and hopefully bringing in more sales than ever before.

Do you use a CRM that has helped turn your website into a sales machine?

Many business owners don’t realize that there is even a question of how to build good business credit? They think that business credit works similar to personal credit. Since business personal credit builds passively by simply with handling credit wisely, they think business credit does the same. That isn’t the case however. The answer to “How to build good business credit?”can be summed up in one word, intentionally. You must make it a point to build business credit. You have to make it happen.

How to Build Good Business Credit: Fill Your Cornucopia with Business Accounts

In traditional Thanksgiving Day pictures, you see the ever overflowing horn of plenty known as the cornucopia. There are breads, fruits, vegetables and nuts pouring out of the horn shaped basket. If you are a business owner, you need two cornucopias. One is for your business credit, and one is for your personal credit. While you want them both overflowing with healthy accounts, what happens with many is that the business credit one is empty or non-existent. They think it is there and full, while in reality all the accounts they think are hitting their business credit report are actually hitting their personal report.

Why Do you Need Two Cornucopias? Does Business Credit Even Matter?

If you’re wondering why it is important to know how to build good business credit, here is your answer. The business credit cornucopia can hold more. Let me explain. If you try to run a business with only what is in your personal credit cornucopia, you will not have enough. You will need more than what it can hold.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

Here is what that looks like in real life. Your personal credit cards are going to have lower limits than what business credit cards have. Business expenses are, by nature, a lot higher than personal expenses. Therefore, if you try to put business and personal expenses on the same credit cards, you are going to overrun your limits.

Even if you make your payments on time, or even pay off your balances each month, you are likely going to keep hovering near your limits. Not only does this reduce the funding you have available, but it can also have a negative impact on your personal credit score. Here’s how. The closer your balances are to your limit, the higher your debt-to-credit ratio is. A high debt-to-credit ratio has a negative impact on your credit score.

So, this means you need to ask how to build good business credit for two reasons. First, you may not have enough credit availability to run your business successfully without it. Second, if you do not build business credit, you could end up ruining your personal credit. Consequently, not only would your business success be in question, but you could lose the ability to do things like buy a house or a car.

Where Does that Second Cornucopia Come From?

Here is what most business owners do not understand. You have to intentionally go out and get that separate business cornucopia. If you don’t, then any business accounts you open will just go straight to your personal credit cornucopia and wreak the havoc mentioned above. So, how do you do that? How do you establish business credit in the first place so that business accounts report to that, and not to your personal credit? The key is to make your business appear to lenders as a fundable entity, separate from yourself as the owner.

How to Build Good Business Credit: Establishing Fundability

The first thing you need to know is, it is easiest to do this as you are establishing your business. If you are a new business owner just getting started, then set your business up this way on the front end so that you can begin building business credit now. If, however, you are already up and running, it isn’t too late. You may have to do some backtracking, but it will be so worth it. Either way, this is what has to be done. This is the first part of the answer to the question of how to build business credit.

Separate Name and Contact Information

This is an essential first step to weaving a separate business credit cornucopia. Of course, most businesses do not have the exact same name as their owners. The key is, you have to list the business in the business directories under that business name. In addition, it needs to be listed with its own address and phone number.

A question often asked about this is, how do you get a separate business phone number and address if you run your business out of your home or online. Actually, there are several options now for a business telephone number that do not even require you to have a second phone. You can just have your business number forwarded to your personal line.

As for an address, there are a number of virtual office companies that offer a physical mailing address to businesses for just this purpose. Typically, they also offer a number of other useful services such as meeting spaces and live receptionist services.

Get and EIN

When you apply for credit, they always ask for you Social Security Number, or SSN. If you are applying for credit in your business name, you shouldn’t use your SSN. If you do, that account will automatically relate to your personal credit. The way around this is to get your business an EIN. They are free on the IRS website. You may still need to use your SSN for identification purposes when applying for credit under new fraud regulations, but that needs to be the only reason you use it.

You Must Incorporate

This isn’t an option. While it is much easier and cheaper to operate as a sole proprietorship or partnership, you cannot get the separation needed if you do not formally incorporate. Whether you choose an S-corp, LLC, or corporations will depend on your other needs and budget. Any of them will work for establishing fundability. Still, you must choose one.

Get a Business Bank Account

When building fundability, you need to have a separate business bank account. This serves a number of purposes. First, separate from building fundability, this helps you keep your business and personal expenses separate. That will be a tremendous help come tax time.

Secondly, some business credit cards want to see a business bank account with a minimum average balance before they will approve credit. Lastly, it helps lend credibility to the fact that your business is a fundable entity on its own, apart from the owner.

Professional Website and Dedicated Email

In today’s business world, if you do not have an online presence you do not exist. Having a poorly executed online presence is just as bad. You need a professionally built, working website. Pay for design and hosting. The free services are not going to be good enough to help you out here. In addition, you need a dedicated business email address with the same URL as your website. Free email platforms such as Yahoo and Gmail do not look professional.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

Get a D-U-N-S Number

There are several business credit reporting agencies, or CRAs. The 3 most commonly used are Dun & Bradstreet, Experian, and Equifax. Of those three, Dun & Bradstreet is definitely the largest and most commonly used. Before you can have a credit profile with them, you must have a D-U-N-S number. This is how they identify your business.

If you do not have a D-U-N-S number, you will not have a credit profile with Dun & Bradstreet, so you definitely need the number. That’s all you need though. They will try to upsell you on other services, but stay strong and resist. You just need the number, and it’s free.

How to Build Good Business Credit: Fill the Cornucopia

Once you have your separate business credit cornucopia, it’s time to fill it with lots of yummy accounts to build your business credit big and strong. That, again, takes intentionality. You cannot just go out and start applying for credit in your business name. It won’t happen. Just as those that celebrated the first Thanksgiving Day had to actively work to provide the food for the feast, so you will have to actively build business credit. To do this, you have to work through the business credit tiers.

Starting at the bottom tier, you build enough accounts and business credit to move up to the next tier, until you reach the top. Here is a little more about each tier and what it takes to move on to the next.

How to Build Good Business Credit Using The Vendor Credit Tier

This is the first tier on your journey to fill your business credit report with accounts. It consists of starter vendors. These are vendors that will offer your business net terms on invoices without first checking your credit. Then, when you pay, they will report those payments to the CRAs. This is the second part of the answer to how to build good business credit. In this way, you can begin to build credit without having credit.

They will look at other information however. Some like to see a certain amount of time in business. Some will want you to place an initial order, or more than one, before they will extend net terms. Others will want to see a business bank account with a minimum balance. Another thing they sometimes look at is a listing in the business directories. Starter vendors may require any combinations of these things. Find out more about some of the most common starter vendors here.

How to Build Good Business Credit With The Retail Credit Tier

After you have 8 or 10 accounts from the vendor credit tier reporting positive payment information to the CRAs, you can apply for credit in the retail credit tier. These are those cards that you can only use at the specific retail store that issues them. For example, Office Depot cards that you can only use at office depot are in this tier..

How to Build Good Business Credit: Continuing to The Fleet Credit Tier

After you have enough accounts reporting from the retail credit tier, you can apply for cards in the fleet credit tier. These are cards that you can only use for fuel costs and automobile repair and maintenance. Fuelman and Shell are examples of companies that issue cards in this tier.

How to Build Good Business Credit: Finishing with The Cash Credit Tier

This is the top credit tier. It’s the goal. Once you have enough accounts reporting from the fleet credit tier you can apply for cards in this tier. It consists of the standard Mastercard, Visa, Discover, and American Express cards that are not limited to a specific store or type of expense.

How to Build Good Business Credit: Don’t Let Things Start Falling Out

Even though the overflowing cornucopia makes for a pretty Thanksgiving Day picture, you don’t really want the same effect with your business credit. If you do not handle the credit you have properly, you’ll start losing control. Be sure to pay accounts on-time. Remember, don’t buy things you cannot afford just to build business credit. You will end up with the opposite of what you want. Also, be sure you keep an eye on things. You wouldn’t want a bug eating up all that good food in your horn of plenty right?

Monitor your business credit regularly to ensure there are no mistakes and that everything is up to date. We can help you with that here.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

How to Build Good Business Credit: May Your Cornucopia Be Full

I think it’s clear at this point. It takes more than just paying your bills on time to build business credit. Unlike your personal credit score, your business credit score does not appear passively. You have to work to intentionally build it. It isn’t a hard process, but it is a process. You have to trust the process and act responsibly. Now that you know how to build good business credit, it’s time to get started.

Many business owners don’t realize that there is even a question of how to build good business credit? They think that business credit works similar to personal credit. Since business personal credit builds passively by simply with handling credit wisely, they think business credit does the same. That isn’t the case however. The answer to … Continue reading This Thanksgiving Day, Turn Things Around by Learning How to Build Good Business Credit

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

You can even finance a vehicle purchase or lease through our Business Credit Builder. These offers are in Tier 4. So they have certain requirements that business credit neophytes won’t be able to meet. Lenders will want to see you have the income to support the purchase. Consider Ford Commercial Vehicle Financing.

You can even finance a vehicle purchase or lease through our Business Credit Builder. These offers are in Tier 4. So they have certain requirements that business credit neophytes won’t be able to meet. Lenders will want to see you have the income to support the purchase. Consider Ford Commercial Vehicle Financing.