gptengineer.app / Lovable | ONSITE+HYBRID | Stockholm / London | Full-Time | Founding Engineers, Founding Designer

Lovable is made up of a team of pragmatic previous (YC) founders and CTOs, set on being the first to make autonomous code generation work.

This is a hard problem. We believe we can do it by selecting a limited domain, a great AI driven UX and crucially – carefully selecting a single ‘AI-first’ tech stack of open-source, that us engineers love to maintain. That we optimise the system of fine-tuned LLMs (+LMMs) to do well in.

We believe that rapid experimentation and hiring the brightest and most ambitious minds is the way we make this work. You’d be one of the first employees and have a big impact in shaping our product and company!

In particular we’re looking for a Founding Engineer to join our team of AI and product engineers building the software that builds other software.

Qdrant | Software Engineers (Rust), DevRel’s, DevOps, VP Growth | Berlin, Germany / Remote | Full-time | https://angel.co/company/qdrant Qdrant (https://qdrant.tech) is an open-source vector search database. With Qdrant, embeddings or neural network encoders can be turned into full-fledged applications for matching, searching, recommending, and much more. We are looking especially for DevOps engineers to build … Continue reading New comment by andre-z in "Ask HN: Who is hiring? (February 2023)"

Nonetheless, no matter what platform you look at, it’s safe to say that the advertising industry is seeing a slowdown.

Now let’s dive into the obvious bad news, and then we will get into the silver lining and how you should adapt. Because there is hope and you can still do well in this market.

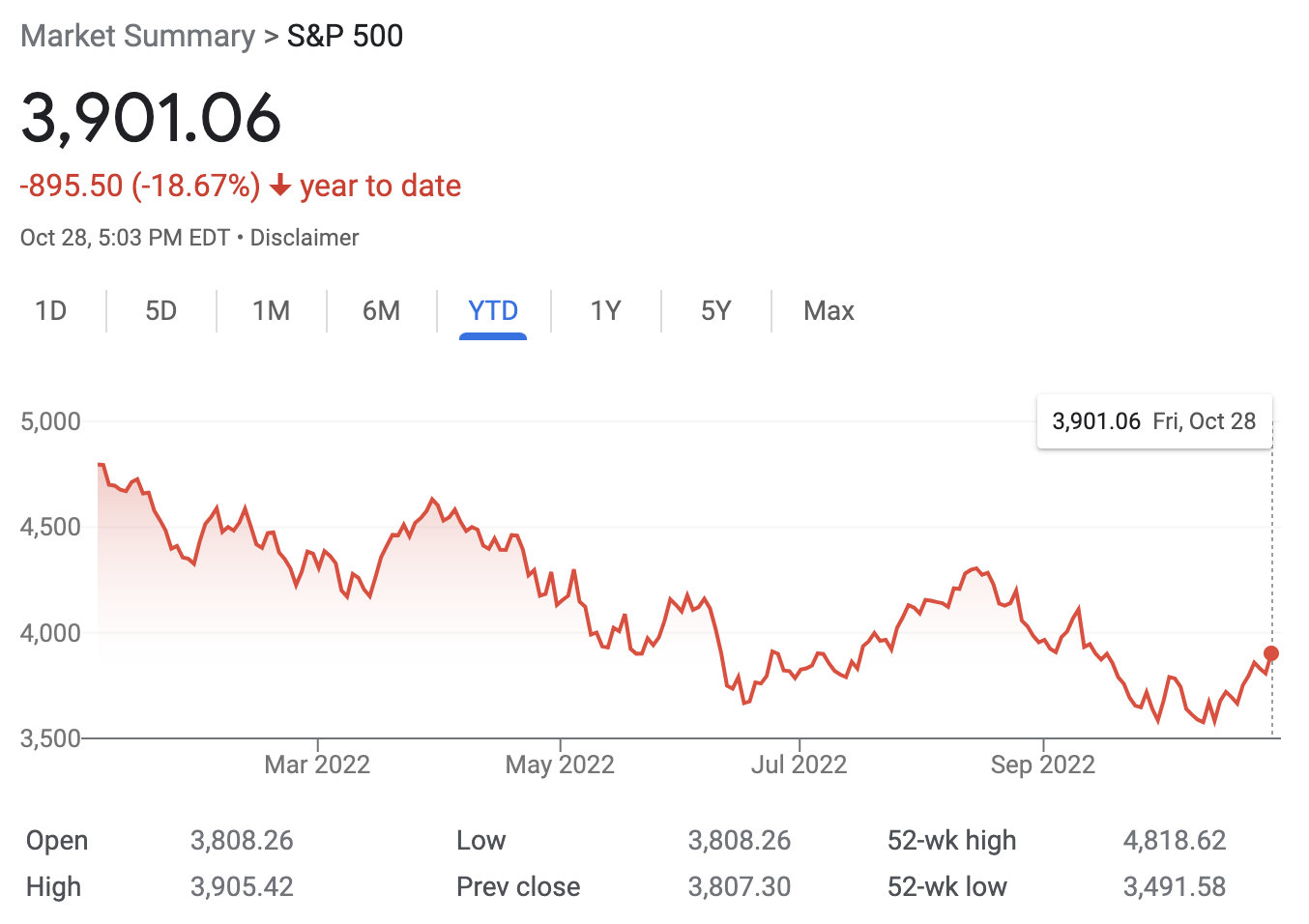

And when you have the S&P 500 down 18.67% it means companies have lost a lot of money… and I mean a lot.

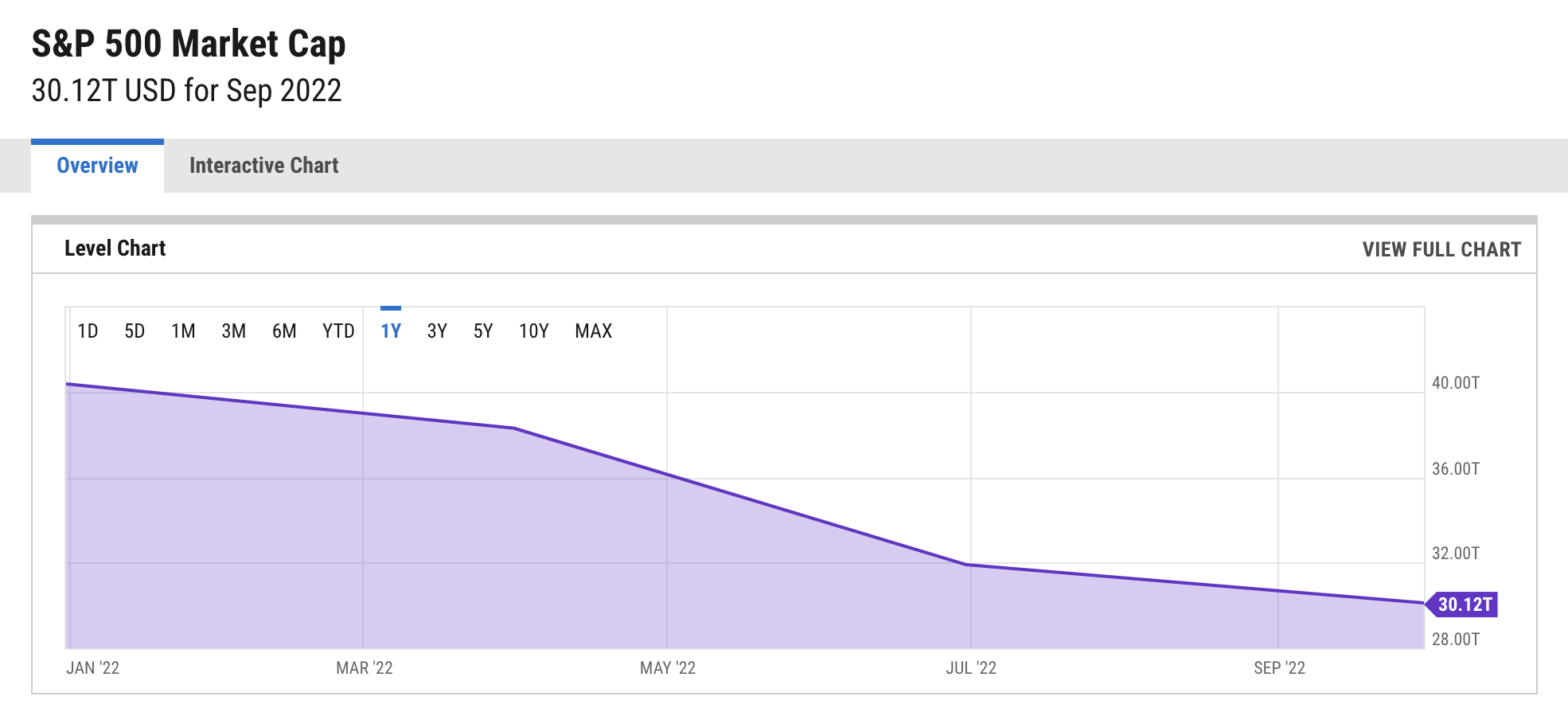

Just think of it this way, the companies in the S&P 500 have a market capitalization of 30.12 trillion dollars.

In December of 2021, the S&P 500 had a market capitalization of 40.36 trillion dollars. That’s roughly a 10 trillion dollar loss.

To put it in perspective, if Apple, Amazon, Google, Facebook, and Microsoft didn’t exist that would only be 6.8 trillion dollars (based on today’s stock price).

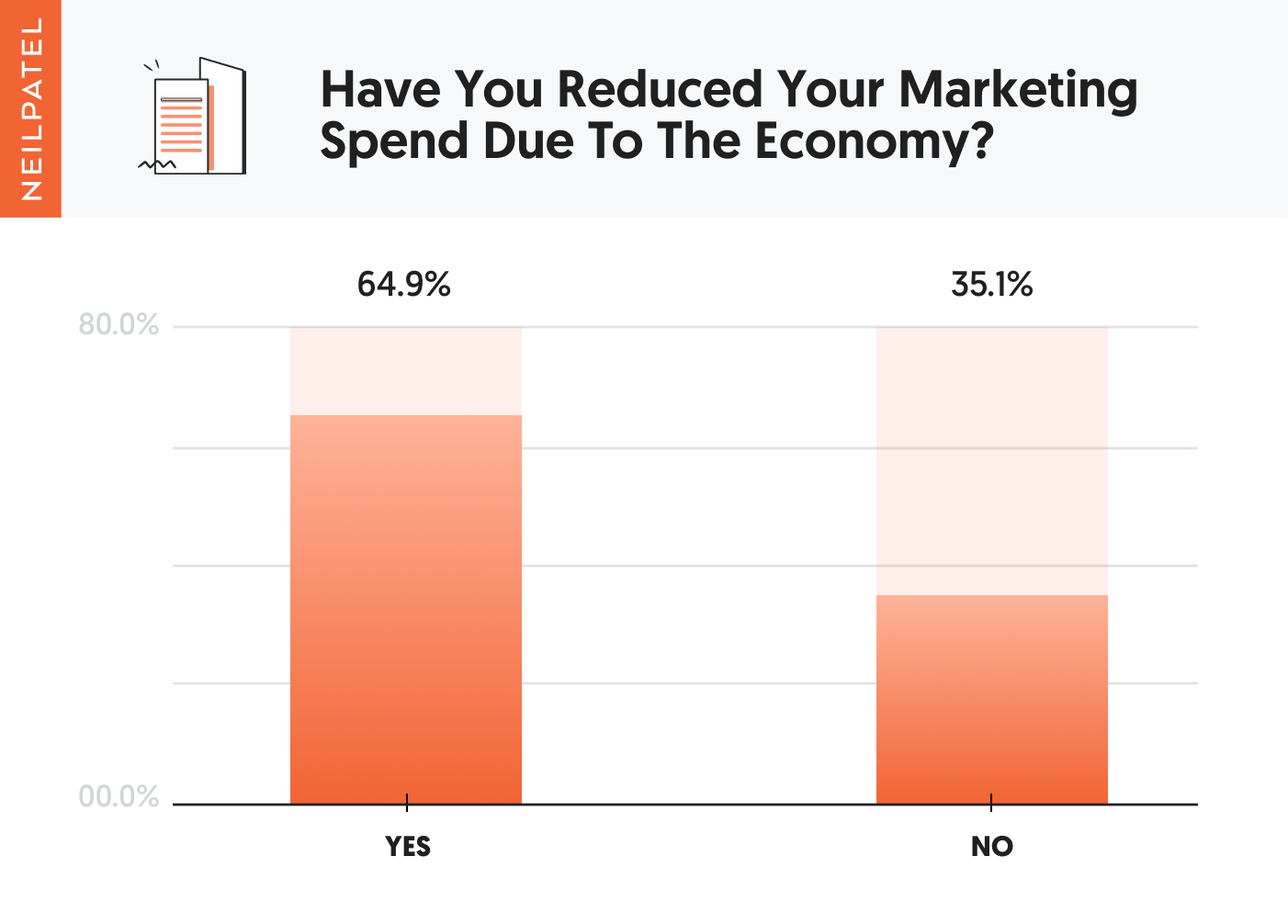

When the market goes down, the value of which companies are worth goes down, which means companies cut back on spending. Marketing happens to be the first thing that gets cut in a bad economy.

And when the value of companies goes down, a lot of people’s net worth goes down. Just in America alone, 43% of the population owns stocks.

So, when people’s net worth goes down, eventually they start spending less. It’s already started to slow too… when you look at data from the first half of this year (inflation-adjusted) spending increased by 1.5% compared to 12% last year.

But what about marketing?

Here’s what’s interesting…

Because our agency, NP Digital, works with companies of all sizes we see data from both small and medium businesses as well as enterprises.

Plus we have offices and employees throughout the world such as in Canada, Brazil, Germany, India, Australia, etc… because we work with companies in multiple regions and help them with their global and local marketing campaigns.

That in combination with working closely with some of the big advertising platforms and having tools like Ubersuggest that tracks millions of domains we really see a lot of data and trends.

Here are the 3 main trends we are seeing (keep in mind the data below is from what we can see and track, as we don’t have data on the whole web or even a large fraction of it):

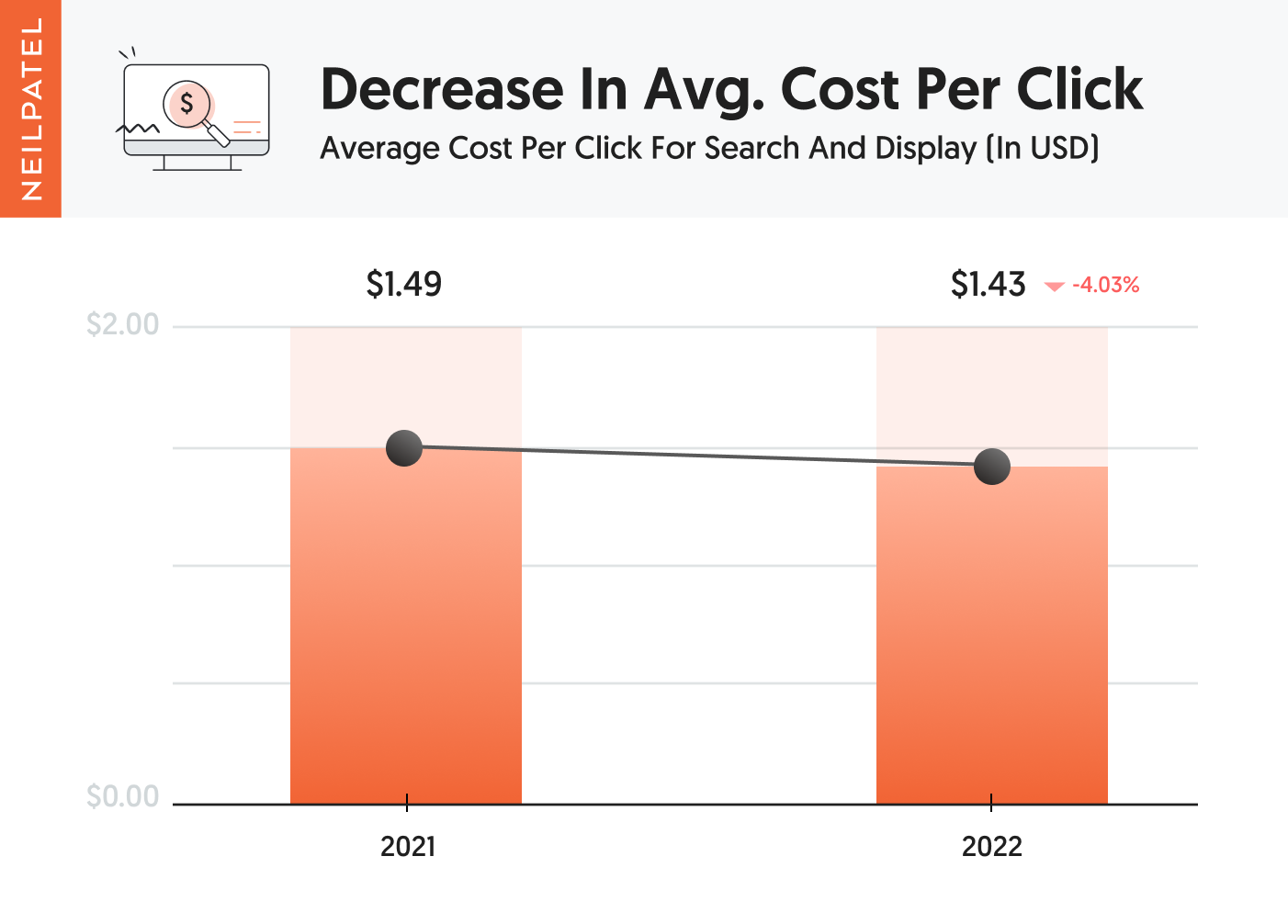

Trend #1: Ad costs are decreasing

Overall, the global costs for ads have been going down by 4%. Some industries like real estate have gone down much more, but with other industries like B2B SaaS, we haven’t seen much of a change with our clients as they optimize for lifetime value.

A lot of this is because businesses are cutting back on their spending in addition to many sectors such as real estate not having the same demand that they had a year ago.

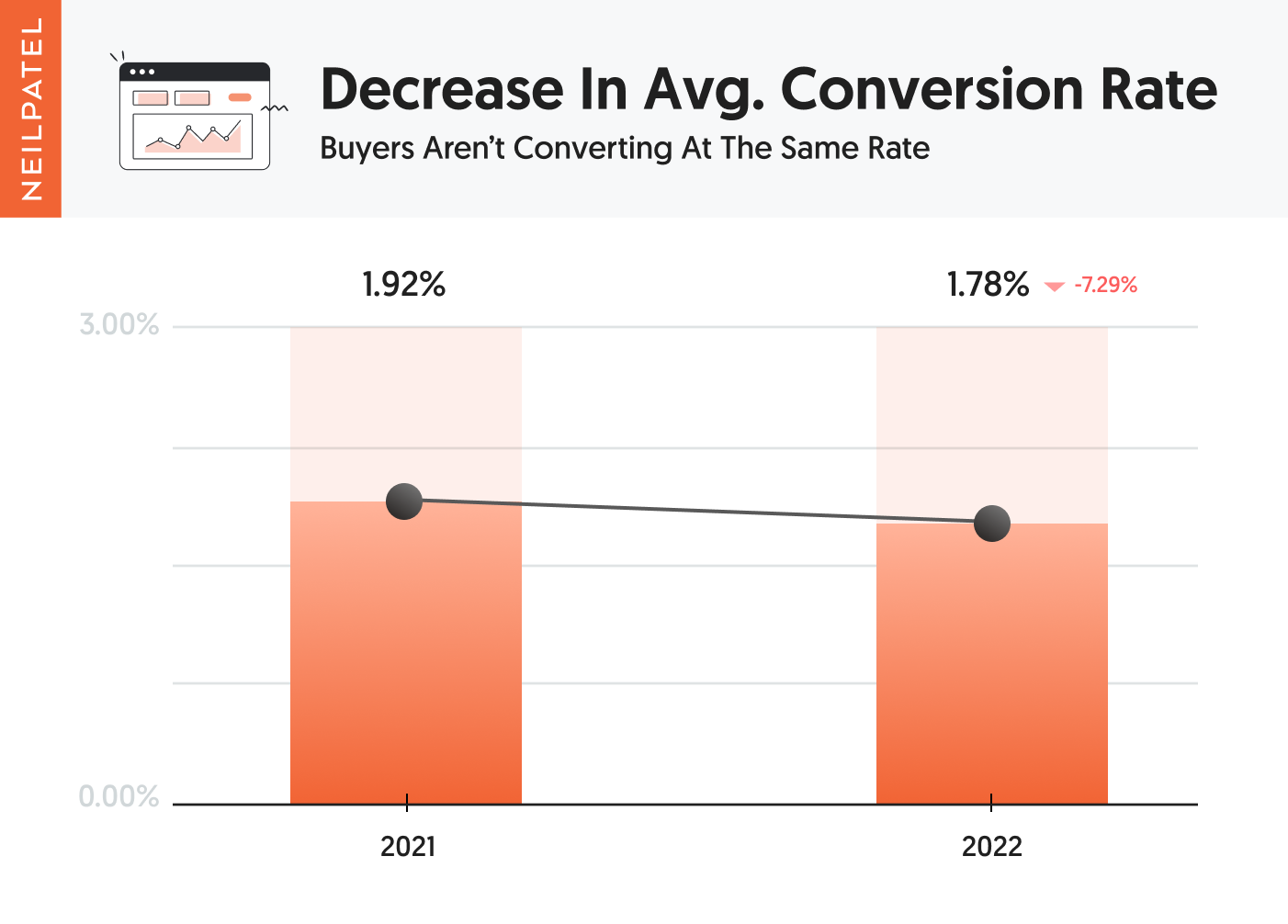

Trend #2: Buyers aren’t converting at the same rate

We aren’t seeing conversion rates as high as they used to be. We’ve seen a drop of 7.13%.

Keep in mind that different websites have different conversion goals. Such as one website may focus on leads while another may focus on a signup or another may focus on a purchase.

Conversion rates are also affected by many other factors such as companies increasing prices due to inflation costs, shipping costs, and supply chain delays.

Or conversion rates being lower because some people aren’t spending as much because they may have lost their job.

Trend #3: Companies are fearful of the unknown

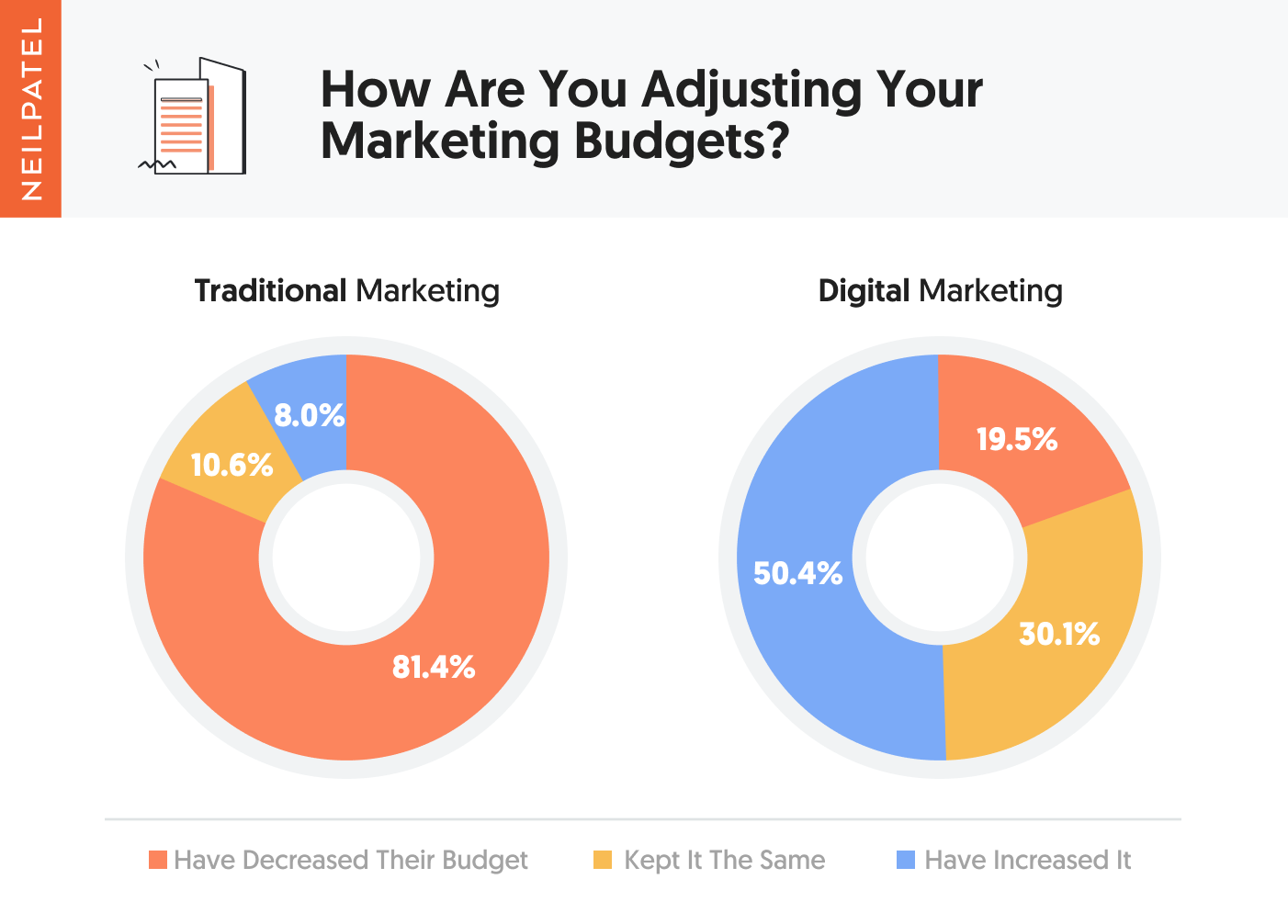

We are seeing some companies pulling back on their total marketing budget because they are afraid of what lies ahead.

But we are also seeing companies shift their budget to digital marketing because it is easier to track than let’s say traditional TV or radio advertising.

Now we don’t manage traditional budgets for our clients, but we handle the digital side. In a good or a bad economy, companies tend to spend on digital marketing (things like SEO, paid ads, email marketing, social media, etc) as long as it is profitable.

The silver lining in marketing

As I mentioned earlier, we see a lot of data.

There’s a pattern that we have seen with the companies that have been growing this year (the ones we work with at least).

And to be clear, when I say growing, I mean companies that are generating more revenue and profit.

These companies are also taking advantage of the current economic climate to double down on their whole business, not just marketing, to gain more market share.

So, what are these growing companies doing in this economy?

Conversion optimization – 83% of them have doubled down on conversion rate optimization. If you can get more of your visitors to convert into customers through copy, images, or products you can generate more sales. A great example of this is Legion which will grow around 40% this year mainly due to conversion rate optimization, while a lot of their D2C competitors are flat or declining.

Influencer marketing – 49% have either doubled down on their influencer marketing budgets or started influencer marketing. Rates for influencer marketing have gone down. They can convert well too if you focus on micro-influencers that have your target audience. They tend to be both cheaper and generate more revenue. You just need thousands of them to really build scale (not hundreds).

SEO – SEO is a long-term play, but it provides a massive ROI. Only 2% of the companies we work with that have grown this year have slowed down on their SEO efforts. 98% of them continued their current budgets or increased them when it comes to SEO.

Global expansion – an easy way to generate more revenue is to add new regions to sell your products and services in. 19% of the winning companies we work with have expanded into new regions. This creates more revenue generation opportunities, and you’ll find that marketing is much cheaper in most regions compared to the U.S. or U.K. Sure you won’t generate as much revenue, but the ROI tends to be higher from what we are seeing.

Email marketing – it’s rare that we work with a company that isn’t collecting emails or already doing email marketing. But what’s funny is companies assume that if you just send out promotional emails every once in a while, or a few educational ones… that’s considered email marketing. Sadly there is much more to it. For example, segmenting your lists and sending different campaigns to different people. Or optimizing your open and click rates. 77% of the companies we work with that grew this year doubled down on email marketing and fine-tuned their campaigns.

Omnichannel marketing – there is multi-channel marketing and there is omnichannel marketing. 100% of the companies we worked with that grew focused on omnichannel marketing and continually expanded. What I mean by this is when a company uses omnichannel marketing, the channels work together and they are also using learnings from each channel to maximize others. Versus multi-channel marketing where each channel just sits in a silo. TikTok has been massive for ecommerce… and channels like Snap, Pinterest, Reddit, Bing or even Quora that people don’t really talk about have been effective too.

Conclusion

Just because the economy isn’t where you want it to be, it doesn’t mean you can’t grow.

And if you really have headwinds ahead of you such as the mortgage industry, you can still make a lot of changes that will put the company in a much better place when the economy starts to recover.

In other words, start thinking outside the box. Don’t focus all of your energy on the news… sure it’s smart for you to stay up to date with what is happening, but the majority of your time should be spent on solutions and new ways to grow.

Lenders pull business credit reports and scores from a business credit bureau. However, not every business has a business credit report at all, let alone a credit score. Business credit, in stark contrast to consumer credit, does not start building automatically.

Avoid These Mistakes When It comes to Your Business Credit Profile

With consumer credit, as soon as you use your first credit card you have a credit report. If you continue to use credit responsibly, that report will include a strong credit score. The same is not true of business credit, and that leads us to mistake number one.

#1: Assuming You Are Automatically Set Up With the Business Credit Bureau

Just owning a business does not ensure you have a business credit profile. There are some things you have to be intentional about to ensure this happens. The first step is setting up your business with a Fundable foundation to ensure that it is recognized as a separate entity from you as the owner. This has to be done before you can even get credit in the name of your business.

Then, a business credit profile can be established with the bureaus.

How Do You Set Up a Business to Be Fundable?

In addition to a D-U-N-S number, you need to be sure your business has:

Separate contact information

An EIN

A dedicated business bank account

A professional website

And its own email address

This list is not exclusive, but it is a great start. Additionally, you’ll need to be incorporated. Operating as a sole proprietorship or partnership does not help you get set up with any business credit bureau.

Why Does a Fundable Setup Matter?

If your business is not set up to be Fundable, the information on the credit report may not be accurate. Furthermore, if your business is not set up to be a separate entity from you the owner, payment experiences may not go to business credit bureaus at all.

#2: Assuming There Is Only One Business Credit Bureau

There are many business credit bureaus. The three main ones are Dun & Bradstreet, Experian, and Equifax. Among the others, FICO SBSS is gaining popularity. Not all of them function the same way when it comes to setting up a profile with them either. It’s different for each one.

Many of them don’t really require anything from you. But, you still have to have your business set up properly. Then, when your creditors report payments, they are reflected accurately.

Dun & Bradstreet

D&B is the oldest and largest credit reporting agency. Go to D&B’s website and look for your business. Don’t see it? It’s probably because you do not yet have a D-U-N-S number. You MUST apply for a D-U-N-S number from them. If you do not have one and your creditors report payments, your business will not be recognized in the D&B system regardless of how your business is set up. This number is how D&B gets your company into their system. You can get one for free.

Once you have a D-U-N-S number, you’ll need at least 3 payment experiences before they assign a PAYDEX score. A payment experience is just a reported purchase from a business, which reports to a credit reporting agency.

Experian

Experian will assign your business an identification number called a BIN after you have a payment experience reported to them. Just be sure your business is set up to be Fundable. Then when you have business creditors that report to them, your business will be in the system.

Equifax

Equifax assigns companies an Equifax ID. It doesn’t appear that you will need to sign up for or request one.

#3: Assuming You Already Have a Business Credit Profile With a Business Credit Bureau at All

Suppose you have been in business for a while. Maybe you are just now figuring out what business credit is. Maybe you thought you had credit in the name of your business, when actually what you have is business funding that you got based on your personal credit.

Where do you start if this is the case?First, look for your business credit profile from each of the main credit reporting agencies, starting with D&B. Of course, if you do not have a D-U-N-S number you will not be in their system.It is POSSIBLE that you may be in the Experian or Equifax system. but you’ll want to check your information closely and request corrections to any mistakes.

Business Credit Monitoring

The next question is, how do you do this? You can go through the business credit bureaus directly, but it can be costly. Credit Suite offers business credit monitoring with all three of the most commonly used business credit reporting agencies, for a fraction of the cost.

Once you see your reports, or lack thereof, you can be proactive in either correcting errors or establishing initial reports. What sort of errors are you looking for? In addition to payment experiences being reported incorrectly, you need to look at your actual business information.

Make sure your business contact information is up-to-date and accurate. If you already have an EIN, ensure that it is attached to your business and is correct. One big issue a lot of small business owners run into is inconsistency in the name of the business.

Something as small as using an ampersand in one place and the word “and” in other places can cause big problems. Ensuring your business name is correct and consistent everywhere, including on your business credit reports, is crucial also.

#4: Ignoring FICO SBSS as a Business Credit Bureau

This score is becoming increasingly common. It stands for FICO Liquid Credit Small Business Scoring Service. Unlike your personal FICO, the SBSS reports on a scale of 0 to 300. The higher the score the better. In general, most lenders demand a score of at least 160.

The thing is, you don’t really “set up” your business with FICO SBSS. The scoring model for this score is very different from other business credit scoring models. However, that does not mean you are helpless.

How Does FICO SBSS Calculate Business Credit Score ?

The score itself isn’t readily accessible. The formula for calculations is proprietary, and they guard it well. The information is not public. Of course, this means you can go into a lender totally blind as to what your FICO SBSS credit score may be.

With other credit reports from business credit reporting agencies, you can actually get a copy of your credit report and know where you stand. In contrast, the FICO SBSS can be different from lender to lender.

How Does a Lender Get Your FICO SBSS Score?

After you fill out a loan application and turn it in with all necessary documents, the lender processes this information and sends it to FICO with a request for your SBSS score. At this time, the lender can ask for certain factors in the score to carry more weight than others. Your score can vary depending on how a lender weighs each factor .

A score variation can happen if a lender puts more weight on your personal credit score or your business credit. Similarly, they could choose to weigh annual revenue as more important than payment history. It is their choice.

FICO then searches business credit information from business credit agencies including D&B, Experian, and Equifax. As a result, your score with these bureaus affects your FICO SBSS.

What Can You Do?

Even though there is no real way to set up your business with FICO SBSS, you can definitely work to affect the score. Establish your business with the other business credit bureaus. Keep your personal and business credit in good order. Then, if a lender chooses to use that score, regardless of how much weight they put on each factor, you should be good.

You Must Be Intentional When it Comes to Your Profile with Any Business Credit Bureau

You aren’t powerless. The great thing about business credit is that it does not just carry you off before you know what is happening. In contrast, you have to intentionally jump in. The first step is to set you business up to be Fundable. Then, get a D-U-N-S number. After that, find accounts that report and get started building your business credit score. Check out our business credit builder for a step-by-step guide to building the strongest business credit score possible for your business.

My name’s Fred Wu, I’m an experienced Elixir and Ruby developer who has worked on multiple commercial projects as well as having released multiple open source Hex packages and Rubygems.

I work at a fintech startup as CTO, leading a small team. During Covid I’ve been pumping out around 40 extra hours per week on freelancing work. My day job involves mostly the non-coding part of problem solving so it’s a nice mix of pace for me to keep my coding skills sharp during the evenings and on weekends.

I’ve been using Elixir for half a decade, ruby for over a decade, lead and built multiple commercial B2B & B2C SaaS projects. I’ve always been very hands on, and have worked with multiple tech stacks in the past, including JS/React, PHP, Golang, and most recently Clojure at the startup I’m currently working at.

– And a few years ago when I was heavily involved in the ruby/rails community, I had done an experimental project building a “layer 0” ORM on top of ActiveRecord and Sequel: https://github.com/fredwu/datamappify

If you think my skills and experience could add value to the project I’d love to chat more. You could reach me at ifredwu at gmail dot com. Thanks!

GDPR Cookie Consent Agreement

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.