If solving complex HCI problems excites you and you’ve read the case study on how TurboTax used UX + UI to make doing taxes fun, this is the job for you.

You will join a small and self-sufficient team to build a yet-to-be-announced product from the ground up. This team will be you (owning UI + UX), a PM, developers, QAs, and product marketers. You and your teammates will build, measure, and learn together.

At TrueVault, we want to make data privacy as simple as possible for businesses, so they have no excuses not to be a good corporate citizen. If data privacy is important to you, you will find many like-minded people here at TrueVault.

Our ideal candidate: – Really understands how to, and has a passion for, turning a long and dreary process (like filing a tax return) into small consumable steps for “average Joe” business users – Understands that UX and UI are two different disciplines and is proficient in both

Other facts about this position: – This is a remote position (we’ve been 100% remote since 2017) – You can work from anywhere in the world but your work hours have to overlap Pacific Standard Time (California) at least 6 hours a day – This is a full-time contract position

To apply, email the following to jobs@truevault.com: – Link to or PDF of your work portfolio = A short (1-2 sentence) reason why you are interested in this job

TrueVault is an Equal Opportunity Employer. We are committed to providing an inclusive work environment free of discrimination and harassment for everyone, regardless of race, color, religion, national or ethnic origin, sex, age, sexual orientation, gender identity, disability, sexual orientation, marital status, military service or other non-merit factors.

If solving complex HCI problems excites you and you’ve read the case study on how TurboTax used UX + UI to make doing taxes fun, this is the job for you.

You will join a small and self-sufficient team to build a yet-to-be-announced product from the ground up. This team will be you (owning UI + UX), a PM, developers, QAs, and product marketers. You and your teammates will build, measure, and learn together.

At TrueVault, we want to make data privacy as simple as possible for businesses, so they have no excuses not to be a good corporate citizen. If data privacy is important to you, you will find many like-minded people here at TrueVault.

Our ideal candidate:

– Really understands how to, and has a passion for, turning a long and dreary process (like filing a tax return) into small consumable steps for “average Joe” business users

– Understands that UX and UI are two different disciplines and is proficient in both

Other facts about this position:

– This is a remote position (we’ve been 100% remote since 2017)

– You can work from anywhere in the world but your work hours have to overlap Pacific Standard Time (California) at least 6 hours a day

– This is a full-time contract position

To apply, email the following to jobs@truevault.com:

– Link to or PDF of your work portfolio

= A short (1-2 sentence) reason why you are interested in this job

TrueVault is an Equal Opportunity Employer. We are committed to providing an inclusive work environment free of discrimination and harassment for everyone, regardless of race, color, religion, national or ethnic origin, sex, age, sexual orientation, gender identity, disability, sexual orientation, marital status, military service or other non-merit factors.

I am a 4th year undergraduate student of bachelor’s in Indian Institute of Information Technology, Allahabad, India graduating in May 2021. I have previously worked at Gojek as a Product Engineering Intern, where I worked on building dev analytics dashboard to help 100+ developers across different teams within Gojek to identify and improve bottlenecks. I like building things and currently working on building https://featuremonkey.com – a user feedback management portal.

Brave | Software Engineer (Ruby on Rails) | REMOTE US/Canada | Full-time | brave.com

Brave is looking for an experienced Software Engineer to work on Ruby on Rails publisher app. This is a high profile and impactful, hands-on position in an early stage startup. We’re primarily looking for someone with strong front-end skills.

Requirements

2+ years experience with Ruby on Rails experience. Working experience with JavaScript Enthusiasm and familiarity with blockchain Experience with software development via distributed development teams Comfortable working in an open source setting A passion for helping protect users’ privacy and security Written and verbal communication skills in fluent English Proven record of getting things done

Do you need business funding for bad credit? You may feel that – or you may have heard – that you can’t get business funding for bad credit. The best, easiest, and fastest way to do so is to build business credit. Because then your bad credit won’t matter quite so much. Any Small Business … Continue reading Is it Possible to Get Business Funding for Bad Credit?

Numerous Streams Income Online The crucial to making several streams of easy revenue online is to expand your product or services an individual must not have just one resource of easy earnings online however increase resources. Electronic books, associate advertising, audioproducts and also marketing are means to develop an easy revenue from the Internet. A …

Do you need business funding for bad credit? You may feel that – or you may have heard – that you can’t get business funding for bad credit.

The best, easiest, and fastest way to do so is to build business credit. Because then your bad credit won’t matter quite so much.

Any Small Business Can Get Business Funding for Bad Credit

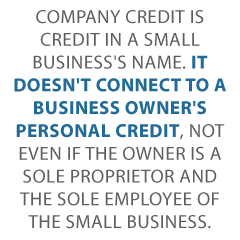

Company credit is credit in a small business’s name. It doesn’t connect to a business owner’s personal credit, not even if the owner is a sole proprietor and the sole employee of the small business.

Consequently, an entrepreneur’s business and consumer credit scores can be quite different.

The Advantages of Business Funding for Bad Credit

Considering that business credit is separate from consumer, it helps to secure a business owner’s personal assets, in case of court action or business bankruptcy.

Also, with two distinct credit scores, an entrepreneur can get two separate cards from the same merchant. This effectively doubles purchasing power.

Another advantage is that even startup businesses can do this. Going to a bank for a business loan can be a formula for disappointment. But building business credit, when done the right way, is a plan for success

Consumer credit scores depend on payments but also various other components like credit use percentages.

But for business credit, the scores really merely depend on if a small business pays its bills on a timely basis.

The Process

Establishing company credit is a process. It does not occur automatically. A company must actively work to build business credit.

Having said that, it can be done readily and quickly, and it is much swifter than developing personal credit scores.

Merchants are a big part of this process.

Accomplishing the steps out of order results in repetitive denials. No one can start at the top with business credit. For example, you can’t start with retail or cash credit from your bank. If you do, you’ll get a rejection 100% of the time.

Business Fundability

A small business must be fundable to loan providers and vendors.

Therefore, a business needs a professional-looking website and email address. And it needs to have website hosting bought from a vendor like GoDaddy.

In addition, business phone numbers need to have a listing on 411. You can do that here: http://www.listyourself.net.

In addition, the company phone number should be toll-free (800 exchange or the like).

A small business also needs a bank account devoted only to it, and it has to have all of the licenses necessary for running.

Licenses

These licenses all have to be in the identical, correct name of the small business. And they must have the same business address and telephone numbers.

So note, that this means not just state licenses, but possibly also city licenses.

Visit the Internal Revenue Service web site and get an EIN for the company. They’re free. Pick a business entity such as corporation, LLC, etc.

A business may get started as a sole proprietor. But they absolutely need to switch to a sort of corporation or an LLC.

This is to lessen risk. And it will maximize tax benefits.

A business entity matters when it involves tax obligations and liability in case of a lawsuit. A sole proprietorship means the owner is it when it comes to liability and tax obligations. Nobody else is responsible.

The best thing to do is to incorporate. You should only look at a DBA as an interim step on the way to incorporation.

Kicking Off the Business Credit Reporting Process

Begin at the D&B web site and get a cost-free D-U-N-S number. A D-U-N-S number is how D&B gets a company in their system, to produce a PAYDEX score. If there is no D-U-N-S number, then there is no record and no PAYDEX score.

Once in D&B’s system, search Equifax and Experian’s websites for the company. You can do this at www.creditsuite.com/reports. If there is a record with them, check it for accuracy and completeness. If there are no records with them, go to the next step in the process.

By doing this, Experian and Equifax have activity to report on.

Starter Vendor Credit

First you ought to establish tradelines that report. Then you’ll have an established credit profile, and you’ll get a business credit score.

And with an established business credit profile and score you can begin to get credit for numerous purposes, and from all sorts of places.

These sorts of accounts often tend to be for things bought all the time, like marketing materials, shipping boxes, outdoor work wear, ink and toner, and office furniture.

But first off, what is trade credit? These trade lines are credit issuers who give you starter credit when you have none now. Terms are in most cases Net 30, rather than revolving.

Therefore, if you get approval for $1,000 in vendor credit and use all of it, you need to pay that money back in a set term, such as within 30 days on a Net 30 account.

Details

Net 30 accounts must be paid in full within 30 days. 60 accounts must be paid fully within 60 days. Unlike revolving accounts, you have a set time when you have to pay back what you borrowed or the credit you made use of.

To start your business credit profile the proper way, you ought to get approval for vendor accounts that report to the business credit reporting bureaus. As soon as that’s done, you can then make use of the credit.

Then pay back what you used, and the account is on report to Dun & Bradstreet, Experian, or Equifax.

Vendor Credit – It Makes Sense

Not every vendor can help in the same way true starter credit can. These are merchants that grant approval with minimal effort. You also want them to be reporting to one or more of the big three CRAs: Dun & Bradstreet, Equifax, and Experian.

Non-reporting trade accounts can also be helpful. While you do want trade accounts to report to at the very least one of the CRAs, a trade account which does not report can also be of some value.

You can always ask non-reporting accounts for trade references. Additionally, credit accounts of any sort can help you to better even out business expenditures, thereby making financial planning less complicated.

Store Credit

Store credit comes from a variety of retail service providers.

You must use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, use the business’s EIN on these credit applications.

Fleet Credit

Fleet credit is from companies where you can purchase fuel, and fix and take care of vehicles. You must use your Social Security Number and date of birth on these applications for verification purposes. For credit checks and guarantees, make certain to apply using the company’s EIN.

These are companies like Visa and MasterCard. You must use your Social Security Number and date of birth on these applications for verification purposes. For credit checks and guarantees, use your EIN instead.

These are usually MasterCard credit cards. With more credit, these are within reach.

Monitor Your Business Credit to Help Yourself Get Business Funding for Bad Credit

Know what is happening with your credit. Make sure it is being reported and fix any inaccuracies as soon as possible. Get in the habit of checking credit reports. Dig into the details, not just the scores.

We can help you monitor business credit at Experian and D&B for 90% less than it would cost you at the CRAs. See: www.creditsuite.com/monitoring.

Fix Your Business Credit to Increase Your Chances for Getting Business Funding for Bad Credit

So, what’s all this monitoring for? It’s to challenge any mistakes in your records. Errors in your credit report(s) can be fixed. But the CRAs typically want you to dispute in a particular way.

Dispute Any Errors to Improve Your Chances to Get Business Funding for Bad Credit

Disputing credit report mistakes generally means you mail a paper letter with copies of any proofs of payment with it. These are documents like receipts and cancelled checks. Never mail the originals. Always send copies and retain the originals.

Fixing credit report inaccuracies also means you precisely detail any charges you contest. Make your dispute letter as crystal clear as possible. Be specific about the problems with your report. Use certified mail to have proof that you mailed in your dispute.

A Word about Building Business Credit and How to Get Business Funding for Bad Credit

Always use credit smartly! Don’t borrow beyond what you can pay off. Track balances and deadlines for payments. Paying promptly and completely does more to boost business credit scores than almost anything else.

Establishing business credit pays. Excellent business credit scores help a small business get loans. Your loan provider knows the business can pay its debts. They recognize the company is for real.

The company’s EIN connects to high scores and lenders won’t feel the need to ask for a personal guarantee.

It is the simplest way to get business funding for bad credit.

Getting Business Funding for Bad Credit: Takeaways

Business credit is an asset which can help your small business for many years to come. It is the most surefire way to get business funding for bad credit. And, while you’re at it and improving your business credit, you may want to work on improving your personal credit. It is a similar process in the sense that you need to pay your bills on time, correct any errors, and add any missing information.

Because one way around trying to get business funding for bad credit is to stop having bad credit in the first place.

Learn more here and get started toward growing company credit.

Do You Need to Know Just How Banks Determine Your Recession Business Banking Rates?

Banks are in the business of judging your company’s creditworthiness. This has a direct relationship to several important issues. Ignore these at your peril! It pays to take the time to try to understand how your recession business banking rates will work.

Assets concentrated in ever‐larger banks is troublesome for local business proprietors. Big financial institutions are a lot less likely to make small loans. Economic recessions mean financial institutions become more careful with financing. For this reason, you need to understand your business bank ratings. It’s the only way you will be able to improve them.

Your Recession Business Banking Rates – It All Has to do With Your Bank Credit Score

But what’s that all about?

Did you know there are many ways you can ravage your bank credit score? It is, regrettably, quite easy to run a power saw through your bank rating. Your recession business banking rates can easily end up taking a hit.

But before going any further, do you know the difference between bank credit ratings and small business credit?

Business credit is the full and complete amount of cash that your small business can receive from all manner of lenders. That means credit unions, credit card companies, and also renting businesses. And it also means vendors, under what’s called trade credit or vendor credit or trade lines.

A bank credit score, on the other hand, is a measure of the full amount of borrowing ability which a company can get from the banking system only.

Bank Credit Scores Explained

A company can get more business credit fast . That is, as long as it has at least one financial institution reference. Plus it must have an average day to day account balance of at the very least $10,000 for the most recent three months. This setup will generate a bank credit rating of a Low-5. So this means it is an Adjusted Debt Balance of from $5,000 to $30,000.

A lower score, like a High-4, or balance of $7,000 to $9,999 will not result in an automatic turn down of the small business’s loan application. But it will slow down the approval process.

What is a Bank Rating?

A bank rating is a measure of the average minimum balance as kept in a business bank account over a 3 month long period. Hence a $10,000 balance| will rate as a Low-5, a $5,000 balance will rate as a Mid-4, and a $999 balance will rate as a High-3, etc.

A company’s chief goal ought to always be to maintain a minimum Low-5 bank rating (or, an average $10,000 balance) for a minimum of 3 months. This is because, without at the very least a Low-5 score, most financial institutions will assume a business cannot pay back a loan or a business line of credit.

Yet there is one point to keep in mind – you will never see this number. The financial institution will keep this number in its back pocket.

The Bank Rating Ranges

The numbers work out to the following ranges:

To get a High-5 rating, your business will need to have an account balance of $70,000 to $99,999. For a Mid-5 score, your business has to have an account balance of $40,000 to $69,999. And for a Low-5 score, your company should hold onto an account balance of $10,000 to $39,000. So your small business needs this level bank rating or better to get a bank loan.

For a High-4 score, your small business needs to have an account balance of $7,000 to $9,999. And for a Mid-4 rating, your company must have an account balance of $4,000 to $6,999. So for a Low-4 score, your company will need to have an account balance of $1,000 to $3,999.

Your Recession Business Banking Rates – It Can Be Scary Easy to Damage Your Bank Rating

And now, without further ado, here are 7 ways you can leave your bank score in tatters. These methods can all too easily hurt your recession business banking rates.

7th Way to Ruin Your Bank Credit

Don’t maintain a minimum balance for at least three months. Since every bank score cycle has a basis in the last 3 months, a seesawing balance will harm your bank score.

6th Way to Ruin Your Bank Credit Rating

Don’t bother to assure that your company bank accounts are on report the exact same way as all your small business records are. And do not assume they are on report with the exact same physical address (no post office box) and contact number. Sow confusion here by editing one and not another, or not dealing with an error if there is one.

Have a look at our expert research on bank ratings, the obscure reason why you will – or won’t – get a bank loan for your company.

Fifth Way to Destroy Your Bank Credit

To support # 6, don’t make sure that each and every credit agency and trade credit vendor likewise lists the business name and address the precise same way. This is every keeper of financial records, earnings and sales taxes. It includes web addresses and email addresses, directory assistance, etc.

No loan provider is going to think of the myriad ways that a company may be listed, when they check out the business’s creditworthiness. So if they cannot find what they need fast, they will refute an application. Or it won’t be on the report to a company credit reporting bureau such as Experian, Equifax or Dun & Bradstreet.

For that reason, if they are not able to locate what they need quickly, they will simply reject the application. So make certain your documents are a mess!

4th Way to Damage Your Bank Credit Rating

Never handle your bank account responsibly. This means that your small business must not avoid writing non-sufficient funds (NSF) checks at all costs. Such is due to the fact that those decimate bank ratings. Non-sufficient funds checks are something which no company can afford to let happen.

Balancing checkbooks and accounts is so boring anyway. You’ve got adequate cash without even making sure, right?

Third Way to Ruin Your Bank Credit Rating

To add to # 4, do not add overdraft protection to your bank account ASAP, to avoid NSFs. Why bother thinking in advance or preparing for the future? Everything is going to be terrific permanently, right?

Writing checks insufficient funds (NSFs) is a sure way to wreck your bank score.

2nd Way to Damage Your Bank Credit Rating

Do not let your business show a positive cash flow. The cash coming in and leaving your business’s bank account should reflect a positive free cash flow.

A positive free cash flow is the quantity of revenue left over after a firm has paid all its expenses. According to Investopedia, it “represents the cash a company can generate after required investment to maintain or expand its asset base. It is a measurement of a company’s financial performance and health.”

When an account shows a positive cash flow it indicates your small business is generating more revenue than you use to run the firm. That means the bank will feel your small business can cover its costs.

So if you really intend to wreck your bank score, get whatever’s expensive for your company so your costs overtake your profits. Doesn’t every factory merit luxurious carpets in the loading dock?

Have a look at our expert research on bank ratings, the obscure reason why you will – or won’t – get a bank loan for your company.

First Way to Damage Your Bank Credit Rating

Financial institutions have quite the motivation to lend to a small business with consistent deposits. And an entrepreneur must also make regular deposits to keep a positive bank rating. The business owner has to make a lot of regular deposits, greater than the withdrawals they are making, to have and maintain a great bank rating. If they can do that, then they will have a great bank credit score.

Consistency is the hobgoblin of little minds, right? So be a free spirit!

Your Recession Business Banking Rates – It is Way too Easy to Destroy Your Company’s Bank Score – Even Though You Will Never See It

You, the entrepreneur must never make consistent deposits. And these deposits ought to never be more than the withdrawals you are making, to ruin your bank credit.

If you can do these things, then your company will have a horrible bank credit score. And then a bad bank credit score means your firm is much less likely to get small business loans. This is how you can truly muck up your recession business banking rates.

Your Recession Business Banking Rates – Just Kidding: Of Course We Do Not Actually Want You to Destroy Your Company’s Bank Credit Rating!

But your recession business banking rates are a thing of value. You should want to protect and nurture it. So, where do you go from here?

The First Great Way to Rescue Your Bank Credit Rating

Probably the easiest way to achieve and maintain an excellent bank credit rating is to deposit at least $10,000 into your company bank account. And keep it there for as much as six months. While you will still have to make regular deposits, this one simple step will assist in 3 ways. One, you will have kept an excellent minimum balance for at the very least 3 months. Two, you will probably not overdraw with such a great balance. And three, you will be at the magic minimum for a Low-5 bank credit rating. Thus you will be dealing with our # 4 and # 7, above.

And you may even have the ability to get around our # 3. But we still highly recommend overdraft protection.

Have a look at our expert research on bank ratings, the obscure reason why you will – or won’t – get a bank loan for your company.

The 2nd Excellent Way to Rescue Your Bank Credit Rating

A 2nd thing you can do is make certain your small business account details are consistent across the board, everywhere. While it may take some work order to make certain every little thing is right, you will be dealing with our # 5 as well as # 6, above.

The Third Great Way to Rescue Your Bank Credit Score

A 3rd thing you can do is make consistent deposits, as well as make sure they are greater than the quantities you are withdrawing each month. This will take care of our # 1 and also # 2.

Your Recession Business Banking Rates –Takeaways

Your bank score is not to be trifled with. The financial institutions maintain a mystery about them. Still, failing to keep your bank credit rating high will make it a whole lot harder to do well in business. In this way, you can defend and improve your recession business banking rates.

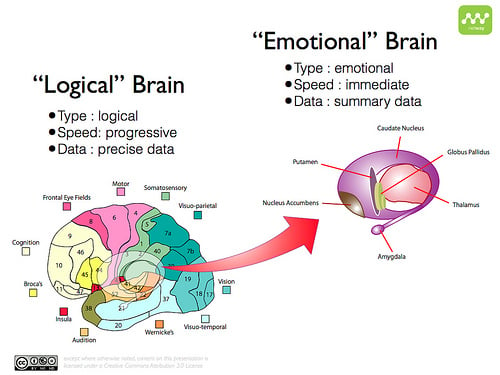

Whether you care to admit it or not, the decisions you make today will be driven by your emotions. In emotional marketing, we talk a lot about using psychological triggers to get customers to click, convert, engage, etc.

“By leveraging common psychological triggers all people have,” you might hear, “you can drive more sales.”

While it may feel like we make decisions with our minds, using logic and reasoning, the “mental triggers” we hear about are tied more to emotion than anything else.

Case in point, Antonio Damasio spent time studying individuals with damage to the area of the brain where emotions were generated and processed.

While these subjects functioned just like anyone else, they couldn’t feel emotion.

The other thing they had in common was they all had trouble with making decisions.

Even simple decisions about what to eat proved difficult.

While they could describe what they should be doing using logic and reason, most decisions couldn’t be settled with simple rationale.

Without emotion, they weren’t able to make a choice.

This is supported by data from Gerard Zaltman, author of “How Customers Think: Essential Insights into the Mind of the Market.”

Zaltman found that95% of cognition happens beyond our conscious brain, instead coming from our subconscious, emotional brain.

Emotions are an X factor you can’t control, but you can’t afford to ignore them in your content marketing.

Why is Emotion Marketing so Effective?

When you make an emotional connection with your audience, it’s incredibly easy to steer them to the desired outcome.

You’ve formed an emotional bond, however brief and fleeting, that makes them open to ideas and suggestions. It creates a certain level of trust that’s virtually impossible to artificially manifest.

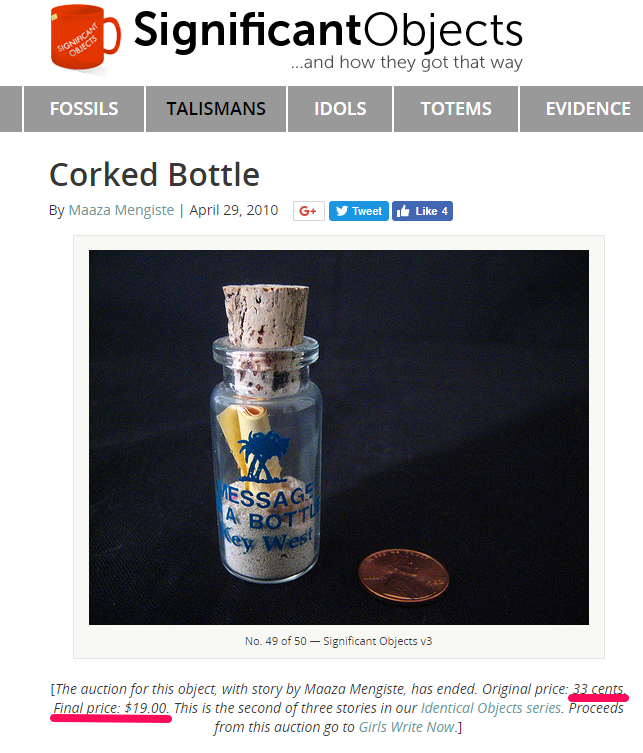

Rob Walker and Joshua Glen found firsthand what an emotional connection can do.

In one experiment, they bought hundreds of items from thrift stores and similar locations — all cheaply priced.

The duo wanted to see if they could sell the products using an emotional connection through the power of stories alone.

With 200 writers on board, they generated fictional stories for the products and used those stories to sell the thrift store items at auction on eBay.

And they did it all using that emotional connection through storytelling.

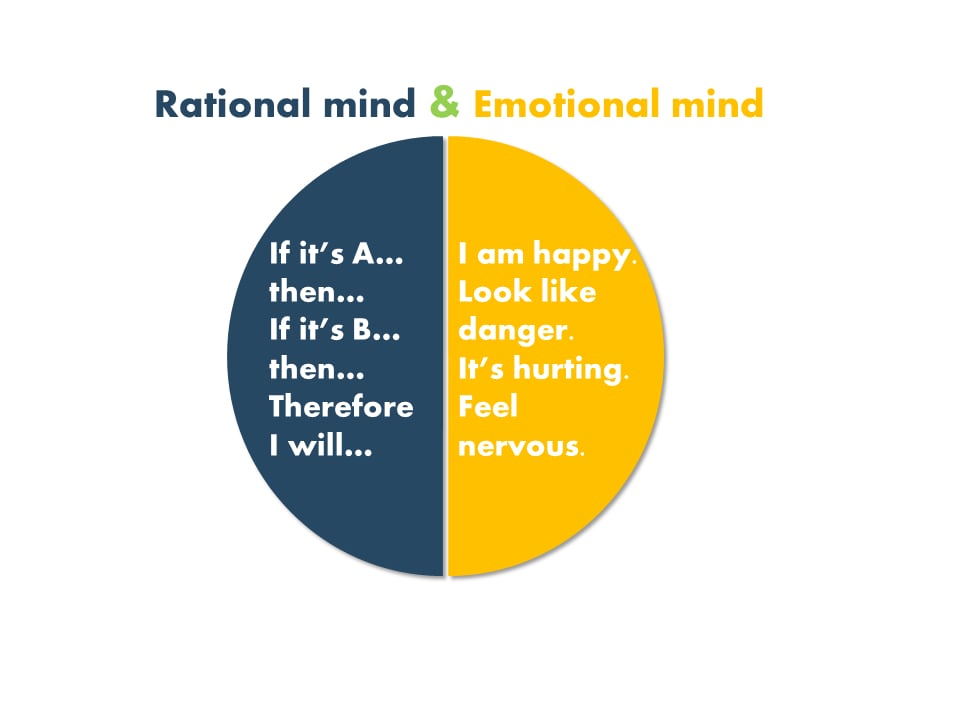

That’s not to say there isn’t a place for the logical or the rational in decision making.

This is where marketers often leverage the theory of dual processing in psychological marketing.

The theory holds that the brain processes thoughts and decisions on two levels.

The first level is that of emotion, which processes automatically, unconsciously, and provides a rapid response when we need it with virtually no effort.

The second level is the more deliberate and conscious thought process, where we handle decisions with reason and logic. It happens far slower than the emotional response.

In most cases, we fire back with a ready response from our emotions and then try to consciously rationalize it.

Think about some big-brand rivalries and preferences will surface in your mind.

How do you feel when you look at this major brand comparison?

Here’s another common one that has people divided, sometimes within the same family:

And then there’s this brand rivalry we know all too well.

In each of these, you likely have an opinion almost instantly about which you prefer, but it’s not because you have a logical reason.

It’s typically tied to emotion and/or experience; how you feel using their products, or how the brands left you feeling after an experience or reading a news article.

The brain then tries to rationalize that emotional response.

For example, your emotional response goes straight to Coke and then your brain works to rationalize the decision by deciding that it tastes better in a can, it’s fizzier, has a stronger bite than Pepsi, etc.

So, while you might feel like you’re making a rational choice about your beverage, it’s really just an emotional one.

The most successful marketers know how to lean on the emotional over logic in order to make their content draw in the audience.

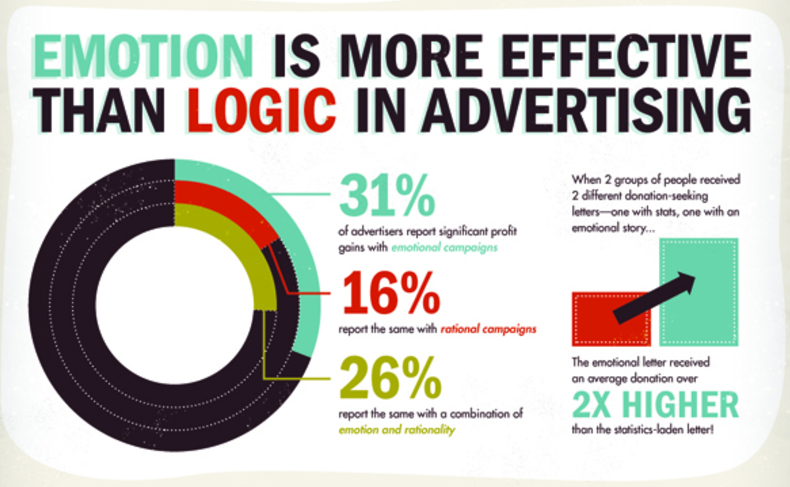

That’s whynearly a third of marketers report significant profit gains when running emotional campaigns, but the number of successful campaigns dips if you introduce logic into the marketing.

And those results get sliced in half when marketers switch to logic over emotion.

We experience a laundry list of emotions every day.

Is it really as simple as leveraging some emotion to make content more effective?

Yes and no.

Emotion is certainly important, but there are also other factors like timing, exposure, the format of the content, how it’s presented, who produced or shared it, etc.

Despite understanding the role emotion plays in content, we still haven’t quite perfected a formula for what makes content go viral.

Though we’ve gotten pretty close.

Brands have long tried to inflate the consumer’s emotional response through manufactured content; some met with great success.

The videos profile a person around the world who uses Intel’s technology to create new experiences and build new technology that makes a difference in the world.

Like 13-year-old Shubham Banerrjee, who used Intel’s technology to build an affordable Braille printer.

And of course, some companies try to leverage emotion and create viral campaigns that just don’t take off.

CIO reported a number of failed viral marketing campaigns, such as “Walmarting Across America.”

In this blog, two average Americans travel across the country visiting Walmart locations, reporting their interactions on a blog along the way.

After countless upbeat entries about how people loved working for the company, it was discovered that the trip was paid for by Walmart and the entire thing was a campaign created and managed by the company’s PR firm.

That didn’t receive a warm reception from the blogosphere, which deemed the content to be a “flog” or fake blog.

Which Emotions Attract the Most Marketing Engagement in Content?

Many emotions fuel our behaviors and our decisions, especially our purchase decisions.

Some more than others — especially when they’re authentic.

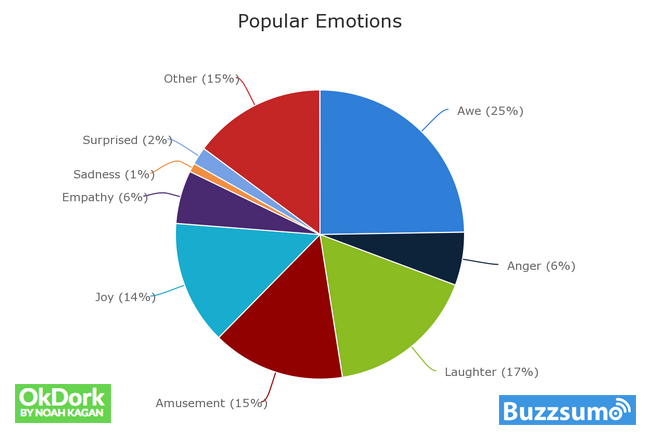

A study wasdone by Buzzsumo analyzing the top 10,000 most-shared articles on the web. Those articles were then mapped to emotions to see which emotions had the greatest influence on content.

The most popular:

Awe (25%)

Laughter (17%)

Amusement (15%)

Conversely, the least popular were sadness and anger, totaling just 7% of the content that was most shared.

Two researchers at Wharton also wanted to dig deeper into virally shared content to find commonalities and better understand what makes that content spread.

What they found was the emotional element, and some very specific results tied to emotions.

Content is far more likely to be shared when it makes people feel good or it creates positive feelings such as leaving them entertained.

Facts or data that shock people or leave them in awe were more likely to be shared.

Instilling fear or anxiety pushes engagement higher, from comments being posted to content being shared.

People most commonly shared content that incited anger, leaving comments as well.

While some emotions are more likely to engage than others, every audience is different. What drives one to action may do very little for another.

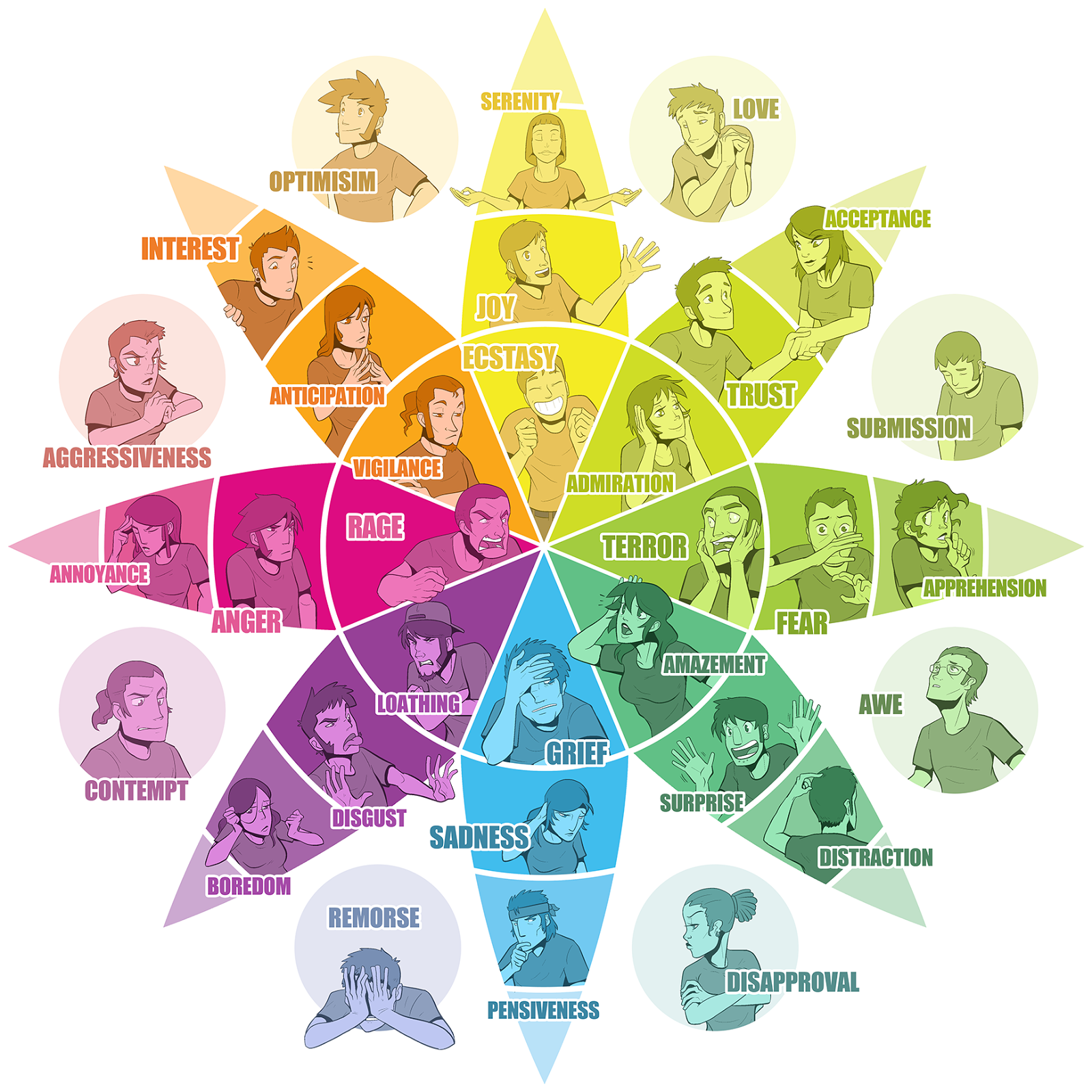

This modern adaptation of Robert Plutchik’s Wheel of Emotion,illustrated by CopyPress, shows the range under eight primary emotions: joy, trust, fear, surprise, sadness, disgust, anger, and anticipation.

For content to be widely shared and have an impact on your audience, it needs to leverage one or more of these emotions.

The proof is on the web, not only in the statistics I shared above, but also in the popularity of user communities that regularly share content.

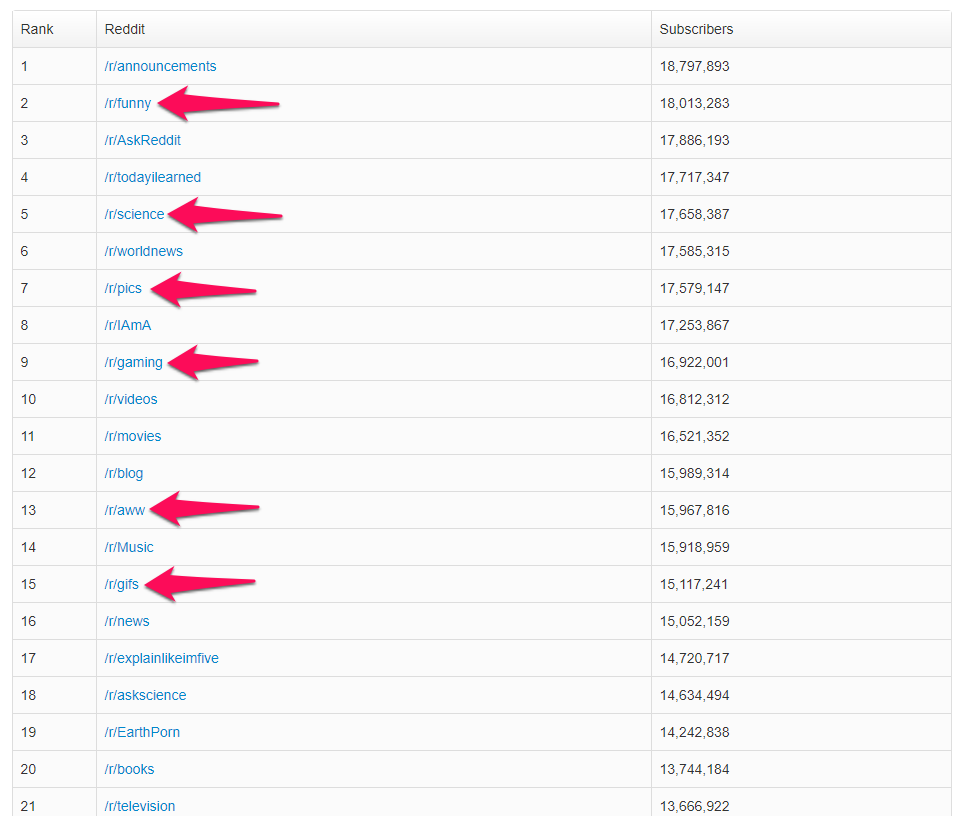

Just look at Reddit and some ofthe most popular subreddits by subscriber count. Each can be tied back to emotions (some more obviously than others) like anticipation, awe, joy, and more.

Here’s how some of those emotions can play into the engagement with your audience:

Anxiety May Cause Uncertainty For Customers

You don’t want your audience to make bad decisions. Bad decisions can lead to buyer’s remorse, which can paint your brand and the overall experience in a negative light.

But it can be helpful if you leave the audience a bit more open to influence.

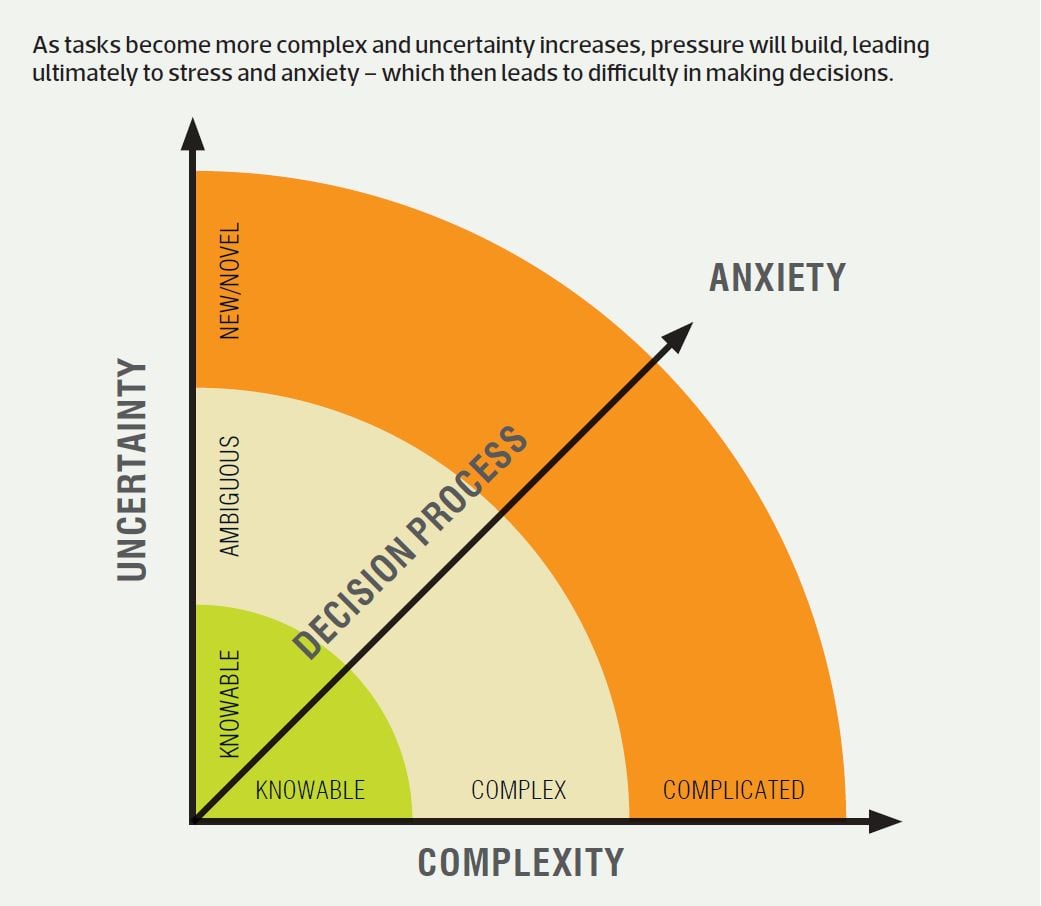

A Berkeley study revealed that anxiety can be linked to difficulty in using information around us to make decisions. When we experience uncertainty, it becomes harder to make decisions and our judgment is clouded.

Still, anxiety can also spur people to act as a result of that uncertainty.

Take a two-year study by Wharton Ph.D. student Alison Wood Brooks and a Harvard Business School professor.

They found that upon increasing the anxiety of certain subjects with video footage, 90% of the “anxious” participants opted to seek advice and were more likely to take it.

Only 72% of the participants in a neutral state, who viewed a different video, sought advice.

Capture the Focus of Your Emotional Marketing Audience With Awe

Awe is comparable to wonder, but it doesn’t always fall under the umbrella of joy or humor.

It’s intended to captivate the audience and keep them riveted.

You often see this kind of hook in headlines that seem so earth-shatteringly significant that no one in their right mind would want to miss it.

Co-founder Drew Houston submitted his product to the website Digg, hoping to get some visibility from the social bookmarking site. That headline helped significantly.

Another great example of using Awe to capture attention is a video produced by Texas Armoring Corporation.

To emphasize the quality of the company’s bullet-resistant glass, the CEO crouched behind one of TAC’s glass panels while several rounds were fired at it from an AK-47.

Awe can impact decision making as much as anxiety.

A study from Stanford University found that people experiencing awe are more focused on the present and less distracted by other things in life. They also tend to be more giving of their time.

When you have their attention and their focus, they’re more likely to have time to rationalize a decision.

Drive People to Action With Laughter and Joy Through Emotional Marketing

While joy and laughter can have their lines blurred, they’re really two different emotions when it comes to your content.

Because while laughter often leads to joy, not everything that is joyful is laugh-out-loud funny.

Still, next to awe, joy, laughter, and amusement were the highest contributors to social sharing and engagement in the above studies.

That influence goes all the way back to early childhood.

Per psychoanalyst Donald Winnicott, joy and amusement are hardwired into us from birth.

His studies tell us that our innate desire for joy increases when it’s shared. That’s the nature of the “social smile.”

That explains why these feelings or emotions are such huge drivers behind the virality of content. Happiness, overall, is a huge driver for content sharing.

In fact,Jonah Berger’s study of the most-shared articles in the New York Times (around 7,000 articles) revealed the same kind of results around emotion.

The more positive the article, the more likely it was to go viral.

Brands have worked “joy marketing” into their strategies for decades, aiming to make their audience feel warm, comfortable, and happy.

Joy can take a lot of forms, though, and it doesn’t have to be commercially intended to elicit a direct sale.

Look at what Beringer Vineyards did with influencer marketing.

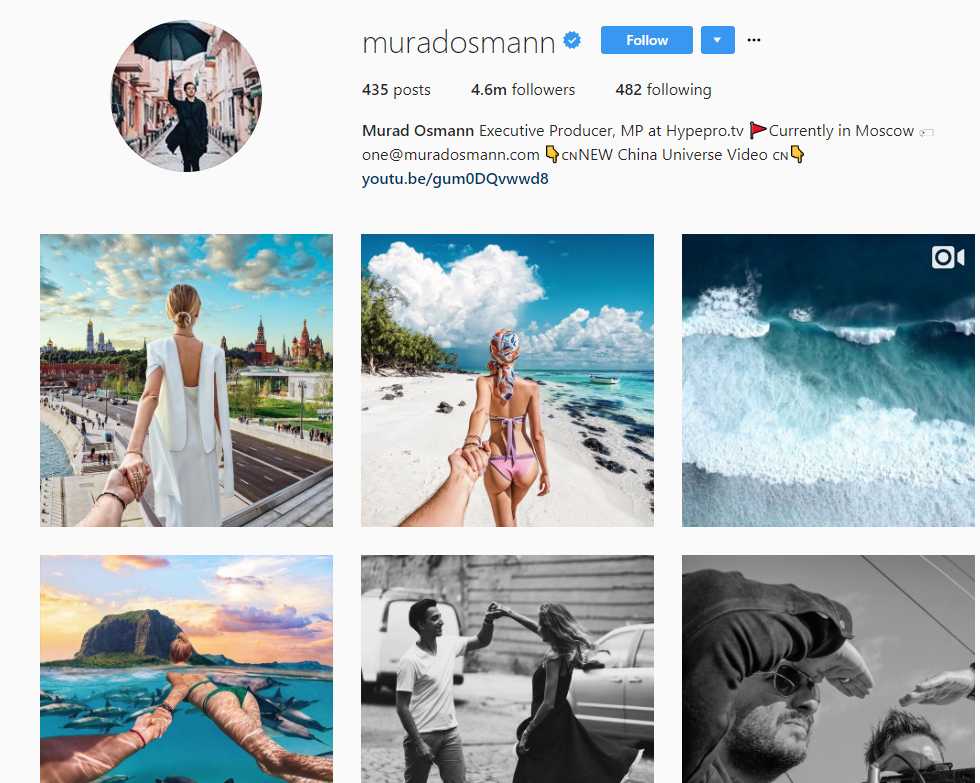

Russian Instagram sensationsMurad and Nataly Osmann built a following of more than 4.5 million people with photos featuring them holding hands at locations around the globe during their world travels.

They attached the hashtag #FollowMeTo on those posts.

The couple teamed up with Beringer Vineyards to create some images meant to inspire joy, love, and of course the sense of adventure the couple already shared with their hashtag.

Immediate Gains in Emotional Marketing From Anger

Anger may be perceived as a negative emotion by some, but it can have positive influences as well as positive outcomes when leveraged in the right way.

A leading researcher in the study of anger, Dr. Carol Tavris, draws a parallel between anger and how it impacted society over the years.

Women’s suffrage, for example, developed from anger and frustration.

Anger can be empowering for the individual, bringing a sense of clarity and positive-forward momentum. It gives people a feeling of direction and control according toa study from Carnegie Mellon.

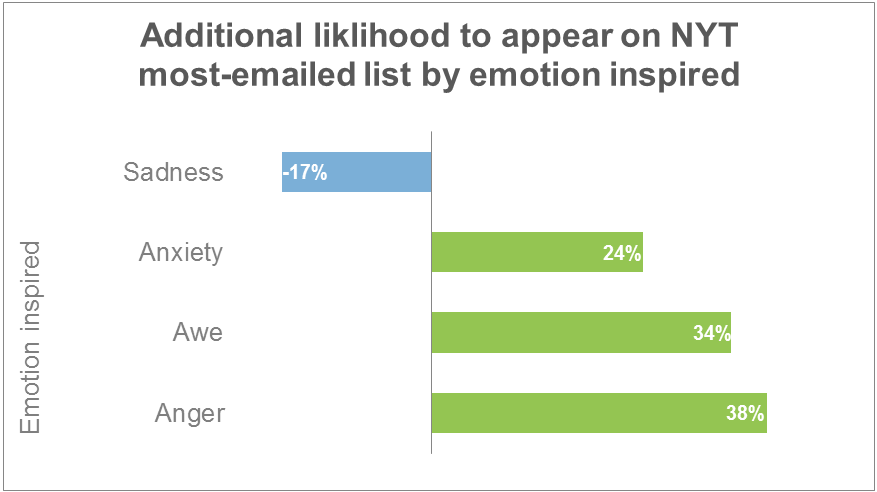

In fact, Berger’s study of the New York Times content found that content which incites feelings of frustration or anger is34% more likely to be featured on the Time’s most emailed list than the average article.

Now, I’m not suggesting that you deliberately create controversy by taking shots at readers or picking fights.

The key with using anger in content is to frame an issue that incites anger or frustration in a way that’s constructive.

This piece of content is simple, yet it provokes engagement as well as thought when results are revealed in comparison to what an individual perceives to be the truth.

Using the Right Emotional Marketing Words in Content

The difference between logic and emotion in content comes down to the words we use and how we position statements and information.

When creating copy and content, you have to be acutely aware of whether you’re taking a rational or emotional approach to the information you’re sharing.

You need to think about the response you want to elicit to help guide your content development to make the right kind ofpsychological and emotional connection with your audience.

The context of your copy can remain the same.

By changing the words you use, however, you can make content appeal more to the emotions of the audience and prospective customer.

The simplest approach to finding the right high-emotion words takes only three steps:

Think about the action you want your audience to take when they read your content.

Decide what kind of emotional state will drive that action. What would make them do what you want them to do?

Choose emotionally persuasive words appropriate to the action and the emotion.

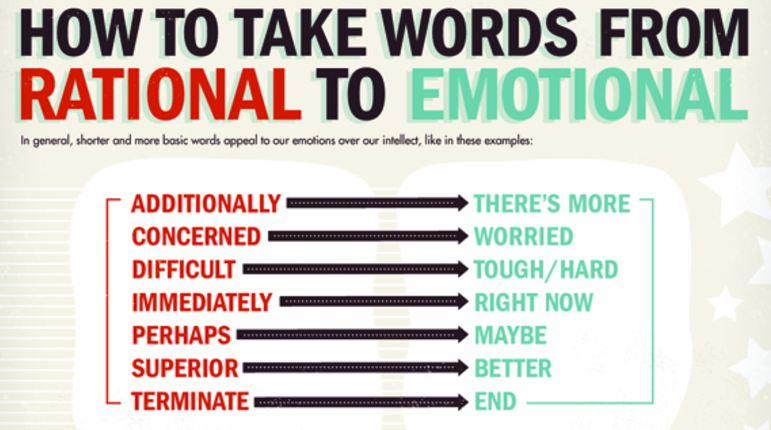

What you’ll find in researching the right words is that emotionally persuasive and impactful words tend to be abrupt. It’s the short, concise, basic words that appeal most to our emotions over our intellect.

The majority of this emotionally weighted list (and there are over 350 items) is made up of shorter words.

The rational mind, on the other hand, tends to associate with longer and more complex words.

You Can’t Assume When it Comes to Emotional Marketing

It’s not easy to make that emotional connection with your audience. You have to know them.

Like anything else in marketing, your decisions and the content you create needs to be based on data. In this case, that data is your audience research.

That same research that tells you what topics to create, where your audience spends their time, and the content they prefer to view, can clue you into how to make that emotional connection.

In this case, you want to build up the psychological profile of your audience. You can achieve this by asking the right questions to help steer your content research and production.

What do they find humorous?

What are the pain points that frustrate them?

What topics make them angry?

What are common problems they speak about?

What kind of content is being shared that clearly pleases them or brings joy?

Your research could turn up a common topic or theme that appears frequently in the content they read and share.

For example, you might discover that a certain segment or demographic in your audience has a strong affinity to family values, or health and wellness.

Turn that into a content campaign that shares the feel-good side of your company.

Delve into the family life of your employees, how your company supports the work/life balance, or better health initiatives.

Google is well known for its company structure, promoting flexible schedules, support of family time, personal projects, and a focus on work/life balance.

The company often shares behind-the-scenes images (visual content) showing off employees enjoying what they do. Here’s an example from Google Sydney’s offices:

That can influence a positive emotional response toward the brand when targeted segments see that content.

Emotional Marketing Works in the B2B Process

Don’t get caught up with the dated idea that emotion is only applicable to consumer-focused businesses.

Emotional marketing has its place in the B2B world as well.

You may be dealing with a longer buying process between one or more organizations, but the decisions are still made (and fueled by) people who are absolutely driven by emotion.

That includes emotions like:

Awe: over what a solution is capable of and feeling empowered to bring that solution to the workplace.

Anticipation: in finding a piece of the puzzle in a product or service that will help the company achieve its next goal or milestone.

Fear: in purchase decisions that could reflect on the individual, resulting in a personal risk associated with a B2B purchase.

Joy: in knowing that a B2B purchase is likely to lead to a positive outcome that will reflect positively on the individual.

You hold a great deal of influence with your audience when you’re able to tap into their emotions.

Once you understand your audience, you can better determine their emotional state.

From there, make the decision about whether you need to influence and exploit emotions that are already present, or if you want to create or give rise to emotions the audience wasn’t initially expecting or experiencing.

Even the most (seemingly) rational decisions are influenced by emotion — and that applies to everyone.

When you learn how to leverage that emotion in your content, you will see increases in engagement, social action, and conversions within your funnel.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.