Secured – Those guaranteed under the regards to an insurance coverage.

Advantage – The cash paid to the insurance policy holder when a case is made.

Proposal Price – The asking price or cash-in worth of your device holdings.

Bonus offer – Relates to a with-profits plan. The quantity is reliant upon the earnings made by the insurance coverage business.

Exchangeable Term Assurance – A term insurance plan which provides you the choice to transform your existing plan to a whole-life or endowment insurance plan, without needing to take more medical checkups.

Vital Illness Insurance – A plan that pays a round figure on the medical diagnosis of harmful diseases suggested in the regards to the strategy.

Reducing Term – A kind of term life insurance policy where the fatality advantage lowers each year as per your plan. This kind of certification is often marketed as home mortgage insurance policy.

Endowment Insurance – An insurance coverage that pays a specified quantity at the end of a given duration or upon the fatality of the guaranteed if it happens within that duration.

Family Members Income Benefit – Term guarantee which pays cash to the life ensured’s dependants for a collection duration, instead of paying a round figure.

Surefire Bond – A bond in which principal as well as passion are ensured by an entity besides the company. Surefire Bonds can be earnings or development.

Enhancing Term – The quantity as well as the cover you pay right into the plan are boosted by a certain percent yearly relied on the initial amount guaranteed. Created as a method to raise your life cover as your revenues rise.

Financial Investment Bond – Combines financial investment with some life cover. The settlements you make right into an insurance coverage plan or financial investment bond, normally a swelling amount, are spent in the insurance coverage firm’s with-profits or unit-linked funds (Life Funds).

Life Fund – This typically refers to Unit connected Investment Funds. Such funds are utilized for people holding life guarantee plans to spend in.

Maturation – A concurred day when an endowment plan finishes as well as the profits, consisting of any type of bonus offers, are payable.

Shared – A life insurance policy business that is possessed by its with-profits insurance holders.

Deal Price – The cost at which fund devices are purchased.

Costs – The quantity of cash paid right into an insurance plan.

Exclusive – A life insurance policy firm that releases its revenues to its investors.

Certifying Policy – A life guarantee based financial savings prepare that needs to be composed for a minimum of 10 years as well as need to satisfy specific certifying plan requirements to guarantee the last payment is free of tax.

Eco-friendly Term – Term Insurance that might be restored for one more term without proof of insurability.

Solitary Premium Policy – Where a solitary round figure is spent for an insurance coverage.

Amount Insured – The quantity of cash that is ensured to be paid under an insurance coverage, prior to any type of bonus offers are included.

Give up Value – Not appropriate to all life insurance policy plans. When he or she stops insurance coverage, the quantity that an insurance coverage policyholder is qualified to get

Term Insurance – Provides insurance holder with security just. Life insurance policy payable to a recipient just when an insured passes away within a defined number of years (the term).

Incurable Bonus – This is an additional perk figured out when a fatality or maturation insurance claim is paid. If the plan has actually been in-force for a minimal number of years at insurance claim time, incurable reward is usually only paid. The quantity depends on the revenues made by the insurer.

A kind of Life Fund that can spend in UK as well as abroad shares, home, dealt with rate of interest protections and also cash money. When you spend in this fund via an insurance coverage plan, you acquire ‘systems’.

If your insurance coverage plan is unit-linked, some of your cash is made use of to acquire ‘systems’ in a fund. Usually refers to plans that provide security as well as conserving such as endowment insurance coverage, entire life insurance policy as well as financial investment bonds.

Unit-Linked Single Premium Bond – A solitary round figure life insurance policy plan where your financial investment is topped a variety of Life Funds.

Whole Life Insurance – Whole life insurance policy gives a survivor benefit for the insurance policy holder as it develops money worth. The plan continues to be active for the life time of the guaranteed, as long as costs are paid according to the plan arrangement. You can select insurance policy that pays on fatality an assured amount just, the amount plus any kind of incentives that have actually been included, or the amount plus any type of extra worth from the development of the funds purchased.

Without Profits – When a plan gets to maturation or the insurance policy holder passes away, the quantity paid is the fundamental ensured amount just. You would certainly not be qualified to any type of incentives.

With Profits – Relates to insurance policy plans that integrate financial investment with security. This kind of plan is qualified to a share of the revenues made by the insurance policy firm.

With Profits Bond – An insurance coverage where your round figure remains in a lot of instances purchased a Unitised With Profits Fund (which is detailed under the Life Funds area).

Lowering Term – A type of term life insurance coverage where the fatality advantage reduces each year as per your plan. The repayments you make right into an insurance coverage plan or financial investment bond, generally a swelling amount, are spent in the insurance policy business’s with-profits or unit-linked funds (Life Funds). When you spend in this fund via an insurance coverage plan, you acquire ‘devices’. Normally refers to plans that supply security as well as conserving such as endowment insurance policy, entire life insurance policy as well as financial investment bonds.

Whole Life Insurance – Whole life insurance policy supplies a fatality advantage for the insurance holder as it constructs up money worth.

Credit Score Cards Without Late Fees? What You Don’t Know Can Hurt You

The passion prices aren’t especially reduced as well as the costs billed for paying late or going over your limitation can be high. Late charges of $39 aren’t unusual, as well as they are evaluated if your expense falls short to show up by the due day, also if it was postponed in the mail.

The debt card business have actually been paying attention to customer grievances concerning costly late charges and also numerous of them have actually reacted. There might be a spin included; Citibanks’s Simplicity card lugs no late costs as long as you make an acquisition each month within the payment duration. Aren’t late costs the card firm’s means of making certain that you pay your costs at all?

With the Citibank card, paying late brings the typical charge of up to $39 if you pay late and also have not made an acquisition throughout the invoicing duration. If you have actually made an acquisition within the invoicing duration, however you have actually still paid late, Citibank may, at its choice, elevate your passion price. American Express will certainly likewise elevate your rate of interest price if you pay late two times in a year, though not as high as the 30% or so that Citibank will certainly bill.

With passion prices possibly climbing to virtually 30% as well as using to your superior equilibrium, you would certainly be a lot far better off maintaining an existing card and also paying the late cost than the hundreds or also thousands of additional bucks you would certainly pay on a big equilibrium after the fine passion price is used. Of training course, you can stay clear of both late costs as well as rate of interest price walkings by merely paying your costs on time as well as preserving a tiny equilibrium or no equilibrium at all.

Aren’t late charges the card firm’s means of making certain that you pay your costs at all? With the Citibank card, paying late brings the typical cost of up to $39 if you pay late as well as have not made an acquisition throughout the invoicing duration. With rate of interest prices possibly increasing to almost 30% and also using to your exceptional equilibrium, you would certainly be a lot far better off maintaining an existing card and also paying the late cost than the hundreds or also thousands of additional bucks you would certainly pay on a big equilibrium after the fine rate of interest price is used. Of program, you can stay clear of both late charges as well as passion price walks by merely paying your expense on time and also preserving a little equilibrium or no equilibrium at all.

Credit Score Cards Without Late Fees? What You Don’t Know Can Hurt You

The passion prices aren’t especially reduced as well as the costs billed for paying late or going over your limitation can be high. Late charges of $39 aren’t unusual, as well as they are evaluated if your expense falls short to show up by the due day, also if it was postponed in the mail. The debt card business have actually been paying attention to customer grievances concerning costly late charges and also numerous of them have actually reacted. There might be a spin included; Citibanks’s Simplicity card lugs no late costs as long as you make an acquisition each month within the payment duration. Aren’t late costs the card firm’s means of making certain that you pay your costs at all? With the Citibank card, paying late brings the typical charge of up to $39 if you pay late and also have not made an acquisition throughout the invoicing duration. If you have actually made an acquisition within the invoicing duration, however you have actually still paid late, Citibank may, at its choice, elevate your passion price. American Express will certainly likewise elevate your rate of interest price if you pay late two times in a year, though not as high as the 30% or so that Citibank will certainly bill. With passion prices possibly climbing to virtually 30% as well as using to your superior equilibrium, you would certainly be a lot far better off maintaining an existing card and also paying the late cost than the hundreds or also thousands of additional bucks you would certainly pay on a big equilibrium after the fine passion price is used. Of training course, you can stay clear of both late costs as well as rate of interest price walkings by merely paying your costs on time as well as preserving a tiny equilibrium or no equilibrium at all.

Aren’t late charges the card firm’s means of making certain that you pay your costs at all? With the Citibank card, paying late brings the typical cost of up to $39 if you pay late as well as have not made an acquisition throughout the invoicing duration. With rate of interest prices possibly increasing to almost 30% and also using to your exceptional equilibrium, you would certainly be a lot far better off maintaining an existing card and also paying the late cost than the hundreds or also thousands of additional bucks you would certainly pay on a big equilibrium after the fine rate of interest price is used. Of program, you can stay clear of both late charges as well as passion price walks by merely paying your expense on time and also preserving a little equilibrium or no equilibrium at all.

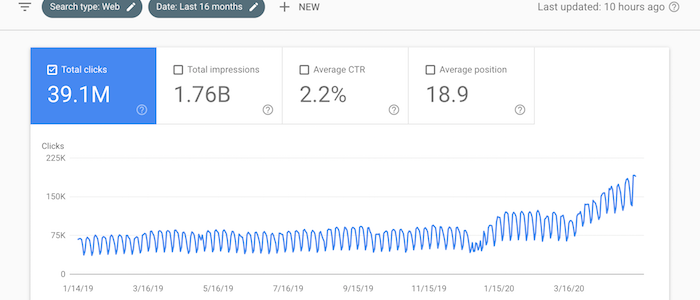

As you can see from the screenshot above, I’ve driven 30 million visitors to my website from SEO. Technically it’s more, but who’s counting. What’s funny, though, is I barely look at my traffic, even as Google continually rolls out algorithm updates. I know that sounds contradictory because if you are an SEO, why wouldn’t …

Recurring Income Home Business Online– What To Look For Do you intend to have the ability to take some time off whenever you intend to, as well as job whenever you want to? Do you wish to utilize your company with a network of companions that deal with you and also for you– without you …

Get Business Credit Cards with no Personal Guarantee and Beat the Business Recession

Do you know how to beat the business recession? You get business credit cards with no personal guarantee? We do, and we are here to show you how. This method will work no matter what is happening with COVID-19.

Normally, getting credit isn’t easy.

You know what I’m talking about. You looked around the big banks, and then the medium-sized banks and then the small ones. And you tried the banks where you do business. And you also tried the others suggested by your friends or business associates. But after your long quest, you were unable to acquire any kind of a small business credit card without a personal guarantee.

Assets focused in ever‐larger banks is problematic for small business proprietors. Big financial institutions are much less likely to make small loans. Economic declines mean banks become extra careful with lending. Fortunately, business credit does not count on financial institutions.

The Baddish News – in the Business Recession and Beyond

There are over 500 distinct business credit cards around but less than fifty of them grant credit to companies in the absence of a personal guarantee. Complicating matters, these cards are not marketed or granted to all interested clients.

You can identify with the banks’ viewpoint. They don’t like risk so they attempt to diminish it by securing a business credit card. They accomplish this by asking you, the business owner, to guarantee payments from your private finances. So, this is in the event of business default.

If worst comes to worst, and as a guarantor or co-signer you are not able to pay the financial obligation, then your individual assets will be executed. If you provide a personal guarantee and don’t pay your business credit card bills, the bank can seize your accounts, your vehicle, your residential property, and your stocks.

And they can seize whatever else you may have used to guarantee that card.

But your standpoint, of course, is that you need to have this card to run your company better.

Get Business Credit Cards with no Personal Guarantee in a Business Recession: What You Can Do

The first thing you can do, and it’s easier said than done, is to have patience, and grow creditworthiness for your small business in the same manner that you have established your personal credit history. For most companies, this means paying your debts punctually, plus staying in business for a while, to develop a record of creditworthiness.

To get rid of the sticking point of a personal guarantee, you will have to demonstrate to the bank that your small business is solid. And you have to show that it can produce consistent earnings, and it has a substantial cash flow.

And the business needs to have a flawless payment history. If all the above can be shown, it will be a lot easier to find small business credit cards with no personal guarantee.

This is how to start establishing business credit without personal guarantee.

Get Business Credit Cards with no Personal Guarantee in a Business Recession: Here are Measures You Can Take:

Get Business Credit Cards with no Personal Guarantee in a Business Recession: Step 1

Set apart yourself from your company. This means you can help your cause by incorporating or becoming a limited liability company (LLC). This is a separate entity from the owner(s). And it means you must register for a separate identification number with Internal Revenue Service.

If your business is already an LLC you can skip this step altogether.

Find out why so many companies are using our proven methods to improve their business credit scores, even during a recession.

Get Business Credit Cards with no Personal Guarantee in a Business Recession: Step 2

Get several company credit cards with personal guarantees. The ones with high spending limits will be better. This is because they are the only ones reported to the business credit agencies. And you definitely want business credit cards that do not report to personal credit.

Make sure when you buy these products, they have the personal guarantee removal feature baked right in. Keep your credit utilization at one third of your credit limit or less. Pay in a timely manner every time.

Make sure to use these small business credit cards to make your business’s large orders. These purchases, in combination with a low revolving debt and of course on time payment will all help.

These actions will demonstrate to the bank that your company can control its financial resources well. It will also persuasively show that the profit your business yields is enough to take care of financial obligations and more.

This can lead to an unsecured business credit card no personal guarantee.

Details

Make certain that your personal credit history stays spotless. Eventually, you can file a personal guarantee removal request for these preexisting business credit cards. So, this is normally six months to one year.

The financial institution will hold an account review. But they could also consider your private credit report. If the bank approves your request then you have met your goal. If the bank says no, don’t lose hope. Just go to the next step.

No personal guarantee business credit cards can be yours.

Get Business Credit Cards with no Personal Guarantee in a Business Recession: Step 3

You can elect to make an application for third-party guaranteed lending. For example, this could be an SBA loan, for financing. Settling such a loan will help you develop your business credit score.

You can also make an application for a small business credit card from a particular retailer. These retail credit cards often do not require a personal guarantee. Chose a store where your company makes purchases often. And by all means do not forget about those prompt payments!

These retail credit cards, along with an SBA loan will raise your PAYDEX score from Dun and Bradstreet. If you are unfamiliar with the term, the quick version is that PAYDEX is for businesses what FICO is for people.

Retail credit cards will give you an extra advantage from the start. This is because they will decrease your personal liability for your company debt. These are business credit cards for new businesses without personal guarantee.

Ask the financial institution again to take off the personal guarantee clause. Or apply for new business credit cards without any personal guarantee. Yes, new business credit cards without personal guarantee are possible.

You can try this once you have gotten an 80 PAYDEX score under the above conditions. This is when your opportunity to get such credit cards will increase exponentially.

Another Technique to Get a Business Credit Card with no Personal Guarantee in a Business Recession

Each specific card of this type asks you, the business owner, to satisfy a set of conditions. But these conditions will differ from one card to another. For a Sam’s Club ® Business MasterCard ® you need your business to bring in over $5 million in yearly sales.

The Bremer Bank Visa ® Signature Business Company Card is available for businesses with annual revenues between $1 million and $10 million. But at the same time other company credit cards with no personal guarantee attached call for an open Dun & Bradstreet file. Plus there can be other requirements to be met.

Be sure to consult the card issuer. And read through all the specifics of the promotion carefully.

Business Credit Cards with no Personal Guarantee in a Business Recession: Build Business Credit

Increase your chances big time by building business credit!

Small business credit is credit in a business’s name. It doesn’t link to an owner’s individual credit, not even if the owner is a sole proprietor and the solitary employee of the company.

Accordingly, a business owner’s business and consumer credit scores can be very different.

The Advantages

Considering that small business credit is distinct from individual, it helps to protect a small business owner’s personal assets, in case of legal action or business insolvency.

Also, with two distinct credit scores, a business owner can get two different cards from the same merchant. This effectively doubles buying power.

Another benefit is that even new ventures can do this. Visiting a bank for a business loan can be a formula for frustration. But building company credit, when done properly, is a plan for success.

Individual credit scores rely on payments but also additional components like credit usage percentages.

But for business credit, the scores actually only hinge on whether a small business pays its debts promptly.

The Process

Establishing business credit is a process, and it does not happen automatically. A small business will need to actively work to develop small business credit.

Having said that, it can be done easily and quickly, and it is much speedier than establishing personal credit scores.

Merchants are a big part of this process.

Carrying out the steps out of sequence will cause repetitive denials. Nobody can start at the top with small business credit. For example, you can’t start with retail or cash credit from your bank. If you do, you’ll get a denial 100% of the time.

Starting with vendors is how to get easy business credit cards no personal guarantee.

Company Fundability

A business must be fundable to loan providers and merchants.

Hence, a company will need a professional-looking website and e-mail address. And it needs to have website hosting from a company like GoDaddy.

Plus, company telephone and fax numbers ought to have a listing on 411.com.

In addition, the company telephone number should be toll-free (800 exchange or the like).

A small business will also need a bank account dedicated strictly to it, and it needs to have every one of the licenses essential for running.

Licenses

These licenses all must be in the correct, appropriate name of the small business. And they need to have the same business address and phone numbers.

So keep in mind, that this means not just state licenses, but potentially also city licenses.

Working with the Internal Revenue Service

Visit the Internal Revenue Service website and obtain an EIN for the small business. They’re totally free. Select a business entity like corporation, LLC, etc.

A company can start off as a sole proprietor. But they will probably wish to switch to a kind of corporation or an LLC.

This is in order to minimize risk. And it will make the most of tax benefits.

A business entity will matter when it involves tax obligations and liability in case of a lawsuit. A sole proprietorship means the business owner is it when it comes to liability and tax obligations. No one else is responsible.

A corporate business card will be in the corporate name. Yes, that even includes corporate credit cards without personal guarantee. And it can even mean start up business credit cards without personal guarantee. This is how to get a credit card without credit.

Setting off the Business Credit Reporting Process

Begin at the D&B website and obtain a cost-free D-U-N-S number. A D-U-N-S number is how D&B gets a business in their system, to produce a PAYDEX score. If there is no D-U-N-S number, then there is no record and no PAYDEX score.

Once in D&B’s system, search Equifax and Experian’s web sites for the small business. You can do this at www.creditsuite.com/reports. If there is a record with them, check it for correctness and completeness. If there are no records with them, go to the next step in the process.

In this way, Experian and Equifax will have something to report on.

Start with business credit cards without personal credit.

Vendor Credit

First you ought to build trade lines that report. This is also referred to as vendor credit. Then you will have an established credit profile, and you’ll get a business credit score.

And with an established business credit profile and score you can begin to get retail and cash credit.

These kinds of accounts have the tendency to be for the things bought all the time, like marketing materials, shipping boxes, outdoor work wear, ink and toner, and office furniture.

But first off, what is trade credit? These trade lines are credit issuers who will give you initial credit when you have none now. Terms are often Net 30, instead of revolving.

Therefore, if you get an approval for $1,000 in vendor credit and use all of it, you will need to pay that money back in a set term, such as within 30 days on a Net 30 account.

Soon, these will be business credit cards that do not require a personal guarantee.

Find out why so many companies are using our proven methods to improve their business credit scores, even during a recession.

Accounts That Don’t Report

Non-Reporting Trade Accounts can also be helpful. While you do want trade accounts to report to a minimum of one of the CRAs, a trade account which does not report can still be of some worth.

You can always ask non-reporting accounts for trade references. And also credit accounts of any sort should help you to better even out business expenditures, thus making financial planning simpler. These are providers like PayPal Credit, T-Mobile, and Best Buy.

These won’t start out as small business credit cards without personal guarantee. But in time, they can be credit cards for businesses with no personal guarantee.

Retail Credit

Once there are 3 or more vendor trade accounts reporting to at least one of the CRAs, then move to retail credit. These are businesses like Office Depot and Staples.

Fleet Credit

Are there more accounts reporting? Then move onto fleet credit. These are companies such as BP and Conoco. Use this credit to purchase fuel, and to fix, and maintain vehicles. Only use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, make sure to apply for business credit card no personal guarantee using the small business’s EIN.

By now, you’ll get a business credit card no personal credit check.

Find out why so many companies are using our proven methods to improve their business credit scores, even during a recession.

Cash Credit

Have you been responsibly handling the credit you’ve up to this point? Then move onto more universal cash credit. These are companies like Visa and MasterCard. Just use your Social Security Number and date of birth on these applications for verification purposes. For credit checks and guarantees, use your EIN instead.

These are normally MasterCard credit cards. If you have more trade accounts reporting, then these are doable.

Make sure to use the business EIN to apply for business credit card without personal guarantee. Then you will get a business credit card no personal guarantee.

A Word about Business Credit Building in a Business Recession

Always use credit sensibly! Never borrow beyond what you can pay off. Monitor balances and deadlines for repayments. Paying in a timely manner and fully will do more to boost business credit scores than almost anything else.

Establishing small business credit pays off. Excellent business credit scores can help a business get a business loan no personal guarantee. Your lending institution knows the business can pay its financial obligations. They recognize the small business is authentic.

The company’s EIN links to high scores and loan providers won’t feel the need to request a personal guarantee.

Business credit is an asset which can help your business for many years to come. It’s really the only way to get a business credit card no personal guarantee required.

Get Business Credit Cards with no Personal Guarantee in a Business Recession – These Could be Yours

With patience and over time, you can get business credit cards with no personal guarantee. All you need to have is what the banks ask. That is, a dependable small business generating consistent profit, with a strong cash flow. And then, you will have what it takes.

This is how to get business credit card without personal guarantee. The COVID-19 situation will not last forever!

I know that sounds contradictory because if you are an SEO, why wouldn’t you obsess about traffic, right?

Well, it’s because I’ve learned some hard lessons over the year… mainly because I’ve made a lot of mistakes.

So today, I wanted to share them with you so that you can learn from my mistakes… so here goes:

Lesson #1: Don’t obsess over rankings, obsess over conversions

I used to check my rankings every single day. Literally.

On top of that, I would log into Google Analytics 4 to 5 times a day and continually check my traffic.

That’s all I cared about back in the day… boosting my organic traffic.

But here is the thing: As my rankings and traffic went up over the years, my revenue didn’t go up proportionally.

For example, during one quarter in 2017, my SEO traffic went up 39.52%, but my revenue from SEO went up only 4.29%.

I quickly learned that traffic isn’t everything. If you can’t convert the traffic into revenue it doesn’t matter.

That taught me that you need to focus on the right keywords that drive conversions and continually optimize your site for conversions.

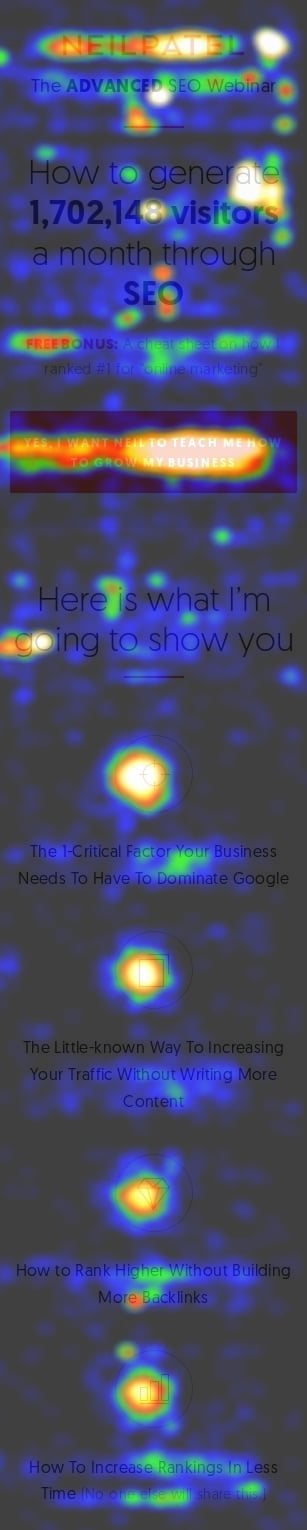

An easy first step for you to take is to install Crazy Egg and run a heatmap to see where people click so you adjust your design and copy to get more sales.

Lesson #2: The easiest way to grow your SEO traffic is international expansion

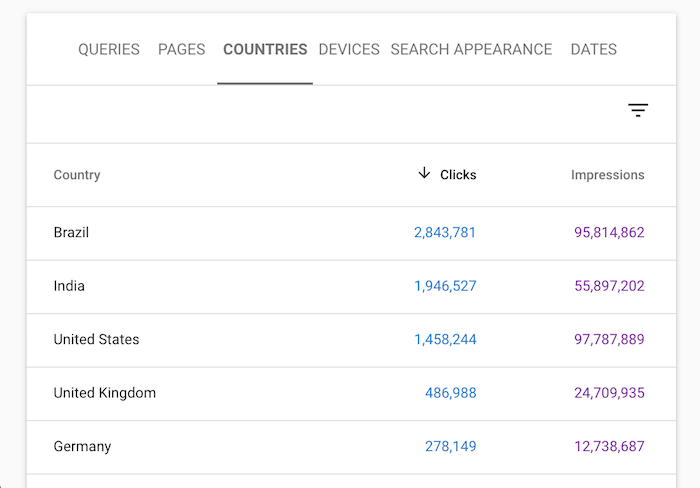

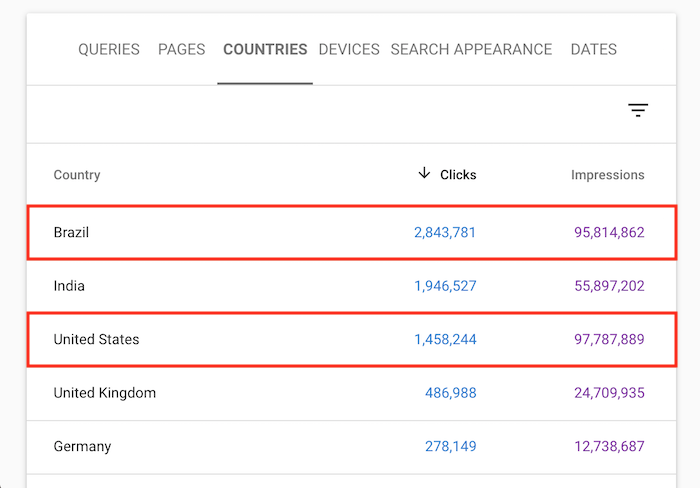

You already know that I get a lot of SEO traffic, but do you know what country drives most of my traffic?

If you guessed United States, you are wrong.

Brazil is my most popular region, followed by India.

International SEO is the easiest way to expand and grow your traffic. Here are a few posts that you should read before you expand your SEO globally:

Lesson #3: Keywords are very, very, very, very important

When I used to write my content, I didn’t obsess about the keywords when I should have.

My team actually proved me wrong on this.

I used to focus on writing content for humans and didn’t worry about search engines. My team, on the other hand, obsesses about keywords.

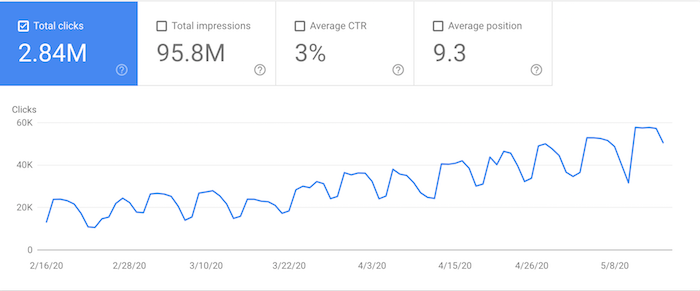

Just look at the growth of our traffic in Brazil because of our obsession with the right keywords.

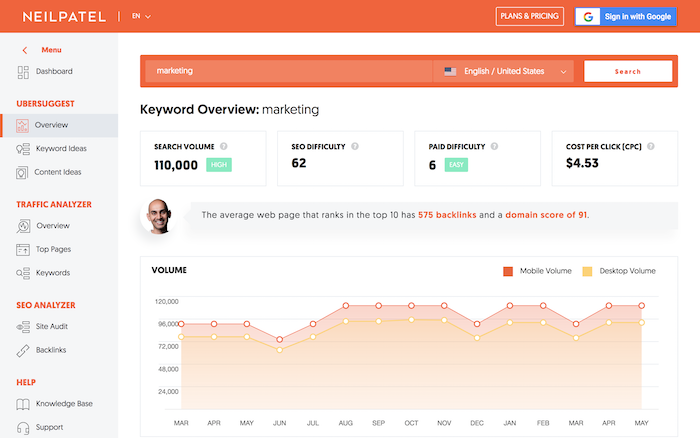

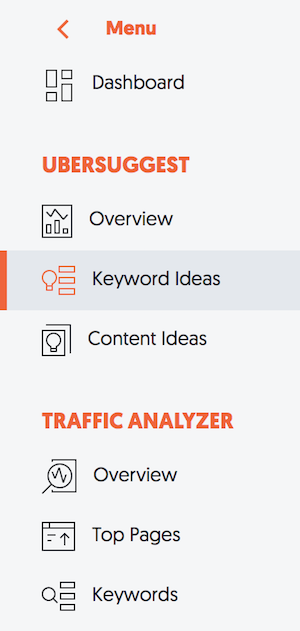

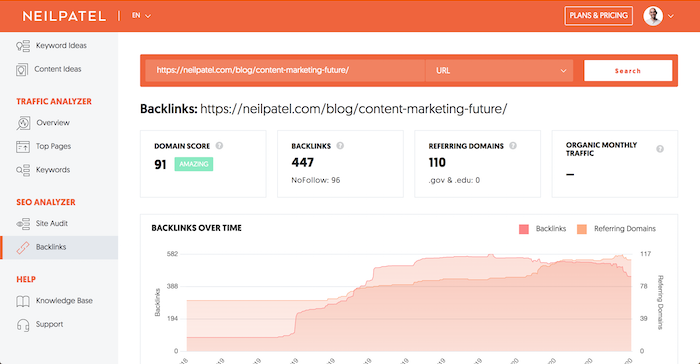

One simple thing I do before writing that has really helped is I head over to Ubersuggest and type in a few of the keywords that I want to go after.

Once it loads, you’ll see a report like the one above. I want you to then click on “Keyword Ideas” in the left-hand navigation.

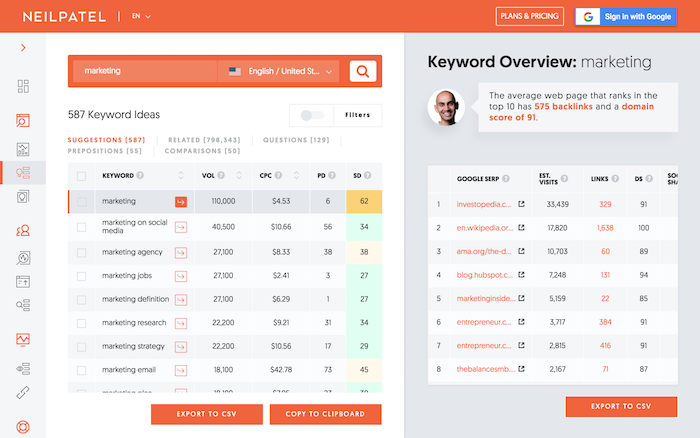

You’ll see a report that contains a list of keywords that you could potentially be targeting.

Make sure you click on the “Related” tab, as well as “Questions” and “Comparisons” … scroll through the list. You’ll see hundreds of keywords. Pick all of the ones that are relevant and ideally have a high cost per click (CPC). These are the keywords that’ll not only drive traffic but revenue as well.

Whenever I write a blog post, I go through this step. Every single time.

Lesson #4: AMP pages can drive more SEO traffic

AMP pages load faster on mobile devices than non-AMP pages.

If you aren’t familiar with the AMP framework, read this.

What most people won’t tell you about AMP pages is that:

In regions like the United States, Canada, and the United Kingdom, countries with decent Internet infrastructure, you won’t see much of an increase in traffic.

In regions with poor Internet infrastructure, like Brazil, you’ll see a 10 to 15% lift in mobile SEO traffic by having AMP pages.

AMP pages don’t convert visitors into customers as well as normal responsive web design. So, you’ll have to work on testing your AMP pages so you can boost your conversion rates.

Lesson #5: SEO will never convert as well as paid ads

When I started off with SEO, I would run projections on how much the traffic would make me.

But the numbers were always off, even if I was able to get the rankings.

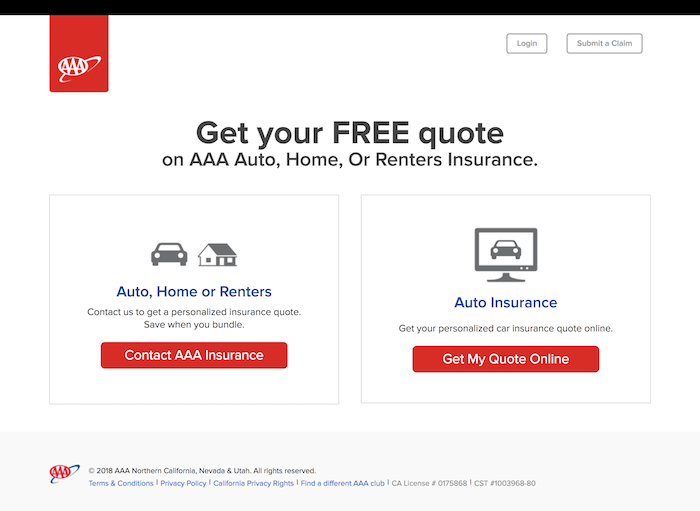

Here’s the main reason: If you are bidding on terms like auto insurance through ads, you can drive people to a landing page that looks like this:

But if you want to rank organically, you’ll have to do it through content. So, your page that ranks well will look more like this and convert less…

It doesn’t mean SEO is bad. In reality, it’s much cheaper in the long run than paid ads and will produce a better ROI. But don’t just assume that if you get 100 visitors from paid ads and 3 purchases that you’ll have the same conversion rate with your SEO traffic.

Chances are it will be significantly lower by maybe 2 or 3x, but because SEO is cheaper, it will be much more profitable.

Lesson #6: Remarketing is one of the best ways to generate an ROI from SEO

If you get a ton of traffic from SEO, there is a simple strategy you can implement to boost your conversions.

Remarket everyone on Facebook, Google, and YouTube.

That way people come to your site, read your content, and build trust with you and your brand.

Then you remarket them throughout the web with ads that prompt your products or services and send them to a landing page that will drive sales.

I’ve been doing this for years, just look at my old remarketing ad…

For the regions I use remarketing in, it is responsible for 46% of my leads.

Lesson #7: Don’t forget to update your old content

I publish one new blog post a week. I’m working on increasing this as I get more time, but for now, it is one a week.

Can you guess how many blog posts I update on a daily basis? Technically it is 0 (me at least), but my team focuses on updating at least 3 old blog posts per day. That’s roughly 90 a month.

Once you have a few hundred pages, make sure you focus on updating your old content or else your traffic will quickly drop.

You can use this content decay tool to see which posts you should update first.

This will help you continually grow your SEO traffic instead of hitting plateaus or seeing your traffic take massive drops.

Lesson #8: Don’t forget to optimize your title tags

One of the easiest ways to grow your rankings is to optimize your title tags.

If you can write persuasive copy and get more clicks, you’ll quickly move up on Google.

In Brazil, we spend more time doing this than we do in the United States.

We get a similar amount of impressions in Brazil, but we have more people focusing on improving our title tags and testing. Hence, we get 95% more SEO traffic in Brazil.

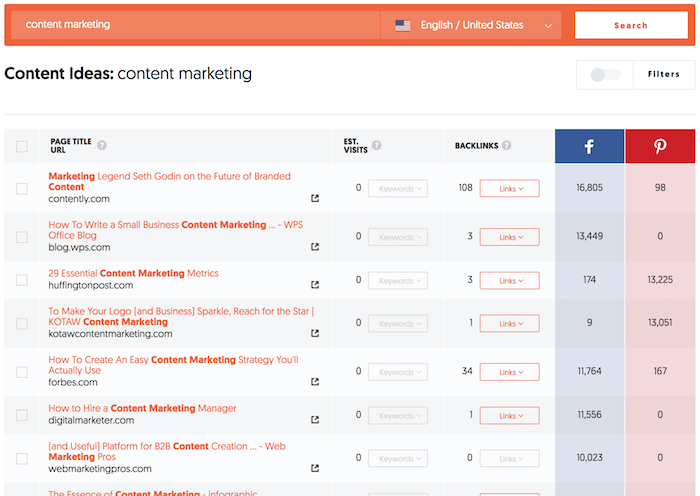

Another simple hack is to use the “Content Ideas” report in Ubersuggest.

On the right side of that report, you can see social share counts from Facebook and Pinterest. And on the left side, you see titles of articles.

Typically, if people like a title they share it more. So, look for titles that have a lot of shares as it will give you ideas on what you can use on your website to get more clicks and boost your rankings.

Lesson #9: Don’t put dates in your URL

I used to put dates in my URLs like:

Neilpatel.com/2017/12/title-of-post/

This causes search engines to assume that your content is related to a specific date. And after that date gets old, search engines assume your content is irrelevant and outdated.

The moment I removed the date from my URLs, I grew my SEO traffic by 58% in 30 days.

The majority of your pages that will rank are blog-related content. And blog posts tend to drive fewer direct conversions because people are on your site to read the content.

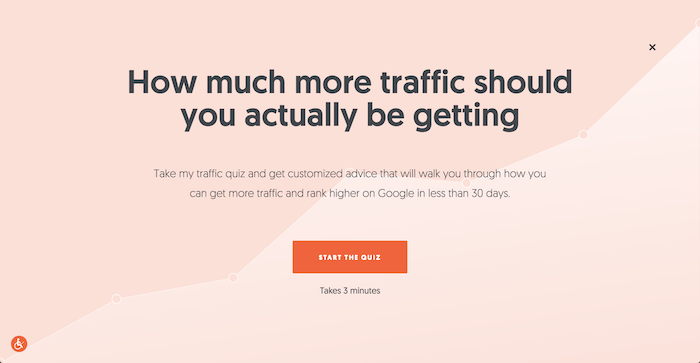

In order to maximize your conversions from SEO, you should consider using exit popups so you can convert more of those visitors into customers as they leave.

When you leave this site in most cases, you’ll see a popup that looks like:

And it drives you to this quiz, which allows me to convert SEO visitors into customers.

You can easily copy me by using Hello Bar. It works for all industries including B2B and ecommerce and even lead generation sites.

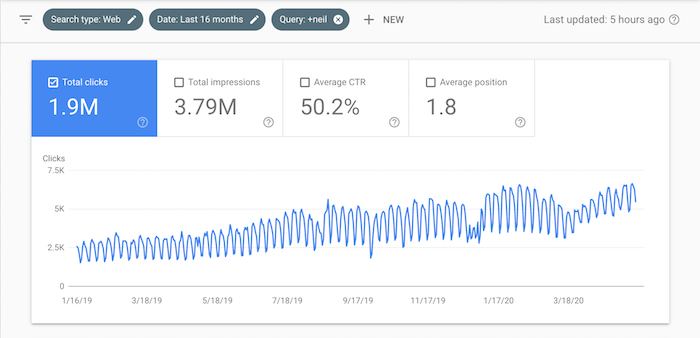

Lesson #11: Brand queries affect rankings

Everyone talks about how you need links to boost rankings.

One of the big reasons for my growth in SEO traffic is the growth in my brand. I’ve seen a direct correlation in which the more people who find me from my name, the more SEO traffic I get.

Just look at my brand growth over time:

I’ve received over 1.9 million visitors over the last 16 months from people typing in variations of my name in Google.

Lesson #12: Don’t waste your money on paid links

I’ve been doing SEO since I was 16 years old. That’s a long time…

When I started off as a kid, I dabbled in paid links and I used to dominate Google for terms like online casino, online poker, web hosting, auto insurance, and even credit cards.

And I was making a killing off of affiliate income from these sites.

But it was all short lived.

Why?

Because I bought links. And eventually Google penalized all of those sites.

If I never purchased links, those sites would have taken longer to rank, but they would have been around today, and I would have generated more income overall.

Don’t buy links, it’s bad and shortsighted.

Lesson #13: Guest post to build a brand, not to build links

I already covered the importance of branding above.

A great way to build your brand and indirectly boost your SEO traffic is through guest posting.

It’s pretty easy to spot a guest post for both a human and algorithm…

But if you are using it to build a brand, great. Focus on the content quality and not links.

Lesson #14: Don’t forget to interlink

Do you know what some of my highest ranked pages are?

The ones that are interlinked.

It takes anywhere from 6 months to a year for many of the interlinks to kick in, but it is still effective none-the-less.

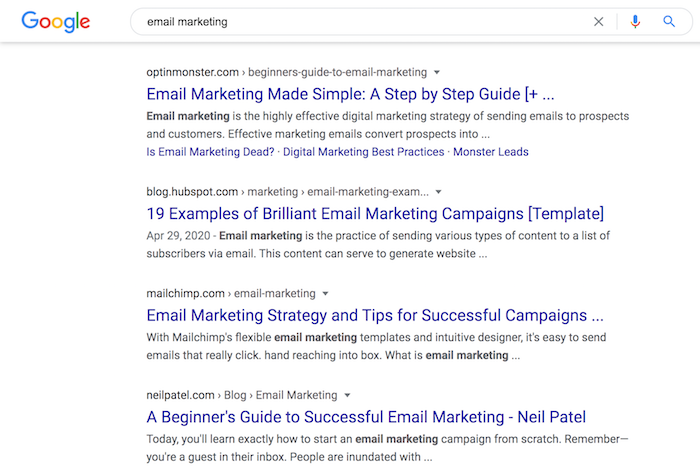

Every time I wrote content, I used to make sure I link out to my older pieces of content when it made sense. But I made a big mistake… I wasn’t going into my older pieces of content and then adding links to my newer pieces of content.

That one change was game-changing for me. It took time to see the results but it worked exceptionally well.

It’s how I rank high for terms like “email marketing”.

Lesson #15: Google isn’t the only game in town

Although Google is the most popular search engine, it isn’t the only one you need to focus on.

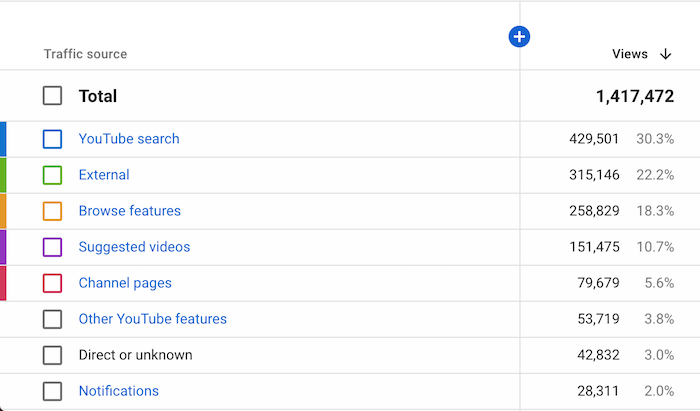

Did you know that YouTube is the second most popular search engine?

Focus on writing high-quality content. It’s why I blog less and try to make my content amazing.

Lesson #18: Tools are better than content marketing

I used to focus all of my energy on content marketing because it drove a lot of links and SEO traffic.

But over time, I realized that creating free tools builds more natural links than anything else I have ever tested.

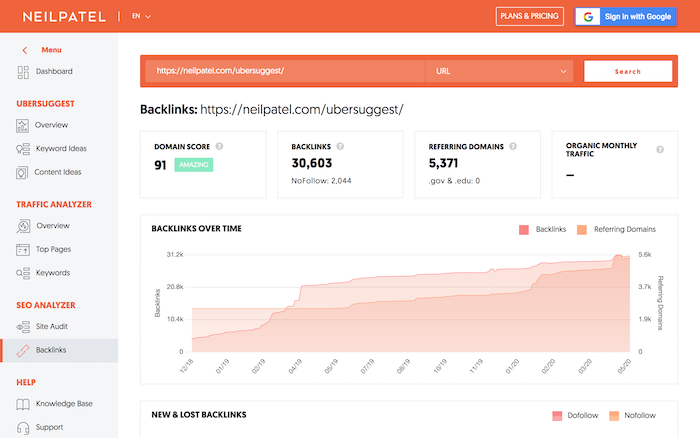

Just look at Ubersuggest. I spent years creating it and look at how many links it has generated…

30,603 backlinks! That’s a lot of links.

If you don’t have the resources to build a custom tool like me, you can always start with buying a white label tool from Code Canyon for $10 or $20. They literally have tools for almost all industries.

Lesson #19: Don’t rely only on SEO

When I first got started in SEO, all I could think about was SEO.

To me, it was the best marketing channel out there because it allowed me to compete with large companies.

Even to this day, I still love SEO more than any other channel.

But it doesn’t stop me from leveraging other marketing channels.

See, years ago you could build a business off of one marketing channel.

Yelp was built through SEO. Dropbox through social media referrals. Facebook through email invites…

Those days don’t exist anymore. You can’t just build your traffic from one channel.

Although you should do SEO, you should also try paid ads, social media marketing, email marketing, push notifications, and anything else that comes out.

Diversify your traffic sources and don’t just rely solely on SEO.

Lesson #20: People love linking to data

Spending money and time to gather your own unique data is an easy way to build links.

Within a two-year period, from 2010 to 2012, 47 infographics generated 2,512,596 visitors and 41,142 backlinks from 3,741 unique domains. They also generated 41,359 tweets and 20,859 likes.

If you don’t have money to hire a designer, you can use Infogram or Canva to create one on your own.

Lesson #22: Google doesn’t penalize for duplicate content

You don’t want to post tons of duplicate content on your site as it’s not the best user experience, but keep in mind that Google doesn’t penalize you for duplication.

They may not just rank the duplicate content as well.

So, if you spend all of this time producing amazing, unique content, why not publish it FIRST on your own website.

Then after a few hours or days if you want to be safe, take that exact content and publish it on Facebook, LinkedIn, and anywhere else that will accept your content.

Literally, take all of the words and paste them onto those social channels.

It will get you extra awareness and branding. Plus, the content should already be indexed on your site, so Google knows it came from your first… and I doubt you care if the duplicated version on LinkedIn ranks. That’s still great branding.

In other words, don’t be afraid to repurpose your content even if it causes duplication.

Just look at this post, for example. I’m also repurposing it into a 4-part podcast series.

Lesson #23: Don’t recreate the wheel

I used to spend hours a week doing keyword research trying to figure out what new terms to rank for.

Eventually, I figured out an easier and better way to find new content topics and keywords to go after.

Go to Ubersuggest, type in your competitor’s domain name and hit search.

In the left-hand navigation click on Top Pages.

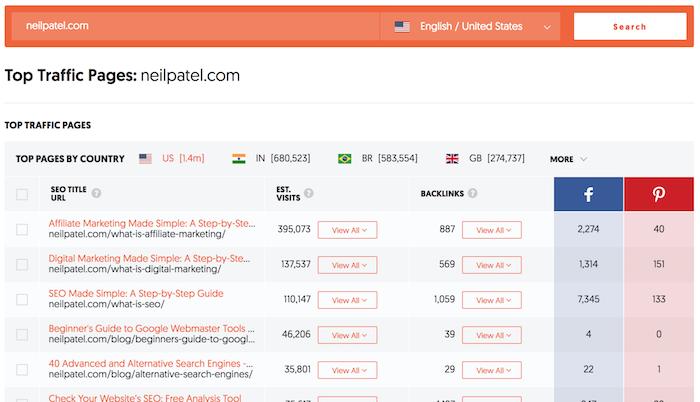

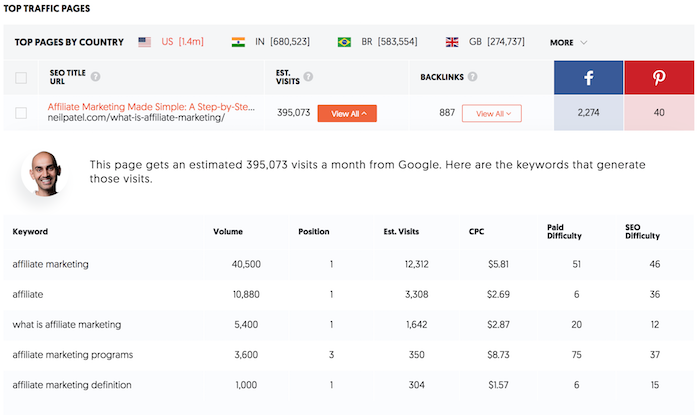

You’ll see a report that shows you all of the popular pages on your competition’s website. This will give you ideas for the type of pages you should create on your website.

Then I want you to click “View All” under Est. Visits (estimated visits). This will show you all of the keywords that drive traffic to that page.

You now have a list of topics and keywords for each topic to go after.

Lesson #24: Don’t pick a generic domain name

Remember how in Lesson 11 I talked about brand queries and how they helped rankings?

After I learned that, I decided to go buy exact match domain names where the domain name was the keyword.

That way I would get lots of brand queries without trying.

Well, there’s an issue… even if you rank high, what you’ll find is you will have a low click-through rate in most cases.

If you have a low click-through rate, it tells Google your brand isn’t strong and people don’t prefer it, which can hurt your ranking.

So instead of focusing on exact match domains, unless you have millions to spend on branding like Hotels.com, focus on building a memorable brand.

Pick something that is unique, easy to spell, and easy to remember.

Lesson #25: Learn from blackhat SEOs, but don’t go over to the dark side

Blackhat SEOs come up with some interesting data and experiments.

Many of them don’t work for long, but they are interesting none-the-less.

Although I don’t recommend practicing blackhat SEO, I do recommend following them.

The easiest way you can learn from them is by reading Blackhat World.

People there share some interesting insights, especially every time there is a major Google algorithm update.

Again, I don’t recommend practicing blackhat SEO, but following them may help you uncover “white hat” techniques that can increase your rankings. Not everything they do is bad… many of them use legitimate tactics as well.

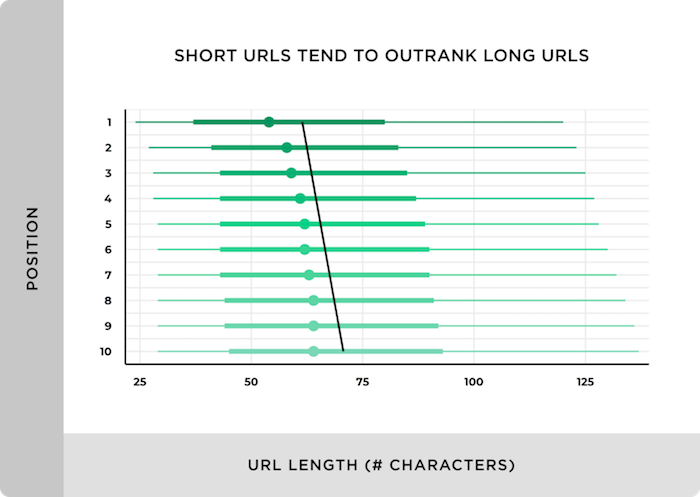

Lesson #26: Short URLs rank better than long ones

My URLs used to be the title of my blog post.

For example, with this post I would have used this URL in the past…

URLs at position #1 are on average 9.2 characters shorter than URLs that rank in position #10. So, keep them short.

Lesson #27: The power’s in the list

If you want your content to rank high on Google, you need more people to see it.

Whether it is from social shares, or from push notifications or email blasts… the more people that see your content, the more engagement it will get, and the more people that will link to it.

I used to do a ton of manual outreach every time I published a new blog post and I would email people asking them to link to me.

And it works, it’s just time consuming and a pain.

These days, I have a better strategy… send out an email blast every time I publish a new post.

I can now get anywhere from 20,000 to 50,000 clicks per email I send out.

Now of course you won’t get that from day one as it took me years to build up my email list.

But you can start today by collecting emails. You can easily do that through Hello Bar.

And as your list grows, so will the clicks to your blog and the number of links you get, which in turn will increase your rankings.

Lesson #28: Don’t let your foot off the peddle

This was one of the hardest lessons I learned.

It’s exhausting to continually blog and do your own SEO. Sometimes you just want a break.

With my old blog, Quick Sprout, I used to publish 12 blog posts a month and I did that consistently for 3 years.

One day I decided that I wanted to stop for a month. So, I took a 30-day break.

Guess what happened to my traffic?

It tanked by 32%.

So, then I started blogging again. And guessed what happened to my traffic after I started blogging?

It didn’t come right back.

It took me 3 months to get back to where I was.

When things are working for you, don’t slow down. Keep pushing harder, even if you are exhausted. Because the moment you stop, you’ll drop, and it is a lot of work to get back to where you were.

Lesson #29: The best SEO advice comes from conferences

The best SEO advice I have ever learned over the years has come from conferences.

And no, I don’t mean by sitting in on the sessions, although you can learn from those too.

The best SEO secrets and advice I learned came from networking. When you go to these conferences, hundreds if not thousands of other SEOs are there. And when you go to the bar after hours and mingle with people, you’ll quickly pick stuff up.

You’ll be shocked at what people tell you. It’s how I learned a lot of the good tactics that I still use today.

Lesson #30: Never stop learning

This one may sound obvious but when things are going well, people get complacent.

Just think about that for a bit… that’s roughly 9 algorithm updates per day.

Because they are changing so quickly, you won’t survive if you don’t stay up to date.

Yes, the ideal strategy is to do what’s best for your users or visitors as in the long run, Google wants to promote those sites, but it doesn’t mean that you can ignore the changes happening in the industry.

Read all of the SEO blogs out there, attend conferences as I mentioned above… experiment on test sites… push yourself to be better.

That drive of always improving and always wanting to learn more has helped me tremendously. It’s one of the reasons for my growth in rankings over the years.

Conclusion

There are a lot of lessons that you will learn as your rankings grow and as you spend more time on SEO.

But hopefully, you don’t have to waste time and go through the same mistakes I made. You don’t want to learn these lessons the hard way.

That’s why I decided to share them. I want to save you the time and help you achieve your traffic goals faster.

Secured – Those guaranteed under the regards to an insurance coverage. Advantage – The cash paid to the insurance policy holder when a case is made. Proposal Price – The asking price or cash-in worth of your device holdings. Bonus offer – Relates to a with-profits plan. The quantity is reliant upon the earnings made by the insurance coverage business. Exchangeable Term Assurance – A term insurance plan which provides you the choice to transform your existing plan to a whole-life or endowment insurance plan, without needing to take more medical checkups. Vital Illness Insurance – A plan that pays a round figure on the medical diagnosis of harmful diseases suggested in the regards to the strategy. Reducing Term – A kind of term life insurance policy where the fatality advantage lowers each year as per your plan. This kind of certification is often marketed as home mortgage insurance policy. Endowment Insurance – An insurance coverage that pays a specified quantity at the end of a given duration or upon the fatality of the guaranteed if it happens within that duration. Family Members Income Benefit – Term guarantee which pays cash to the life ensured’s dependants for a collection duration, instead of paying a round figure. Surefire Bond – A bond in which principal as well as passion are ensured by an entity besides the company. Surefire Bonds can be earnings or development. Enhancing Term – The quantity as well as the cover you pay right into the plan are boosted by a certain percent yearly relied on the initial amount guaranteed. Created as a method to raise your life cover as your revenues rise. Financial Investment Bond – Combines financial investment with some life cover. The settlements you make right into an insurance coverage plan or financial investment bond, normally a swelling amount, are spent in the insurance coverage firm’s with-profits or unit-linked funds (Life Funds). Life Fund – This typically refers to Unit connected Investment Funds. Such funds are utilized for people holding life guarantee plans to spend in. Maturation – A concurred day when an endowment plan finishes as well as the profits, consisting of any type of bonus offers, are payable. Shared – A life insurance policy business that is possessed by its with-profits insurance holders. Deal Price – The cost at which fund devices are purchased. Costs – The quantity of cash paid right into an insurance plan. Exclusive – A life insurance policy firm that releases its revenues to its investors. Certifying Policy – A life guarantee based financial savings prepare that needs to be composed for a minimum of 10 years as well as need to satisfy specific certifying plan requirements to guarantee the last payment is free of tax. Eco-friendly Term – Term Insurance that might be restored for one more term without proof of insurability. Solitary Premium Policy – Where a solitary round figure is spent for an insurance coverage. Amount Insured – The quantity of cash that is ensured to be paid under an insurance coverage, prior to any type of bonus offers are included. Give up Value – Not appropriate to all life insurance policy plans. When he or she stops insurance coverage, the quantity that an insurance coverage policyholder is qualified to get Term Insurance – Provides insurance holder with security just. Life insurance policy payable to a recipient just when an insured passes away within a defined number of years (the term). Incurable Bonus – This is an additional perk figured out when a fatality or maturation insurance claim is paid. If the plan has actually been in-force for a minimal number of years at insurance claim time, incurable reward is usually only paid. The quantity depends on the revenues made by the insurer. A kind of Life Fund that can spend in UK as well as abroad shares, home, dealt with rate of interest protections and also cash money. When you spend in this fund via an insurance coverage plan, you acquire ‘systems’. If your insurance coverage plan is unit-linked, some of your cash is made use of to acquire ‘systems’ in a fund. Usually refers to plans that provide security as well as conserving such as endowment insurance coverage, entire life insurance policy as well as financial investment bonds. Unit-Linked Single Premium Bond – A solitary round figure life insurance policy plan where your financial investment is topped a variety of Life Funds. Whole Life Insurance – Whole life insurance policy gives a survivor benefit for the insurance policy holder as it develops money worth. The plan continues to be active for the life time of the guaranteed, as long as costs are paid according to the plan arrangement. You can select insurance policy that pays on fatality an assured amount just, the amount plus any kind of incentives that have actually been included, or the amount plus any type of extra worth from the development of the funds purchased. Without Profits – When a plan gets to maturation or the insurance policy holder passes away, the quantity paid is the fundamental ensured amount just. You would certainly not be qualified to any type of incentives. With Profits – Relates to insurance policy plans that integrate financial investment with security. This kind of plan is qualified to a share of the revenues made by the insurance policy firm. With Profits Bond – An insurance coverage where your round figure remains in a lot of instances purchased a Unitised With Profits Fund (which is detailed under the Life Funds area).

Lowering Term – A type of term life insurance coverage where the fatality advantage reduces each year as per your plan. The repayments you make right into an insurance coverage plan or financial investment bond, generally a swelling amount, are spent in the insurance policy business’s with-profits or unit-linked funds (Life Funds). When you spend in this fund via an insurance coverage plan, you acquire ‘devices’. Normally refers to plans that supply security as well as conserving such as endowment insurance policy, entire life insurance policy as well as financial investment bonds. Whole Life Insurance – Whole life insurance policy supplies a fatality advantage for the insurance holder as it constructs up money worth.

Hi, I am Can. I am a career changer Front-End Developer currently studying to be a Full-Stack (MERN) Developer, previously team leader, and Helicopter Pilot. I am looking for my first developer job.

Check my projects on GitHub and portfolio website. If you are interested, please do drop me a line!

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.