ESI Group | Software development engineer | San Diego, CA | Full-time | Onsite preferred post-Covid

ESI Group is currently seeking a software development engineer to work in our San Diego office. We are a small team with diverse backgrounds focused on developing desktop software applications in the field of vibro-acoustics simulation. Our clients include NASA, Boeing, Airbus, GM, and Ford.

We are looking for a developer with a Bachelors/Masters degree in the Sciences or Engineering. The successful candidate must have excellent C++ skills. We also use Python, Qt, MFC and CMake to develop our applications. We use GitLab as our version-control platform with continuous-integration, unit testing and package management via Conan, to complete our DevOps toolkit. We create UI wireframes and write product specifications to refine our development requirements. Many of our team members are skilled in numerical methods and high performance computing.

Being a small team, you’ll enjoy a high level of autonomy and the ability to influence new products and features on several levels. You’ll learn from our wealth of pooled knowledge and share your expertise in return. The office setting is casual, and we all enjoy the freedom of flex-time schedules.

Please contact Tracy at ext-tracy.sidall@esi-group.com with any questions you may have relating to the position or company. Don’t forget to mention HN in the email.

Covid-19 has turned the world topsy turvy. There is no way around it. Most businesses need a little extra financial cushion at the very least. Most need much more than that. What happens in this post COVID-19 economy is literally unfolding as we watch. A commercial line of credit could be just the thing to keep your business going during a recession.

Get a Commercial Line of Credit Fast

The thing is, most business owners need money right now. That means you need the fastest, most cost-effective commercial line of credit that you can get. Why a line of credit rather than a loan? There are a few reasons, but one main reason.

Commercial Line of Credit vs. Loan

The most basic definition of a commercial line of credit is that it is a revolving credit, similar to a credit card. You have a limit and continuous access to that limit while making payments only on the portion you use each month.

For example, if you have a $10,000 line of credit, you can use however much of those funds you need each month for whatever you want, unless your lender issues some sort of restriction. If you use $2,000, then when you get your statement you will have to pay $2,000 plus the interest, rather than a payment plus interest on the entire amount of the loan.

If you were to pay $1,000, then spend another $500, you would pay on the $1,500 balance the next month. Your payments change as your balance changes. Just like with a credit card.

What is the advantage of a line of credit over a term loan? Flexibility, hands down. With a line of credit, you do not have to repay or pay interest on any amount that you do not use. You have access to the funds as needed, but you do not have to repay the entire amount unless you use the entire amount.

Now, you’re probably thinking that credit cards are super easy to get, and they work the same way. It’s revolving credit. You only use what you need. You only pay back what you need.

Why is one better than the other? In some cases, a credit card may be the better option. This is a choice to make based on several different factors.

The main difference between the two that most borrowers need to know is that a line of credit typically has a lower consistent interest rate. However, there are no perks like 0% interest or cash back that you sometimes see with credit cards.

Another benefit with a credit card is that it is typically unsecured credit, meaning you do not have to have collateral. Many credit lines do require security, or collateral.

Middle Ground: Credit Line Hybrid

There is middle ground between unsecured and secured credit, and between a commercial credit line and credit cards. It’s called a credit line hybrid. A credit line hybrid is revolving, unsecured financing that allows you to fund your business without putting up collateral, and you only pay back what you use. It’s quickly accessible, lower interest, and high limit. It’s the best of both worlds.

Who Qualifies for this Type of Commercial Line of Credit?

Who qualifies for a credit line hybrid? Well, if you have a personal credit score of at least 685, you’re off to a good start. In addition, you can’t have any liens, judgments, bankruptcies or late payments. Furthermore, in the past 6 months you should have less than 5 credit inquiries, and you should have less than a 45% balance on all business and personal credit cards. It’s also preferred that you have established business credit as well as personal credit.

If you do not meet all of the requirements, it’s okay. You can take on a credit partner that meets each of these requirements. Many business owners work with a friend or relative to fund their business. If a relative or a friend meets all of these requirements, they can partner with you to allow you to tap into their credit to access funding.

What are the Benefits of This Type of Commercial Line of Credit?

There are many benefits to using a credit line hybrid. First, as already mentioned, it is unsecured. That means you do not have to have any collateral to put up. Next, the funding is “no-doc.” You do not have to provide any bank statements or financials.

Not only that, but typically approval is up to 5x that of the highest credit limit on the personal credit report. Furthermore, frequently you can get interest rates as low as 0% for the first few months, allowing you to put that savings back into your business.

The process is pretty fast, especially with a qualified expert to walk you through it. One other benefit is this. With the approval for multiple credit cards, competition is created. That means it’s likely if you handle the credit responsibly, that you can get interest rates lowered and limits raised every few months.

Private Lenders: Another Way to Get a Commercial Line of Credit Fast

Private lenders generally operate online. They typically offer lines of credit to those with credit scores that are lower than what is generally required by traditional banks. In addition, often you can get the funds within a few days of application, rather than a few weeks. Here are a few examples.

Kabbage

Kabbage offers a credit line of up to $150,000 with no credit score required. The catch is that the interest rate is between 32 and 108%. The business must have been in existence for at least one year and have revenue of at least $50,000.

Due to the extremely high interest rate, this is really only an option for those businesses that cannot get financing due to a low or nonexistent credit score and need something immediately.

StreetShares

The credit line that StreetShares offers goes up to $100,000 for those who have a business credit score of at least 600. You also have to have been in business for at least one year, and have at least $25,000 in revenue. It requires weekly repayment.

This is a good option for smaller businesses that are okay in the credit department but have trouble meeting higher revenue criteria. Also, the interest rate minimum is lower than some. The low end at 9%.

OnDeck

If you have a credit score of at least 600 you can get a credit line of up to $100,000 with OnDeck . The interest rate is a little higher than some that require a higher credit score minimum. It ranges from 13.99 to 39.99 percent.

Again, due to the higher interest rate, this should only be an option if you cannot meet the higher credit score requirement with a lender that offers a lower interest rate.

The credit line at Lending Club goes up to $300,000. It requires a credit score of 600, at least one year in business, and $50,000 or more in revenue. The repayment term is 25 months. In addition, they require collateral for limits over $100,000.

This is a good option for those who meet the requirement as there is a higher limit available with collateral, and the interest rate can go as low as 6.25%. Also, the repayment terms are more manageable.

Credit Card Options

Of course, while not the perfect solution, credit cards are an option. You have to be careful, and you want to research to ensure you get the best rates and terms possible. Here are some to start with.

Brex Card for Startups

The Brex Card has no yearly fee. Also, you will not need a personal guarantee. However, this card does not work for every industry.

To determine creditworthiness, Brex checks a company’s cash balance, spending patterns, and investors. Rewards include 7x points on rideshare and 4x on Brex Travel. Also, you can get triple points on restaurants and get double points on recurring software payments. Get 1x points on everything else.

Capital One® Spark® Classic for Business

The Capital One® Spark® Classic for Business is another good one to consider. It has no annual fee, but there is also no introductory APR offer. The regular APR is a variable 24.49%. However, you can get unlimited 1% cash back on every purchase for your company and there is no minimum to redeem.

While this card is within reach if you have fair credit scores, beware of the APR. If you can pay promptly, and completely, it’s a good deal.

Ink Business Unlimited℠ Credit Card

The Ink Business Unlimited℠ Credit Card has no annual fee and a 0% introductory APR. After that expires, the APR is a variable 14.74 to 20.74%.

Earn unlimited 1.5% cash back rewards on every purchase made for your company and get $500 bonus cash back after spending $3,000 in the initial 3 months from account opening. Rewards rewards for cash back, gift cards, travel and more using Chase Ultimate Rewards®. You will need superb credit to get approval for this card.

Blue Business® Plus Credit Card from American Express

Get double Membership Rewards® points on everyday business purchases like office supplies or client dinners. This applies to the first $50,000 spent each year. You get 1 point per dollar after that. Your credit has to be really good to qualify.

American Express® Blue Business Cash Card

Another one to check out is the American Express® Blue Business Cash Card. It is identical to the Blue Business® Plus Credit Card from American Express. However its rewards are in cash instead of points. You get 2% cash back on all eligible purchases up to $50,000 per calendar year. After that, it’s 1%.

There is no yearly fee, and there is a 0% introductory APR for the first one year. Afterwards, the APR is a variable 14.74 to 20.74%. You will need awesome credit to qualify for this card.

The Capital One® Spark® Cash for Business card is another great option. It has an introductory $0 annual fee for the first year. After that, it costs $95 per year. There is no introductory APR deal. The regular APR is a variable 18.49%.

You can get a $500 one-time cash bonus after spending $4,000 in the first 3 months from account opening. Also, you get unlimited 2% cash back. YOu can rRedeem any time without any minimums. You will need fabulous credit scores to qualify.

Discover it® Business Card

Another good one is the Discover it® Business Card. It has no yearly fee. There is an introductory APR of 0% on purchases for twelve months. Then, the regular APR is a variable 14.49 to 22.49%.

You get unlimited 1.5% cash back on all purchases, with no category restrictions or bonuses. Also, they double the 1.5% Cashback Match™ at the end of the first year. There is no minimum spend requirement either.

You can download transactions easily to Quicken, QuickBooks, and Excel. This one also requires great credit scores.

The thing with credit cards is, you have to be so careful. As with all debt, payments must be made on time. However, the higher interest rates make this a little harder than it typically is with a commercial line of credit.

A Commercial Line of Credit Can Help You Right Now

In this post COVID world, most business owners need money fast. A commercial line of credit is the best way for that to happen, especially if you can get a credit line hybrid. Truly, with the ability to use a credit partner, virtually everyone can access this type of funding. It’s low interest, high limit, fast access to the funds you need to make sure your business thrives regardless of the state of the economy.

Will Our Fundation Group LLC Recession Funding Review Help Satisfy Your Need for Business Funding? We Put It to the Test

Fundation Group LLC is one of many lending companies online. They provide term loans and lines of credit. Foundation confirmed the information we found about them online. We look at the specifics and drill down into the details. So check out our Fundation Group LLC recession funding review.

Fundation Group LLC Recession Funding Review: Background

Fundation Group LLC is located online here: http://www.fundation.com/. Their physical address is located in Reston, VA. Plus you can call them at: (888) 390-0064. So their contact page is here: https://fundation.com/about/.

Their capital base has come from Goldman Sachs; Garrison Investment Group; and Midcap Financial, LLC.

Fundation Group LLC Recession Funding Review: Term Loans

Funding as soon as one business day. Up to $500,000 is available; terms go up to 4 years. Payments are twice per month. No specific collateral is needed. They want a personal guarantee. Fundation will take out a UCC-1 blanket lien for most borrowers.

They do not seem to have a time in business requirement anymore. Fundation also does not seem to have an annual revenue or personal credit requirement anymore.

Fundation Group LLC Recession Funding Review: Fees

Rates are risk-based; the higher the risk, the higher the rate.

Interest rates are not listed; they will be determined based on several factors. There are no prepayment fees.

Cost of Loans

Several factors are considered when Fundation decides on the cost of a loan. These factors include time in business and seasonality. They also include financial metrics. So these metrics include profit margin and amount of debt.

Fundation Group LLC Recession Funding Review: Lines of Credit

Up to $150,000 is available. The new balance after each draw is amortized in equal installments over 18 months. Payments are monthly. No specific collateral is needed. They want a personal guarantee. Fundation will take out a UCC-1 blanket lien for most borrowers.

They do not seem to have a time in business requirement anymore. Fundation also does not seem to have an annual revenue or personal credit requirement anymore.

Fundation Group LLC Recession Funding Review: Fees

There are no prepayment fees. Just pay the outstanding balance plus accrued interest if you prepay

your loan or line of credit.

Keep your business protected with our professional business credit monitoring. It’s a worthwhile investment, saving you money even during a recession.

Fundation Group LLC Recession Funding Review: Advantages

Advantages include no apparent time in business requirement. Their maximum loan amount is fairly high.

Fundation Group LLC Recession Funding Review: Disadvantages

Disadvantages are they want personal guarantees for pretty much everything and will take out a UCC blanket lien.

A Fantastic Alternative – Establishing Business Credit

Business credit is credit in a small business’s name. It doesn’t attach to an owner’s individual credit, not even when the owner is a sole proprietor and the solitary employee of the small business.

As such, a business owner’s business and individual credit scores can be very different.

The Advantages

Because business credit is distinct from personal, it helps to protect a small business owner’s personal assets, in case of a lawsuit or business bankruptcy.

Also, with two distinct credit scores, a small business owner can get two different cards from the same merchant. This effectively doubles buying power.

Another benefit is that even startup ventures can do this. Visiting a bank for a business loan can be a formula for disappointment. But building small business credit, when done right, is a plan for success.

Personal credit scores depend upon payments but also other factors like credit utilization percentages.

But for small business credit, the scores actually only depend on whether a business pays its invoices punctually.

The Process

Establishing company credit is a process, and it does not occur without effort. A company has to actively work to establish company credit.

However, it can be done readily and quickly, and it is much quicker than establishing consumer credit scores.

Vendors are a big aspect of this process.

Performing the steps out of sequence will cause repetitive denials. Nobody can start at the top with small business credit. For example, you can’t start with retail or cash credit from your bank. If you do, you’ll get a rejection 100% of the time.

Business Fundability

A company must be fundable to credit issuers and vendors.

For that reason, a company will need a professional-looking web site and e-mail address. And it needs to have site hosting from a company like GoDaddy.

And, company phone and fax numbers must have a listing on ListYourself.net.

In addition, the company telephone number should be toll-free (800 exchange or the equivalent).

A small business will also need a bank account devoted strictly to it, and it needs to have all of the licenses essential for operation.

Licenses

These licenses all must be in the perfect, appropriate name of the company. And they must have the same business address and phone numbers.

So keep in mind, that this means not just state licenses, but potentially also city licenses.

Keep your business protected with our professional business credit monitoring. It’s a worthwhile investment, saving you money even during a recession.

Dealing with the Internal Revenue Service

Visit the IRS web site and acquire an EIN for the small business. They’re totally free. Select a business entity such as corporation, LLC, etc.

A company can get started as a sole proprietor. But they will most likely wish to switch to a kind of corporation or an LLC.

This is in order to minimize risk. And it will make best use of tax benefits.

A business entity will matter when it pertains to tax obligations and liability in case of litigation. A sole proprietorship means the business owner is it when it comes to liability and taxes. No one else is responsible.

Sole Proprietors Take Note

If you operate a company as a sole proprietor, then at least be sure to file for a DBA. This is ‘doing business as’ status.

If you do not, then your personal name is the same as the small business name. Therefore, you can end up being directly responsible for all small business debts.

Plus, according to the Internal Revenue Service, by having this arrangement there is a 1 in 7 probability of an IRS audit. There is a 1 in 50 probability for corporations! Prevent confusion and noticeably reduce the chances of an IRS audit at the same time.

Setting off the Business Credit Reporting Process

Begin at the D&B web site and obtain a totally free D-U-N-S number. A D-U-N-S number is how D&B gets a business into their system, to produce a PAYDEX score. If there is no D-U-N-S number, then there is no record and no PAYDEX score.

Once in D&B’s system, search Equifax and Experian’s websites for the company. You can do this at www.creditsuite.com/reports. If there is a record with them, check it for accuracy and completeness. If there are no records with them, go to the next step in the process.

By doing this, Experian and Equifax will have something to report on.

Vendor Credit

First you must build trade lines that report. This is also referred to as vendor credit. Then you’ll have an established credit profile, and you’ll get a business credit score.

And with an established business credit profile and score you can begin to get retail and cash credit.

These sorts of accounts have the tendency to be for the things bought all the time, like marketing materials, shipping boxes, outdoor work wear, ink and toner, and office furniture.

But first off, what is trade credit? These trade lines are credit issuers who will give you initial credit when you have none now. Terms are often Net 30, rather than revolving.

So, if you get approval for $1,000 in vendor credit and use all of it, you must pay that money back in a set term, such as within 30 days on a Net 30 account.

Keep your business protected with our professional business credit monitoring. It’s a worthwhile investment, saving you money even during a recession.

Retail Credit

Once there are 3 or more vendor trade accounts reporting to at least one of the CRAs, then move onto retail credit. These are companies like Office Depot and Staples.

Just use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, use the business’s EIN on these credit applications.

Fleet Credit

Are there more accounts reporting? Then move to fleet credit. These are companies like BP and Conoco. Use this credit to buy fuel, and to fix and maintain vehicles. Just use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, make sure to apply using the company’s EIN.

Cash Credit

Have you been sensibly handling the credit you’ve up to this point? Then progress to more universal cash credit. These are companies such as Visa and MasterCard. Just use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, use your EIN instead.

These are frequently MasterCard credit cards. If you have more trade accounts reporting, then these are doable.

Monitor Your Business Credit

Know what is happening with your credit. Make certain it is being reported and deal with any mistakes ASAP. Get in the practice of taking a look at credit reports. Dig into the particulars, not just the scores.

Update the details if there are inaccuracies or the details is incomplete.

Fix Your Business Credit

So, what’s all this monitoring for? It’s to contest any mistakes in your records. Mistakes in your credit report(s) can be corrected. But the CRAs normally want you to dispute in a particular way.

Disputes

Disputing credit report errors typically means you send a paper letter with duplicates of any proofs of payment with it. These are documents like receipts and cancelled checks. Never send the originals. Always send copies and retain the original copies.

Fixing credit report inaccuracies also means you precisely itemize any charges you contest. Make your dispute letter as understandable as possible. Be specific about the issues with your report. Use certified mail so that you will have proof that you sent in your dispute.

A Word about Building Business Credit

Always use credit responsibly! Don’t borrow beyond what you can pay off. Track balances and deadlines for repayments. Paying punctually and fully will do more to boost business credit scores than pretty much anything else.

Building business credit pays. Great business credit scores help a business get loans. Your credit issuer knows the business can pay its financial obligations. They know the company is bona fide.

The business’s EIN attaches to high scores and loan providers won’t feel the need to demand a personal guarantee.

Business credit is an asset which can help your business for years to come. Learn more here and get started toward growing company credit.

Fundation Group LLC Recession Funding Review: Upshot

A company needing higher amounts will likely do better with Fundation. But there are negatives.

Entrepreneurs will find they have to give up a personal guarantee and, on top of that, have a UCC blanket lien held by Fundation. A company that fails and ends up going out of business could be particularly harsh for an entrepreneur – so companies which are unsure of the chances of their success would do well to seek out other types of funding, where they either hand over a personal guarantee or a UCC blanket lien but not both.

And finally, as with every other lending program, whether online or offline, always remember to read the fine print and do the math. Go over the details with a fine-toothed comb, and decide whether this option will be good for you and your company. In addition, consider alternative financing options that go beyond lending, including building business credit, in order to best decide how to get the money you need to help your business grow.

Disclosure: This content is reader-supported, which means if you click on some of our links that we may earn a commission.

Unless you’re independently wealthy, most small business owners need a loan at one point or another. From paying for startup costs to expansion projects, equipment, or unexpected incidents, quick access to funding will make it easier for your company to grow.

Whether you’re launching a brand new venture or own an established business, there are so many different small business lending options out there to consider.

Which small business loan is best for you? This guide contains everything you need to know on the subject.

How to Choose the Best Small Business Loans For You

Small business loans come in all different shapes and sizes. So as you’re evaluating different options, there are specific considerations that must be examined. I’ll explain each one in greater detail below.

Lender

When most people think about getting a loan, they automatically assume that a bank is their only option. But in addition to small local banks and national bank chains, there are lots of other lenders that can provide your small business with capital.

You can explore credit unions, crowdfunding sites, P2P lenders, loan marketplaces, nonprofit lenders, and even alternative lending solutions.

The qualification requirements and loan terms will vary from lender to lender.

Loan Type

Most lenders offer multiple types of loans for small business owners. Some common small business loan types include SBA loans, lines of credit, installment loans, short term loans, equipment loans, commercial real estate loans, and merchant cash advances.

In some cases, you’ll need to provide the lender with more information about what you’ll be doing with the funds. For example, an equipment loan couldn’t be used to purchase inventory, and a commercial real estate loan couldn’t be used to buy a new vehicle.

Lines of credit are great options to have since they can be used for lots of different purposes. We’ll talk more about these different loan types in greater detail shortly.

Capital Required

The loan amount you’re seeking also needs to be taken into consideration. There’s a big difference between $5,000, $50,000, and $5 million.

Certain lenders are better for microloans and small amounts, while others are known for lending large sums of cash.

Take a look at the minimum and maximum amounts available before you apply for a loan. Generally speaking, you shouldn’t apply for more than you need (unless it’s a line of credit). Otherwise, you’ll have higher interest payments.

Minimum Qualifications

In most cases, you won’t qualify for every type of loan. So pay close attention to these terms before you apply, or you’ll just be wasting your time (and potentially hurt your credit).

Some lenders will only loan money to companies that have been in business for a certain number of years. There are also some cash flow requirements, annual revenue requirements, and business owner credit score requirements for certain loans.

Loan Terms

The loan terms are crucial when you’re evaluating different options. How soon will you need to pay the money back? What interest rates will you be paying?

Make sure you look beyond the dollar amount and take a deeper look at the terms.

Businesses with bad credit won’t have access to the lowest interest rates and loan terms. So you’ll definitely want to shop around until you’re comfortable with the options presented to you.

The Different Types of Small Business Loans

There are tons of different small business loans out there. But I want to quickly highlight the most popular options to give you a better understanding of how they work.

SBA Loan

SBA loans are backed by the Small Business Administration. This federal agency helps businesses gain access to better funding resources.

These loan amounts typically range from $50,000 to $5 million with terms from 10-25 years.

SBA loans usually have great rates (since the SBA reduces the lender’s risk), but they can be tough to qualify for. The process to apply and get approved for an SBA loan can be slow.

Business Line of Credit

Lines of credit are great for those of you who need flexibility. Instead of receiving a lump sum of cash, you can borrow up to your credit amount as needed.

Business lines of credit can range anywhere from $1,000 up to $500,000.

It’s usually easy to qualify for a line of credit if you’ve been in business for more than a year and have $50,000+ in annual revenue. Interest rates vary based on the lender, your credit score, and other qualification terms. But you’ll only pay interest on the amount you borrow on the revolving line.

Term Loan

Term loans are funded quickly. In some instances, you can receive cash within 24 hours of getting approved. It’s common for term loans to be used for working capital, equipment, operations, and more.

Some of these loans are short term and must be paid back as early as 12-24 weeks. Others have repayment terms in the 1-5 year range.

Term loans typically have fixed interest rates or flat fees, so your payments won’t increase throughout the lifetime of the loan.

Merchant Cash Advance

With a merchant cash advance program, small businesses can borrow against future earrings to secure capital. These loans are repaid with a daily percentage of your credit card sales, as previously agreed upon with the lender.

Most merchant cash advances can be used for a wide range of needs. Similar to a term loan, you can usually get access to funds quickly as well.

It’s easy to get approved for a merchant cash advance, but the interest rates are usually high.

Equipment Financing

The name is pretty self-explanatory here—the money from equipment financing must be used to purchase equipment. But it’s worth noting that the term “equipment” is pretty broad.

In addition to things like conveyor belts, forklifts, and machinery, other types of equipment like accounting software, or payment processing systems would also fall into this category.

Equipment financing is usually secured by the equipment you’re purchasing. If you fail to repay the loan, the lender can seize the equipment.

Business Credit Card

Credit cards and loans are obviously not the same. But a business credit card can potentially be a great option to finance certain purchases.

Some cards offer businesses introductory promotions like 0% APR financing within the first year of opening an account. So you can potentially buy something at 0% interest by putting it on your new credit card (assuming it’s less than your credit amount). But beyond the introductory offer, credit cards will have significantly higher interest rates than other types of loans.

A secured loan requires some type of collateral in order for you to qualify. This is common for high-risk businesses. If the business defaults on the loan, the lender will seize the collateral.

Since secured loans don’t pose as much of a risk to lenders, the interest rates are usually low.

Unsecured Loans

An unsecured loan is the exact opposite of a secured loan. Businesses can borrow money without having to put up any collateral.

In order to qualify for an unsecured loan, your business usually needs to have a long track record of profitability and success without any liens or outstanding debts. If the lender thinks you’re a high risk to default on the loan, they might require you to secure the loan with collateral.

Crowdfunding Loans and P2P Loans

These types of loans are sourced from a pool of investors. You can get these loans from crowdfunding websites with small amounts collected from the general public or get them from alternative lending platforms where individuals offer P2P loans as a source of income.

If you can’t qualify for a traditional loan, you might consider a crowdfunding or P2P borrowing option.

#1 – Fundbox Review — Best For Short-Term Loans

Fundbox is used by 100,000+ businesses across a wide range of industries.

Technically, they offer business lines of credit. But the repayment period on the amount you borrow gets paid back over a 12 or 24-week plan, which falls into the short-term loan category.

Using Fundbox is simple, and you’ll get fast access to cash whenever you need it. To apply, you just need to connect your bank account and accounting software, so Fundbox can view your financials.

You’ll only pay for funds that you draw from your line of credit, so you can use Fundbox multiple times for various short-term loans. There’s no penalty for early repayments.

Before you withdraw funds, Fundbox gives you a transparent calculation of the principal, interest amount, and weekly payments due. So you can plan accordingly and know exactly how much you owe each week for the duration of the loan.

Fundbox is perfect for short-term situations when you need a little extra cash. It’s commonly used for late invoices payments, unplanned expenses, and to float small businesses during periods of slow sales.

Apply online, and get a decision within minutes. Funds can be transferred to your account as soon as the next business day.

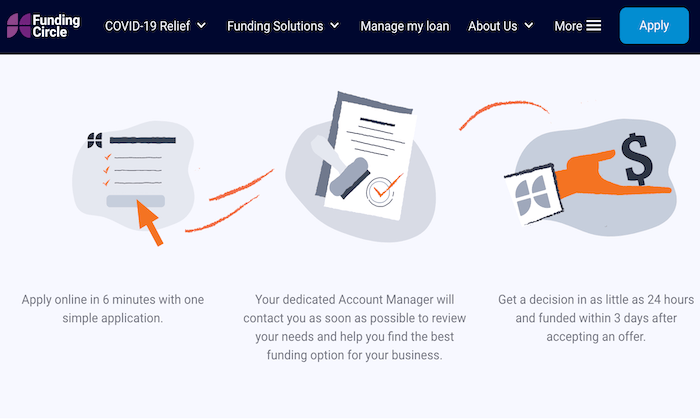

#2 – Funding Circle Review — Most Versatile Loan Options

Funding Circle is an industry leader in the small business lending category. It’s a popular choice for businesses that want fast and affordable loan options.

With a single application, Funding Circle will provide you with multiple loan types and options to choose from.

Loan types and funding solutions provided by this lender include:

SBA loans

Business term loans

Merchant cash advances

Business lines of credit

Invoice factoring

Working capital loans

You can get a decision in less than 24 hours and gain access to funds within three days of getting approved. Funding Circle has term loans from $25,000 to $500,000 and SBA loans from $20,000 to $5 million.

I also like Funding Circle because the platform makes it easy for you to manage your loan online. Apply on their website by filling out an application—it takes just six minutes to complete.

#3 – Accion Review — Best For Startups

Accion is a nonprofit organization dedicated to helping small business owners and entrepreneurs fund their startups.

In fact, Accion is the largest nonprofit lending network in the US.

Accion offers term loans of up to $250,000 at an affordable rate. You can apply online or over the phone to get a tailored solution that fits your unique needs.

Here are some of the business types that Accion commonly lends money to:

Women owned businesses

Minority owned businesses

Food and beverage businesses

Small businesses

Startups

Veteran owned businesses

Business owners with disabilities

Green businesses

Accion also has a wide range of small business resources available to help you achieve success in your industry. With 25+ years of experience in the small business lending space, I strongly recommend Accion to startups and other businesses in the categories listed above.

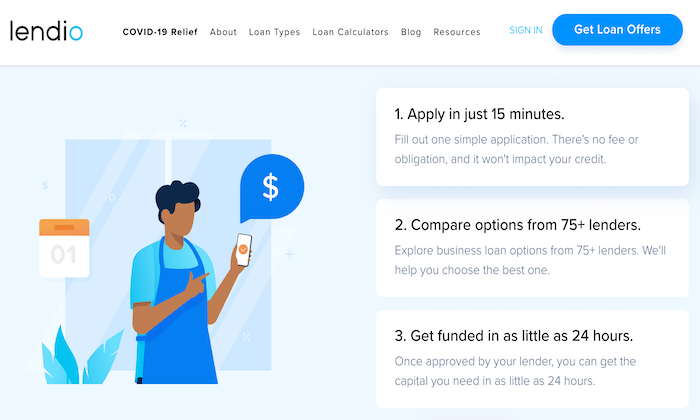

#4 – Lendio Review — Best Small Business Loan Marketplace

Lendio isn’t a small business lender. But it’s one of the most popular online marketplaces for business loans.

If you want to compare loan options from 75+ lenders with a single platform, look no further than Lendio.

This marketplace has facilitated $10+ billion in funding to 216,000+ small businesses. There is a wide range of loan types available through Lendio’s network of lenders, including:

Startup loans

Term loans

Commercial mortgages

Short term loans

SBA loans

Merchant cash advances

Business lines of credit

Business credit cards

Equipment financing

Accounts receivable financing

Business acquisition loans

I also like Lendio because they provide additional resources for small business owners, like financing calculators and bookkeeping guidance.

Just fill out some quick information about your business online to get loan offers from lenders in the Lendio network.

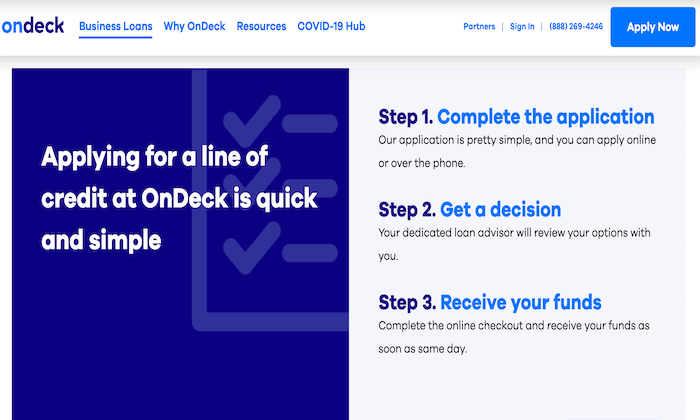

#5 – OnDeck Review — The Best For Revolving Credit

OnDeck has delivered $13+ billion to businesses across the globe. They offer term loans of up to $250,000 and business lines of credit up to $100,000.

I like OnDeck because it’s so simple. After you complete an application online or over the phone, a dedicated loan advisor will go over your options with you. OnDeck offers funding as early as the same business day.

Your line of credit from OnDeck is a great option for working capital. Only withdraw what you need, when you need it, and just pay interest for the amount borrowed.

Repay your line of credit over a 12-month term agreement with automatic weekly payments and no prepayment penalties.

To qualify, you must be in business for at least a year with a minimum personal FICO score of 600 and an annual revenue of $100,000+.

OnDeck periodically reviews your credit profile. So you can automatically qualify for higher credit line limits without having to apply for an increase. You’ll also benefit from a consolidated weekly payment on all withdrawals, so you won’t have to worry about making multiple payments.

#6 – Kiva Review — Best 0% Interest Small Business Loans

If you need a microloan and you’re not in a rush to get it, Kiva will let you borrow up to $15,000 at 0% interest—no strings attached.

As a global nonprofit, Kiva has helped 2.5+ million entrepreneurs raise $1+ billion.

The only downside of Kiva is that it takes quite a bit of time to actually get the loan. So it’s not ideal for businesses that need cash fast.

First, you need to fill out an online application that can take up to 30 minutes to complete. Then you need to prove your creditworthiness by convincing your friends and family to loan you money, which is about a 15-day process. Finally, you can go public on Kiva and make your loan visible to 1.6+ million lenders across the world (an additional 30 days).

On the positive side, you’ll have up to 36 months to repay your loan at 0% interest. It’s tough to beat that deal.

But if you’re looking for large sums of cash as fast as possible, this won’t be the best choice for your business.

Summary

If your small business needs money, there are lots of different small business loan options for you to consider.

Which one is the best?

The answer depends on a wide range of factors, like the amount you need, the loan type, lender, and more. Regardless of your situation, you can find the best loan options for your business based on my recommendations in this guide.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.