According to Smart Insights, 49 percent of organizations don’t have a clearly defined digital strategy.

Choosing the right digital strategy for your business is essential. Experience helps you sift through what to do differently, what not to do, and where to focus your energy. Having a fresh perspective from an outside eye can make all the difference. What’s more important is choosing a company that can execute that strategy.

When you need to choose the best digital strategy company, you may be wondering where to start. Here’s a list of our picks for the best digital strategy companies in the world.

1. Neil Patel Digital — Best For Content Marketing & Digital Strategy

I’ve written more than 4,294 blog posts in 10 years. I’ve created millions of words and I’ve used content marketing to build three companies of my own. I used content marketing to generate 195,013 visitors a month and I’ve done the same things for my fortune 500 clients. When it comes to digital strategy and content marketing I’ve shown it can work.

I do the same thing for clients with my agency, NP Digital. We help our clients develop a digital strategy that maximizes the results they achieve with their content marketing, advertising, and SEO campaigns.

The focus with our digital strategy is revenue. Everything we do is focused on producing real results for businesses whether that’s more traffic, leads, or revenue.

REQ is a Washington DC based, award-winning agency with enterprise-level experience. They’re industry veterans with some of the best talent in the business.

Projects start at $50,000. They offer a comprehensive suite of solutions for your marketing and digital strategy needs. Including:

Advertising & Media

Digital Advocacy

Brand Strategy

Reputation Management

Public Relations

Data & Analytics

They’ve been named to both the Inc.500 and Deloitte Fast 500 lists – they’re one of the fastest growing companies in America. They have offices in Washington, DC, New York, Boston, San Diego, Las Vegas, and San Francisco.

3. Usman Group – Best for Mid-market Business Strategy

With 80% of its clients in mid-market range, earning between 10M – 1B, the Usman Group specializes in digital strategy and market research. They provide analysis, strategy, execution, and measurement to help clients deploy successful campaigns.

They apply the four key principles of design thinking, learn from people, identify patterns, make solutions tangible, iterate continuously, in all of their client engagements.

Projects start at $10,000. You get a hand-picked team that will provide evidence-based, practical strategy and recommendations.

DeSantis Breindel is a New York City based digital strategy company that specializes in end-to-end branding strategy. They help businesses with brand differentiation, customer experience, merger & acquisition branding, brand valuation, brand launch, and employee engagement.

Projects start at $75,000. They offer thorough research and measurement for your digital branding, brand identity and strategy, content marketing, customer experience design, and film production services.

DeSantis Breindel’s client list includes:

Verifone

Lathrop Gage

OneSpan

SailPoint

Lincoln International

Lewis Roca

5. Mabbly – Best for Data Analysis, Channel Strategy

Mabbly is a Chicago based strategic design agency that relies on digital strategy, market research, and data analytics. They focus on turning complex problems into growth opportunities. Supporting human connection with digital experiences, via sophisticated design and data-backed digital strategy.

Mabbly’s team of digital and brand strategists work together to curate a channel strategy that combines the message along with the medium that’s right for your business opportunity. Projects start at $25,000.

Ironpaper bills itself as a B2B growth agency. Their conversion growth strategy is focused on gaining traction with growth up to 1 percent. The growth phase is set at 1 to 3 percent, with anything above 3 percent listed as scaling.

What’s interesting about Ironpaper is the fact that they discuss the elephant in the room.

“Oftentimes, enterprises try to answer the question, ‘What is a good conversion rate?’’ without any context. What is a good conversion rate? When establishing conversion rates, context is everything.

A lack of context can actually do harm to a marketing team, because it causes teams to make the wrong assumptions.”

This tells you that Ironpaper isn’t focused on vanity metrics or conversion manipulation. They know the difference between high and low value conversions. Their projects start at $10,000 and are focused on small businesses.

3 Characteristics That Make a Great Digital Strategy Company

Your digital strategy company should be able to provide you with specifics ahead of time. While many companies are able to provide you with amazing strategies, many are unwilling to demonstrate this ahead of time.

1. Your agency asks the right questions

Creating an exceptional digital strategy begins with your agency asking the right questions. These questions determine what will be answered and where your answers will go. Here’s a small sample of the questions your agency should be asking.

How is our business currently performing?

Which parts of your business are underperforming?

What’s our goal for each area of our business?

What do customers expect from our product and our business?

Which marketing channels are our customers active on?

Which marketing channels should we use to accomplish our goals?

Which metrics and KPIs will we use to evaluate performance?

How should we promote our products and services in the market to achieve our goals?

These questions inform your digital strategy.

Why are we in business?

Where are we right now?

Where do we want to go?

How will we get there?

Your digital strategy framework should answer four high-level questions. Good digital marketing agencies should be asking these questions at the beginning of the engagement process.

2. Your agency is willing to share strategy

The agency you choose should be willing to share sample strategies with you. This doesn’t mean that you should expect your agency to provide the entire strategy upfront, for free. Spec work isn’t ideal and that’s not what you’re looking for.

You’re looking for one example.

They can share this with you over the phone, in your proposal or quote, or in a sample report. You’re looking for them to share a small snippet, a piece of their proposed digital strategy. This is important for several reasons. With sample data you can:

Evaluate your agency’s competence

Use sample data to evaluate potential performance

Assess their digital strategy or marketing priorities

Outline knowledge gaps and weak points in their process

You’re not asking for a comprehensive strategy document, you’re simply asking your agency to pick one part of your business and create a strategy around that; ask your agency a question (e.g., how would you increase sales for one of my products?).

3. Your agency can implement Strategy

Venture Capitalist Arthur Rock, believes strategy is important, but not as important as people who can execute that strategy.

“Over the past 30 years, I estimate that I’ve looked at an average of one business plan per day, or about 300 a year, in addition to the large numbers of phone calls and business plans that simply are not appropriate. Of the 300 likely plans, I may invest in only one or two a year; and even among those carefully chosen few, I’d say that a good half fail to perform up to expectations.

The problem with those companies (and with the ventures I choose not to take part in) is rarely one of strategy. Good ideas and good products are a dime a dozen. Good execution and good management in a word, good people are rare.”

A great strategy isn’t enough. You need amazing people who can implement your digital strategy and produce the results you need to grow.

Your agency should have two things:

A team that can implement your digital strategy

A proven track record showing that they’ve achieved this consistently in the past

If they can provide you with both or they’re willing to provide you with a trial period where you’re able to test their ability to execute your digital strategy, then it may be a good fit.

What To Expect From a Great Digital Strategy Company

Your agency should provide you with detailed specifics for each of these points. If you have more questions or concerns, you’ll want to bring those up with your agency.

A clear track record: Your agency should be able to show you samples, references, case studies, and reviews showing that they’ve achieved results for other clients.

Clear milestones: You’re looking for clear milestones, timelines, and deliverables that show you’re able to create and implement a plan successfully. Your agency should be able to provide you with a timeline, explaining how long everything will take to implement, and when they anticipate you’ll begin seeing results.

Agency procedures: You’ll want to see how your agency plans on approaching your campaign or project. They should be able to break down the approach that goes into their strategy document; this document should clarify how they’ll approach your campaign, what you should expect, what their goals are and more.

The digital strategy company you choose should provide you with the options you need to implement the plan successfully.

Conclusion

Choosing the right digital strategy for your business is essential. You need a plan to guide you, outlining where you are, where you want to go, and how to get there. Having a fresh perspective from an outside eye can mean the difference between success and failure.

Remember, executing your digital strategy plan is even more important than simply having a plan. Use this pool to choose a digital strategy company that will partner with you to achieve your business goals.

Disclosure: This content is reader-supported, which means if you click on some of our links that we may earn a commission.

Every business needs insurance. Depending on your business type and industry, some of you will need more protection than others.

Without insurance, you could be liable for potentially hundreds of thousands or even millions of dollars.

What happens if one of your vehicles is involved in an accident? How will you pay for the damages of a fire or flood in your office? What if an employee or customer slips and falls on your property?

You need to have insurance, or you’ll be paying these costs out of pocket.

But finding the best business insurance package for your organization can be tricky. On the one hand, you want to make sure that you’re covered, but on the other, you don’t want to overpay on premiums.

The best way to start your search is by choosing a reputable business insurance provider—I’ve narrowed down the top business insurance companies in this guide.

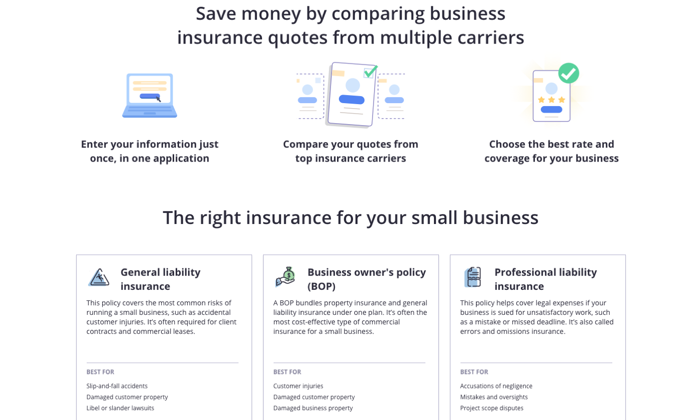

There is no “one-size-fits-all” plan for business insurance. Every organization is unique, so you’ll need custom protection based on your needs. Certain insurance providers are definitely better for specific types of insurance, as well as other factors.

As you’re browsing and getting quotes from different providers, make sure you keep the following considerations in mind:

Industry

Some insurance providers have more experience covering businesses within certain industries.

For example, a restaurant would have very different insurance needs from a construction company. A dental practice won’t have the same needs as an ecommerce website. You get the idea.

So as you’re evaluating a potential provider, take a look at their existing clients and industries served. Do they have experience covering businesses in your industry? If not, look elsewhere.

Customer Service

If you have to submit a claim, you want to make sure that your insurance provider has your back. When you pick up the phone, will someone answer?

Any delay in the claims process will cost your business money. Let’s say there is a flood at your retail storefront. If your insurance company drags their feet, you might not be able to re-open. How soon will someone come to evaluate the property? How quickly can they approve a contractor to repair the damages?

Choose an insurance company that will go the extra mile to serve your business in times when you need their help the most—that’s what you’re paying them for.

Reputation of Provider

There are literally thousands of insurance companies in the United States. Some are brand new, some have been around since the inception of insurance, and many fall somewhere in between.

In most cases, I prefer to go with an older insurance company with a long-standing reputation. These providers have seen it all, and they’ve survived the test of time. You run some risk if you go with a newer company. Let’s say you have some obscure or rare situation with a claim. It could be a first for a new company, and they might not know how to handle it.

Coverage Options

We’ll talk about the different types of business insurance in greater detail shortly. But in a perfect world, you’d like to get all of your business insurance coverage under one roof.

Getting property insurance from one provider, vehicle insurance from another, and general liability from a third company is just too confusing. So look for an insurance company that has a wide array of coverage options that accommodate your needs.

Premiums

Getting proper coverage is obviously important, but how much is this going to cost you?

If you choose the cheapest plan you can find, you’ll probably be exposed to some more out of pocket costs. But if you choose the most expensive plan on the market, do you actually need all of that coverage?

Look for a balance between these two extremes. When it comes to insurance, I typically like to be a bit more conservative. I’d rather overpay a little bit than risk not being fully covered. But this all depends on your individual risk tolerance.

The Different Types of Business Insurance

There are dozens of different business insurance types. But for the purposes of this guide, I’m going to focus on the ones that are the most common and applicable to the masses.

General Liability Insurance

General liability coverage protects you from risks like bodily injuries and property damage. This typically includes medical payments if someone is hurt on your company’s property. General liability can also protect you from lawsuits related to things like libel, slander, privacy violations, copyright infringement, wrongful evictions, and more.

Most businesses will need some type of general liability coverage.

Professional Liability Insurance

Professional liability and general liability are often confused with each other, although the two are not one in the same.

Professional liability insurance is also referred to as errors and omissions (E&O) insurance. This protects businesses sued by clients claiming damages for professional services that you provide. Things like an accountant making a mistake on a tax return or a web developer making mistakes on a site that they manage would be examples where professional liability insurance is necessary.

BOP Insurance

Business owners insurance (better known as BOP) is a policy that combines liability and property into one package. It’s very common for small and mid-sized business owners across a wide range of industries. Most contractors will carry some form of BOP insurance as well.

BOP packages do not cover your employees—it’s specific to business owners.

Workers’ Compensation Insurance

Once you hire your first employee, workers’ compensation should be immediately added to your business insurance policy. Most states require workers’ comp insurance by law.

The coverage pays for things like medical expenses and disability for employees who were injured on the job. This could include minor slip and fall injuries to long-term conditions (like carpal tunnel) or even death.

Business Interruption Insurance

This type of insurance will protect your company if your operations are interrupted during some type of disaster or catastrophic event. Organizations with physical locations that could lose income due to these types of interruptions can benefit from a business interruption policy.

Your business can be compensated for lost income in these types of scenarios.

Vehicle Insurance

This type of business insurance policy is pretty-self explanatory. Just like you need insurance for your personal vehicle, you’ll need to cover any vehicles used for business purposes. If an accident occurs with one of your vehicles (whether you’re driving or not), you’ll need this type of coverage.

Property Insurance

Whether you own or lease physical space, you need to have property insurance. Again, it’s similar to the type of insurance you’d have to protect your home or apartment.

This type of insurance will protect your business from events like fires or theft. Your equipment, inventory, furniture, etc. should all be covered in this policy. However, it’s worth noting that some types of natural disasters, like earthquakes, aren’t always covered in a standard property insurance policy. You might have to pay extra for this type of coverage, depending on your area and the insurance provider.

Product Liability Insurance

If your company manufactures products that are sold to the general public, you must have product liability insurance. This coverage will protect your company from lawsuits related to damages caused by your products.

For example, if someone is injured using one of your products, they could sue your company directly for their medical expenses. That’s when product liability insurance would kick in.

#1 – Chubb Review — Most Versatile Business Insurance Packages

Chubb is one of the most reputable business insurance providers on the market today. They are known for exceptional customer service.

This provider has a wide range of plans for small businesses, commercial insurance, industry-specific policies, and more.

Compared to other insurance providers on the market, Chubb has one of the most extensive coverage portfolios that you can find. Some examples of these policy categories include:

Accident and health

General liability

Cyber insurance

Environmental packages (premises pollution liability and contractor pollution liability)

International insurance packages

Management liability

Inland and ocean marine

Product recall liability

Professional liability

Workers’ compensation

Chubb has over 200 years of experience in the business insurance space. Just be aware that their premiums tend to be a bit higher than other options—but you’re paying for the best.

#2 – CNA Review — The Best Custom Business Insurance Plans

CNA is another reputable provider in the business insurance world. They have 120+ years of expertise in this field.

With CNA, you’ll benefit from a custom insurance package to help manage your risks and liabilities.

There are certain industries that CNA has the most experience working with; these include construction, education, manufacturing, healthcare, real estate, wholesale, technology, professional services, finance, and more.

Here’s a quick glance at some of the types of business insurance offered by CNA:

Workers’ compensation insurance

Professional liability insurance (errors and omissions)

Property insurance

Commercial auto insurance

Business interruption insurance

General liability insurance

Equipment breakdown insurance

I like CNA because you can pick and choose which types of coverage you need, and get them bundled into a single policy that’s custom fit to your needs.

#3 – Hiscox Review — Best For Small Business Insurance

Hiscox is my top recommendation for small business owners. Their policies are affordable, while still providing you with enough coverage to protect your organization from a wide range of potential scenarios.

When I say that Hiscox is great for small businesses, I mean ALL small businesses. They’re currently providing protection to organizations in 180+ different industries.

The list of coverage types offered by Hiscox isn’t quite as extensive as some of the other options on the market today. But they still have more than enough options to accommodate the needs of most businesses.

General liability insurance for small business

Professional liability (E&O) insurance for small business

Business owners policy (BOP) for small business

Short-term liability insurance for small business

Cyber insurance for small business

Workers’ comp for small business

Commercial auto insurance for small business

Umbrella insurance for small business

Employment practices liability insurance for small business

Hiscox is an established name in the business insurance world. They’ve been around since 1901 and insure 300,000+ small businesses across the US.

#4 – Insureon Review — Best Business Insurance Marketplace

Technically speaking, Insureon isn’t actually an insurance provider; it’s an online marketplace for business insurance.

But this robust platform definitely deserves a spot on my list. Insureon is super easy to use, and it’s the best way to compare coverage options from different providers in a single place.

If you’re looking to get the best possible rate, I strongly recommend Insureon. Otherwise, you’d have to get quotes from different providers individually, which is much more of a hassle.

Insureon allows you to compare free quotes from some of the top-rated and well-known business insurance providers on the market today (including some of the options on our list).

Travelers

Chubb

Hiscox

Hannover

The Hartford

Liberty Mutual

AmTrust Financial

The list goes on and on. You can browse policies for professional liability insurance, cyber liability insurance, BOP policies, general liability insurance, commercial property insurance, workers’ compensation insurance, and more.

Insureon is typically geared toward smaller businesses. But it’s used across a wide range of different industries.

#5 – Progressive Review — The Best For Commercial Auto Insurance

Progressive is an industry leader in the commercial auto coverage space.

With 45+ years of experience, they aren’t quite as old as some other players in the industry. However, Progressive is definitely a well-established and trustworthy provider for commercial auto policies.

Here’s a list of some common types of business vehicles insured by Progressive:

Buses

Limousines

Trucks

Vans

Landscaping vehicles

Tow trucks

Box trucks

Snow plows

Sports utility vehicles (for hauling cargo and transporting products)

Pickup trucks

Trailers

It’s worth noting that there are certain types of vehicles that Progressive will NOT insure. This includes emergency vehicles (like fire trucks and ambulances), golf carts, double-decker buses, monster trucks, race cars, wheelchair buses, and a few others.

In addition to the commercial policies, Progressive also has coverage for general liability, BOP, professional liability, workers’ comp, and more.

#6 – The Hartford Review — The Best For Workers’ Comp

For those of you who don’t know, Hartford, Connecticut is known as the “insurance capital of the world.” So it’s no surprise to see The Hartford (named for its headquarters’ namesake) on our list.

This company was founded more than two centuries ago, back in 1810. To say they are a well-established name in the business insurance industry would be a drastic understatement.

The Hartford has an extensive list of product offerings for business insurance. Some of their most popular policies include:

Business owners’ policy (BOP) insurance

General liability insurance

Workers’ compensation insurance

Business income insurance

Commercial auto insurance

Commercial property insurance

Commercial flood insurance

Home-based business insurance

Professional liability insurance

Multinational business insurance

Overall, the workers’ comp coverages provided by The Hartford are second to none. If you want to give your employees the very best protection, look no further than The Hartford.

Summary

In a market saturated with business insurance options, there are really only six choices that I’d consider.

If you choose one of the names reviewed above, you can rest easy knowing that your business is being protected from a well-established and reputable provider.

Be sure to use the methodology I described earlier as you’re shopping around and evaluating different options. That’s the only way to get the best possible business insurance policy for your company.

Requirements:

– 3+ Years XP as Product Manager or related position

– At least some experience working as Engineer in BE Applications

– Some first-hand experience working with Databases.

– Some experience working in SaaS B2B environment.

Most people only think of loans when they think about funding a business. Financing is for sure the most common way to do it, but not all financing comes in the form a traditional term loan. Furthermore, there are options that are not even considered financing because you do not have to repay the funds. The truth is, small business fundraising may not look the way you expect it to.

Small Business Fundraising Can Happen in More Ways than You Thin

Small business fundraising can include loans, but it can also include investors, grants, and more. Beyond that, if you do go with financing of some sort, there are other options out there besides traditional banks and credit unions.

When you think of loans you probably think of traditional loans. These are the most popular, but they are not an option for everyone. There are other types as well.

Traditional Loans

These are loans from traditional banks and credit unions. As a business, your business credit score can help you get some types of funds even if your personal score isn’t awesome. That isn’t necessarily the case with this type of lending however.

With a traditional lender term loan, you are almost always going to have to give a personal guarantee. This means, personal credit will likely weigh heavy on their decision. If your personal credit score isn’t in order, you’ll probably have trouble.

How high does your credit score have to be? Typically, if you have at least a 750 you are in pretty good shape. Sometimes you can get approval with a score of 700+, but the terms will not be as favorable.

If you have awesome business credit, your lender might be more flexible. However, your personal credit score will still play a large role when it comes to terms and interest rate.

These are the most popular choice for small business fundraising because they typically have the best rates and terms. However, they are also the hardest to get.

SBA Loans

SBA loans are traditional bank loans, but they have a guarantee from the federal government. The Small Business Administration, works with lenders to offer small businesses financing solutions that owners may not be eligible for based on their own credit history. Because the government is offering a guarantee, lenders are able to be more flexible when it comes to the owner’s personal credit score.

In fact, it is possible to get an SBA microloan with a personal credit score between 620 and 640. These are very small loans, up to $50,000. They may also require personal collateral.

The trade-off with SBA loans is that the application process is lengthy. There is a ton of paperwork connected with these types of loans.

Here are some of the most popular SBA loan programs.

7(a) Loans

These are federally funded term loans up to $5 million. The funds can be used for expansion, purchasing equipment, working capital and more. Banks, credit unions, and other specialized institutions in partnership with the SBA process these loans and disburse the funds.

This is by far the most popular of the SBA loan programs, and the funds are available for a broad range of projects, from working capital to refinancing debt, and even buying a new business or real estate.

504 Loans

These loans are also available up to $5 million. Funds can buy machinery, facilities, or land. They are generally used for expansion, and private sector lenders or nonprofits process and disburse the money. They work well for commercial real estate purchases especially.

Microloans

Microloans are available in amounts up to $50,000. They work for starting a business, purchasing equipment, buying inventory, or for working capital. Community based nonprofits handle the administration of these programs as intermediaries. Unlike most other SBA loan programs, financing comes directly from the Small Business Administration.

These loans max out at $350,000. The turnaround for express loans is much faster, with the SBA taking up to 36 hours to give a decision. The application process is shorter also.

SBA CAPLine

There are 4 distinct CAPline programs. The main difference between each is the types of expenses they can fund. Each of them carries a maximum amount of $5 million and an interest rate that ranges from 7% to 10%. Funding can take 45 to 90 days.

The four different programs are:

Seasonal CAPLines

Financing for businesses preparing for a seasonal increase in sales.

Contract CAPLines

Financing for businesses that need funding to fill a contract.

Builder’s CAPLines

Financing for businesses taking on a real estate or construction project.

Working capital CAPLines

Financing for businesses that are struggling with a short-term slump in sales.

SBA Community Advantage Loans

This is a pilot program set to either expire or extend in 2020. It’s designed to promote economic growth in underserved areas and markets. Those that make decisions about debt approval look over factors such as poor credit or low revenue if the business has the potential to stimulate the economy or create jobs in underserved areas.

Private Non-Traditional Loans

These are loans from lenders other than traditional banks and credit unions that offer terms loans. Usually they operate online. The difference between these and traditional lenders is that the loans have looser approval requirements and a much faster application process. Most often you can simply apply online, get approval in as little as 24 hours, and the funds are in your account within 24 to 48 hours after approval. Here are just a few options for this type of small business fundraising.

Funding Circle

If you are looking for a low APR, go with Funding Circle. They have fixed rate term loans and require a credit score of 620 or above. There is no minimum revenue requirement. However, they do require you to be in business for at least 2 years.

OnDeck

OnDeck offers lines of credit and term loans with fixed interest rates. You can get up to $500,000 with a term loan. The minimum FICO they require is 600. In addition, you must have $100,000 minimum annual revenue and be in business for at least one year.

Rapid Finance

With a large selection of financing products that includes term loans, Rapid Finance can be a great option for larger amounts. In addition to term loans, they offer bridge loans, healthcare cash advances, and lines of credit. Terms are from three to six months. Amounts range from $5,000 to $1,000,000. Unfortunately, they do not make their minimum credit score readily available. Still, you can use their quote tool. It will give you an idea of what you qualify for.

StreetShares

StreetShares offers invoice financing, term loans, and lines of credit. There is only a one year time in business requirement. Also, they require less minimum annual revenue than the others at only $25,000. The minimum credit score is 600.

Small Business Fundraising: Other Financing

In addition to term loans, there are other types of financing available for small business fundraising.

Lines of Credit

This is basically the traditional lender’s version of a business credit card. The credit is revolving. That means you only pay back what you use, just like a credit card. Rates are typically much better than a credit card however. The application and approval process is more similar to that of a traditional term loan than a credit card.

If you need revolving credit and can qualify for a term loan, this is the best of the available business money types for you. It is great for bridging cash gaps and covering short term expenses without the high credit card interest rates.

Unlike credit cards, there are no cash back rewards or loyalty points with a line of credit. As a result, some business owners prefer business credit cards despite typically higher rates.

Invoice Factoring

If you are an established business with accounts receivable, you have invoice factoring as an option. This is where the lender buys your outstanding invoices at a premium, and then collects the full amount themselves. You get cash right away, without waiting for your customers to pay the invoices.

This is a good option if you need cash fast, or if you do not qualify for other types of funds. The interest rate varies based on hold old the invoices are. A merchant cash advance is a similar option, in which a lender lends cash based on average daily credit card sales. Repayment is made daily credit card sales as well.

Small Business Fundraising: Crowdfunding

Crowdfunding is a newer option for finding investors. While the average Joe that wants to start a business needs funding, it is not always possible to find one or two large investors. With crowdfunding, you can literally have a “crowd” of investors fund your business $5 and $10 at the time.

There are many crowdfunding sites, but the most popular are Kickstarter and Indiegogo. The platforms are similar but there are some important differences. The most obvious is the timing of when you actually receive the funds that others invest in your company.

Kickstarter requires a preset goal, and you do not receive your funds until you reach your goal. For example, if you set a goal of $20,000 when you start your campaign, you will not receive any money that investors offer up until you reach that $20,000.

Indiegogo also requires a goal. In contrast to Kickstarter, they offer the option to receive funds as you go if you prefer. They also have an option called InDemand. This program allows you to continue raising funds after your original campaign is over without starting a whole new campaign. It is more of an extension of the first one.

There are other crowdfunding sites out there as well. Different ones work better for certain businesses and vendors. To determine which one you might have the most luck with, you will need to do some research. Keep in mind your type of business and the specific business each one appeals too.

Small Business Fundraising: Angel Investors

These are informal investors that generally invest at the start of a company. They typically receive equity in exchange.

Angel investing is risky. If a startup fails early on, investors will lose their investments completely. As a result, professionals will look for a defined exit strategy, acquisitions, or initial public offerings (IPOs).

The best way to find angel investors is to ask around. You can also try an angel investors website or network.

Small Business Fundraising: Grants

While grants are less commonly available than other options, they are more common that you probably think. Typically, they are offered by professional organizations. There are some government grants available also. There is stiff competition, but they are definitely worth a shot if you think you may qualify.

While requirements vary from grant to grant, and most are only awarded to a certain number of recipients, they are definitely worth exploring. This is especially true if you fall into one of these basic categories.

Women owned business

Minority owned business

Businesses run by veterans

Businesses in low income areas

There are also some corporations that offer grants in a contest format that do not require much other than that you meet the corporation’s definition of a small business and win the contest.

Small Business Fundraising: Explore All Your Options

When you need to think about small business fundraising, be sure to consider all your options. It may be that traditional loans will work best for you, but that may not be the case at all. Even if you do qualify for loans, why not consider grants and investors as well. It’s free money. Any money you can get that will reduce the amount of debt you have to take on is a good thing.

If you want to expand your opportunities even further, work on the overall fundability of your business. There are things affecting it that you probably don’t even realize can make a difference. There is a lot more to it than just your credit score.

How you set up your business, your business phone number, and even past speeding tickets can indirectly affect fundability. If you work to reduce negative impact and increase positive impact on fundability, you can open the door to even more small business fundraising opportunities.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.