Minimizing Debt Before It’s Too Late … How To Avoid The Pitfalls Of Creeping Debt

Decreasing financial debt typically isn’t a high top priority for individuals till they have actually currently entered difficulty with overspending. Utilizing a couple of standard standards, as well as financial obligation estimations, can assist you see when your financial debt tons is getting involved in the risk area.

Budgeting Guidelines

Off, financial institutions make use of budgeting standards when accepting and also assessing credit scores. You have a greater danger of debt applications being rejected if your financial debt goes beyond the economic neighborhoods suggested standards.

Obtaining, and also maintaining, your financial obligation according to advised budgeting standards, is a crucial action in financial obligation decrease. Utilize the adhering to advised budgeting standards (the exact same ones utilized by Financial Institutions) to assess the products in your budget plan:

Real estate 35% – Mortgage or rental fee, tax obligations, fixings, renovations, insurance coverage, as well as energies;

Transport 20% – Monthly repayments, gas, oil, repair services, insurance policy, car park & public transport;

Financial obligation 15% – Credit cards, individual financings, trainee financings & various other financial obligation settlements;

All various other expenditures 20% – Food, insurance coverage, prescriptions, physician & dental practitioner expenses, garments & individual;

Investments & Savings 10% – Stocks, bonds, money gets, retired life, rental realty, art, and so on

. Financial Obligation Income Ratios

The 2nd action is computing your financial obligation revenue proportion. You will certainly recognize simply exactly how essential financial obligation lots is to your total monetary image as soon as you recognize what your proportion is. Your financial debt earnings proportion is the percent of your regular monthly take-home income that mosts likely to paying financial debts.

You compute it by taking the quantity required to settle financial obligations monthly, consisting of rental fee or home loan, and also divide by your net income (your take-home pay after tax obligations). Keep in mind, this is “Debt” proportion, so just consist of real financial debt payment in the estimation.

Debt To Debt Ratio

Since you pay off a credit history card is no factor to shut your account, simply. One unknown reality concerning the Credit to Debt Ratio is the reverse result it carries your credit history. If you settle a bank card, as well as shut the account, you are really adversely influencing your credit report.

The factor for this unfavorable result remains in the computation of the Credit to Debt Ratio itself. This proportion is the connection of your financial debt total amount vs. your credit line.

You determine it by splitting the complete credit line of all charge card and also financing accounts by the total amount of the real financial debt (invested overall). Currently, if you repay a charge card, you are lowering the real financial obligation, which is terrific, however, if you shut the account, you are additionally considerably decreasing the credit line you have, as well as generally by a greater portion than the financial obligation decrease.

Pay Yourself

Vital to lasting economic success, as well as securing your future, is paying on your own. Financial obligations and also various other monetary responsibilities, cash for enjoyment, and also various other investing constantly appear to take a greater top priority. Assume concerning it, if you aren’t worth being paid initially, after that is?

Snowball The Credit Cards

Paying simply $10 added a month on a credit scores card, over the minimum necessary repayment, can reduce your settlement term in fifty percent, if not even more! Press out that added settlement, nonetheless little, every month, and also take benefit of the compounding impact of snowballing your financial obligation away.

Bear in mind, you do not need to be a monetary whiz to recognize what’s happening with your debt as well as financial obligation. Simply a couple of basic estimations, as well as an eye on the future, will certainly go a lengthy method to aid you do well economically as well as maintain your financial obligation controlled. Be secure, be clever, do the mathematics!

The 2nd action is computing your financial obligation revenue proportion. When you recognize what your proportion is, you will certainly recognize simply exactly how essential financial obligation lots is to your general monetary photo. Your financial debt revenue proportion is the percent of your regular monthly take-home pay that goes to paying financial obligations.

One little well-known reality regarding the Credit to Debt Ratio is the reverse result it has on your credit scores rating. Bear in mind, you do not have to be a monetary whiz to comprehend what’s going on with your credit report as well as financial obligation.

Minimizing Debt Before It’s Too Late … How To Avoid The Pitfalls Of Creeping Debt

Decreasing financial debt typically isn’t a high top priority for individuals till they have actually currently entered difficulty with overspending. Utilizing a couple of standard standards, as well as financial obligation estimations, can assist you see when your financial debt tons is getting involved in the risk area. Budgeting Guidelines Off, financial institutions make use of budgeting standards when accepting and also assessing credit scores. You have a greater danger of debt applications being rejected if your financial debt goes beyond the economic neighborhoods suggested standards. Obtaining, and also maintaining, your financial obligation according to advised budgeting standards, is a crucial action in financial obligation decrease. Utilize the adhering to advised budgeting standards (the exact same ones utilized by Financial Institutions) to assess the products in your budget plan: Real estate 35% – Mortgage or rental fee, tax obligations, fixings, renovations, insurance coverage, as well as energies; Transport 20% – Monthly repayments, gas, oil, repair services, insurance policy, car park & public transport; Financial obligation 15% – Credit cards, individual financings, trainee financings & various other financial obligation settlements; All various other expenditures 20% – Food, insurance coverage, prescriptions, physician & dental practitioner expenses, garments & individual; Investments & Savings 10% – Stocks, bonds, money gets, retired life, rental realty, art, and so on . Financial Obligation Income Ratios The 2nd action is computing your financial obligation revenue proportion. You will certainly recognize simply exactly how essential financial obligation lots is to your total monetary image as soon as you recognize what your proportion is. Your financial debt earnings proportion is the percent of your regular monthly take-home income that mosts likely to paying financial debts. You compute it by taking the quantity required to settle financial obligations monthly, consisting of rental fee or home loan, and also divide by your net income (your take-home pay after tax obligations). Keep in mind, this is “Debt” proportion, so just consist of real financial debt payment in the estimation. Debt To Debt Ratio Since you pay off a credit history card is no factor to shut your account, simply. One unknown reality concerning the Credit to Debt Ratio is the reverse result it carries your credit history. If you settle a bank card, as well as shut the account, you are really adversely influencing your credit report. The factor for this unfavorable result remains in the computation of the Credit to Debt Ratio itself. This proportion is the connection of your financial debt total amount vs. your credit line. You determine it by splitting the complete credit line of all charge card and also financing accounts by the total amount of the real financial debt (invested overall). Currently, if you repay a charge card, you are lowering the real financial obligation, which is terrific, however, if you shut the account, you are additionally considerably decreasing the credit line you have, as well as generally by a greater portion than the financial obligation decrease. Pay Yourself Vital to lasting economic success, as well as securing your future, is paying on your own. Financial obligations and also various other monetary responsibilities, cash for enjoyment, and also various other investing constantly appear to take a greater top priority. Assume concerning it, if you aren’t worth being paid initially, after that is? Snowball The Credit Cards Paying simply $10 added a month on a credit scores card, over the minimum necessary repayment, can reduce your settlement term in fifty percent, if not even more! Press out that added settlement, nonetheless little, every month, and also take benefit of the compounding impact of snowballing your financial obligation away. Bear in mind, you do not need to be a monetary whiz to recognize what’s happening with your debt as well as financial obligation. Simply a couple of basic estimations, as well as an eye on the future, will certainly go a lengthy method to aid you do well economically as well as maintain your financial obligation controlled. Be secure, be clever, do the mathematics!

The 2nd action is computing your financial obligation revenue proportion. When you recognize what your proportion is, you will certainly recognize simply exactly how essential financial obligation lots is to your general monetary photo. Your financial debt revenue proportion is the percent of your regular monthly take-home pay that goes to paying financial obligations. One little well-known reality regarding the Credit to Debt Ratio is the reverse result it has on your credit scores rating. Bear in mind, you do not have to be a monetary whiz to comprehend what’s going on with your credit report as well as financial obligation.

Believe Before You Buy A Consumer Debt Consolidation Program

Globe has actually come to be quick relocating today. With the increase in the economic situation as well as accessibility to sources worldwide, it is not unusual to see lots of people enter financial obligation and afterwards take into consideration registering in a customer financial obligation combination program. There can be numerous costs that can go back to haunt your joy.

Expenses such as education and learning expenses, own a home expenses, various other expenses and also clinical costs quickly accumulate and also end up being the factor behind your cash money water drainage. There is constantly a slim line of distinction in between maintaining your head over water as well as sinking in the red. Financial obligation debt consolidation procedure is quick acquiring footing in the economic market these days.

You can discover different customer financial obligation combination programs readily available that can aid you address your financial debt issues. You can warrant your demand to go in for a financial debt loan consolidation program depending on exactly how much deep in credit history you locate on your own in. You require to keep in mind that by the financial debt loan consolidation procedure, you do not remove any kind of exceptional financial debt.

Financial obligation loan consolidation can resolve numerous kinds of financial obligations such as credit history card financial debts, clinical financings and also individual lendings. As a customer, you should keep in mind that the period of a customer financial obligation loan consolidation program is generally longer than the various other car loans. While looking for a customer financial obligation combination program on the Internet, you need to be extremely clear in what you are looking for in the program.

Financial obligation combination may offer you an impression of points being in control. You ought to wind up your financial debt loan consolidation finance within the slated time duration to conserve on your own some rate of interest.

With the broaden in the economic climate as well as accessibility to sources around the world, it is not odd to see several individuals obtain right into financial debt and also after that think about enlisting in a customer financial debt combination program. You can discover different customer financial debt combination programs offered that can aid you fix your financial obligation issues. You require to keep in mind that by the financial obligation loan consolidation procedure, you do not get rid of any type of exceptional financial obligation.

Financial obligation debt consolidation can attend to different kinds of financial obligations such as credit scores card financial obligations, clinical lendings as well as individual car loans. While looking for a customer financial debt combination program on the Internet, you ought to be really clear in what you are looking for in the program.

Believe Before You Buy A Consumer Debt Consolidation Program

Globe has actually come to be quick relocating today. With the increase in the economic situation as well as accessibility to sources worldwide, it is not unusual to see lots of people enter financial obligation and afterwards take into consideration registering in a customer financial obligation combination program. There can be numerous costs that can go back to haunt your joy.

Expenses such as education and learning expenses, own a home expenses, various other expenses and also clinical costs quickly accumulate and also end up being the factor behind your cash money water drainage. There is constantly a slim line of distinction in between maintaining your head over water as well as sinking in the red. Financial obligation debt consolidation procedure is quick acquiring footing in the economic market these days.

You can discover different customer financial obligation combination programs readily available that can aid you address your financial debt issues. You can warrant your demand to go in for a financial debt loan consolidation program depending on exactly how much deep in credit history you locate on your own in. You require to keep in mind that by the financial debt loan consolidation procedure, you do not remove any kind of exceptional financial debt.

Financial obligation loan consolidation can resolve numerous kinds of financial obligations such as credit history card financial debts, clinical financings and also individual lendings. As a customer, you should keep in mind that the period of a customer financial obligation loan consolidation program is generally longer than the various other car loans. While looking for a customer financial obligation combination program on the Internet, you need to be extremely clear in what you are looking for in the program.

Financial obligation combination may offer you an impression of points being in control. You ought to wind up your financial debt loan consolidation finance within the slated time duration to conserve on your own some rate of interest.

With the broaden in the economic climate as well as accessibility to sources around the world, it is not odd to see several individuals obtain right into financial debt and also after that think about enlisting in a customer financial debt combination program. You can discover different customer financial debt combination programs offered that can aid you fix your financial obligation issues. You require to keep in mind that by the financial obligation loan consolidation procedure, you do not get rid of any type of exceptional financial obligation.

Financial obligation debt consolidation can attend to different kinds of financial obligations such as credit scores card financial obligations, clinical lendings as well as individual car loans. While looking for a customer financial debt combination program on the Internet, you ought to be really clear in what you are looking for in the program.

Just think about that for a minute… and let that sink in. It’s

roughly 9 changes per day.

So how can you beat this gigantic company at their own game and rank high? Especially when you consider that they generate over $100 billion+ per year in ad revenue?

The real trick to rank well is to leverage technology.

See, although Google has made things harder, there are things you can do now that I couldn’t when I first started. For years now technology has evolved, which has made your life easier as an SEO.

Here are 7 advanced SEO strategies that I’m implementing as we speak and you should too.

Advanced SEO Strategy #1: SEO A/B Split Testing

To improve your rankings, what do you have to do?

You have to go in and manually make changes to your site.

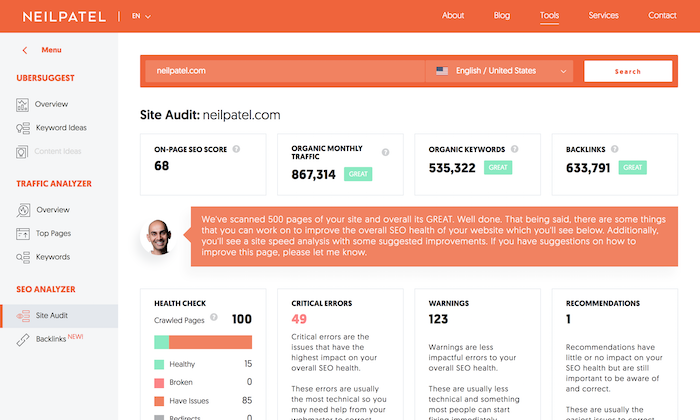

And if you aren’t sure what changes to make, just put in your URL into this SEO Analyzer and it will spit

out a report like the one below.

But there is one issue with making changes manually, and I

know this because I own an ad agency and I

do the SEO for my own website.

It takes forever to make changes.

Heck, I can barely keep up with the changes I need to make on NeilPatel.com as I have far too many pages.

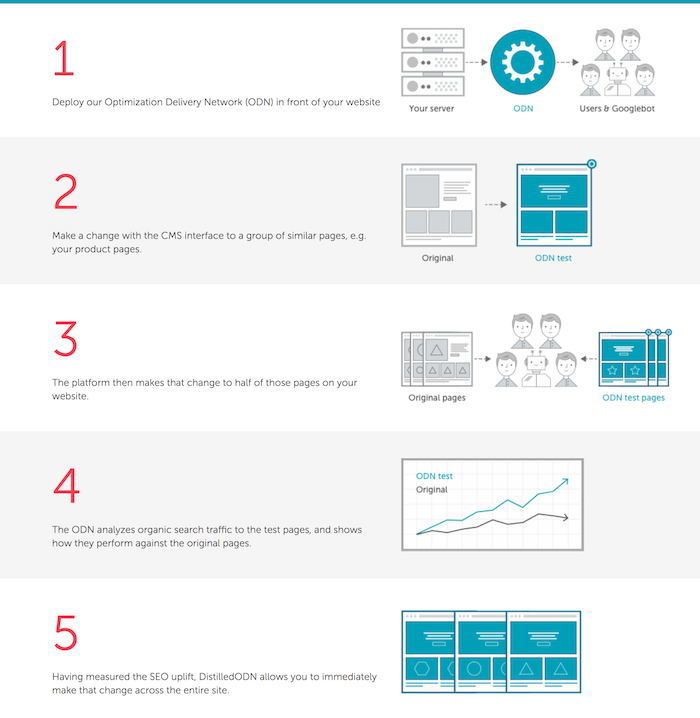

But now with companies like Rank Science and Distilled ODN, you no longer have to make changes to your site.

I know that sounds crazy, but think about what I just said.

You no longer have to make changes to your site.

You are probably wondering how right?

When you want to track your website, you just install a

piece of javascript like the one Google Analytics gives you and you are off to

the races.

Rank Science and Distilled ODN are similar. You install a piece of javascript and that’s it. From there it doesn’t matter if you have a CMS, or how your website is built, or any of that… they can make changes to your HTML code without you needing to do anything.

You don’t even have to give them your server password or an FTP login. The technology has changed so much that the simple javascript you add to your website can now make the changes for you.

I know that may be hard to believe, but that is how A/B testing worked for years. If you use Optimizely, VWO, or Crazy Egg… you just add a javascript and from their end, they can adjust your site.

So why can’t the same be done for SEO? Why do you have to manually make changes still?

The cool part about tools like ODN or Rank Science is they can make the changes automatically, which is really useful if you have thousands of pages.

Here’s how they work:

This way your site can always be SEO-friendly without you having to make any of the adjustments yourself.

Advanced SEO Strategy #2: E-A-T

In the SEO world, there has been an acronym that has been thrown around a lot and it is E-A-T.

It stands for expertise, authority, and trustworthiness.

Google no longer wants to rank just “good” content. Now, they are worried that a piece of content that ranks is inaccurate and can hurt the potential searcher.

For example, let’s imagine you are giving medical advice on your site. You have a ton of links and all of the right signals to rank well but your content is inaccurate. Now imagine someone injures themselves after taking your advice… well, that would be bad.

In the SEO world, you see sites in the health space or financial space having more issues with Google algorithm updates because their information may be inaccurate and Google is looking for sites to prove their expertise, authority, and trustworthiness.

But my hunch is, over the next year or two, they will crack down on many more industries.

If you are going to rank a site, everyone these days can manipulate SEO signals, but it is hard to manipulate things like expertise, authority, and trustworthiness. Especially when you combine all three.

One thing I’m focusing on in the next 12 months is to increase what I believe will help boost my rankings in the long run.

How you may ask? Well, I’m going to leverage a handful of

tactics:

Guest post – guest posting on popular industry and news sites should help increase my brand recognition over time. I used to do this more frequently in the past and I will kick this off again. If you don’t know how to guest post, check this out.

Speak at conferences – I’ve slowed down on this a bit, but I will pick it up for the same reason above. It should help with E-A-T. If you haven’t spoken at many events, the key is to just apply to a lot of them and eventually some will accept you.

Awards and recognition – continually apply for more awards. I used to do this when I was much younger and I’ve gotten lazy about it these days. The same goes for publishing more books… I already have one New York Times bestseller, why not go for a few more?

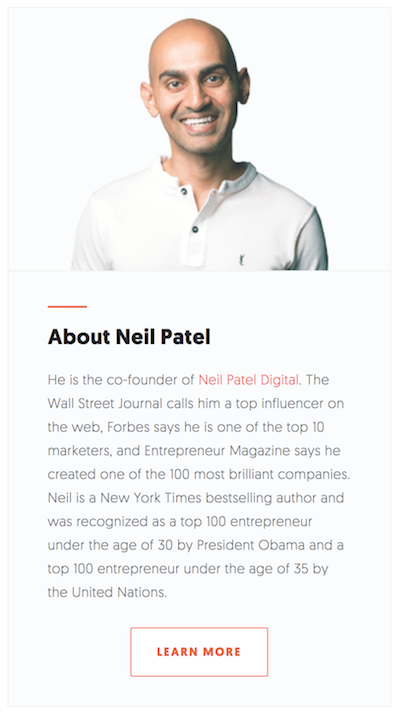

A simple thing that you can do if you believe you have been negatively impacted by some of the more recent Google updates is to include an author bio box on every piece of content you write. And, of course, use author schema markup.

A good example of this is my author box…

Using this should help boost your long-term rankings.

Advanced SEO Strategy #3: Host HTML Files From a CDN

We all know that speed impacts rankings. It also impacts conversion rates. Walmart, for example, boosted their conversion rate by 2% for every second of load time they reduced.

And nowadays more Google searches happen on mobile devices, hence load time and speed really matter.

I already have a faster server… my hosting bill is a bit

more than I would like.

And it’s actually going to get a bit worse.

Currently, I have a server where my site is hosted. That server is somewhere in the United States… I believe the east coast.

That means if someone wants to visit my website from let’s say New York City, it should load fairly fast. However, if someone from São Paulo, Brazil wants to visit NeilPatel.com, it would take a bit longer as they are further away from my server.

To solve this, I’ve been using a CDN. A CDN is a content delivery network.

Services like Cloudflare cache your images and static content and server it from the closest server to the person visiting your website.

So now when someone from São Paulo visits my website, they are usually served up cached content from a server in Brazil. This makes their experience load much faster.

But as your content changes, and with things like WordPress

blogs where you are constantly getting comments and going through page changes,

not all of your content is served up through a CDN.

My team is now making a tweak to improve my load time even more. So instead of serving up my HTML pages from my server, we are now going to serve them up from a CDN.

In other words, we are trying to serve as much of our site from a CDN.

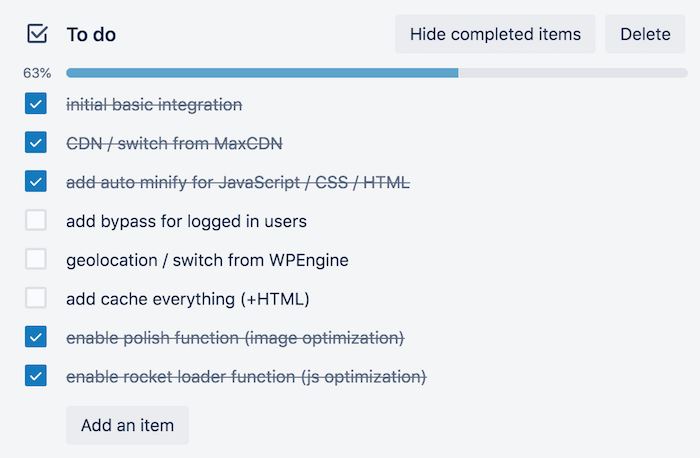

As you can see from the Trello list above, that’s all of the

stuff we are working on serving up from our Cloudflare account in order to

speed up our site and eventually boost our search rankings and conversion

rates.

I wish I can walk you through how to do it step by step, and maybe that could be a future blog post, but the easiest is to just find a developer from UpWork to do it for you.

Advanced SEO Strategy #4: Multi-lingual Title Tag Tests

Similar to Rank Science, there’s a tool I currently use to

test my title tags.

I use to automatically test my title tag and meta description to maximize my click-through rate. And like Rank Science, you just add a piece of javascript and it can start running tests for you automatically.

That way, you don’t have to manually keep changing things.

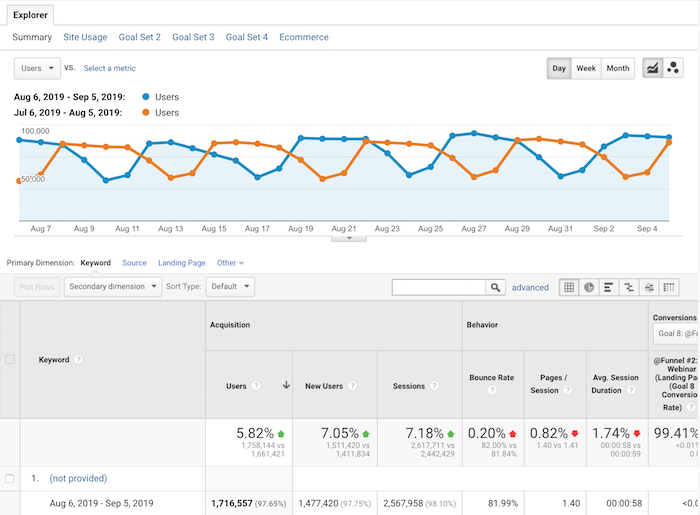

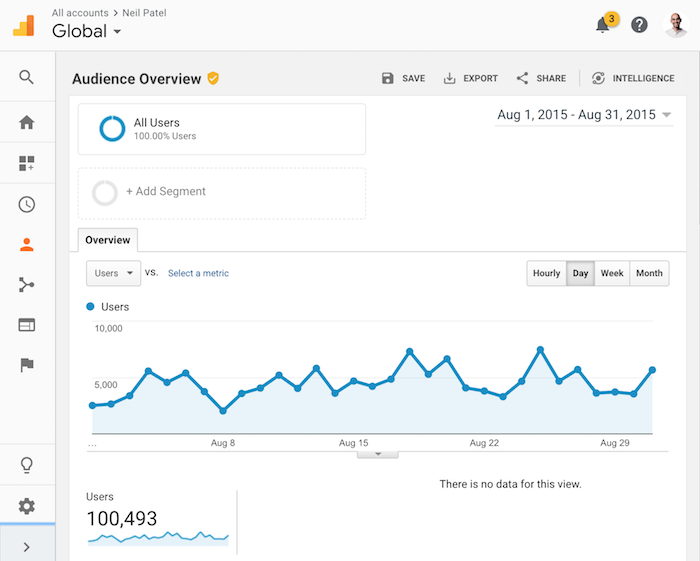

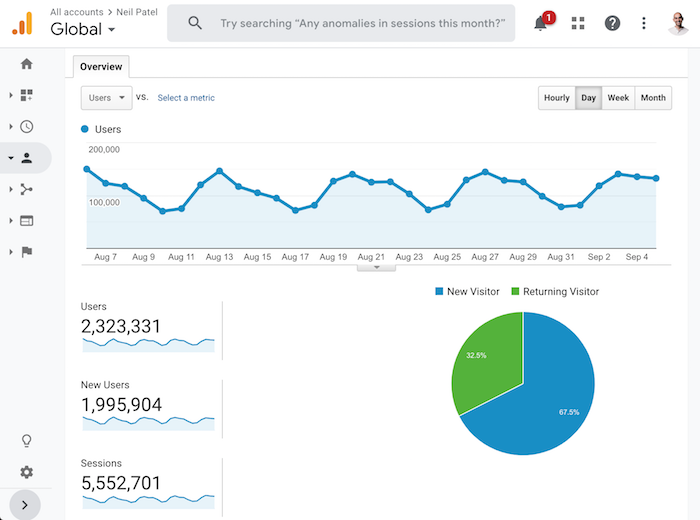

And Clickflow has worked well for me for over the past year… really well. Just look at my month-over-month growth from the past couple of months.

Just in the last 31 days, I saw an increase in organic

traffic by 96,723 just through title tag split tests.

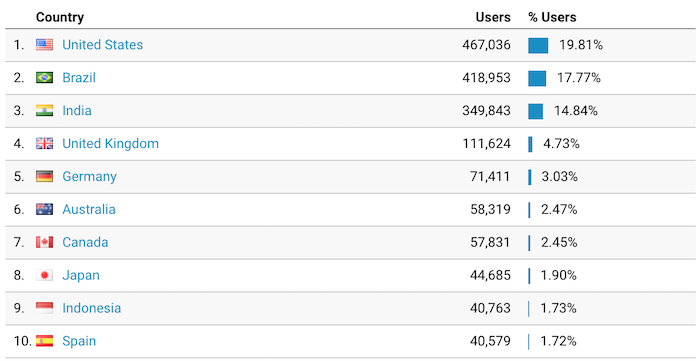

But here is the kicker: I’m only able to effectively use the software for my English content. Now just imagine if I did this in less competitive markets like Brazil where I am generating 418,953 unique visitors a month.

Or what if I did that with my German blog or Spanish blog? The possibilities are endless!

Sure in English, not many SEOs are doing title tag split testing but some still are. In other regions, many marketers haven’t even heard of this yet.

So, over the next few months, my team will have to manually

do this to figure out what works in these markets.

If you haven’t done it yet in English, check out this post. Here you will see some of the basic findings when it comes to boosting CTRs were:

Title tags that contain a question generate 14.1% more clicks on average.

Title tags between 15 and 40 characters generate the most clicks.

Leveraging emotions can increase clicks. Meta tags with a positive or negative emotion generated roughly 7% more clicks.

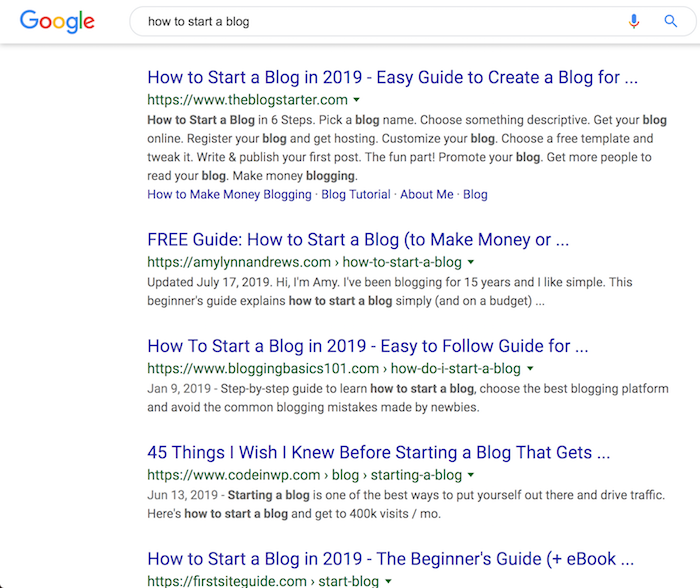

And if you want something really simple, I’ve found that adding the year in your title tag can drastically increase CTR.

For example, look at a lot of the top results that rank for

the phrase “how to start a blog”.

3 of the top 5 results contain the year in the title tag.

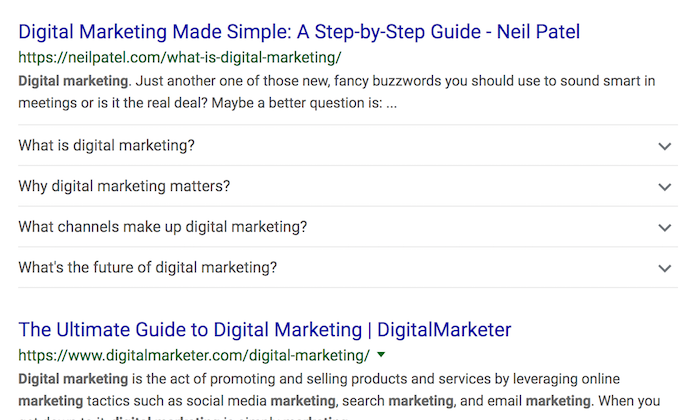

Advanced SEO Strategy #5: FAQpage Schema Markup

I blogged about this in the past, but less than .17% of

sites are leveraging it.

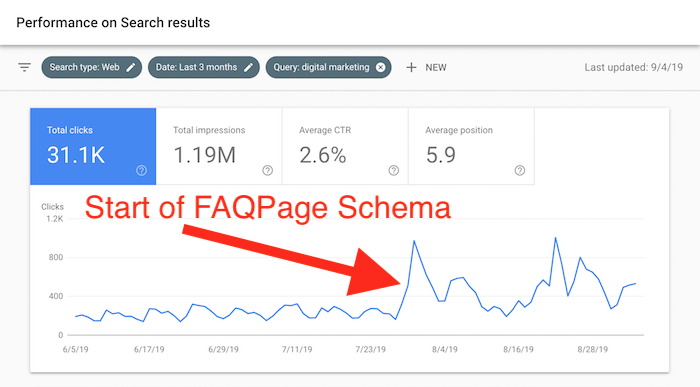

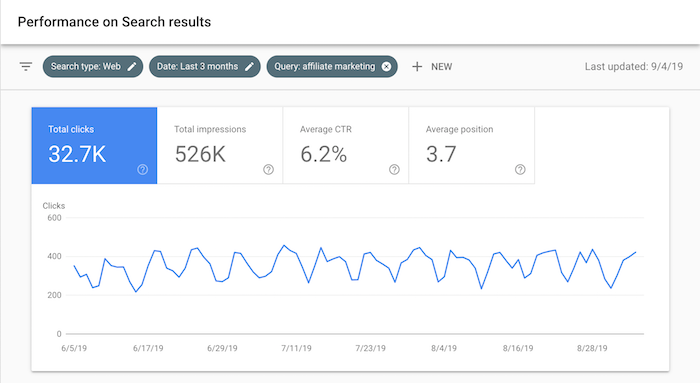

Before I get into it, just look at my search traffic from

the term “digital marketing”.

Sure the chart is bouncing up and down a lot, but I’m getting way more traffic than I was before I implemented the FAQpage markup.

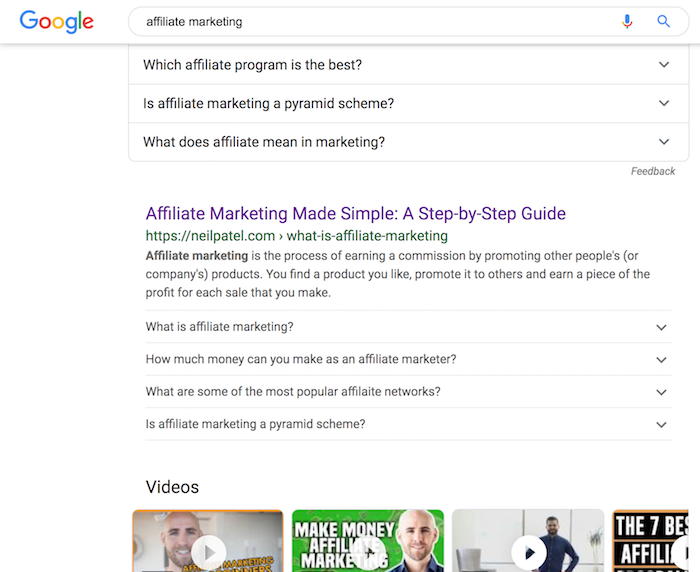

In essence, what it does is add common FAQ-based questions to your search listing. Similar to the image below.

I know some people say that if you add this to your site then there is no reason for people to visit your site. And in essence, Google wins because it keeps them on their search engine.

But the way I look at it is if your website provides amazing content and helps create an amazing experience, a portion of those people will remember your URL and will come back in the future.

Plus if you aren’t in the number 1 spot, you don’t have much to lose by implementing this. Even if you are in the number 1 spot like I am for my affiliate marketing page and you add FAQpage schema…

I’ve found that when I add the FAQpage schema my traffic

hasn’t dropped.

Now all I have to do is add this for another 649 blog

posts that we identified that are a good fit for this on my blog. 🙁

Advanced SEO Strategy #6: Content Clusters

I bet you have content on your site. And similar to me, when

you wrote the content you used tools like Ubersuggest and wrote whatever

had a lot of search volume.

And if you want to get a bit more organized and move faster, you probably even used a content calendar.

But just like me, I bet over the years you never focused on clustering your content together. And because you didn’t you probably have tons of pages on similar topics if not the same topic.

This is a big problem because it confuses Google.

For example, I have so many pages on “keyword tools” and “keyword research” that Google doesn’t necessarily know which page to rank. Because of this, my rankings for some of those terms are somewhat stable, but the rank page from my site constantly changes.

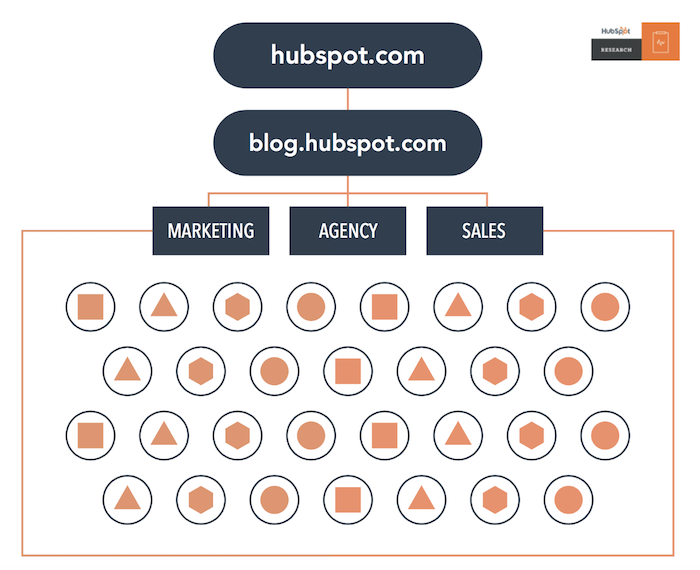

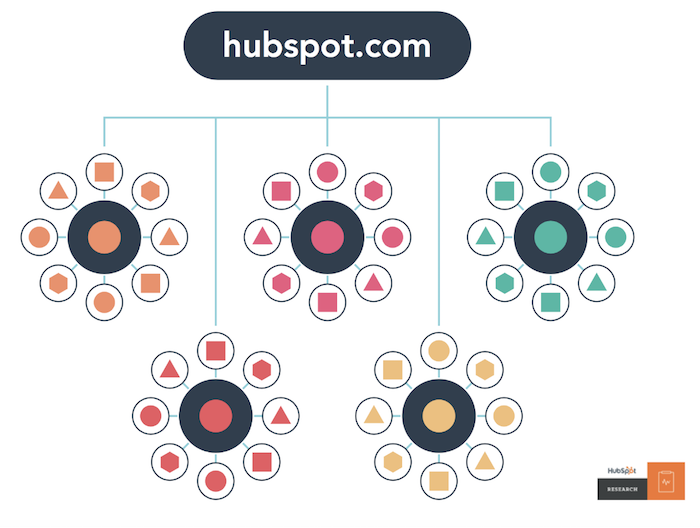

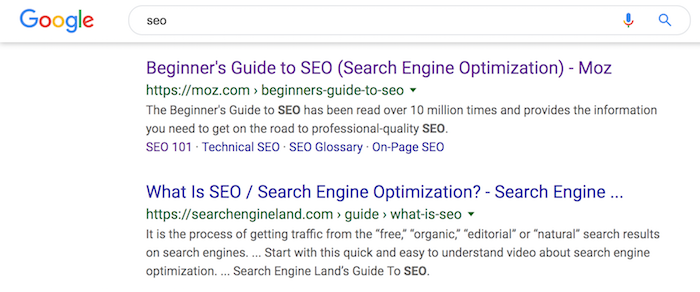

A good solution to this problem and improved overall rankings is to use content clusters. A great example of a site that didn’t use clustering but now does is Hubspot.

Their content went from looking like this:

To looking like this:

The overall goal is to have sections of your site and blog about specific topics. And from there you can link and connect other articles around the same topic together. Doing this lets the search engines know which one is the main topic through things like breadcrumbs and URL hierarchy.

They are telling search engines that the chapter is part of the whole Beginner’s Guide to SEO and they did this through the use of folders.

And here is another chapter… https://moz.com/beginners-guide-to-seo/keyword-research

As you can see, they followed the same structure. This a simple way to use content clustering to improve your rankings. Case in point, they rank number 1 on Google for the term “SEO” and have for years.

Now I just have to do this with my whole site in multiple

languages.

Advanced SEO Strategy #7: Conquer the World

I’m serious when I say that by the way… I really am going

after all of the major countries.

The most vital SEO strategy I ever learned came from a Google employee. And it was simple… Google has tons of content to choose from when it comes to ranking sites in English but they lack a lot of high-quality content in other regions.

So, I decided to do something simple years ago… I translated my content into other languages. That’s how my traffic has gone from this:

To this:

Sure, I have leveraged a lot of other tactics over the years as well, like building Ubersuggest into a free SEO tool. But even that, Ubersuggest has grown so fast because it is translated into 9 different languages.

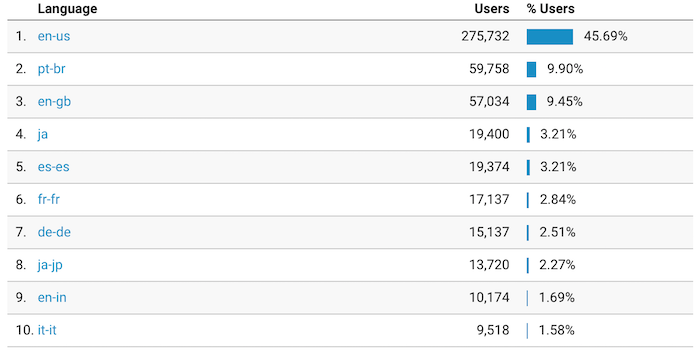

Just look at the language breakdown of Ubersuggest’s traffic

stats.

When you combine all of the different variations of English, all of the other variations make up roughly 40% of the tools traffic.

Now with my blog, I haven’t gone as far as translating it into as many languages as the tool, but I plan on translating it eventually into 22 languages. I pick them based on population size and GDP.

This one will take me a few years to really scale up but it provides massive gains for me.

This is a must if you want to not only dominate SEO but business in general. Companies these days aren’t just based in the US or UK or China… they are all going global.

Conclusion

No matter if you have been doing SEO for just a few weeks or

even years like me, there is always more to do.

Google is constantly changing and with the new technology

that’s available to you, there is still a lot of room to do well.

As you can see from the above strategies, that’s the stuff I am focusing on over the next 12 months. They’re tactics that work and provide results.

Some of them are really advanced and require engineering

help, but SEO is no longer just about hiring a marketer and having them help

you get more traffic. To really do well, you have to get a bit more technical

than most marketers are comfortable with.

So, what do you think of the strategies above? Have you

tried any of them yet?

Google makes over 3,200 algorithm changes per year. That’s a lot of changes. Just think about that for a minute… and let that sink in. It’s roughly 9 changes per day. So how can you beat this gigantic company at their own game and rank high? Especially when you consider that they generate over $100 … Continue reading 7 Advanced SEO Strategies I’m Trying to Implement Before 2020

How to Tell the Difference Between Legit Creditors and Predators Out to Eat You Alive

Watch any animal reality show and you will see what happens between predators and prey. In a similarly menacing way, some lenders actually prey on unsuspecting borrowers. Not only do they leave finances in ruins, but often the trail of destruction trails across their entire lives. They basically eat their prey alive. How can you avoid falling victim to these devilish creatures? We are going to show you how to tell the difference between legit creditors and predators, so that you can survive in the credit wilderness.

Know Thy Enemy: What is Predatory Lending

According to Investopedia: “Predatory lending benefits the lender and ignores or hinders the borrower’s ability to repay a debt. These lending tactics often try to take advantage of a borrower’s lack of understanding concerning loans, terms, or financial literacy.”

Basically, just like predators in the wild, predatory lenders take advantage of the weak. They look for those that are unassuming, easily tricked into coming closer, and without suitable defenses. Then they pounce.

In the wild, predators often disguise themselves as something else. Consider the venus fly trap. To the fly, it looks like a flower. The fly saunters over to enjoy the beauty, and snap! It’s gone before it even knows what hit it. That is the peril of a predatory lender. It looks great, inviting even. Before you know it, however, they trap you. The best protection you can have is to know the difference between creditors and predators. Don’t be fooled. Learn the signs and build your defenses. Know thy enemy.

Common Signs that a Creditor is Actually a Predator

The only way to tell the difference between creditors and predators is to know the signs of a predator. They are not that hard to spot if you know what tricks to look for.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

Payment is King

If you are trying to get a loan and the “creditor” continues to emphasize what your payment will be, while downplaying how much the actual loan is, that creditor might be a predator. While a monthly payment is obviously important for budgeting purposes, you need to know all the terms of the loan.

A lender can use many tactics to ensure your monthly payment is where you need it to be to fit your budget. They can increase the loan period, adjust terms, and add balloons to make things look much better than they really are. The result is that you get a really bad loan in exchange for a temporary lower payment.

Burst the Balloon

Speaking of balloon loans, those are also a common predatory lending practice. They use them to provide unsuspecting borrowers with a low monthly payment for most of the loan. Most borrowers do not realize that they are typically only covering the interest for each month.

In fact, usually the principle isn’t reduced at all by payments until the very end of the loan. The final payment ends up being a large “balloon” payment that should pay off the entire principal of the loan all at once. Most of the time borrowers are not prepared for this, and they end up either refinancing or defaulting.

Unpack the Packing: Unnecessary Baggage

Packing is another practice that predatory lenders seem to lean towards. It involves them adding extras onto the loan. You do not need these extras, and they add them without your knowledge. The most common culprits are insurance products that are not necessary for your situation. You pay for them without realizing it, and they offer you no benefit.

Excessive Points and Fees

It’s not uncommon for lenders to charge points and fees on a loan. It is a practice that some use to increase profits. As a general rule, one point is worth one percent of the loan balance.

Asking for more points and higher fees than is normal for the type of loan you are getting can be a sign of predatory lending. If you feel that is what is going on, dig deeper.

How do you know what is “normal” and what is excessive? As a general rule, three points, or 3% of the loan amount or less, is a decent deal. This includes appraisals and title insurance, which are necessary. Research to see what is normal for your area, but know this is a good rule of thumb.

The New York Connection: Of Creditors and Predators and Judgements and Confessions

New York plays a unique role in the predatory lending drama. Knowing this can provide a pivotal clue when trying to determine if you are about to become prey. In New York, state law is friendly to confessions of judgement. Cash -advance companies, which are a huge faction of the predatory lending family, almost always make borrowers sign one of these as a loan condition.

If a borrower signs a confession of judgment, they are basically agreeing to lose in a court battle if a dispute arises about repayment. Regardless of where these types of loans take place, almost all of them contain a New York confession of judgement. If you see one of these in your loan documents, run.

Punishment for Paying Early

If they are going to charge a prepayment penalty, you should be wary. Early payment is a good thing, even though the lender loses some interest. It isn’t a deal breaker, but it should definitely cause you to look for other red flags and proceed with caution.

Obviously Seeking the Weak

Senior citizens, those with no credit or bad credit, minorities, those considered low income are all easy targets. They are more likely that others to get tangled up with predatory lenders, according to a 2015 Center for Responsible Lending report. Stay away from lenders that advertise in a way that targets these populations.

Language such as “bad credit doesn’t matter” is a definite sign. In addition, lenders that initiate contact unprovoked and those that try to rush your decision are bad news.

It’s a Bad Deal Now, but They’ll Fix It

Lenders that are searching for prey may try to get borrowers to sign on to a bad deal by promising to make it better in a future refinance. Do not fall for this. A bad deal is a bad deal. Just walk away.

Loan “Flipping” is NOT the Same a House “Flipping”

Flipping a house in real estate terms can actually be very profitable. However, loan flipping is something else altogether, and predatory lenders are great at it. When they see you struggling, they offer a refinance. While it may lower your payments, you end up paying points and fees again. Eventually you end up owing more than ever on your house, car, or whatever it is you used as collateral.

It is a vicious cycle that can bury you quickly.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

The Payment Isn’t “All In”

This is typically and issue with predatory lending in mortgages. Inquire from the beginning as to whether there will be an escrow account set up for your required tax and insurance payments. Lenders that are not on the up and up will often make payments look super low because they do not include all the costs a borrower is responsible for.

What Are Some Questions I Can Ask to Help Discern Between Good Creditors and Predators?

Protecting yourself means recognizing these signs, they will not always be obvious. Sometimes you need to look a little closer. Asking these questions, whether to yourself or to the lender, can help you get to the root of the issue.

Is the offer too good to be true?

As with almost anything in life, if it seems too good to be true, it probably is.

What does the product truly cost?

If the lender doesn’t spell it out for you, do the math yourself. If you need help understanding it all, find someone you trust that can walk you through it. You need to know exactly what this loan is going to cost you. That means all fees, points, insurance, and taxes need to be clear before you can make an educated decision.

Does the lender check my ability to repay?

It is ridiculous to think you will get a loan without the lender ensuring you can repay. It doesn’t have be a credit check. If they do not at least verify income or employment however, there is almost certainly a problem.

Does the lender help me build credit?

Not all lenders do this, but if they do help you build your credit score, it is a point in their favor.

Does the lender require electronic payments?

While there is nothing wrong with paying electronically, the requirement that electronic payments are the only way you can pay should throw up a red flag.

Have others complained about the lender?

Check out reviews online. Look them up on the Better Business Bureau’s website at BBB.org. Find out if others have had a good experience with the lender, or not.

Is Anyone Doing Anything to Separate Creditors and Predators?

In recent years there has be a push by legislators to put an end to predatory lending practices. There have been safety nets in place for far longer however. What is being done? Does anyone care? Actually, yes, they do.

The Truth in Lending Act

It really started way before now with the Truth in Lending Act of 1968. This Act requires that lenders clearly communicate the sum of all payments, APR, and amount to be paid in interest and fees. In addition, the total credit that is being extended must be made clear. All of this has to be disclosed before a loan contract is signed.

Another component of the Truth in Lending Act is that a borrower has the right of rescission. This means that with certain loans, borrowers have three days to cancel after signing.

The Consumer Financial Protection Bureau

After the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the Consumer Financial Protection Bureau was born. The goal of the CFPB is to help oversee federal laws that protect consumers financially. They have resources that can help borrowers learn to decipher loan terms and risks, and also help them report and resolve any complaints they may have against lenders.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

Signs of a Good Lender

Telling the difference between good creditors and predators means more than just knowing how to spot the bad guys. There are things to look for that can clue you in as to whether a lender is actually good, or if they are just not a predator. There is a gray area, and even reputable lenders can fall into poor practices.

Knowing that, keep in mind that legitimate lenders will always check your ability to pay. They may rely on a credit check or some other means. In addition, they will not pressure you. The best will actually offer tools to help educate you financially so that you can better understand the details of the loan.

Also, a good lender will have few complaints. Consumers will almost always complain liberally if they feel like they were ripped off. In addition to BBB.org, check out the CFPB Complaint Database and the Federal Trade Commission’s scam alerts. While even good lenders get complaints occasionally, a long history of dissatisfied customers is a huge warning sign.

Other Ways to Protect Yourself

Like I said, the best way to know the difference between creditors and predators, and avoid becoming a predator’s prey, is to educate yourself. Here are some additional sources for doing just that:

The Money & Credit pageon the Federal Trade Commission’s website has tons of educational articles on a broad variety of topics including debt, credit and loans.

The Ask CFPB pageincludes answers to hundreds of questions related to personal finance, many of which you can apply to business finance as well.

The attorney general’s officein your specific state will be able to help if you need to submit complaints. They can also help you understand consumer protections in your own area.

Learn the Difference Between Legit Creditors and Predators to Avoid Problems with Personal and Business Finance

Predatory lending is prevalent in the realm of personal finance, but that does not mean that business finances are unaffected. Many business loans are dependent on personal credit scores, which a bad loan from a predatory lender can devastate. This is one reason building business credit is so important.

The fact is, however, a bad loan is like a predatory parasite. It seeks out the weak, and once it attacks, it attaches itself to your finances and plagues every aspect of them, even slipping to the business realm if left unattended. It can cause devastation that could last for years. Don’t let it happen to you. Learn the signs, and make sure you can tell the difference between creditors and predators.

How to Tell the Difference Between Legit Creditors and Predators Out to Eat You Alive

Watch any animal reality show and you will see what happens between predators and prey. In a similarly menacing way, some lenders actually prey on unsuspecting borrowers. Not only do they leave finances in ruins, but often the trail of destruction trails across their entire lives. They basically eat their prey alive. How can you avoid falling victim to these devilish creatures? We are going to show you how to tell the difference between legit creditors and predators, so that you can survive in the credit wilderness.

Know Thy Enemy: What is Predatory Lending

According to Investopedia: “Predatory lending benefits the lender and ignores or hinders the borrower’s ability to repay a debt. These lending tactics often try to take advantage of a borrower’s lack of understanding concerning loans, terms, or financial literacy.”

Basically, just like predators in the wild, predatory lenders take advantage of the weak. They look for those that are unassuming, easily tricked into coming closer, and without suitable defenses. Then they pounce.

In the wild, predators often disguise themselves as something else. Consider the venus fly trap. To the fly, it looks like a flower. The fly saunters over to enjoy the beauty, and snap! It’s gone before it even knows what hit it. That is the peril of a predatory lender. It looks great, inviting even. Before you know it, however, they trap you. The best protection you can have is to know the difference between creditors and predators. Don’t be fooled. Learn the signs and build your defenses. Know thy enemy.

Common Signs that a Creditor is Actually a Predator

The only way to tell the difference between creditors and predators is to know the signs of a predator. They are not that hard to spot if you know what tricks to look for.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

Payment is King

If you are trying to get a loan and the “creditor” continues to emphasize what your payment will be, while downplaying how much the actual loan is, that creditor might be a predator. While a monthly payment is obviously important for budgeting purposes, you need to know all the terms of the loan.

A lender can use many tactics to ensure your monthly payment is where you need it to be to fit your budget. They can increase the loan period, adjust terms, and add balloons to make things look much better than they really are. The result is that you get a really bad loan in exchange for a temporary lower payment.

Burst the Balloon

Speaking of balloon loans, those are also a common predatory lending practice. They use them to provide unsuspecting borrowers with a low monthly payment for most of the loan. Most borrowers do not realize that they are typically only covering the interest for each month.

In fact, usually the principle isn’t reduced at all by payments until the very end of the loan. The final payment ends up being a large “balloon” payment that should pay off the entire principal of the loan all at once. Most of the time borrowers are not prepared for this, and they end up either refinancing or defaulting.

Unpack the Packing: Unnecessary Baggage

Packing is another practice that predatory lenders seem to lean towards. It involves them adding extras onto the loan. You do not need these extras, and they add them without your knowledge. The most common culprits are insurance products that are not necessary for your situation. You pay for them without realizing it, and they offer you no benefit.

Excessive Points and Fees

It’s not uncommon for lenders to charge points and fees on a loan. It is a practice that some use to increase profits. As a general rule, one point is worth one percent of the loan balance.

Asking for more points and higher fees than is normal for the type of loan you are getting can be a sign of predatory lending. If you feel that is what is going on, dig deeper.

How do you know what is “normal” and what is excessive? As a general rule, three points, or 3% of the loan amount or less, is a decent deal. This includes appraisals and title insurance, which are necessary. Research to see what is normal for your area, but know this is a good rule of thumb.

The New York Connection: Of Creditors and Predators and Judgements and Confessions

New York plays a unique role in the predatory lending drama. Knowing this can provide a pivotal clue when trying to determine if you are about to become prey. In New York, state law is friendly to confessions of judgement. Cash -advance companies, which are a huge faction of the predatory lending family, almost always make borrowers sign one of these as a loan condition.

If a borrower signs a confession of judgment, they are basically agreeing to lose in a court battle if a dispute arises about repayment. Regardless of where these types of loans take place, almost all of them contain a New York confession of judgement. If you see one of these in your loan documents, run.

Punishment for Paying Early

If they are going to charge a prepayment penalty, you should be wary. Early payment is a good thing, even though the lender loses some interest. It isn’t a deal breaker, but it should definitely cause you to look for other red flags and proceed with caution.

Obviously Seeking the Weak

Senior citizens, those with no credit or bad credit, minorities, those considered low income are all easy targets. They are more likely that others to get tangled up with predatory lenders, according to a 2015 Center for Responsible Lending report. Stay away from lenders that advertise in a way that targets these populations.

Language such as “bad credit doesn’t matter” is a definite sign. In addition, lenders that initiate contact unprovoked and those that try to rush your decision are bad news.

It’s a Bad Deal Now, but They’ll Fix It

Lenders that are searching for prey may try to get borrowers to sign on to a bad deal by promising to make it better in a future refinance. Do not fall for this. A bad deal is a bad deal. Just walk away.

Loan “Flipping” is NOT the Same a House “Flipping”

Flipping a house in real estate terms can actually be very profitable. However, loan flipping is something else altogether, and predatory lenders are great at it. When they see you struggling, they offer a refinance. While it may lower your payments, you end up paying points and fees again. Eventually you end up owing more than ever on your house, car, or whatever it is you used as collateral.

It is a vicious cycle that can bury you quickly.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

The Payment Isn’t “All In”

This is typically and issue with predatory lending in mortgages. Inquire from the beginning as to whether there will be an escrow account set up for your required tax and insurance payments. Lenders that are not on the up and up will often make payments look super low because they do not include all the costs a borrower is responsible for.

What Are Some Questions I Can Ask to Help Discern Between Good Creditors and Predators?

Protecting yourself means recognizing these signs, they will not always be obvious. Sometimes you need to look a little closer. Asking these questions, whether to yourself or to the lender, can help you get to the root of the issue.

Is the offer too good to be true?

As with almost anything in life, if it seems too good to be true, it probably is.

What does the product truly cost?

If the lender doesn’t spell it out for you, do the math yourself. If you need help understanding it all, find someone you trust that can walk you through it. You need to know exactly what this loan is going to cost you. That means all fees, points, insurance, and taxes need to be clear before you can make an educated decision.

Does the lender check my ability to repay?

It is ridiculous to think you will get a loan without the lender ensuring you can repay. It doesn’t have be a credit check. If they do not at least verify income or employment however, there is almost certainly a problem.

Does the lender help me build credit?

Not all lenders do this, but if they do help you build your credit score, it is a point in their favor.

Does the lender require electronic payments?

While there is nothing wrong with paying electronically, the requirement that electronic payments are the only way you can pay should throw up a red flag.

Have others complained about the lender?

Check out reviews online. Look them up on the Better Business Bureau’s website at BBB.org. Find out if others have had a good experience with the lender, or not.

Is Anyone Doing Anything to Separate Creditors and Predators?

In recent years there has be a push by legislators to put an end to predatory lending practices. There have been safety nets in place for far longer however. What is being done? Does anyone care? Actually, yes, they do.

The Truth in Lending Act

It really started way before now with the Truth in Lending Act of 1968. This Act requires that lenders clearly communicate the sum of all payments, APR, and amount to be paid in interest and fees. In addition, the total credit that is being extended must be made clear. All of this has to be disclosed before a loan contract is signed.

Another component of the Truth in Lending Act is that a borrower has the right of rescission. This means that with certain loans, borrowers have three days to cancel after signing.

The Consumer Financial Protection Bureau

After the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the Consumer Financial Protection Bureau was born. The goal of the CFPB is to help oversee federal laws that protect consumers financially. They have resources that can help borrowers learn to decipher loan terms and risks, and also help them report and resolve any complaints they may have against lenders.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

Signs of a Good Lender

Telling the difference between good creditors and predators means more than just knowing how to spot the bad guys. There are things to look for that can clue you in as to whether a lender is actually good, or if they are just not a predator. There is a gray area, and even reputable lenders can fall into poor practices.

Knowing that, keep in mind that legitimate lenders will always check your ability to pay. They may rely on a credit check or some other means. In addition, they will not pressure you. The best will actually offer tools to help educate you financially so that you can better understand the details of the loan.

Also, a good lender will have few complaints. Consumers will almost always complain liberally if they feel like they were ripped off. In addition to BBB.org, check out the CFPB Complaint Database and the Federal Trade Commission’s scam alerts. While even good lenders get complaints occasionally, a long history of dissatisfied customers is a huge warning sign.

Other Ways to Protect Yourself

Like I said, the best way to know the difference between creditors and predators, and avoid becoming a predator’s prey, is to educate yourself. Here are some additional sources for doing just that:

The Money & Credit pageon the Federal Trade Commission’s website has tons of educational articles on a broad variety of topics including debt, credit and loans.

The Ask CFPB pageincludes answers to hundreds of questions related to personal finance, many of which you can apply to business finance as well.

The attorney general’s officein your specific state will be able to help if you need to submit complaints. They can also help you understand consumer protections in your own area.

Learn the Difference Between Legit Creditors and Predators to Avoid Problems with Personal and Business Finance

Predatory lending is prevalent in the realm of personal finance, but that does not mean that business finances are unaffected. Many business loans are dependent on personal credit scores, which a bad loan from a predatory lender can devastate. This is one reason building business credit is so important.

The fact is, however, a bad loan is like a predatory parasite. It seeks out the weak, and once it attacks, it attaches itself to your finances and plagues every aspect of them, even slipping to the business realm if left unattended. It can cause devastation that could last for years. Don’t let it happen to you. Learn the signs, and make sure you can tell the difference between creditors and predators.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.