Senior full-stack software engineer with over 7 years of experience, currently working at Postman Inc., previously at SAP and Genpact. I am programming language and framework agnostic i.e. I can learn and work with any language and/or framework as required. Looking for either fully remote roles or roles with international relocation. It would be great if the role would allow me to work on challenging things. Additionally, I hold an H1B that can be transferred over if required. Please visit my portfolio (https://atchyut.dev) and/or blog (https://blog.atchyut.dev) to learn more about me.

You can join our team of ML, backend (Rust) and frontend (TS, React) engineers and work at the intersection of AI and developer tools.

Using our product, you can ask questions about large codebases in natural language, just like you’d talk to ChatGPT. You can also find code, paths and identifiers using regex and navigate defs/refs using precise code navigation. The project is open source (https://github.com/BloopAI/bloop) and is built from the ground up in Rust and Typescript.

Some highlights from the stack you’ll be working with:

– We ship a Tauri based desktop client, a new Rust based alternative to Electron. By indexing local repos, we bring code search to everyone’s desktop.

– We’re using a new vector search engine qdrant, written in you guessed it – Rust. This powers our low latency semantic retrieval.

– We’re one of the earliest production projects to ship with Anthropic AI’s Claude.

We’re looking for someone experienced, and we’d expect this to be apparent through:

– Creativity, obsession with visual detail and consistency

– Respect for team and process

– A wide comfort zone

– Passion for the craft, eg: mentorship, Open Source contribution or speaking at events

You’ll work predominantly on the frontend, which is deployed to both the desktop and cloud versions of bloop. Our current stack is React, Typescript and Tauri.

We’re an international remote-first team of 7 with offices in London. Preference will be given to those on GMT+/-3 as we’re not an entirely async company and this leaves the necessary overlap to collaborate. We get together about three times per year in-person to hang out.

We just raised $7m from top funds, namely LocalGlobe, Khosla and Sands Capital as well as leaders in the field like Hamel Husain who led GitHub’s code search team. We also host one of the largest meetups on the subject, AI4Code London (https://ai4code-london.github.io/).

If you’d like to explore working with us, please reach out to me at louis [at] bloop [dot] ai with “HN Frontend Engineer” in the subject line and a note about why this is exciting and a link to your portfolio or linkedin/resume.

I am looking for a (preferably remote) frontend role. Most recently I have been working at Microsoft and developed the a redesigned Win11 Windows Search Box navigation feature using React, TypeScript, and SASS/CSS. I created Accessibilities, Right to Left Language Capabilities, Light/Dark/High-Contrast Mode and Visual Parity tests for new features. Also, refactored Bing search suggestion React Components to use as Generic Component to reduce code and increase reusability.

Location: Los Angeles, CA (Currently in Seattle, WA)

Remote: Yes, as well as hybrid

Willing to relocate: (San Diego, Los Angeles, Orange County – I wish to stay/live in California)

If your answer is yes, then you need a detailed guide on how to start a startup.

For those of you who haven’t launched a business before, it can sound like an intimidating task.

Don’t get me wrong – I’m not saying that getting your startup off the ground is an easy mission.

It takes hard work, dedication, money, some sleepless nights, and, yes, some failures before you succeed.

Nearly 20 percent of businesses fail in the first year, and just because you make it beyond 12 months doesn’t mean your startup is going to continue to thrive.

According to government stats, 30.6 percent of businesses fail after their second year, 49.7 percent fail after five years, and 65.6 percent fail after their tenth year.

Once you get your company off the ground, it doesn’t get any easier: you need to work just as hard to keep it going each year.

With that said, it’s useful to have a guide and a set of instructions to follow to learn how to launch a startup.

When I write about launching a startup, I’m talking from personal experience. I’ve created several startup companies like Crazy Egg, Hello Bar, and NP Digital.

I’m happy to share my knowledge and experience to help make things a little easier and less stressful for you as you go through this process.

Realistically, it takes hundreds of stages to launch your company, but I’ve narrowed down the top 7 steps into a blueprint for you to follow if you want to learn how to start a startup and learn how to create and develop your own business.

In the following article, I outline and discuss each step in detail so you have a better understanding of what I’m talking about.

Let’s begin with the basics.

1. Create a Business Plan

Have you heard the saying ‘if you fail to plan, you plan to fail?’ That was the thinking of Founding Father Benjamin Franklin.

Well, research appears to back that up. Study after study shows that businesses with a plan are more likely to succeed. In addition, you can find many articles spelling out the importance of a business plan.

“A business plan is a very important and strategic tool for entrepreneurs. A good business plan not only helps entrepreneurs focus on the specific steps necessary for them to make business ideas succeed, but it also helps them to achieve short-term and long-term objectives.”

It’s pretty straightforward, really. Having an idea is one thing, but having a legitimate business plan is another story.

A proper business plan gives you a significant advantage, but what should you include in a business plan? It helps if you think of it as a written description of your company’s future. Basically, you outline what you want to do and how you plan to do it.

Typically, these plans outline the first three to five years of your business strategy and detail your business’s purpose and aims. Ideally, your document should outline your business goals, strategies, and your plans for achieving them.

Here are the key steps to writing a successful business plan:

Outline your business goals

Describe your target market

Explain your product or service

Detail your marketing and sales strategies

Write down your financial projections and detail the funding

Summarize your overall strategy

If you need some help with your plan, the Small Business Administration has an easy-to-follow guide, along with some templates.

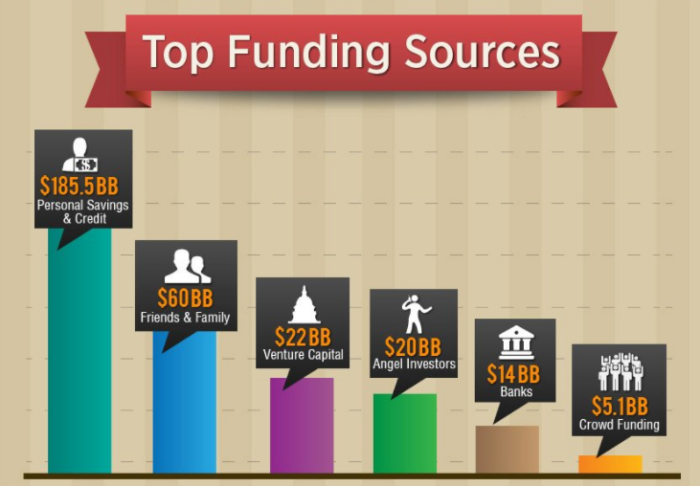

2. Secure Appropriate Funding

Without adequate funding, your business won’t launch or stay afloat long-term. According to Statista, in 2021, there were nearly 840,000 businesses that had been in operation for less than a year. Many of these startups won’t survive because they underestimate the cost of doing business.

Perhaps you’re wondering what level of financing you need? When it comes to raising cash, there’s no magic number that applies to all businesses. The startup costs vary from industry to industry, so your company may require more or less funding depending on the situation.

Costs also vary depending on whether you’re a brick-and-mortar store, e-commerce enterprise, or service business. If you’re unsure how much you might need, try the SBA’S startup cost templates to get a better idea.

Online startup loans, which you can apply for online and pay back over time, with interest.

SBA microloans, providing up to $50,000 in loans for start-up businesses. The main advantage is the lower interest rates.

Lines of credit, which is a type of loan available in both secured and unsecured formats.

Invoice factoring/financing, a process in which a business sells its invoices to a third party, at a discount.

Friends/family/personal loans, which are unsecured loans.

Business loans, which you pay back over an agreed period.

Angel investors, who have considerable wealth and give seed funding to start-up businesses.

Crowdfunding, where you raise money from a group of investors online.

Let’s circle back to our business plan for a minute.

All business plans contain a financial plan. This usually includes a:

Balance sheet, which displays your business’s assets, liabilities, and owner’s equity of the company.

Sales forecast, which predicts future sales.

Profit and loss statement, which details your earning and spending patterns. This figure helps calculate your net income.

Cash-flow statement, or financial statement detailing how much your business has spent and generated.

You use these financial statements to determine how much funding you need to launch successfully. Additionally, you may discover that the number is significantly higher than you originally anticipated.

For example, I’m sure you’ve heard someone say, “That would make a great app,” or “I should make an app for this.”

Do you know how much it costs to make an app? Depending on the complexity, you’re looking at anything between $40,000 – $300,000, and that’s just to make it.

This is the point I’m making: to secure the appropriate funding, you need to find out how much money you need.

To find this number, you must research and predict realistic financials in your business plan.

Let’s say you discover that your startup needs $100,000 to get off the ground.

What if you don’t have $100,000?

You’ve got some options, like bank loans and commercial lenders, and that’s the way many small businesses go. With this said, banks are less likely to give large amounts of money to new companies with no income or assets to default on, which may make it hard for your typical startup to get the funding they need.

Don’t worry, your dream isn’t dead yet. You can find investors. They could be:

However, whichever method you use, proceed carefully because you don’t want to start giving away significant equity in your company before you launch.

Then, if you get lucky and find a potential investor, you need to know how to pitch your idea quickly and effectively. Here are some tips to help you do that:

Memorize your financial numbers; ensure you know them inside out.

Refer to your business plan and ensure your financial figures cover the costs.

Make sure your business plan is presentable so you can give potential investors a copy.

Practice and perfect your pitch.

One more thing: It’s imperative that your business plan has a proper executive summary to entice busy investors.

Once you secure the appropriate funding, you can proceed to the next step of how to start a startup business: finding the right people.

3. Surround Yourself With the Right People

No one makes it on their own. William Proctor might not have been a high-profile, successful businessman if he hadn’t met James Gamble.

Where would we go for advice if Larry Page hadn’t met Sergey Brin? Not Google, that’s for sure.

Then what if Ben Cohen never met Jerry Greenfield? We would’ve been denied one of the world’s most famous ice cream brands.

Even if you’ve already got a co-founder in place, you need some core staff.

CEO and COO. Between them, they develop a vision and put it into action.

Product Manager, who is responsible for taking a product from its development stages and onto the market.

Chief Technology Officer, who works with executive members to oversee the technical side of a business.

Chief Marketing Officer, whose job involves creating a marketing strategy and executing it.

Sales Manager, for managing customer relationships, selling products/service, and motivating the team.

Chief Finance Officer, who manages the financial planning and decisions for a company.

Business Development Officer. This is a varied role that involves drawing up a business plan, establishing funding, and building customer/relationship funding.

Customer Service Officer, who assists customers with their questions, any complaints, and providing product information.

However, your business structure depends on the industry, so look at the above as definitive.

When you’re just starting up, hiring an entire team often isn’t realistic, and you find yourself wearing several business hats. That’s OK, to an extent. Just remember to play to your strengths and outsource if you can’t afford to recruit.

That said, there are some experts you should consider essential, including a:

Lawyer

Accountant

Financial advisor

Unless you’re an expert in law, finances, and accounting, these three people can help save your business some money in the long run.

They can explain the legal requirements and tax obligations based on how you structure your business. For example, it could be a:

Sole proprietorship

Partnership

Corporation

Limited liability company

While your lawyer, accountant, and financial advisors are not necessarily employees on your payroll, they are still important people to surround yourself with.

Finally, for this section, don’t forget the fundamentals for starting any company:

Get a federal ID number from the IRS. The IRS lets you submit your business information online to get your employer identification number (EIN).

Get insured: Shop around and find an insurance agent who can get you plenty of coverage at an affordable rate.

Now that you’ve got staff, you need to start work on a website and find a place to base your business.

4. Find a Location and Build a Website

Now you’re ready for the next stage of your how-to start a startup plan: finding a physical location and setting up a website.

Whether it’s offices, retail space, or a manufacturing location, you need to buy or lease a property to operate your business.

Unless you’re working from a home office, your two main options are leasing or ownership. Leasing usually works as out more expensive long term; however, don’t just base your decision on costs. Leasing and ownership both have their pros and cons. Look at the whole picture before making a decision.

I appreciate that it may not be realistic for all entrepreneurs to tie up the majority of their capital in real estate.

Strategize for this in your business plan and try to secure enough funding so that you can afford to buy property. It’s worth the investment and can save you money in the long run.

Let’s move on to setting up a website.

Today, your company can’t survive without an online presence. Don’t wait until the day your business officially launches to get your website off the ground, either, and remember, it’s never too early to start promoting your business.

If customers are searching online for a service in your industry, you want them to know that you exist, even if you’re not quite open for business yet.

The beauty of an online presence is you can even start generating some income through your website before you find premises. If it’s applicable, start taking some pre-orders and scheduling appointments.

Here are some tips about how to launch and promote a successful website:

When designing a website, it is important to keep the user in mind. The layout of the website should be easy to navigate and use. The colors and fonts should be easy on the eyes.

Make your website visually appealing. Use eye-catching images and dynamic designs to make the website stand out from the competition.

Keep the content of the website fresh and up-to-date to keep users coming back to visit your site. Your website is an ideal place to keep your audience up-to-date with a glimpse inside your company, product launches, and, of course, the details of your business premises.

Another important thing to keep in mind is usability. Your site should be easy to use on all devices, from desktop computers to smartphones and tablets.

I’ve got a video tutorial that explains how to speed up your website.

All of these items combined may sound tough, but it’s really not that difficult. Just focus on one task at a time, and you’ll get there.

Once your website is up and running, you need to expand your digital presence. To do this, use social media platforms like:

Facebook

Twitter

Instagram

TikTok

Linkedin

Snapchat

Your prospective customers are using these platforms, so you need to be on them, too. However, when choosing a platform, ensure you go where your core audience is. For instance, if you’re targeting a younger market, TikTok may be ideal.

5. Become a Marketing Expert

If you’re not a marketing expert, you need to become one.

You might have the best product or service in the world, but if nobody knows about it, then your startup can’t succeed.

To start spreading the word, you must learn how to use digital marketing techniques like:

Content marketing

Affiliate marketing

Email marketing

Search engine optimization (SEO)

Social media marketing (SMM)

Search engine marketing (SEM)

Pay-per-click advertising (PPC)

However, if you’re starting a small business in a local community, some of the traditional methods can still work well. Think:

For those of you who aren’t efficient marketers, there is no shame in hiring a marketing director or even a marketing team, depending on the size of your company.

Your marketing efforts will be one of the most important, if not the most important, components of launching your startup business. To improve your chances of success:

Allocate a marketing budget.

Determine how you’re going to distribute this money across different channels.

Have a plan and try to maximize your return on investment for each campaign.

Take these numbers into consideration before you spend your entire budget on something like banner ads.

If you’re following this plan in order, the good news is that you’re already on the right track to building a customer base.

Starting a website, growing your digital presence, and becoming an effective marketer are all steps in the right direction. However, now it’s time to put these efforts to the test. That means:

Opening your doors (or website) for business.

Getting a customer to make a purchase is the first step.

Retaining customers.

There are three keys to customer retention:

Customer service

Customer service

Customer service

It’s no secret. The customer needs to be your main priority. They are the lifelines of your business, and they need to be treated accordingly.

Once you establish a steady customer base, you can use it to your advantage.

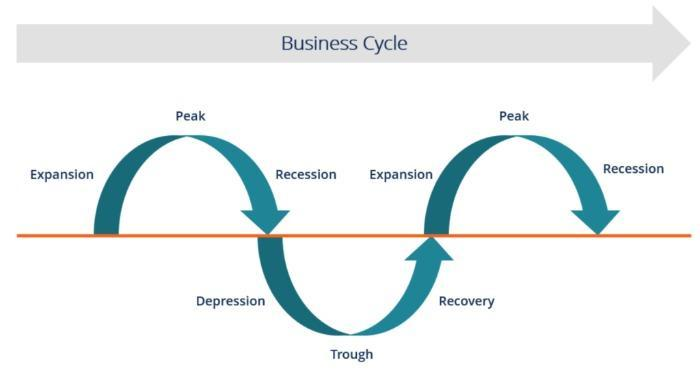

As illustrated above, you face peaks and valleys while your company operates.

Mistakes and setbacks happen.

Some of these things will be out of your control, like a natural disaster or a crisis with the nation’s economy.

Employees will come and go.

You’ll face tough decisions and crossroads.

Sometimes, you’ll even make the wrong decision.

That’s OK.

Part of being an entrepreneur is learning from your mistakes.

It’s important to recognize when you’ve done something wrong, move forward, and try your best to make sure it doesn’t happen again.

Pay your bills.

Pay your taxes.

Operate within the confines of the law.

As long as you’re doing these things, you’ll be able to fight through any obstacle your startup company faces in the future.

FAQs

How Do I Start a Startup?

Check if your idea is viable. Do some research and ask around. Are people looking for a business/service like yours? Then ask yourself: How are other businesses in your sector performing? Have you spotted a genuine gap in the market? Then you’re ready to start drawing up a business plan.

Where Can I Acquire Startup Funding?

There are several sources, including personal financing, banks, crowdfunding, friends, family, angel investors, and venture capitalists.

Do I Need a Website to Launch My Startup?

In the vast majority of cases, yes. You also need a social media presence that is applicable to your audience. After all, social media is a free, efficient way to reach a huge volume of people that you couldn’t otherwise target.

How Can I Use Marketing to Launch My Startup?

It depends on your budget. Begin with strategies like social media, free press release distribution, and content marketing. As your business grows, you can allocate a budget for affiliates, email marketing, SEO, online ads, and influencer campaigns.

The percentage of entrepreneurs in the United States is growing strong, and each one of them is going to face challenges along the way.

With that said, having a proper blueprint to follow helps simplify the process. You can get learn the basics of how to start a startup by following the seven steps, and adapting them to suit your individual needs.

With that said, most successful businesses start with validating an idea, creating a comprehensive business plan, and raising adequate funding. Without proper financial planning, your startup doesn’t stand a chance.

Then, surround yourself with the right people and play to your strengths.

For instance, if you’re great at organizing and motivating, focus on that; If marketing just isn’t you, outsource it to a professional who excels in that area.

Don’t forget about lawyers, insurance agents, and accountants to keep your business in order, and make sure you have essentials like an online presence.

Launching your startup is an imperfect journey, and you must prepare for unforeseen circumstances. However, proper planning and execution help limit these hurdles and get your business off to a flying start.

How will you raise funding to get your startup company off the ground?

BitMEX | Analytics team | CH / CA (BC) / SG / HK / Remote (VISA)

Derivatives exchange, USD 1 trillion/y turnover; ~100TB of relational internal data now, PB-scale external sources later; Redshift, PostgreSQL, Tableau, kdb+, legacy Python but open to Haskell/Mercury/Idris on Nix, Rust, Zio, Kotlin, OCaml for new projects.

Spend the morning supporting users then handover to the next time zone. Afternoon for undisturbed R&D.

Mid-level IC roles. Work entirely remotely, subject to regulatory considerations. We can relocate you to Zurich (Switzerland), Singapore, Hong Kong or Vancouver (Canada). Experience programming smart contracts or trading in DeFi is appreciated by management.

Process: filter question > ~1-4h take home test > culture fit call > offer.

Did you know you can apply for credit in your business name and it won’t hit your personal credit report? You can, no matter what is happening with the economy! There’s a trick to it though. You have to set your business up properly, and you have to apply with the right information. It is possible to get business credit without SSN being an issue.

Get Business Credit without SSN and Make Your Business More Fundable

When you get business credit without using your SSN, you take the first step in obtaining credit in the name of your business. That is separate credit that only affects the credit score of your business, not your personal credit score.

Of course, there is way more to separating business credit from personal credit than knowing how to get business credit without SSN, but that is definitely a place to start.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit, even in a recession.

Get Business Credit Without SSN

There is really no amazing trick to this. You can easily get business credit without SSN by simply using an EIN (Employer Identification Number) in place of the SSN on credit applications. That one simple step will disconnect debt taken in the name of your business from your personal debt. Again, there are a few more steps to keep it completely separate but, this is huge and very simple.

You can get an EIN for free on the IRS website. Just go to IRS.gov and apply. The process is fast. Once you have that number, you have taken the first step in building credit for your business separate from yourself. This is the pivotal step getting business credit without your SSN.

It is important to note that you may have to provide your SSN for identification purposes to help prevent fraud. However, this is different than getting credit using your SSN. If you use your social security number for identification purposes only, the debt will still not be connected to it.

Separate Your Bank Accounts

You have to open a separate, dedicated business bank account. There are a few reasons for this. First, it will help you keep track of business finances. It will also help you keep them separate from personal finances for tax purposes.

There’s more to it however. There are several types of funding you cannot get without a business bank account. Many lenders and credit cards want to see one with a minimum average balance. In addition, you can’t get a merchant account without a business account at a bank. The result is, you cannot take credit card payments. Studies show shoppers usually spend more when they can pay by credit card.

Kick Your Business Out of the Nest! Separate Contact Info Is a Must

Your business needs its own phone number, fax number, and address. You can still run your business from your home or on your computer. You don’t even have to have a fax machine.

In fact, you can get a business phone number and fax number that will work over the internet instead of phone lines without a lot of trouble. In addition, the phone number will forward to any phone you want it to. You can simply use your personal cell phone or landline if you want. Whenever someone calls your business number it will ring straight to you.

Faxes can be sent to an online fax service, if anyone ever happens to actually fax you. This part may seem outdated, but it does help your business appear legitimate to lenders.

You can use a virtual office for a business address. How do you get a virtual office? What is that? It’s not what you may think. This is a business that offers a physical address for a fee, and sometimes they even offer mail service and live receptionist services. In addition, there are some that offer meeting spaces for those times you may need to meet a client or customer in person.

Make Sure Your Website and Email Address are In Synch

What does a website and email address have to do with business funding? These days, you do not exist if you do not have a website. However, having a poorly put together website can be even worse. It is the first impression you make on many, and if it appears to be unprofessional it looks bad to lenders as well as customers.

Spend the time and money necessary to make sure your website is professionally designed and works well. Pay for hosting too. Don’t use a free hosting service. Along these same lines, your business needs a dedicated business email address. Make sure it has the same URL as your Website. Don’t use a free service such as Yahoo or Gmail.

Incorporate

Incorporating your business as an LLC, S-corp, or corporation is non-negotiable. It lends credence to the legitimacy of your business. It also offers some protection from liability.

Which option you choose does not matter as much for fundability as it does for your budget and needs for liability protection. The best thing to do is talk to your attorney or a tax professional.

Now, incorporation is important to business credit building. However, so is time in business. The longer you have been in business the more fundable you appear to be. Time in business starts on the date of incorporation, regardless of when you actually started doing business. That means, it is vital to incorporate as soon as possible.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit, even in a recession

Where to Start to Get Business Credit without SSN

Once you have these things in place, you can start applying to get business credit without SSN, but with your EIN. Don’t just jump into credit cards. It helps to begin with starter vendors. There are a few out there.

Starter vendors are vendors that sell items you use everyday in the course of business. They will extend credit in the form of net terms on invoices without a credit check. Then, they will report payments on those invoices to the business credit reporting agencies.

If you have followed the steps, then when they report those payments, they will be reporting in your business name to the business credit reporting agencies such as Dun & Bradstreet, Equifax, and Experian. This is how you start to build your business credit score.

Get Business Credit Without SSN: What Next?

After you get enough starter vendor accounts reporting, you’ll be able to apply for other types of cards and without your SSN. The key is to apply for certain types of cards in a specific order. For example, it is best to start with store cards. These are cards that are issued with a specific store name. Typically, you can only use them at that specific store or on that store’s website. Examples include Office Depot and Best Buy. Some fleet cards fall into this category as well.

Fleet cards are cards that you can only use for fuel or auto repair and maintenance. It is usually easier to get approval for these cards after you have several starter vendors and store cards reporting. Examples of fleet credit cards include Fuelman and Shell.

After enough of these types of accounts are reporting to the business credit reporting agencies in your business name, with your EIN, then you can apply for general use credit cards. Those are the credit cards you can use anytime, anywhere, on anything. Usually, they have the best interest rates and rewards. They also have the highest credit limits, meaning you have instant access to the funds you need to run your business day in and day out.

Get Business Credit With SSN: A Warning

Here are a few key things to remember when you get business credit without SSN.

First, the whole point is to separate your business credit from your personal credit. Why do this? There are a few reasons. For example, you typically get a higher credit limit when you get credit related to your business with an EIN than you would with your SSN.

Another reason, however, is so that your personal credit is not affected if you have problems on your business credit report. However, you want your business credit to be strong also. The only way to make this happen is to handle your credit responsibly. Do not bite off more than you can chew. Make your payments regularly and on-time. Bad business credit is just as harmful as no business credit.

Keep and Eye on Your Business Credit

It’s important to keep an eye on your business credit while you are going through this process. Once you get business credit without SSN, you’ll need to keep tabs on which accounts are reporting, how many accounts are reporting, and what your score looks like. This is how you will know when it is time to apply for other types of cards.

It is also how you will know when there is a mistake. If you do see a mistake, you can contest it in writing to have it removed.

When it comes to business credit monitoring, there are a few different credit reporting agencies. The main three we have already mentioned. They include Dun & Bradstreet, Experian, and Equifax. There are others as well, but if you know what your business credit score is with the main three, you can have a good idea of what it is with any credit reporting agency.

Funding in the Meantime

It takes some time to get business credit without SSN. If you need money to run your business quickly, while you work through the process, you might consider a credit line hybrid. This is revolving, unsecured financing that allows you to fund your business without putting up collateral. Furthermore, you only pay back what you use.

It’s easier than you may think to qualify. You can do so with a personal credit score that is way below what you would need to get approval for a term loan or line of credit at a traditional bank. The minimum is 685. Even if you did get approval at a traditional bank with this score, your interest rate would be much more than what is typical with a credit line hybrid.

In addition to meeting the minimum credit score requirement, you can’t have any liens, judgments, bankruptcies or late payments. Also, in the past 6 months, you should have less than 5 credit inquiries, and less than a 45% balance on all business and personal credit cards. While it is preferred that you have established business credit as well as personal credit, it is possible to qualify without business credit. In fact, a credit line hybrid can help build business credit.

What If I Don’t Qualify?

If you do not meet all of the requirements, there is still a chance. You can take on a credit partner that meets each of these requirements. Many business owners work with a friend or relative to fund their business. If a relative or a friend meets all of these requirements, they can partner with you to allow you to tap into their credit to access funding.

What Makes a Credit Line Hybrid A Good Option?

There are many benefits to using a credit line hybrid. First, it is unsecured, meaning you do not have to have any collateral to put up. Next, you do not have to provide any bank statements or financials.

Also, typical approval amounts are up to 5x that of the highest credit limit on the personal credit report. Additionally, interest rates can go as low as 0% for the first few months. You can put that savings back into your business.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit, even in a recession

The process is pretty fast, especially with a qualified expert to walk you through it. One other benefit is this. With the approval for multiple credit cards, competition is created. This makes it easier to get interest rates lowered and limits raised every few months.

Get Business Credit Without SSN and Have Access to Funding to Run and Grow Your Business

One of the largest parts of establishing business credit is to get business credit without SSN. If you use your SSN to apply, that account is going to end up on your personal credit report. This is the opposite of what you want. However, using an EIN instead of an SSN is not enough. You have to follow the other steps to create separation between you and your business. Then, you will be well on your way to building business credit separate from your personal credit. Now is a great time to get started.

Just How To Start Investing In The Stock Market The very best method to begin purchasing the securities market is to select a location of competence. When you begin purchasing the stock exchange, you intend to choose from firms that do organisation in an area with which you are currently acquainted, or that sell a …

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.