Article URL: https://jobs.lever.co/qventus/c0d604cf-ec1c-48ea-847d-5ffc7a67698d Comments URL: https://news.ycombinator.com/item?id=27421523 Points: 1 # Comments: 0

Category: Business News

Business News

How to Get Funding for Women Owned Companies

Women owned companies are exploding onto the scene. In fact, you may be surprised to learn that companies such as Cisco, Liquid Paper, The Body Shop, Spanx, and Proactive are all owned by women.

What Women Owned Companies Need to Succeed

Women owned companies are definitely becoming a force in the entrepreneurial world. According to Fundera, 40% of US businesses are owned by women. If you are ready to join the ranks, here is what you need to know.

Women Owned Companies: Start Off On the Right Foot

All businesses, including women owned companies, need strong fundability. This starts with how your business is set up. The first part of this is separating the business from yourself. This starts with having separate contact information, meaning you do not use your personal address or telephone number as your business address or telephone number.

That sounds easy enough. However, many entrepreneurs, especially women, choose to start their business from their residence. It makes sense. In theory, a female business owner could better manage a home and children if running a business from home. Even a woman, or a man for that matter, without a family could find benefit in the flexibility of running their own business from home. There is no commute, you cut the cost of buying lunch out, and you can work in your pajamas.

Foundation of Fundability

While some would argue these things are not all they’re cracked up to be, one thing is for sure. It is definitely tempting to use your personal contact information as your business information if you work from home. There are two things you need to know about this.

What frustrates you the most about funding your business? Check out how our free guide can help.

Contact Information

First, regardless of where you run your business from, you do not need to use your personal contact information as your business contact information. Second, you can still run your business from your home and still have separate contact information for your business.

The phone number part is easy. You could get a separate phone, but it isn’t necessary. It is easy enough to get a number that works through the internet. You can then forward it to your regular phone, and whenever someone calls your business number it will ring to your personal phone.

An address is a little trickier, but not impossible. Whatever you do, don’t use a P.O. Box or an UPS box. Many types of funding will not accept this type of address. They want to see a physical address.

Other Setup Information

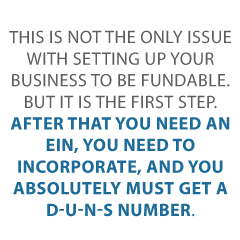

This is not the only issue with setting up your business to be fundable. But it is the first step. After that you need an EIN, you need to incorporate, and you absolutely must get a D-U-N-S number. You also have to open a dedicated business bank account.

The whole point in setting up your business to be fundable is so that you can get funding for your business. There is a huge catch 22 here, as if you are already running a business and are not yet set up to be fundable, you may need money before you can get it done. The set up is only one piece of the fundability puzzle. There are over 100 different fundability factors that lenders consider. Building business fundability takes time.

Best Funding for Women Owned Companies Right Now

The problem is, the longer you wait, the hard it gets to build fundability. Not only that, you need money now, right? How do women owned companies get the funds they need to grow and thrive, or just survive, in the meantime? We have a few suggestions.

Credit Line Hybrid

The credit line hybrid is unsecured business financing. It is available to pretty much anyone for any type of business expense. You can use it for real estate, equipment, working capital, and even startup expenses. Not only that, but there is no security required. Furthermore, there is no down payment, and you do not have to provide income documentation. It is completely no-doc financing.

You do need to have personal credit of 680 or above. Also, there cannot be any late payments in the past 12 months, there can be no open collections or bankruptcies, and there should be less than 4 inquiries in the past 6 months on your consumer credit report. There also has to be at least 2 open credit cards with a $2,000 limit or higher with 2 years of good payment history.

If you do not meet these requirements, you can take on a credit partner that does meet them. The payments will still be reported on the business’s credit report, so business credit will build whether you get the financing yourself or through a credit partner.

You can get up to $150,000, and often interest rates are as low as 0% for the first 6 to 18 months.

Business Revenue Lending

If your business has consistent revenue of $120,000 per year or more, you may qualify for this type of funding. Lenders verify revenue using bank statements. There can be no recent bankruptcies, but the minimum credit score to qualify is as low as 500.

A business must also be in operation for a year or more, and they must do over 5 small transactions each month to get business revenue financing.

What frustrates you the most about funding your business? Check out how our free guide can help.

Merchant Cash Advance

If your business accepts credit card payments and you have at least a 500 FICO, you could get up to $750,000 in a merchant cash advance. Credit rates are usually lower compared to traditional financing as well.

Your business must bring in $100,000 or more per year in credit card sales, and typically you can get approval equal to one months credit card financing volume.

Account Receivable Financing

Outstanding account receivables can also be a source of funding for your business. Get as much as 80% of receivables advanced in less than 24 hours. You get the rest of the accounts receivable amount once you collect full payment for the invoice. Closing takes 2 weeks or less.

Receivables should be with the government or another business. Getting financing with receivables from individuals is not as easy. If you also have purchase orders, then you can get financing to have those filled. You won’t need to use your cash flow to do so.

Equipment Financing

You can secure this type of financing by using existing equipment or new equipment you want to purchase as collateral. Funding is available up to $10 million. Terms range from 5 to 60 months, and you need a minimum 550 FICO.

The equipment must be new, and most types of equipment are acceptable, including software.

You’ll need to provide details on the equipment to be financed and, depending on the loan amount and certain risk factors, you may need to show 2 years corporate and personal tax returns.

Enterprise SBA Loans

For these loans you have to have collateral worth up to at least 50% of the loan amount, but you only need a FICO of 620. There also can be no bankruptcies in the past 4 years. Only for profit companies qualify, and they must have positive trends in sales growth. Generally amounts are available of up to $12 million with terms up to 25-years.

What frustrates you the most about funding your business? Check out how our free guide can help.

Women Owned Companies Can Get the Funding They Need

While there are some women business grant opportunities out there, they are highly competitive and rarely enough to fully fund business needs. These funding options are great for immediate cash needs, and you can work on building your fundability in the meantime. Once your business has strong fundability, you can have pretty much any business funding you need.

The absolute best way to build fundability is with the help of a business credit expert. They can walk you through the complicated web of the many factors that affect fundability, including helping you find accounts that will report to your business credit profile. That is the only way to build a business credit score.

The post How to Get Funding for Women Owned Companies appeared first on Credit Suite.

5 Unwise Ways to Use a Business Line of Credit

Are you on the brink of taking your business to the next level but need an injection of cash? A business line of credit may be the right solution. Once approved, you’ll have access to funds that you can withdraw on an as-needed basis (up to your credit limit). Of course, you’ll eventually have to pay back everything you borrowed plus fees and interest. So how can you best use a business credit line and avoid getting in over your head? Sometimes it helps to know what NOT to do. Here are five unwise ways to use a business lines of credit that you should definitely avoid.

#1 Cover personal expenses

This is a big one, hence, the number one ranking. If you take out a business line of credit, you may be tempted to use some of the proceeds for personal reasons. Maybe you need a little bit to make ends meet or have been waiting for an opportunity to book a getaway? That’s usually not a good idea.

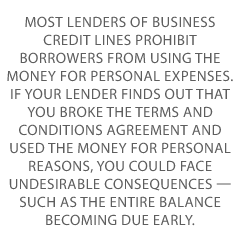

Most lenders of business credit lines prohibit borrowers from using the money for personal expenses. If your lender finds out that you broke the terms and conditions agreement and used the money for personal reasons, you could face undesirable consequences — such as the entire balance becoming due early.

Further, the purpose of the business credit line is to enable you to invest in your business so it grows, is more profitable, and is able to pay back the money you borrow. When you use the money for personal reasons, it’s not helping those causes. So when it comes to a business line of credit, be sure to keep it strictly business.

Demolish your funding problems with 27 killer ways to get cash for your business.

#2 Pay for routine expenses

The best use of a business line of credit is to invest it into your business so it can grow. How? Buying inventory, launching a marketing campaign, and buying equipment are all great examples.

In all of these scenarios, the money you spend should have a good chance of increasing the amount of revenue you earn. In theory, this approach can help you get off the hamster wheel of not having surplus money which causes you to need loans in the first place.

On the other hand, if you are spending borrowed money (which comes with interest charges and fees) to pay routine expenses like rent or utility bills, they are costing you more without offering returns. This can be a slippery slope you want to avoid.

#3 Borrow more than you can repay

When taking out a business credit line, it’s important to consider how much you can reasonably afford to repay. It can be tempting to take as much as you can get and hope for the best. However, a better route is to look at your historical income alongside your projections to figure out what repayment amount you can comfortably afford. If you are expecting a revenue increase, it’s often best to base the amount you can repay on conservative ROI estimations to be sure you can afford the payments.

#4 Withdraw the funds before you need them

One of the biggest benefits of a business credit line over a loan is that you only pay interest once you withdraw money from the credit line. When you don’t need a lump sum all at once, you can save by withdrawing the funds as you need them.

For example, say that you need $10,000 to buy inventory but want to buy it in four stages that cost $2,500 each. You could potentially save by getting a credit line and withdrawing the funds as you need them versus getting the whole $10,000 upfront and paying interest from day one. However, you will have to compare the overall cost of the credit offerings available to you to see which is a better deal.

The bottom line? If you don’t need all the money upfront, don’t withdraw it until you need it!

Demolish your funding problems with 27 killer ways to get cash for your business.

#5 Charge unneeded business expenses

When money becomes available to you, it can get the wheels of your imagination turning. You may start thinking about office upgrades, fancy dinners out with the team, or a new tailored suit. While all of these expenses are for the business, they are not necessary to grow and don’t provide a meaningful ROI. When the line of credit is fully withdrawn, you don’t want to be left regretful, wondering where it all went. Be sure to create a plan for how you will spend the money for strategic purposes that tie directly to growth.

Frequently asked questions about business lines of credit

Now, here are answers to frequently asked questions about business lines of credit.

What is the difference between a secured and an unsecured business line of credit?

Business lines of credit can be secured or unsecured. When secured, it means that you have to offer up some collateral in exchange for the loan. For example, you could provide assets such as inventory, equipment, or buildings. If you default when making repayments on the credit line, your lender can then seize your assets and sell them to pay off the loan.

With an unsecured business credit line, you are approved based on your credit and financial profiles. They trust that you will repay the loan. If you don’t, they can’t directly seize any of your property. However, defaulting on a loan will hurt your credit and can result in a lawsuit where they sue you to recover their losses.

Should I get a revolving line of credit?

A revolving line of credit enables you to borrow money from your credit line, pay it back, and then borrow it again (similar to a credit card). However, credit lines often have higher credit limits and lower interest rates than credit cards. If you need a larger amount of working capital on an ongoing basis, a revolving business line of credit can be a helpful solution.

Explore other small business loan options.

Demolish your funding problems with 27 killer ways to get cash for your business.

Borrow for your business with confidence!

If a business credit line sounds like the right move for your business, the next step is to get approved. What are the common business line of credit requirements? In most cases, you will need at least six months to a year in business and $25,000 in annual revenue. Additionally, you’ll likely need to have a “fair” personal credit score of 580 or higher. Some lenders will want to check your business credit, and if you don’t have any history, will require a higher personal credit score. Keep in mind that requirements and terms can vary from one lender to the next so it’s smart to shop around and compare offers!

Author bio: Jessica Walrack is a professional writer who specializes in business and personal finance. You can find her work featured on MSN Money, The Simple Dollar, Bankrate, and more.

The post 5 Unwise Ways to Use a Business Line of Credit appeared first on Credit Suite.

PocketSuite Is hiring Lead Engineers, Product Designers to enrich small business

Article URL: https://www.ycombinator.com/companies/pocketsuite

Comments URL: https://news.ycombinator.com/item?id=27414470

Points: 1

# Comments: 0

Qventus (YC W15) Is Hiring Data Platform Engineers

Article URL: https://jobs.lever.co/qventus/c0d604cf-ec1c-48ea-847d-5ffc7a67698d

Comments URL: https://news.ycombinator.com/item?id=27421523

Points: 1

# Comments: 0

How to Create a Free Google Website For Your Business

A web presence is essential for getting found online, especially these days. According to Statista.com, nearly a third of consumers in the United States look online for a local business every day. It’s simple: websites are essential for attracting new customers.

A website proves invaluable in other ways, too, like showcasing your products and increasing leads. However, your website doesn’t need to cost a fortune and include the latest features. If you’re a small business that just wants to let customers know who you are and what you do, a free Google website may be just what you’re looking for.

What is Google’s Free Website Builder?

Google’s free website builder is part of Google My Business and helps customers discover you online.

When creating your website, Google takes the information in your GMB business profile and uses it for the building blocks of your website. Aside from some customization, you’re pretty much good to go from there.

Although there’s no cost, free Google websites are professional-looking and offer a selection of contemporary themes.

Google’s website builder is suitable for everyone, even for beginners. There’s no need for technical expertise with a free Google website and no worries regarding extensive backups.

Additional benefits with a free Google website are:

- You don’t need to rely on social media: Not every potential customer is on social media, and many may not be on the platforms you like best. Having a website of your own, where people can Google your name or what you sell and find your information without signing in to Facebook or Twitter, can bring in those customers.

- Ease of use: One of the main benefits of a free Google website is its simplicity, and it delivers great-looking websites. For instance, even the free version of WordPress can seem overwhelming for the absolute beginner, with menus, pages, sub-menus, etc.

- It provides the essentials: If you’re not looking for the whole e-commerce experience, then a free Google website is all you need for reaching out to a broader audience.

Here are some more reasons why you should use a free Google website for getting online.

Why Should You Build a Website Using Google’s Free Tool?

Only 64 percent of small businesses have websites. Meanwhile, 70 percent of potential customers are more likely to buy from a business with a website.

This means 36 percent of businesses may be missing out on 70 percent of buyers.

Websites make businesses seem more legitimate, particularly if the website looks professional. Google websites, which take almost no time to set up and require minimal maintenance, can look like you spent hours of time and thousands of dollars to make it look great.

If Google’s free website gets you found, why not take advantage of its ease of setup and free features?

Google Website Builder Features

The number one thing that sets Google’s business websites apart from others is that it automatically makes the site for you. You can alter things as you need, but if you have a Google My Business account and select the website option, it automatically populates the information on a site for you using a template you choose.

Don’t let its simplicity fool you. A Google My Business free website offers you plenty in the way of features.

For instance, it provides you with built-in optimization so customers can:

- contact or message you

- place orders

- get quotes for services

- book your services or arrange deliveries

Additionally, a free Google website allows you to “showcase what makes your business special” via:

- images

- stories

- posts

Other features worth mentioning are:

- integration with Google Maps and Calendar

- image carousel and video links

- connection with Google Drive

Besides the above, Google gives you automatic updates, advertising, and it’s mobile-friendly too.

As you can see, a free Google website offers a lot to the new business owner, but how does it compare with others?

Google Website Builder Versus WordPress and Other Similar Tools

The Google website builder one-page format beats many other options in the simplicity stakes.

Additionally, it creates a website with almost no effort on your side, which is where Google’s product stands out from similar tools. It also lets you import images with a few clicks, and you can track analytics, so all in all, it offers you the essentials.

The other main advantage over its rivals is you’re not starting from scratch, and you aren’t making all the decisions yourself.

Although it may seem basic to some, Google gives you a functional, great-looking website, and with some imagination, it delivers impressive results.

For inspiration, look at what Steel Mailbox did with theirs. This Google business website starts with the basics that could be pulled in from their business information (e.g., the directions function).

If you click the “hamburger” in the upper left, you see options the company chose to add, which jump you to different page areas. One cool feature they added was a list of mailbox types with brief definitions of each one. This allows people shopping for mailboxes to understand what type they need without having to dig through Steel Mailbox’s non-Google site.

If a customer clicked on one of those blue links, they would be taken directly to the type of mailbox they’re looking for. If they went through the main site—and you can have both a simple Google business site and a more in-depth one—they would likely have to do more digging to find precisely what they need.

What a great feature for customers on the go.

When it comes to this type of website, perhaps its weakest area is ongoing SEO optimization, but you can use a free or paid-for tool to find keywords and include them in your descriptions and posts.

WordPress

While bloggers, Fortune 500 companies, and small businesses use WordPress to build their websites, it’s actually a content management system.

You’ve two options for getting started. WordPress.com gives you the free version, while WordPress.org offers a paid one.

At the free level, the most significant difference between Google and WordPress is that you can create multiple pages within your site, while Google has a one-page format.

When you get to the paid levels, you can add additional functions.

While WordPress offers many more functions than Google websites, no matter which level you use, you have to start from scratch. Nothing is auto-populated. Nevertheless, there are plenty of tutorials online if you’re just learning, and you won’t need to do any coding.

Wix

Wix is another free website builder, although it also offers premium and e-commerce plans too. Getting started is simple. Just sign up or log in with Facebook or Google to get started.

Like WordPress, the free level is relatively limited in functionality. If you’re willing to pay, though, you can access hundreds of templates, additional types of analytics, and more.

Wix provides 500 different templates, and its drag and drop feature means beginners can use it without needing technical expertise.

Other features include:

- media galleries

- mobile optimization

- unlimited fonts

- a personalized SEO plan

Wix also provides coding for visitor tracking, while its analytics tool shows your sales, traffic, and visitor behavior.

How to Customize Your Free Google Website

After you have set up your Google My Business page (detailed steps are in the next section), you’ll be able to see your site free google website in a standard setup. You can then start customizing from there.

The list nearest your sample site includes things you can do right now, like add photos, text, and themes. The one furthest left includes:

- home

- posts

- reviews

- messages

- products

- insights

Take some time to get to know these options and which each one does.

From the home page, you can also:

- finish your profile by adding opening hours, descriptions, and logos

- update customers on news and events

- create a custom @yourbusiness email address

- launch virtue tours and create adverts

You can see the themes, add pictures with a photo gallery, and edit your site’s categories from the other menu.

To best set up your site, follow these steps:

- Choose your theme: For customizing, the most obvious starting point is by looking at the themes. There are ten to choose from, all with different colors and styles of text. Click on them one by one to see which theme most closely matches your business’s style and the image you want to convey.

- Add Photos: Click on the top right-hand corner of the header picture, drag your photo, or upload one from your computer. To add other images, click on “photos” on the left-hand side.

- Editing: Edit text by clicking the blue “Edit” button under photos.

- Additional changes: Click “More” to change settings, publish, or for advice on getting customers.

It’s that easy! You’ve finished building your free Google website, and you should be ready to start getting noticed online.

How to Build Your Free Google Website

Before building your website, set up your Google my Business Page, if you haven’t already. Here’s how to do just that.

- Go to Google’s website builder.

You’re looking for the “website” heading. It’s the third one along at the top.

- Add your business name and click the blue arrow.

- Add your business category.

If your service or industry isn’t clear cut, add the class representing your company the best. Click “Next.”

- Select your location preferences.

Now, Google asks if you want your business location to appear on your website. Either select “Yes, I want it to appear on my website” or “No, I prefer not to.” Depending on the type of business, you may need to include an address. Choose the appropriate option and click “Next.”

- Choose if your business provides deliveries or services.

Choose if your business provides deliveries or services. This step is optional.

- Add your region and click “Next.”

- Add your phone number.

- Add your business address details, including country and zip code.

- Verify your accout.

- Do this by clicking on the “Home” page, which you’ll find at the top of the menu on the left, and following the “Verify” link.

You’re ready to start building your free Google website!

Create a Free Google Website FAQs

What Is the main benefit of a free Google website?

Unlike its rivals, you’re not starting from scratch, and you aren’t making all the decisions yourself. Although it may seem basic to some, a Google site gives you a functional, great-looking website, and with some imagination, you’ll get impressive results.

How do I set up a Google My Business Page?

Google provides step-by-step instructions.

Do I Need Technical Expertise to Build a Free Google Website?

No, a free Google website creates a professional-looking website with minimal input from you.

How Does a Free Google Website Compare With Its Rivals?

While other options offer additional features, Google outshines its competitors regarding simplicity and ease of use.

Conclusion

Having an online presence is a necessity these days. If would-be customers can’t find your website, you’re likely missing out on clients.

However, building a website doesn’t mean spending a lot of money or needing technical expertise. Instead, you can begin by starting with a free Google website and set it up in a few easy steps.

Once you’re online, you can start benefiting from additional leads, more customers, and increased conversions—all the things you need for increasing your business success rate and growing a thriving enterprise.

How has using a free Google Business website affected your business?

How the Azerbaijan Grand Prix descended into chaos

Max Verstappen crashing out of the lead, Lewis Hamilton fluffing the chance to re-claim the championship lead and three of F1’s most popular drivers on the podium. Here’s how Baku;s wild race unfolded.

The post How the Azerbaijan Grand Prix descended into chaos appeared first on Buy It At A Bargain – Deals And Reviews.

Schumacher rages at teammate Mazepin: 'Does he want to kill us?'

Mick Schumacher was furious with Haas teammate Nikita Mazepin for a piece of driving which nearly led to a collision at the end of the Azerbaijan Grand Prix.

The post Schumacher rages at teammate Mazepin: 'Does he want to kill us?' appeared first on Buy It At A Bargain – Deals And Reviews.

How to Build EIN Credit for Your Business

Do You Know How to Build EIN Credit?

Yes, it’s really possible to learn how to build EIN credit for your business.

But let’s start with some definitions and background on business credit.

Business Credit

This is credit in a business’s name. It is not tied to the owner’s creditworthiness. Instead, business credit scores depend on how well a company can pay its bills. Hence consumer and business credit scores can vary dramatically.

Business Credit Benefits

There are no demands for a personal guarantee. You can quickly get business credit regardless of personal credit quality. And there is no personal credit reporting of business accounts. Business credit utilization won’t affect your consumer FICO score. Plus the business owner isn’t personally liable for the debt the business incurs. This can be true for you as you build EIN credit for your business.

Another advantage is that even startup businesses can do this. Visiting a bank for a business loan can be a recipe for frustration. But building business credit, when done correctly, is a plan for success.

Consumer credit scores depend on payments but also various other factors like credit utilization percentages.

But for company credit, the scores truly just hinge on if a small business pays its invoices timely.

Business Credit Details

Being accepted for business credit is not automatic. Building business credit requires some work. Some of the steps are intuitive, and some of them are not.

Vendors are a big component of this process.

Doing the steps out of sequence results in repetitive rejections. No one can start at the top with business credit. For example, you can’t start with retail or cash credit from your bank. If you do, you’ll get a rejection 100% of the time.

Company Fundability to Build EIN Credit

A company must be fundable to lending institutions and vendors.

That is why, a small business needs a professional-looking website and email address. And it needs to have site hosting from a company such as GoDaddy.

Additionally, business phone numbers need to have a listing on 411. You can do that here: https://www.listyourself.net.

Also, the business telephone number should be toll-free (800 exchange or the equivalent).

A company also needs a bank account devoted strictly to it, and it must have every one of the licenses essential for running.

Licenses

These licenses all have to be in the identical, accurate name of the company. And they must have the same company address and telephone numbers.

So keep in mind, that this means not just state licenses, but possibly also city licenses.

Keep your business protected with our professional business credit monitoring.

How to Build EIN Credit: Working with the Internal Revenue Service

Visit the Internal Revenue Service website and get an EIN for the company. They’re free of charge. Select a business entity like corporation, LLC, etc.

A small business may get started as a sole proprietor. But they absolutely need to change to a form of corporation or an LLC.

This is to decrease risk. And it will make the most of tax benefits.

A business entity matters when it involves taxes and liability in the event of a lawsuit. A sole proprietorship means the business owner is it when it comes to liability and taxes. No one else is responsible.

The best thing to do is to incorporate. You should only look at a DBA as an interim step on the way to incorporation.

How to Build EIN Credit: Getting Started

Start at the D&B web site and get a totally free D-U-N-S number. A D-U-N-S number is how D&B gets a small business into their system, to produce a PAYDEX score. If there is no D-U-N-S number, then there is no record and no PAYDEX score.

Once in D&B’s system, search Equifax and Experian’s web sites for the company. You can do this at www.creditsuite.com/reports. If there is a record with them, check it for correctness and completeness. If there are no records with them, go to the next step in the process.

This way, Experian and Equifax have something to report on.

How to Build EIN Credit with Starter Vendors

First you should build tradelines that report. Then you’ll have an established credit profile, and you’ll get a business credit score.

And with an established business credit profile and score you can begin to get credit for numerous purposes, and from all sorts of places.

These kinds of accounts tend to be for things bought all the time, like marketing materials, shipping boxes, outdoor work wear, ink and toner, and office furniture.

But first of all, what is trade credit? These trade lines are credit issuers who give you starter credit when you have none now. Terms are generally Net 30, versus revolving.

Therefore, if you get an approval for $1,000 in vendor credit and use all of it, you need to pay that money back in a set term, like within 30 days on a Net 30 account.

Details

Net 30 accounts must be paid in full within 30 days. 60 accounts must be paid completely within 60 days. Unlike revolving accounts, you have a set time when you must pay back what you borrowed or the credit you made use of.

To launch your business credit profile the proper way, you should get approval for vendor accounts that report to the business credit reporting bureaus. When that’s done, you can then use the credit.

Then pay back what you used, and the account is on report to Dun & Bradstreet, Experian, or Equifax.

Vendor Credit – It Makes Sense

Not every vendor can help in the same way true starter credit can. These are vendors that grant approval with a minimum of effort. You also need them to be reporting to one or more of the big three CRAs: Dun & Bradstreet, Equifax, and Experian.

As you get starter credit, you can also start to get credit from retailers. Here are some stellar choices from us: https://www.creditsuite.com/blog/5-vendor-accounts-that-build-your-business-credit/

Uline

Uline is a true starter vendor. You can find them online at www.uline.com. They sell shipping, packing, and industrial supplies, and they report to Dun & Bradstreet and Experian. You MUST have a D-U-N-S number and an EIN before starting with them. They will ask for your corporate bank information. Your company address must be uniform everywhere. You need for an order to be $50 or more before they’ll report it. Your first few orders may need to be prepaid initially so your business can get approval for Net 30 terms.

- How to apply with them:

- Add an item to your shopping cart

- Go to checkout

- Select to Open an Account

- Select to be invoiced

Marathon

Check out starter vendor Marathon. Marathon Petroleum Company provides transportation fuels, asphalt, and specialty products throughout the United States. Their comprehensive product line supports commercial, industrial, and retail operations. This card reports to Dun & Bradstreet, Experian, and Equifax. Before applying for multiple accounts with WEX Fleet cards, make sure to have enough time in between applying so they don’t red-flag your account for fraud.

To qualify, you need:

- Entity in good standing with Secretary of State

- EIN number with IRS

- Business address- matching everywhere.

- D-U-N-S number

- Business License (if applicable)

- And a business bank account

- Business phone number listed on 411

Your SSN is required for informational purposes. If concerned they will pull your personal credit talk to their credit department before applying. You can give a $500 deposit instead of using a personal guarantee, if in business less than a year. Apply online. Terms are Net 15. Get it here: https://www.marathonbrand.com/.

Grainger Industrial Supply

Grainger Industrial Supply is likewise a true starter vendor. You can find them online at www.grainger.com. They sell hardware, power tools, pumps and more. They also do fleet maintenance. And they report to D&B. You need a business license, EIN, and a D-U-N-S number.

- To qualify, you need the following:

- A business license (if applicable)

- An EIN number

- A company address matching everywhere

- A corporate bank account

- And A D-U-N-S number from Dun & Bradstreet

Your business entity must be in good standing with the applicable Secretary of State. If your business doesn’t have established credit, they will require additional documents. So, these are items like accounts payable, income statement, balance sheets, and the like.

Apply online or over the phone.

Accounts That Do Not Report

Non-reporting trade accounts can also be helpful. While you do want trade accounts to report to a minimum of one of the CRAs, a trade account which does not report can still be of some value.

You can always ask non-reporting accounts for trade references. And also, credit accounts of any sort ought to help you to better even out business expenditures, thus making financial planning simpler.

Store Credit

Store credit comes from a variety of retail service providers.

You must use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, use the company’s EIN on these credit applications.

Fleet Credit

Fleet credit is from service providers where you can purchase fuel and fix and take care of vehicles. You must use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, make certain to apply using the company’s EIN.

Keep your business protected with our professional business credit monitoring.

Cash Credit

You must use your SSN and date of birth on these applications for verification purposes. For credit checks and guarantees, use your EIN instead.

These are frequently MasterCard credit cards.

Monitor Your Business Credit

Know what is happening with your credit. Make certain it is being reported and address any errors as soon as possible. Get in the practice of checking credit reports. Dig into the particulars, not just the scores.

We can help you monitor business credit at Experian, Equifax, and D&B for a lot less than it would cost you at the CRAs. See: www.creditsuite.com/monitoring.

Update Your Information

Update the info if there are inaccuracies or the data is incomplete.

Fix Your Business Credit

So, what’s all this monitoring for? It’s to challenge any errors in your records. Mistakes in your credit report(s) can be taken care of. But the CRAs usually want you to dispute in a particular way.

Disputes

Disputing credit report mistakes typically means you send a paper letter with copies of any proof of payment with it. These are documents like receipts and cancelled checks. Never send the originals. Always mail copies and keep the original copies.

Fixing credit report errors also means you specifically detail any charges you challenge. Make your dispute letter as clear as possible. Be specific about the concerns with your report. Use certified mail to have proof that you sent in your dispute.

Keep your business protected with our professional business credit monitoring.

A Word about How to Build EIN Credit

Always use credit smartly! Never borrow more than what you can pay off. Monitor balances and deadlines for repayments. Paying on schedule and fully does more to increase business credit scores than nearly anything else.

Building small business credit pays off. Excellent business credit scores help a small business get loans. Your lender knows the small business can pay its financial obligations. They know the company is for real.

The small business’s EIN links to high scores and loan providers won’t feel the need to request a personal guarantee.

How to Build EIN Credit: Takeaways

Business credit is an asset which can help your small business for years to come. Learn more here and get started toward establishing small business credit.

The post How to Build EIN Credit for Your Business appeared first on Credit Suite.

How to Use YouTube Ads to Grow Your Business

Being a marketer is an interesting job.

On the one hand, you’re expected to keep up with trends. When a new social media platform starts to take off, you’d better be there promoting your brand.

Still, you can’t just blindly follow those trends. Popular platforms become saturated with dozens of competitors, and standing out becomes nearly impossible.

Don’t get me wrong; social media ads can work wonders. I’ve just noticed there are plenty of underutilized marketing platforms right now. The most noticeable of which is YouTube ads.

YouTube ads are one of the most overlooked ad formats in digital marketing, and it’s easy to figure out why.

The massive focus on social media ads combined with the challenge of creating compelling high-quality video content makes YouTube ads a tough sell to small business owners.

Can YouTube ads be tough to grasp? Sure, at first. Luckily, once you get over that initial hurdle, YouTube ads offer some pretty unique marketing tools you can’t find anywhere else.

That’s why today, we’re taking a deep dive into the world of YouTube ads, from ad types to strategy. We’ll even walk you through creating your first one!

5 YouTube Ad Types

If you’re unfamiliar with YouTube, their primary advertising format is known as the TrueView ad. Before we can understand the value of skippable in-stream ads, we need to take a closer look at YouTube’s TrueView ad approach.

TrueView ads were created to solve a massive problem. Before TrueView ads, users lacked any meaningful way to control their advertising experience. Without a way to meaningfully interact with the content, ads ran the risk of being both frustrating and irrelevant.

YouTube was hoping to present itself as a valuable advertising platform, but its original approach to advertising severely limited the effectiveness and efficiency of brand marketing efforts. No brand wants to waste precious time and money selling to viewers who simply aren’t interested.

Here’s the simple explanation: Your brand only pays for TrueView Ads when viewers watch for at least 30 seconds, watch your entire video, or interact with your ad via call-to-action (CTA).

1. Skippable In-Stream Ads

The first variation of the TrueView ad is the skippable in-stream ad. At a minimum of 12 seconds and a maximum of six minutes, in-stream ads play before a viewer’s video on YouTube.

These ads feature a countdown timer on screen, as well as a link to the brand website. You can also tag on a companion banner ad, but it’s worth pointing out these companion banner ads won’t be on all YouTube pages where your in-stream ads are served.

Of course, the most important part of this variant is the option to skip the video ad after five seconds. If they choose to skip and don’t interact with your ad, you don’t have to pay a dime. Assuming you uploaded the video to your YouTube channel, once the viewer watches for 30 seconds, a view is attributed to your view count.

2. Video Discovery Ads

TrueView Discovery ads are promoted throughout YouTube, appearing as an image thumbnail with up to three lines of text. These ads function as an entirely optional way for viewers to consume your brand content.

Discovery ads are visible on the YouTube homepage, at the top of a viewer’s YouTube search results, and on the suggested videos list on their video’s watch page. The best part? Your brand doesn’t spend a dime on these ads unless viewers interact with them.

That’s what makes this advertising approach so useful to brands and marketers. TrueView ads work to protect both the viewer’s time and your brand’s money.

3. Non-Skippable In-Stream Ads

If the TrueView approach just doesn’t interest your brand, YouTube has plenty of other options. Non-skippable ads function a bit differently on this platform. They might look just like skippable ads on the surface, but you’ll be limited to a 15-second ad window for non-skippable ads.

Beyond that, you’ll be dealing with a cost per thousand (CPM) payment structure, forcing you to pay for every thousand views.

The only scenario where you’d want to use something like this is when you’re dealing with a proven target audience or when your brand is looking to maximize its reach. Otherwise, there’s a strong chance you could waste time and money selling to the wrong prospects.

4. Bumper Ads

As you research YouTube ads, you’ll likely come across bumper ads and wonder what purpose they serve. What makes them different from the traditional non-skippable in-stream ad?

The most significant difference is the duration of your ad window. Instead of 20 seconds, bumper ads are expected to last less than six seconds.

Why would this distinction matter? Well, a viewer’s time and attention are valuable commodities. YouTube needs to protect their user experience, primarily by providing users with relevant information. YouTube limits these bumper ads to avoid frustrating viewers with non-skippable ads.

The key to making bumper ads work is creating something memorable. The format might not support long-form stories, but there are plenty of ways to portray your brand in five seconds.

5. Masthead Ads

Think of YouTube Masthead as YouTube’s premium advertising experience. Imagine your ad being the first thing viewers see whenever they use the platform. It’s a marketer’s dream come true, and with good reason.

Of course, there’s a reason you’ve never seen a small business on that masthead. That premium experience comes with a premium price tag. At about $2 million per day, masthead ads are extremely expensive and far beyond the average brand’s marketing budget.

Think of these like Super Bowl ads: impressive reach and traffic, but not reasonable for most marketers. YouTube’s other advertising formats are more cost-effective, easier to experiment with, and generally more valuable to your brand’s marketing journey.

What Makes YouTube Ads Unique?

With all the different variants and the added work of creating a compelling video ad, some marketers might wonder why they should use YouTube ads over social media ads. After all, that’s a ton of extra work when you could just make some simple visuals on Facebook ads.

While it’s certainly easier to make ads on social media, YouTube is a powerful tool for brands looking to promote high-quality video content to a massive audience. In fact, in a side-by-side comparison, an Agorapulse study found YouTube ads produced more views, more clicks, and higher conversions than Facebook Ads!

How to Decide Which Kind of YouTube Ad Is Right for Your Business

You’re ready to get started with your YouTube video ads. You’ve done all your audience and keyword research, and you know what the messaging should look like. Now you just need to pick an ad format.

When you’re first getting started, settling on a format to use can quickly become confusing. Should you use TrueView ads because you’re only charged per interaction? Are impressions more important or is traffic your only priority?

If you’re completely new to the world of YouTube ads, this breakdown of video ad formats by marketing objective exists to help you take that first step forward. Not to worry, your brand will start to identify what works well over time via testing and data collection.

Brand Consideration: Video Discovery Ads

One of the most compelling reasons to experiment with discovery ads is their potential as a brand consideration tool.

Instead of focusing on squeezing in a quick ad before someone else’s video, you can integrate your ad content into the YouTube search experience. This is where your keyword research can really shine. Create content that revolves around those low competition keywords with high volume.

When viewers click on your ad, they’ll be taken to your YouTube channel to watch that video. The goal here is less about CTAs and conversion and more about providing a closer look at your brand. If you have great instructional videos or interesting presentations, a discovery ad can work wonders for you.

Brand Awareness: Non-Skippable Ads

For the sake of clarity, let’s define a few terms before we move on. Brand awareness is about maximizing visibility for your brand. Ideally, it lays the foundation for effective lead generation.

The main objective of lead generation is to both identify likely prospects quickly and offer properly defined metrics. Both lead generation and brand awareness are powerful tools when used correctly, but it’s vital you understand when to best use them.

Think of brand awareness as the top of the marketing funnel, leading into quality lead generation.

If your primary marketing goal is casting a wide net, non-skippable ads can effectively raise awareness for your brand. These ads can appear pre-roll, mid-roll, or even post-roll. If you’re worried about placement, YouTube serves these ads whenever they believe viewers are most likely to watch.

Lead Generation: TrueView In-Stream Ads

Maximizing brand awareness is great, but if you want to turn your traffic into interested prospects, you’ll need ad content that truly converts.

TrueView in-stream ads are perfect for this because they’re designed to be skippable. They introduce a level of reliability to the marketing experience. This potential prospect found the first five seconds of your ad compelling and was willing to stick around.

My favorite part? If a viewer doesn’t want to consume your content, they can just leave, at no cost to you. If the viewer does want to interact, they’ve now provided you with some very valuable information. They’re genuinely interested in your brand!

Message Reinforcement: Bumper Ads

Let’s say you’ve already established an audience via digital media. You want to get a message out to them, maybe to announce your latest shoe release or phone launch. You need to maximize your budget, but you don’t really need to educate your target audience on the brand.

This is one of the scenarios where bumper ads perform well. The bumper ad doesn’t allow for much in terms of storytelling or education. What it can do is allow just enough time to hype up a new product or service.

Reach: Masthead Ads

We’ve already established that Masthead ads aren’t for the average small business. While they may not be a cost-effective way to market your brand, they do highlight a lesson about ad budgets in marketing: specifically, the concept of ROI.

On the surface, spending millions of dollars on a single ad can seem ridiculous. What if the messaging doesn’t land perfectly? What if you were wrong about the target audience’s pain points? It seems like such a massive risk. Still, massive brands are doing this regularly. Why?

Well, consider how these massive brands approach marketing. With millions on the line, their latest marketing campaign is composed of detailed, layered strategy with one element at its center: data, and lots of it.

This data, likely collected over several years, confirms they’ll receive a positive ROI from this investment. Where small brands see risk, massive brands see growth opportunities.

Of course, it’s not like only massive brands are entitled to that level of confidence. The commitment to making data-driven decisions is what elevates any marketing strategy.

Masthead ads aren’t impressive because they’re expensive. They’re impressive because they show that with enough data, even the biggest risks become manageable.

How to Create a Video Ad for YouTube

Let’s say you’ve never created a video ad before. All this video ad strategy sounds great, but it won’t make you a master visual content creator overnight. Fortunately, you don’t need to spend months learning how to edit to make compelling videos. When in doubt, a little external guidance goes a long way.

Google is hard at work getting YouTube Video Builder, their accessible video creation software, ready for the public. In the meantime, tools like Promo and Animoto walk you through the process of building strong video ads in minutes.

Measure the Success of Your YouTube Ads

YouTube ads track plenty of metrics for you automatically, everything from watch time to engaged-views data is available, if you’re interested.

Unfortunately, that much information can be overwhelming when you’re new to the platform. When you’re first getting started, focus on view rate for skippable ads. This is essentially your true engagement rate, determining how well you can turn viewers into interested prospects.

If your view rate is low, there are a few possibilities. Maybe your headline doesn’t draw people in. Maybe your video doesn’t capture the viewer’s attention quickly enough. Remember those first five seconds need to be compelling.

For non-skippable ads, the focus is still on engagement. The only difference is that you’ll use click-through rate (CTR) to determine whether your ad connects your target audience.

If your CTR is unusually low, there are two possibilities. Either the video is being delivered to the wrong audience or the video itself is not connecting with your target audience. I advise testing for both by experimenting with different target audiences and creating multiple videos.

How to Create YouTube Ads

Ready to get started? Here’s how to create your first YouTube ad.

- Upload Your Video

Log into your brand’s YouTube account and click on the camcorder icon on the top-right of YouTube. Then, click “Upload Video.”

From there, you’ll be taken to the upload window where you can now upload your video. Make sure you fill in title, description, and tag information. - Create Your Campaign

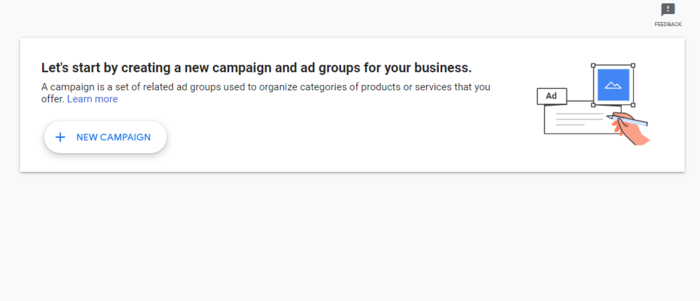

Sign in to your Google Ads Account and select “New Campaign.”

You’ll see an option to choose a campaign goal, but just click on “create a campaign without a goal’s guidance” for now. You can now select a campaign type, so select “Video” or “Display,” based on your goals.For our purposes, we’re going to focus on the “Video” option. At this point, you’ll be asked to select a campaign subtype. Select the most appropriate option and click “Continue.”

- Configure Your Campaign

Now that you’ve created your campaign, it’s time to configure it properly. Start by giving your campaign a name for easy data collection.

Then, confirm your bid strategy, ad budget, and campaign duration. From there, also confirm your networks, locations, and languages.

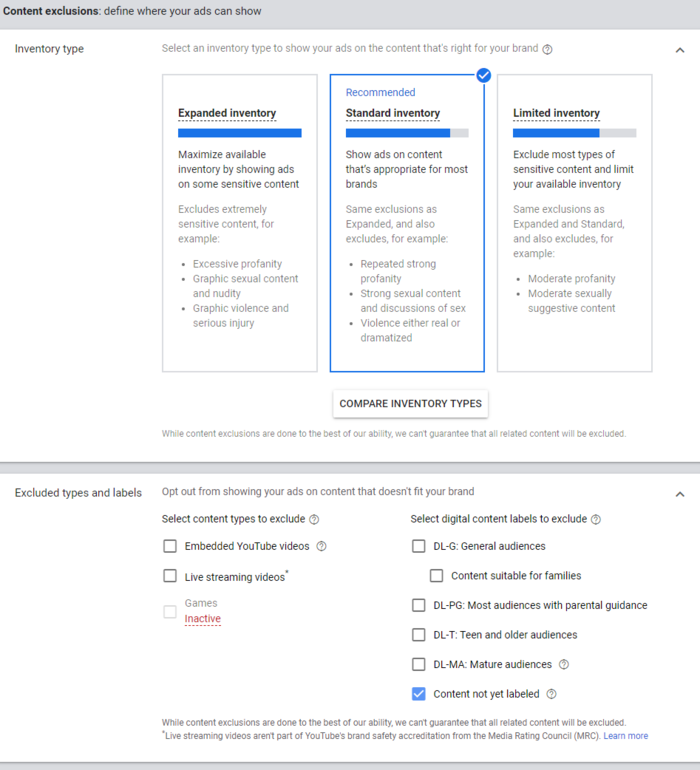

Content exclusions are in this section as well. This determines where your ads are shown. If your brand is typically family-friendly, you’ll likely want to choose limited inventory. If your brand is more mature, expanded inventory could be a good fit. You can also exclude certain types of content and labels here.

- Target Your Audience

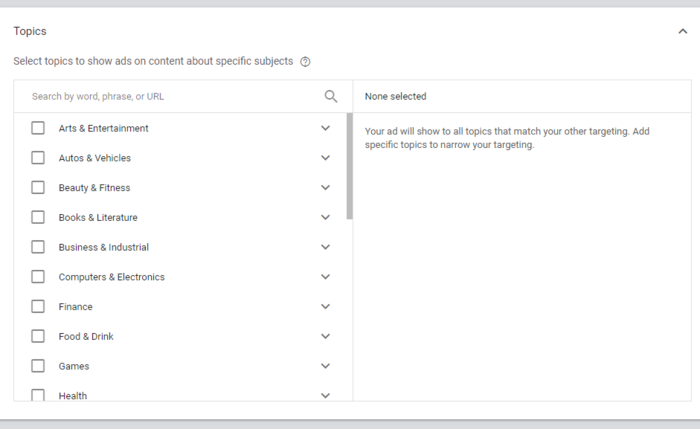

When targeting your audience, start by defining their demographic information including age, gender, parental status, and household income. Google also lets you experiment with some more specific audiences like “bachelor’s degree” or “health care industry.”

Use keywords, topics, and placements to further narrow down your targeting.

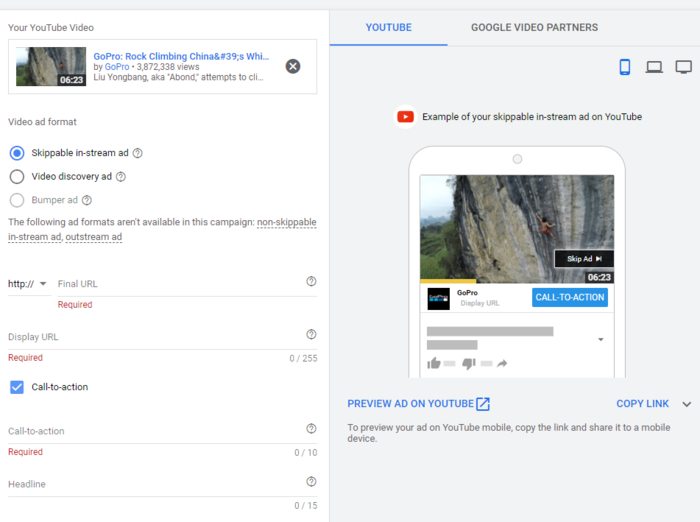

- Finalize Your Ad

Set your maximum bid. In the “Create your video ad” section, find your YouTube video and choose the appropriate video ad format (as listed in the above sections.)

Once your video ad format is selected, fill in the “Final URL” and “Display URL” sections. You can also include your call-to-action and your headline here.

You can auto-generate a companion banner, or upload your own below.

Once you’re ready, click “Create Campaign” and you’re all set!

Final Thoughts on Growing Your Business With YouTube Ads

Listen, I get it. Wrapping your head around YouTube ad creation can be a bit of a challenge at first.

The idea behind this guide is to arm you with a strong foundational understanding of how YouTube ads function, and how you can make your own.

Feel free to bookmark this guide if you ever need a refresher course, especially when it comes to campaign and video creation.

Fortunately, YouTube ads function just like any other digital marketing platform. Focus on your key metrics, test regularly, and above all else, respect the data. The path to consistent growth might not be glamorous, but it certainly gets results.

What digital marketing platform do you think is underutilized right now?