Article URL: https://angel.co/company/curebase/jobs Comments URL: https://news.ycombinator.com/item?id=21766411 Points: 1 # Comments: 0

Category: Business News

Business News

What to Be Aware of When Considering Student Loan Consolidation – Recent Implications

What to Be Aware of When Considering Student Loan Consolidation – Recent Implications

What to Be Aware of When Considering Student Loan Consolidation – Recent Implications

Trainee loan consolidation fundings are amongst one of the most prominent refinancing lendings as they make payment of the education and learning financings less complicated to manage. Since they supply crucial advantages, those car loans are in high need. A few of those advantages are offered with both personal and also government pupil loan consolidations, however some come just with the government loan consolidations.

It’s vital to understand that personal education and learning car loans can not be combined right into government loan consolidation car loan, however there are personal lending institutions – few, though – that provide exclusive debt consolidation of those personal pupil financings.

Exclusive loan consolidation financings can consist of government education and learning finances, nonetheless, consisting of those government car loans in an exclusive combination lending is generally not preferable for a variety of factors. With personal debt consolidation, you will certainly shed essential, charitable advantages of the government finances, such as versatile payment terms and also financing mercy and also termination arrangements. Exclusive combination will certainly commonly enhance your reliable rates of interest and also you will certainly pay far more to offer your education and learning financial obligation – although you’ll obtain reduced month-to-month repayments.

For those factors, it’s advised to look for government debt consolidation funding initially and also just if you can not obtain one, search for an exclusive loan consolidation.

Personal loan providers aren’t just recently ready to settle trainee lendings as they were some years back. For 2 major factors – initially, the worldwide credit history dilemma and also 2nd, the regulation passed just recently by the Congress that substantially lowered the aids for giving education and learning lendings (consisting of trainee debt consolidation finances).

The current debt crisis fiasco made the exclusive lending institutions tighten their borrowing requirements for the possible debtors using for the trainee loan consolidation lendings. You will certainly not be subject to any kind of credit rating check and also income-level examination when asking for a government pupil debt consolidation funding. It figures out the overall quantity you’ll have to pay back when you take the debt consolidation car loan.

According to credit score service resources, in order to be qualified for a personal pupil loan consolidation financing and also obtain a rate of interest that will certainly make the loan consolidation rewarding, you will certainly require a FICO credit rating of 700 – a minimum of 50 factors more than it was simply a couple of years back. The exclusive loan providers need currently your debt-to-income proportion to be a lot reduced than 50%.

What should you do if you truly require to settle your trainee fundings see the personal debt consolidation funding as your only possibility? Well, in order to enhance your possibility of obtaining one, you might utilize a co-signer, as an example your moms and dads, or someone that has great credit score ranking.

It’s crucial to state below some downsides that the consumers that take trainee loan consolidation lendings encounter.

Of all, if your major factor for looking for combination is to decrease your regular monthly repayments, you have to keep in mind that while your regular monthly settlements will certainly be reduced (occasionally by as much as 50%) and also your financial resources will certainly be less complex due to the fact that you’ll have just one month-to-month settlement, it will certainly all come at greater expense. Why? Due to the fact that you will certainly need to be stuck to the car loan for longer amount of time, as the reduced repayments need longer payment and also the complete quantity of the rate of interest paid will certainly be greater.

If you take the loan consolidation finance, your elegance duration will certainly frequently be reduced as well as you might likewise shed financing discount rates offered by the stemming lending institutions. As well as, if you have a Perkins financing, generally it is far better to leave it alone and also not settle it as Perkins car loans have essential advantages not discovered in various other car loans as well as they would certainly be shed in combination.

Pupil combination fundings are amongst the most preferred refinancing fundings as they make settlement of the education and learning lendings much easier to deal with. Personal debt consolidation financings can consist of government education and learning car loans, nevertheless, consisting of those government financings in a personal combination financing is normally not preferable for a number of factors. With personal combination, you will certainly shed essential, charitable advantages of the government financings, such as adaptable payment terms and also financing mercy as well as termination stipulations. If you take the loan consolidation lending, your elegance duration will certainly usually be reduced as well as you might likewise shed funding discount rates given by the stemming lending institutions. As well as, if you have a Perkins lending, typically it is far better to leave it alone as well as not settle it as Perkins financings have crucial advantages not discovered in various other fundings as well as they would certainly be shed in loan consolidation.

The post What to Be Aware of When Considering Student Loan Consolidation – Recent Implications appeared first on ROI Credit Builders.

Kinds Of Health Insurance

Sorts Of Health Insurance

Medical insurance is developed to safeguard versus loss of revenue and also expenditures for treatment. There are 2 wide classifications of medical insurance plans: special needs earnings plans as well as clinical cost plans.

Special needs revenue plans can additionally be described as loss of earnings, loss of time or substitute earnings. This sort of plan will certainly pay advantages to a guaranteed that is handicapped and also can no more function to make a normal revenue. Repayments can be month-to-month or regular relying on the plan.

Clinical expenditure plans are stood for by a variety of insurance coverage from extremely marginal to extensive plans with several protection. Some consist of both health problems and also crashes, numerous health center costs and also various other expenses referring to treatment such as crash and also illness plans, hospital-stay plans, fundamental clinical cost plans and also significant clinical expenditure plans.

Any one of these plans could cover different mixes of the above and also might be paid in a swelling sum.Some plans cover just crashes and also not ailment. As you may envision, plans such as this are extremely certain regarding what is thought about a crash.

It is very important to comprehend what is specified as a crash as it concerns the medical insurance market: a mishap is an occasion that is unexpected as well as unpredicted.

Any kind of conversation of this kind of plan additionally uses to any kind of kind of plan that consists of unexpected insurance coverage, not simply mishap certain plans.

Mishap advantages are most generally spent for unexpected death (likewise called unexpected fatality), unintended loss of arm or leg or view (dismemberment), loss of time and/or revenue, healthcare facility costs, medical expenditures, and also clinical expenditures like brows through to the medical professional.

Life insurance coverage plans will typically be paid no matter of the reason of fatality. An unintended advantage is paid ONLY if the fatality is unintended as opposed to a fatality by all-natural reasons or health problem.

The individual that obtains the survivor benefit is called the recipient. The plan proprietor has the right and also obligation of calling recipients. Typically there is a key recipient nevertheless he/she can designate a 2nd as well as also a 3rd recipient.

The key recipient is the initial individual in line to obtain the advantage in case of the fatality of the plan owner. The plan proprietor can likewise call a 2nd recipient that would certainly obtain the advantage in case the key recipient passes away prior to the guaranteed. Some plans can consist of a 3rd recipient that would certainly remain in line after the very first 2.

There is one more crucial component in relation to mishap plans: An unintentional fatality might not be instantaneous. An individual can pass away as an outcome of an injury months after the mishap event. Due to the fact that the majority of specify that the unintentional fatality advantage will just be paid if fatality happens within 3 months of the mishap, review your plan very carefully.

Life insurance policy plans will normally be paid no matter of the reason of fatality. The key recipient is the very first individual in line to get the advantage in the occasion of the fatality of the plan owner. The plan proprietor can additionally call a 2nd recipient that would certainly obtain the advantage in the occasion the main recipient passes away prior to the guaranteed. There is an additional essential component in respect to crash plans: An unintended fatality might not be instantaneous. Review your plan meticulously due to the fact that many state that the unintentional fatality advantage will just be paid if fatality happens within 3 months of the mishap.

The post Kinds Of Health Insurance appeared first on ROI Credit Builders.

The post Kinds Of Health Insurance appeared first on #1 SEO FOR SMALL BUSINESSES.

The post Kinds Of Health Insurance appeared first on Buy It At A Bargain – Deals And Reviews.

Federal Reserve signals no rate hikes in 2020, just one in 2021

The Federal Reserve left its benchmark interest rate unchanged and signaled no changes next year after its latest meeting to evaluate the economy. The Fed’s so-called dot plot shows no rate hikes in 2020 and just one in 2021. The “current stance of monetary policy is appropriate to support sustained expansion of economic activity,” the Fed said Wednesday. The U.S. appears to have stabilized at steady but slower rate of growth and inflation is still below the Fed’s 2% target. The vote was unanimous to leave the short-term fed funds rate at a range of 1.5% to 1.75%.

Market Pulse Stories are Rapid-fire, short news bursts on stocks and markets as they move. Visit MarketWatch.com for more information on this news.

The post Federal Reserve signals no rate hikes in 2020, just one in 2021 appeared first on WE TEACH MONEY LIFE SELF DEFENSE WITH FINANCIAL GOALS IN MIND.

The post Federal Reserve signals no rate hikes in 2020, just one in 2021 appeared first on Buy It At A Bargain – Deals And Reviews.

Get Corporate Credit Cards Using EIN Only

Here’s How to Get Corporate Credit Cards Using EIN Only

Is it possible to get corporate credit cards using EIN only? Absolutely!

We looked at a ton of company credit cards and did the research for you. So, here are our preferences.

Per the SBA, company credit card limits are a whopping 10 – 100 times that of personal credit cards!

This shows you can get a lot more cash with business credit. And it also means you can have personal credit cards at stores. So, you would now have an added card at the same stores for your company.

And you will not need collateral, cash flow, or financials to get company credit.

Corporate Credit Cards Using EIN Only: Benefits

Perks vary. So, make certain to select the benefit you like from this variety of options.

Secure Corporate Credit Cards Using EIN Only for Average Credit

Capital One® Spark® Classic for Business

For average credit, we like the Capital One Spark Classic for Business. It has no yearly fee. There are cash-back rewards. The card earns an unlimited 1% cash back on all purchases. There is an annual fee of $0.

With this card, you will get benefits including an auto rental collision damage waiver, and purchase security. And you also get extended warranty coverage. And you get travel and emergency assistance services.

But BEAR IN MIND: the ongoing APR is 24.74% variable APR. And the penalty APR is even higher, 31.15%. Also, there is no sign-up bonus.

Get it here: https://www.capitalone.com/small-business/credit-cards/spark-classic/

Corporate Credit Cards Using EIN Only – Credit Builder Cards

Discover it® Student Cash Back

Make sure to check out the Discover it® Student Cash Back card. It has no annual fee. The card also has a six-month introductory period of 0% APR on purchases. And there is an APR of 14.99 – 23.99% variable on all purchases after that period.

One distinct feature is that it offers an incentive for students to maintain good grades with a $20 statement credit. If scholars earn a GPA of 3.0 or better each school year, the card will award the $20 statement credit annually for up to five years.

Details

Use this credit card to build personal credit. While this is a personal card versus a business card, for new credit users, their FICO scores will be important. And this card offers an outstanding way to raise FICO while also getting rewards.

You can get 5% cash back at different places each quarter such as grocery stores, gas stations, restaurants or Amazon.com up to the quarterly maximum. After that, this card offers unlimited 1% cash back on all purchases.

In the initial year, all cash back rewards are matched 100%.

Downsides include a cash advance fee of either $10 or 5% of the amount of each cash advance, whichever is greater. And though they waive the first late payment fee, a fee of up to $37 applies on all other late payments. There is also a returned payment fee of up to $37.

Get it here: https://www.discover.com/credit-cards/cash-back/it-card.html

Ironclad Secured Corporate Credit Cards Using EIN Only

Wells Fargo Business Secured Credit Card

Check out the Wells Fargo Business Secured Credit Card. It charges a $25 annual fee per card (up to 10 employee cards). It also requires a minimum security deposit of $500 (up to $25,000) and it is meant to help cardholders set up or rebuild their credit.

Select this card if you wish to earn 1.5% per dollar in purchases without any limits or earn one point for every dollar in purchases. You also earn 1,000 bonus points for every month your company makes $1,000 in purchases on the card.

Details

Also, you get free FICO scores every month. There are no foreign transaction fees. It is possible to upgrade to unsecured credit. Your account is regularly reviewed. And you may become eligible for an upgrade to an unsecured card with responsible use over time. Approval is not guaranteed and depends on factors including how you manage this and your other accounts.

APR is the current prime rate plus 11.90%. There is no introductory APR period and no sign-up bonus. This is not a credit card for balance transfers.

Get it here: https://www.wellsfargo.com/biz/business-credit/credit-cards/secured-card/

Reliable Low APR/Balance Transfers Corporate Credit Cards Using EIN Only

Discover it® Cash Back

Check out the Discover it® Cash Back card. There is a 10.99% introductory APR for six months from date of first transfer. So, this is for transfers under this offer which post to your account by January 10, 2019.

After the introductory APR expires, your APR will be 14.99% to 23.99%. So, this is based on your creditworthiness. Your APR will vary with the market, which is based upon the Prime Rate.

Details

You can get 5% cash back at different places each quarter. So, these are places like gas stations, grocery stores, restaurants, Amazon.com, or wholesale clubs. But this is up to the quarterly maximum each time you activate. Also, automatically earn unlimited 1% cash back on all other purchases.

You will get an unlimited dollar-for-dollar match of all the cash back you have earned at the end of your first year, automatically.

Get it here: https://www.discover.com/credit-cards/cash-back/it-card.html

Small Business Credit Cards with 0% APR – Pay Zero!

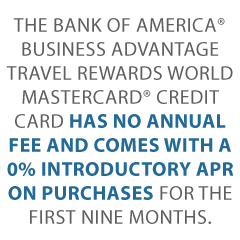

Bank of America® Business Advantage Travel Rewards World Mastercard® Credit Card

The Bank of America® Business Advantage Travel Rewards World Mastercard® credit card has no annual fee and comes with a 0% introductory APR on purchases for the first nine months. After that, the card has a 13.24 – 23.24% variable APR

Earn 3 points/dollar spent when you book travel via the Bank of America Travel Center and 1.5 points/dollar on all other purchases. You can earn unlimited points and points never expire.

Details

There is a 25,000-point sign-up bonus when you spend $1,000 in the first 60 days of opening up the account. Cardholders get travel accident insurance, and lost luggage reimbursement.

They likewise get trip cancellation coverage, trip delay reimbursement and other perks.

There is no introductory rate for balance transfers. Also, bonus categories are limited.

Get it here: https://www.bankofamerica.com/smallbusiness/credit-cards/products/travel-rewards-business-credit-card/

JetBlue Plus Card

Check out the JetBlue Plus Card for yet another offer of a 0% introductory APR

Earn six points/dollar on JetBlue purchases, two points/dollar at eating establishments and grocery stores. And get one point/dollar on all other purchases.

Details

Spend $1,000 in the initial 90 days and pay the annual fee, and get 40,000 bonus points. New cardholders receive a 12 month, 0% introductory APR on balance transfers made in 45 days of account opening.

Thereafter, the variable APR on purchases and balance transfers is 17.99%, 21.99% or 26.99%, based on creditworthiness. Benefits include a free first checked bag and 50% savings on in-flight purchases.

There is a $99 yearly fee for this card.

Get it here: https://cards.barclaycardus.com/cards/jetblue-card/

Remarkable Corporate Credit Cards Using EIN Only with No Annual Fee

Uber Visa Card

Check out the Uber Visa Card. Uber is the very first ride-sharing service to offer a credit card, in a partnership with Visa and Barclays.

The card offers 4% back per dollar spent at restaurants, takeout and bars, including UberEATS. Also, get 3% back on hotel, airfare and vacation home rentals. And get 2% back on online purchases.

So, this includes retailers and subscription services like Uber and Netflix. And get 1% back on all other purchases. Each percent/point has a value of 1 cent. Redeem points for cash back, gift cards or Uber credits directly within the app.

By spending at least $500 in the initial 90 days, users can earn a $100 sign-up bonus. Cardholders spending at least $5,000 per year are eligible to receive a $50 credit toward online subscription services.

Details

If you pay your cellphone bill with this card, you are insured up to $600 for cellphone damage or theft.

Cardholders are eligible for exclusive access to specific events and offers. Uber expects most of these offers will be available in major cities like New York, San Francisco, Los Angeles, Chicago and DC. There is no foreign transaction fee.

But there is no introductory rate. The APR is a variable 16.99%, 22.74% or 25.74%, based on your creditworthiness. Cardholders with less than stellar credit will be on the higher end of the range.

Also, there are restrictions on Uber credits. To redeem points as credits within the Uber app, accumulate at least 500 points, or $5. Cardholders can convert a maximum of 50,000 points, or $500, per day.

Get it here: https://www.uber.com/c/uber-credit-card/

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

Costco Anywhere Visa® Business Card by Citi

Not taking Uber? Then you’ll need to fill your gas tank someway. Why not do so with the Costco Anywhere Visa® Business Card by Citi?

This card earns cash back with every purchase. Earn 4% cash back on the first $7,000 spent on eligible gas purchases annually (1% after that). Get 3% cash back at restaurants and on eligible travel purchases. Also, earn 2% cash back at Costco and Costco.com. And earn 1% cash back on all other purchases.

Note: the $0 yearly fee is only for Costco members. And an active Costco membership is required. Cardholders will get access to damage and theft purchase protection, extended warranty coverage and travel accident insurance.

Also, there is no sign-up bonus available with this card.

Get it here: https://www.citi.com/credit-cards/credit-card-details/citi.action?ID=Citi-costco-anywhere-visa-business-credit-card

Ink Business Cash℠ Credit Card

Consider the Ink Business Cash ℠ Credit Card. Companies can earn cash back with each purchase. Spend $3,000 in the first three months from account opening. And you’ll earn a $500 bonus cash back.

There is a $0 yearly fee with a 0% introductory APR for 12 months on purchases and balance transfers. After that, the APR is a 15.24 – 21.24% variable.

The card comes with travel and purchase coverage benefits. So, this includes an auto rental collision damage waiver and extended warranty protection.

Details

Earn additional cash back on business categories. So, these include office supply stores, telecommunications, gas stations and restaurants.

Note: this credit card has a balance transfer fee. Pay 5% of the amount transferred or $5, whichever is more. Also, there is a foreign transaction fee of 3%.

Get it here: https://creditcards.chase.com/small-business-credit-cards/ink-cash

United MileagePlus Explorer Business Card

Get a good look at the United MileagePlus Explorer Business Card.

Get 2 miles/dollar with United and at restaurants, filling stations and office supply stores. All other purchases earn 1 mile/dollar. Earn a 50,000-mile sign-up bonus after spending $3,000 in the first three months from account opening.

Benefits include priority boarding, a free first checked bag for you and a companion on the same reservation.

Details

Also, get two United Club passes annually. And get hotel and resort perks including upgrades. Additionally, get early check-in and late checkout. And get an auto rental collision damage waiver.

Also, get baggage delay insurance, lost luggage reimbursement, trip cancellation and interruption insurance. Finally, get trip delay reimbursement, purchase protection, price protection and concierge service.

After the first year, the card has an annual fee of $95. APR of 17.99% – 24.99%, based on creditworthiness.

Get it here: https://creditcards.chase.com/small-business-credit-cards/united-mileageplus-explorer-business

Starwood Preferred Guest® Business Credit Card from American Express

Another possibility is the Starwood Preferred Guest Business Credit Card from American Express.

This card is for those who stay at Starwood Preferred Guest and Marriott hotels often. Earn six points per dollar of eligible purchases at participating SPG and Marriott Rewards hotels.

And earn four points per dollar at American restaurants, US gas stations, and on US purchases for shipping.

Also, earn four points to the dollar on wireless telephone services purchased directly from US service providers. For all other eligible purchases, get two points per dollar.

Details

Earn 75,000 bonus points when you spend $3,000 in the initial three months of account opening. Benefits include free in-room premium internet access, Sheraton Club lounge access, and purchase protection.

Plus, you get car rental loss and damage insurance. And you get baggage insurance. There is also a global assistance hotline. And there is a roadside assistance hotline. And get travel accident insurance and extended warranty coverage.

The most significant issue is the annual fee. There is a $0 introductory annual fee for the first year, then it’s $95 after that. Plus, there is no 0% introductory APR. Instead, there is a 17.74 – 26.74% variable APR

Get it here: https://www.americanexpress.com/us/credit-cards/business/business-credit-cards/spg-amex-starwood-credit-card

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

Terrific Corporate Credit Cards Using EIN Only for Cash Back

SimplyCash Plus Business Credit Card from American Express

Look at the SimplyCash Plus Business Credit Card from American Express. There is a $0 annual fee. And there is a 0% APR on purchases So this is for the initial 15 months an account is open.

But when the introductory period expires, the APR for purchases is 14.24 to 21.24%. So, this is variable and based on creditworthiness.

Details

This card has various benefits. These include purchase protection, car rental loss and damage insurance. And they also include a baggage insurance plan, extended warranty coverage and a global assist hotline.

Also, get 5% cash back at US office supply stores and on wireless telephone services. So, these must be bought from American service providers. But this applies to the initial $50,000 of yearly spending. Then, you get 1% cash back.

You also earn 3% cash back on spending category of your choice. So, this is from eight distinct categories. They include airfare, gas, advertising and computer purchases. But it applies to the first $50,000 of yearly spending. Then, you get 1% cash back.

Cash-back bonuses are automatically credited to the customer’s billing statement.

Note: you cannot use this credit card for balance transfers. There is a foreign transaction fee of 2.7%. The credit card charges up to $38 in late fees. And the returned check fee is also $38. The penalty APR is 29.99%.

And, it applies if you have two or more late payments within 12 months. It can also apply if you fail to make the minimum payment on time or have a returned payment.

Get it here: https://www.americanexpress.com/us/small-business/credit-cards/simply-cash-plus-business-credit-card/44279

Capital One® Quicksilver® Card

Check out the Capital One® Quicksilver® Card. It offers flat-rate rewards of 1.5% on all purchases. There are no limits to the amount of cash back rewards which cardholders can earn. Also, the card has a $0 annual fee.

New cardholders have a 0% APR on purchases and balance transfers for the first 15 months after opening the account. And then they have a 14.74 – 24.74% (variable) APR after that.

A cash bonus of $150 is available for those who make at least $500 in purchases within 3 months of account opening.

Details

Also, cash back rewards do not expire for the life of the account. And there is no limit to how much you can earn.

This credit card also offers travel accident insurance. And you get an auto rental collision damage waiver. There are no foreign transaction fees. And there is extended warranty coverage.

Downsides are the flat reward rate, not allowing for any more than that. And the higher APR after the first 15 months.

Get it here: https://www.capitalone.com/credit-cards/quicksilver/

Unbeatable Corporate Credit Cards Using EIN Only for Jackpot Rewards

Chase Sapphire Preferred® Card

Have a look at the Chase Sapphire Preferred® Card for travel points.

You can get two points to the dollar spent on travel and dining at restaurants. And you can earn one point per dollar on all other purchases. Points can be traded in for cash back, gift cards, or travel.

The card’s benefits include trip cancellation insurance, travel and emergency assistance services. They also include an auto rental collision damage waiver, purchase protection and extended warranty protection.

When you spend $4,000 in the first 3 months from account opening, you will get 50,000 bonus points. These points are worth $625 if you redeem them for travel through Chase Ultimate Rewards.

Details

You can earn an unlimited two points per dollar for travel and dining at restaurants. And then get one point per dollar for all other purchases. Points will transfer equally to 13 leading frequent travel programs with partners. So, these include British Airways, Southwest Airlines, United, and Marriott.

There is no 0% introductory APR on purchases or balance transfers. The card’s standard APR is 17.74 – 24.74% variable. Also, the card has an annual fee of $0 introductory for the first year. And then it skyrockets to $95.

Get it here: https://creditcards.chase.com/rewards-credit-cards/chase-sapphire-preferred

Ink Business Preferred ℠ Credit Card

Get a look at the Ink Business Preferred Credit Card from Chase. Cardholders earn 3 points for every dollar spent on travel, shipping, internet, cable, phone and qualifying advertising with the card. So, this is up to $150,000 each year. And all other purchases earn an unlimited one point per dollar spent.

This is a Visa credit card.

Cardholders get benefits like purchase protection, trip cancellation or interruption insurance. They also get cellphone protection. And they get extended warranty coverage. And they get an auto rental collision damage waiver.

Details

Earn 80,000 bonus points when you spend $5,000 in the first 3 months from account opening. There is an annual fee of $95. You can add employee cards at no additional cost.

This credit card only offers 3 points per dollar to a limit of $150,000 a year. So, this is for travel, shipping, internet, cable, phone and qualifying advertising. All other purchases get an unlimited flat rate of one point per dollar. And there is no introductory APR

Get it here: https://creditcards.chase.com/small-business-credit-cards/ink-business-preferred

Establish business credit fast with our research-backed guide to 12 business credit cards and lines.

Small Business Credit Cards for Luxurious Travel Points

IHG ® Rewards Club Premier Credit Card

Check out the IHG ® Rewards Club Premier Credit Card. it earns hotel rewards worldwide. For each dollar spent at participating IHG hotels, get 10 points. Get two points per dollar spent at gas stations, grocery stores and restaurants.

Plus all, other purchases earn one point. New cardholders can get an 80,000-point sign-up bonus when they spend $2,000 in the first three months of account opening.

Details

This card offers a free one-night hotel stay annually. Plus, there is a wide array of benefits. These include travel and purchase coverage and an upgrade to Platinum Elite status with the IHG Rewards Club. The club offers complimentary room upgrades when available and guaranteed room availability.

The most significant issue is that the card does not have a zero percent APR introductory rate. And the standard APR is 17.99 – 24.99% variable. Also, the yearly fee is $89.

Get it here: https://creditcards.chase.com/a1/ihg/premiernaep

Marriott Rewards® Premier Plus Credit Card

This credit card earns six points/dollar spent at participating Marriott and SPG hotels. And get two points/dollar on all other purchases.

Spend $3,000 in the initial three months from account opening. And earn two free night awards (each has a value of up to 35,000 points).

Cardholders get access to perks including a free one-night stay yearly after account anniversary. Also get travel and purchase protection. So, this includes free standard in-room Wi-Fi and priority late checkout.

Details

Perks include baggage delay reimbursement, and lost luggage reimbursement. There is also trip delay reimbursement. And there is purchase protection. In addition, there are concierge service and automatic Silver Elite status, which includes a 20% bonus on points.

Spend $35,000 each account year, and get an upgrade to Gold Elite status. So, that includes a complimentary room upgrade, free daily breakfast and 4 PM late checkout.

There is an annual fee of $95. The APR is a 17.99– 24.99% variable.

Get it here: https://creditcards.chase.com/marriott/apply

The Perfect Corporate Credit Cards Using EIN Only for You

Your outright best corporate credit cards using EIN only will hinge on your credit history and scores.

Only you can pick which features you want and need. So, be sure to do your homework. What is outstanding for you could be catastrophic for another person.

And, as always, make certain to establish credit in the recommended order for the best, quickest benefits.

The post Get Corporate Credit Cards Using EIN Only appeared first on Credit Suite.

How to Find the Best Business Loans for Disabled People

Those with disabilities run businesses every day. While there are not a lot of business funding resources available specifically for those with disabilities, some loans work better for them than others. Typically, you would have to wade through everything that’s out there to find the best business loans for disabled people. That could take forever. We try to narrow it down a little.

Where to Start to Find the Best Business Loans for Disabled People

Of course, there are some highly variable factors at play. Whether you are disabled or not, your credit score will make a difference when looking for business loans. Other factors will come into play as well, such as length of time in business and annual revenue. For traditional lenders, credit is still king. The best business loans for disable people with a high credit score (650 or over) include the following.

Best Business Loans for Disabled People: USDA Business Loans

These are loans from the United States Department of Agriculture. They don’t provide loans directly. Rather, they guarantee loans from lenders and provide funds to agencies that act as intermediaries. Since a large share of disabled Americans are in rural communities, the USDA’s focus on these areas is a bonus.

The most popular of the USDA’s many business loan programs is the Business and Industry Guarantee Program. The USDA helps guarantee loans made to businesses in rural areas through this program. By USDA definition, a rural area has fewer than 50,000 residents. Therefore, if your business is located in an area that fits this definition, you could qualify. However, you will also need good credit, adequate business revenue, and potentially some collateral.

Learn business loan secrets and get money for your business.

Best Business Loans for Disabled People: SBA 7(a) Loans

Another option for disabled people with good credit is an SBA loan. Like the USDA, the SBA does not issue loans directly. They guarantee loans made through specific lenders. The 7(a) loan program is the SBA’s most popular. It offers up to $5 million in funding and repayment terms that go up to 25 years.

Entrepreneurs can use these funds to buy commercial real estate, expand a business that is already in operation, start a new business, buy equipment, and more. Not everyone will qualify however. In addition to a credit score of 650 or above, businesses operating for at least two years and already producing revenue are more likely to get approval. Collateral is also a likely requirement. The process takes several weeks.

Best Business Loans for Disabled People: SBA Microloans

The really cool thing about these loans is that you can qualify with credit that is between 550 and 650. They offer up to $50,000 in funding, so they are a great option for micro or home-based businesses. They can be used for hiring, launching a new location, and even remodeling your office. Accion, one of the partner lenders, will work with scores as low as 575. They focus more on the expected income during the loan term than current financial position.

Best Business Loans for Disabled People: SBA Community Advantage Loans

The goal of these loans is to get funds to business owners in underserved groups. This, of course, includes disabled people. They go up to $250,000, so large investments work well with these funds. The application process works the same as with other small business loans in that you need to find an SBA partner lender. Use this tool to find a lender.

Business Loans for Disabled People: Non-Traditional Lender Options

The SBA works with traditional lenders to help get loan funds in the hands of those that may not be able to qualify under traditional requirements. While the government guarantee helps, sometimes it still isn’t enough. If you find this is the case with your, business consider applying for loans from non-traditional lenders.

OnDeck

With OnDeck, applying for financing is quick and easy. Apply online, and you will receive your decision once application processing is complete. Loan funds will go straight to your bank account. The minimum loan amount is $5,000. The maximum is $500,000.

You must have a personal credit score of 600 or more. Also, the business has to be in operation for at least one year. There is an annual minimum revenue requirement of $100,000 as well. In addition, there can be no bankruptcy on file in the past 2 years and no unresolved liens or judgements.

StreetShares

StreetShares began as a service to veterans. These days, they offer term loans, lines of credit, and contract financing. They also offer small business loan investment options. The maximum loan amount is $250,000. Pre Approval only takes a few minutes. They use a soft pull on your credit so it doesn’t affect your score.

To be eligible, you have to be in business for at least 12 months with annual revenue of $25,000. Exceptions are possible however. For example, with loans to companies in business for at least 6 months that have higher earnings, they make decisions on a case by case basis. The borrower’s credit score must be at least 620. For more on StreetShares, see our in-depth review.

Kabbage

Kabbage is an online lender. They offer a small business line of credit that can help businesses meet their goals quickly. The minimum loan amount is $500, and they do not exceed $250,000. You must be in business for at least one year and have $50,000 or more in annual revenue, or $4,200 or more in monthly revenue, over the last 3 months.

Learn business loan secrets and get money for your business.

Kabbage is great if you need cash quickly. Also, their non-traditional approach puts less weight on your credit score, so they may work better for some borrowers than other lenders.

Business Loans for Disabled People: Business Credit Cards

Business loans for disabled people are not easy to get. If your personal credit is totally shot and you are having trouble getting enough funding through business loans, business credit cards can help. Of course, you’re thinking if your credit isn’t good enough to get loans, how are you going to get credit cards?

First, credit cards are easier to get regardless. Those with poor credit scores can still get cards, they just have higher rates and lower limits. However, if you build credit for your business, known as business credit, you can get great business cards and fund your business quite successfully without bringing your personal credit into the picture at all.

Why Should Disabled Business Owners Build Business Credit?

Not just disabled business owners, but all business owners should build credit for their business that is separate from their own. Here’s why. If you have strong business credit you can get business credit cards with favorable terms and nice rewards regardless of what your personal credit looks like. Also, if your business runs into problems, your personal credit will be protected and you will still be able to do things like buy a car or a house.

Business Loans for Disabled People: How to Build Business Credit to Apply for Business Credit Cards

The first thing you have to do is ensure accounts in your business name report to your business credit report and not your personal credit report. Do this by setting up your business as a fundable entity apart from yourself. Start by making sure your business has its own phone number and address that is not the same as yours. Be sure to get these listed in the business 411-directories.

Then, you need to get an EIN. You can do that at the IRS website for free. You’ll use it to apply for credit in place of your SSN. After that you have to incorporate. You can do so as a corporation, S-corp, or LLC. Do some research to determine which option will work best for your budget and liability protection needs, but you have to choose one.

There are just a few more things you need to do to make sure your business stands on its own credit wise:

- Get a D-U-N-S number

- Open a separate business bank account

- Put up a professionally designed and hosted business website. Make sure you have a business email address with the same URL as the website as well.

Business Loans for Disabled People: Build Business Credit

You cannot just apply for business credit cards in your business name right away. First, you have to establish tradelines with starter vendors. These are vendors in the vendor credit tier that will issue invoices with Net 30 or longer terms. While you may need to make a few initial purchases with these vendors to establish yourself as a customer before they will extend these terms, there is no personal credit check. They do sometimes want to see a certain amount of time in business however.

As you pay the invoices consistently and on-time, these vendors will report your payments to the credit reporting agencies, thus establishing your business credit profile. Some of the most common and easiest to start with are Uline, Quill, and Grainger.

Why Start Here?

These are the easiest to start with simply because they sell products that most any business can use on a daily basis. Items such as paper, toner, pens, pencils, packing supplies, and even janitorial supplies. After you order from them a few times, apply for net 30 terms, pay on time, and watch your business credit score start to build like a snowball rolling downhill.

Once you have 8 to 10 tradelines reporting your on-time payments to the credit agencies, you can start to apply to creditors in the other credit tiers.

- Retail Credit Tier– Credit attached to specific stores such as Amazon, Home Depot, and Best Buy.

- Fleet Credit Tier– Companies that offer credit for fuel purchases as well as automobile repair and maintenance.

- Cash Credit– These are the large, well-known credit companies such as Visa, MasterCard, and American Express.

As you can see, it all starts with building trade lines through the vendor credit tier. Then a whole credit world opens up to you!

Learn business loan secrets and get money for your business.

Business Loans for Disabled People: Assistive Technology Business Loans

If you have a disability that makes it necessary for you to use assistive technology to run your business, you could benefit from one of these loans. An example of this would be if you need an automobile that is wheel-chair accessible to make deliveries. Another example would be braille-compatible software, or a hands-free device to make business calls.

Most often these types of loans come from local lenders, and requirements for eligibility vary. The National Disability Institute offers assistive technology loans in New Jersey and New York that range up to $30,000. It is important to note that your credit can affect your ability to get these loans, but if you can show you have sufficient income to pay it back that will help a lot.

Business Loans for Disabled People: Disabilities Don’t Have to Stop You from Funding Your Business

Over the course of a lifetime, a disability can affect a person in a number of ways. You can feel like you are not able to do the same things others can. While this may be true in some cases, often having a disability doesn’t make a difference in what you can do. The difference that has to be made is how you do it. The vision impaired can read, just with their fingers instead of their eyes. The hearing impaired can talk, either with their hands or their mouths. Similarly, those with disabilities can fund a business, they just may have to go about it differently. There are resources for disabled business owners out there, but you have to know where to look.

While it can seem that your disabilities stop you from many things in life, they do not have to stop you from owning and running and successful business. There aren’t a ton of business loans for disabled people exclusively, but there are plenty of options that work well for all types of business owners. Take the time to do the research you need to and figure out what’s out there, what you qualify for, and what you actually need. In the meantime, start building your business credit so you can access business funding at any time. You’ll be glad you did.

The post How to Find the Best Business Loans for Disabled People appeared first on Credit Suite.

Curebase (YC S18) hiring for engineering and sales to reinvent clinical research

Article URL: https://angel.co/company/curebase/jobs

Comments URL: https://news.ycombinator.com/item?id=21766411

Points: 1

# Comments: 0

New comment by KurtisL in "Ask HN: Who is hiring? (December 2019)"

SigOpt | Research Engineer | Onsite San Francisco, CA | Fulltime

https://jobs.lever.co/sigopt/bdff1bd1-ed90-468b-a1b2-020c803…

SigOpt provides an enterprise, hosted service for model development and black box optimization. We’re looking for brilliant and enthusiastic researchers to learn, grow, and build with us!

Research at SigOpt

SigOpt is a service that helps customers efficiently develop effective models in an efficient and data-secure fashion. As customers report the relationship between our recommended model designs and the associated performance, we implement algorithms internally to interpret this relationship and suggest new model designs that may reach higher performance. Our algorithms must be able to perform under various customer circumstances and computational restrictions, and they must yield robust performance for our customers to trust their model development to SigOpt.

Project Ownership: Research engineers are entrusted to own much of the development process for many of our most important and differentiating features. These critical elements of our product require the passion and rigor which defines a research mentality, and research engineers are expected to design and execute (in conjunction with other engineers) the strategies for designing and executing these key projects.

Working at the Cutting Edge: The tools that we provide for our customers must be based on the latest research developments from throughout the mathematics, statistics and machine learning communities. We invest time in reading articles and participating in conferences to know the current state of the community so that we can bring the best tools to bear on our customer’s problems. Research engineers have the important job of developing and/or adapting these strategies to fit in the constraints of an enterprise SaaS black-box solution.

Teamwork: Everyone on the research team has their own expertise and perspective on the research community: statistics, mathematics, operations research and machine learning all contribute to the core of our product. We want all researcher engineers to be both humble teachers and active learners to build the best and most comprehensive team possible. The research team also regularly hosts interns, and interested team members have the opportunity to mentor the next generation of researchers.

Communicating to the World: One of the key ways the research team contributes at SigOpt is by being effective communicators. This can be by documenting our work internally, developing feature/product documentation which speaks to advanced users, developing educational material to bolster SigOpt’s conference presence, writing blog content to present ideas/methodologies to the broad community, or writing articles for conferences/workshops to the research community. We also regularly collaborate with external partners on projects ranging from materials science to artwork.

User Engagement: An important part of SigOpt’s effectiveness lies in understanding our customer’s needs and values. Research engineers are encouraged to spend time with the customer success team during customer meetings to better empathize with customer goals and devise better strategies for serving their needs. This opportunity is unique to life at a small company, and, when successfully executed, this can be the most important element of product discovery/development.

Get Corporate Credit Cards Using EIN Only

Here’s How to Get Corporate Credit Cards Using EIN Only Is it possible to get corporate credit cards using EIN only? Absolutely! We looked at a ton of company credit cards and did the research for you. So, here are our preferences. Per the SBA, company credit card limits are a whopping 10 – 100 … Continue reading Get Corporate Credit Cards Using EIN Only

How to Get More Organic Traffic Without Doing Any SEO (Seriously)

You

all know SEO is a long-term game… at least when it comes to Google.

And yes, who doesn’t want to be at the top of Google for some of the most competitive terms? But the reality is, we don’t all have the budget or time.

So

then, what should you do?

Well, what if I told you there were simple ways to get more organic traffic and, best of all, you don’t have to do one bit of SEO?

Seriously.

So,

what is it? And how can you get more organic traffic?

Well,

this story will help explain it…

The

old days

When

I first started my journey as an SEO, I got really good at one thing.

Getting

rankings!

Now to be fair, this was back in 2003 when it wasn’t that hard to rank on Google (or any other search engine for that matter).

Stuff some keywords into your page, your meta tags, and build some spammy rich anchor text links and you were good to go.

You

could literally see results in less than a month.

SEO wasn’t too complicated back then. So much so, that I even started an SEO agency and created a handful of sites.

I was starting to rank my sites at the top of Google but they didn’t make a dollar. Literally, not a single dollar.

In fact, I was actually losing money on them because I had to pay for the domain registration expenses and hosting.

So, one day I decided that I was tired of losing money and I was going to do something about it. I took the keywords that I was ranking for and started to type them into Google to see who was paying for ads for those terms.

I hit up each of those sites and tried to get a hold of the owner or the person in charge of marketing.

I asked them how much they were paying for ads and offered them the same exact traffic for a much lower price. I was able to do this because I already had sites that ranked for those keywords.

In other words, I offered to rent out my website for a monthly fee that was a fraction of what they were paying for paid ads.

Next thing you know I was collecting 5 figures in monthly checks and my “renters” were ecstatic because they were generating sales at a fraction of the costs compared to what they were spending on paid ads.

So, what’s the strategy?

Well, it’s simple. Back in the day, I used to rent out my websites… the whole site.

These

days I’ve learned how to monetize my own site, so I don’t rent them out.

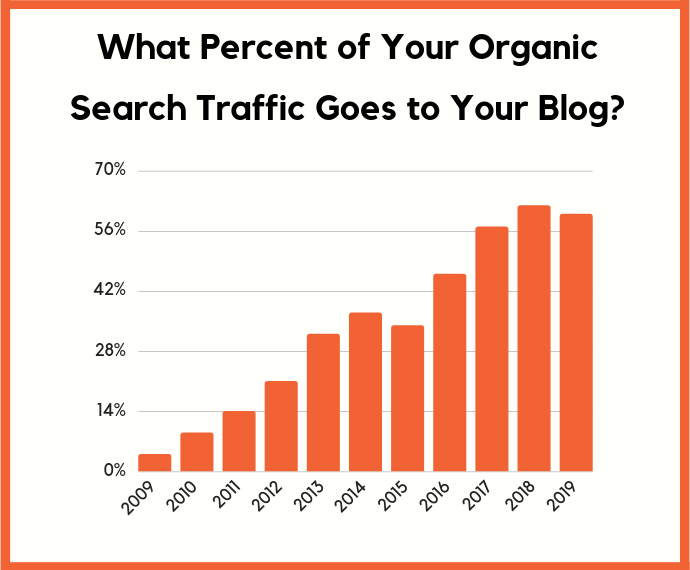

But you know what, most of the sites that rank on Google are content-based sites. Over 56% of a website’s organic traffic is typically going to their blog or articles.

So why not rent a page on someone else’s site? From there, modify that page a bit to promote your products or services?

I

know this sounds crazy, but it works. I have one person that just reaches out

to site owners asking if we can rent out a page on their site. We do this for

all industries and verticals… and when I look at how much we are spending

versus how much income we are generating, it’s crazy.

Here are the stats for the last month:

Rental

fees: $24,592

Outreach costs: $3,000

Legal

costs: $580

Copywriting

and monetization costs: $1,500

Total

monthly cost: $29,672

Now

guess what my monthly income was?

It

was $79,283.58.

Not

too bad.

Now

your cost on this model won’t be as high as mine because you can do your own

outreach, monetize the page you are renting on your own, and you probably don’t

need a lawyer.

And don’t be afraid of how much I am spending in rental fees as you can get away with spending $0 in the first 30 days as I will show you exactly what to do.

Remember, it’s also not what you are spending, it’s about profit and what you are making. If it won’t cost you any money in the first 30 days and you can generate income, your risk is little to none.

Here

are the exact steps you need to follow:

Step

#1: Find the terms you want to rank for

If

you already know the terms you want to rank for, great, you can skip this step.

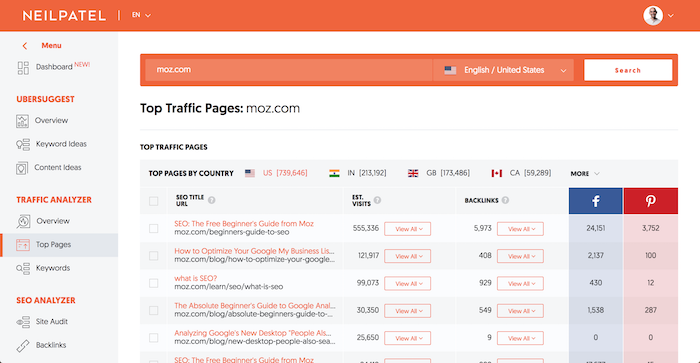

If you don’t, I want you to head to Ubersuggest and type in a few of your competitors’ URLs.

Head

over to the top pages report and look at their top pages.

Now

click on “view all” under the estimated visits column to see a list of

keywords that each page ranks for.

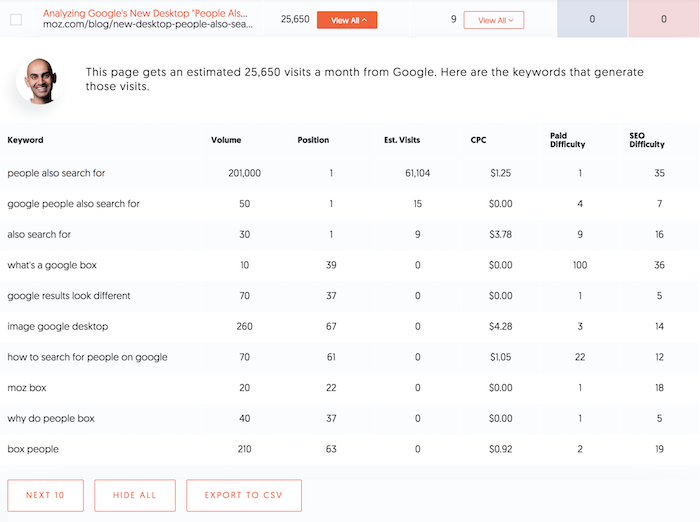

I want you to create a list of all of the keywords that contain a high search volume and have a high CPC. Keywords with a high CPC usually mean that they convert well.

Keywords

with a low CPC usually mean they don’t convert as well.

When

you are making a list of keywords, you’ll need to make sure that you have a

product or service that is related to each keyword. If you don’t then you won’t

be able to monetize the traffic.

Step

#2: Search for the term

It’s

time to do some Google searches.

Look

for all of the pages that rank in the top 10 for the term you ideally want to

rank for.

Don’t

waste your time with page 2.

What

I want you to look for is:

- Someone who isn’t your competitor. Your competition isn’t likely to rent out a page on their site to you.

- A page that isn’t monetized. Not selling a product or service. (If the page has ads, don’t worry.)

- A site owned by a smaller company… a publicly-traded company isn’t likely to do a deal. A venture-funded company isn’t likely to do a deal either (Crunchbase will tell you if they are venture-funded).

Step

#3: Hit up the website

Typically, through their contact page, they should have their email addresses or phone number listed. If they have a contact form, you can get in touch that way as well.

If

you can’t find their details, you can do a whois

lookup to see if you can find their phone number.

What’ll

you want to do is get them on the phone. DO NOT MAKE YOUR PITCH OVER EMAIL.

It

just doesn’t work well over email.

If

you can’t find their phone number, email them with a message that goes

something like this…

Subject: [their website name]

Hey [insert first name],

Do you have time for a quick call this week?

We’ve been researching your business and we would like to potentially make you an offer.

Let me know what works for you.

Cheers,

[insert your name]

[insert your company]

[insert your phone number]

You

want to keep the email short as I have found that it tends to generate more

calls.

Once you get them on the phone, you can tell them a little bit about yourself. Once you do that, tell them that you noticed they have a page or multiple pages on their website that interest you.

Point

out the URL and tell them how you are interested in giving them money each

month to rent out the page and you wouldn’t change much of it… but you need

some more information before you can make your offer.

At this point, you’ll want to find out how much traffic that page generates and the keywords it ranks for. They should have an idea by just looking at their Google Analytics (you’ll find most of these sites don’t use Google Search Console).

Once

you have that, let them know that you will get in touch with them in the next

few days after you run some numbers.

Go back, try to figure out what each click is worth based on a conservative conversion rate of .5%. In other words, .if 5% of that traffic converted into a customer, what would the traffic be worth to you after all expenses?

You’ll

want to use a conservative number because you can’t modify the page too

heavily or else you may lose rankings.

Once

you have a rough idea of what the page is worth, get back on the phone with

them and say you want to run tests for 30 days to get a more solid number on

what you can pay them as you want to give them a fair offer.

Typically,

most people don’t have an issue because they aren’t making money from the page

in the first place.

Step

#4: Monetize the page

If

you are selling a product, the easiest way to monetize is to add links to the

products you are selling.

For

example, if you are selling a kitchen appliance like a toaster, you can add

links from the article to your site.

The easiest way to monetize a blog post is to add links to products or services you are selling.

Don’t delete a lot of the content on the page you are modifying… adding isn’t too much of an issue but when you delete content sometimes you will lose rankings.

As

for a service-based business, linking out to pages on your site where people

can fill out their lead information is great.

Or you can just add lead capturing to the page you are renting out. Kind of like how HubSpot adds lead forms on their site.

I’ve actually found that they convert better than just linking out to your site.

When monetizing the page you are renting, keep in mind that you will need disclaimers to let people know that you are collecting their information for privacy purposes. You also should disclose you are renting out the page and nofollow the links.

Once you are monetizing the page for a bit, you’ll have a rough idea of what it is worth and you can make an offer on what you’ll page.

I recommend doing a 12-month contract in which you can opt-out

with a 30-day notice.

The reason you want a 12-month agreement is that you don’t want to have to keep renegotiating. I also include the 30-day opt-out notice in case they lose their rankings, you can opt-out.

And to clarify on the op-out clause, I have it so only I can opt-out and they are stuck in the agreement for a year.

Conclusion

SEO isn’t the only way you can get more organic traffic.

Being creative, such as renting pages that already rank is an easy solution. Best of all, you can get results instantly and it’s probably cheaper than doing SEO in the long run.

The only issue with this model is that it is really hard to

scale.

If I were you, I would do both. I, of course, do SEO on my own site because it provides a big ROI. And, of course, if you can rent out the pages of everyone else who ranks for the terms you want to rank for, it can provide multiple streams of income from SEO.

The beauty of this is model is that you can take up more than one listing on page 1. In theory, you can take up all 10 if you can convince everyone to let you rent their ranking page.

So, what do you think of the idea? Are you going to try it out?

The post How to Get More Organic Traffic Without Doing Any SEO (Seriously) appeared first on Neil Patel.