Dagen McDowell and the panel on “The Five” Thursday discussed President Biden’s July call with former Afghan President Ghani to portray the situation in Afghanistan as better than the reality on the ground.

Tag: 2019

Leclerc's extension shows how he reshaped Ferrari in 2019

Charles Leclerc joined Ferrari as No.2 driver but has always established himself as Sebastian Vettel’s equal, evidenced in Ferrari’s decision to extend his contract until 2024.

The post Leclerc's extension shows how he reshaped Ferrari in 2019 appeared first on Buy It At A Bargain – Deals And Reviews.

The Best Small Business Credit Card of 2019 for Any Situation

fwistAnd How to Be Sure You are Eligible for the Best Small Business Credit Card for Your Situation When you start wondering what the best small business credit card is, you may be surprised to find out that answer actually can vary. What may be the best credit card for one business may not necessarily … Continue reading The Best Small Business Credit Card of 2019 for Any Situation

The Best Small Business Credit Card of 2019 for Any Situation

fwistAnd How to Be Sure You are Eligible for the Best Small Business Credit Card for Your Situation

When you start wondering what the best small business credit card is, you may be surprised to find out that answer actually can vary. What may be the best credit card for one business may not necessarily be the best small business credit card for another. It all depends on the business and the situation. For example, a business owner that does a lot of travel for his or her business is going to need a different card than one that has a whole fleet of automobiles to manage but doesn’t travel much.

We have done some research to help you find the best small business credit card to fit your specific needs.

Best Small Business Credit Card When You Want 0% APR

Capital One® Quicksilver® Card

This card features flat-rate rewards of 1.5% on all purchases, and there are no limits on cash back rewards. In addition, there is no yearly fee.

New cardholders have a 0% APR on purchases and balance transfers for the first 15 months after starting the account. Afterwards, the rate increases to 14.74 to 24.74% (variable). A cash bonus of $150 is available for those who make at least $500 on purchases within 3 months of account opening.

Also, cash back rewards do not expire for the life of the account. Other benefits include travel accident insurance and an auto rental collision damage waiver. Find out more by going here.

Best Small Business Credit Card When You Want No Annual Fee

Capital One® Spark® Classic for Business

Try the Capital One Spark Classic for Business. It earns an unlimited 1% cash back on all purchases, and you still get the benefits of an auto rental collision damage waiver and purchase security. You also get extended warranty coverage, as well as travel and emergency assistance services.

However, the ongoing APR is 24.74% variable. The penalty APR is even higher at 31.15%. Another drawback is that there is no sign-up bonus. Find out more here.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

Best Small Business Credit Card for Students

Discover it® Student Cash Back

Okay, full disclosure. The Discover it® Student Cash Back card is not a business credit card. It’s a personal card, therefore your credit activity is reported on your personal credit and not your business credit. However, as a student, building your FICO will be important to your future as a business owner.

There is a six-month introductory period of 0% APR on purchases. After that, there is an APR of 14.99 to 23.99% variable on all purchases.

One special feature is that it provides an incentive for students to maintain good grades with a $20 statement credit. If students earn a GPA of 3.0 or higher each school year, they get a $20 statement credit per year for up to five years.

You can get 5% cash back at different places each quarter like grocery stores, filling stations, restaurants or Amazon.com up to the quarterly maximum. After that, the credit card offers unlimited 1% cash back on all purchases. Also, in the first year, all cash back rewards are matched 100%.

Although they waive the first late payment fee, a fee of up to $37 applies on all other late payments. There is also a returned payment fee of up to $37. Find more information here.

Best Small Business Credit Card for Mileage Rewards

United MileagePlus Explorer Business Card

Earn 2 miles per dollar with United and at restaurants, filling stations, and office supply stores. All other purchases earn 1 mile per dollar. There is also a 50,000-mile sign-up bonus after spending $3,000 in the first three months from account opening.

Benefits include priority boarding, a free first checked bag for you and a companion on the same reservation. Also, get two United Club passes annually. Hotel and resort perks, including upgrades, are available as well. Additionally, get early check-in and late checkout. An auto rental collision damage waiver is also a benefit.

After the first year, the card has an annual fee of $95. The APR is 17.99% to 24.99%, based on creditworthiness. Find out more here.

Best Small Business Credit Card if You Have Average Credit

Capital One® Spark® Classic for Business

For fair credit, we like the Capital One Spark Classic for Business. It has no yearly fee and cash-back rewards of unlimited 1% cash back on all purchases. Benefits include an auto rental collision damage waiver and purchase security. In addition, extended warranty coverage as well as travel and emergency assistance services are included. Find out more here.

Best Small Business Credit Card if Luxurious Travel is Your Thing

Chase Sapphire Preferred® Card

Earn two points per dollar spent on travel and dining at restaurants, and one point per dollar on all other purchases. Points can be redeemed for cash back, gift cards, or travel. Benefits include trip cancellation insurance, travel and emergency assistance services and an auto rental collision damage waiver. Purchase protection and extended warranty protection are also included.

When you spend $4,000 in the first 3 months from account opening, you will earn 50,000 bonus points. These points are worth $625 if you redeem them for travel through Chase Ultimate Rewards.

You can get an unlimited two points per dollar for travel and dining at restaurants. And then get one point per dollar for all other purchases. Points will transfer equally to 13 leading frequent travel programs with partners. These include British Airways, Southwest Airlines, United, and Marriott.

Unfortunately, there is no 0% introductory APR on purchases or balance transfers. The card’s standard APR is 17.74 to 24.74% variable. In addition, while there is no annual fee the first year, after that it is $95. Go here for more information.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

Best Small Business Credit Card if You Love Uber

Uber Visa Card

Uber is the first ride-sharing service to offer a credit card, in a partnership with Visa and Barclays. The card offers 4% back per dollar spent at restaurants, takeout, and bars. That includes UberEATS orders. Also, earn 3% back on hotel, airfare and vacation home rentals. You can also earn 2% back on online purchases including retailers and subscription services like Uber and Netflix.

Additionally, you’ll earn 1% back on all other purchases. Every percent/point has a value of 1 cent. Redeem points for cash back, gift cards, or Uber credits directly within the app.

There is no yearly fee, and by spending at least $500 in the first 90 days, users can earn a $100 sign-up bonus. Cardholders spending a minimum of $5,000 yearly are eligible to get a $50 credit toward online subscription services.

Also, if you pay your cellphone bill with this card, you are insured up to $600 for cell phone damage or theft.

While they note cardholders have exclusive access to certain events and offers, Uber anticipates the majority of these offers will be available in major cities like New York, San Francisco, Los Angeles, Chicago and DC. If you aren’t in those cities, that perk may not be one you are interested in.

There is no introductory rate, and the APR is a variable 16.99%, 22.74%, or 25.74%, based on your creditworthiness. Cardholders with lower credit will be on the higher end of the range.

Also, there are restrictions on Uber credits. To redeem points as credits within the Uber app, you must have at least 500 points, or $5. Cardholders can convert a maximum of 50,000 points, or $500, in a given day. Find out more here.

Best Small Business Credit Card for When You Want to Build Business Credit

This is where it gets a little tricky. The thing is, the only way a card can help you build business credit is if you get it on the merits of your business credit. That means you have to apply with your business information, not your own. It also means you must already have some semblance of business credit to gain approval. Any card in your business name that you handle responsibly will definitely help build existing credit even stronger. However, you cannot get a card to build business credit without already having a business credit score.

How Do You Establish a Small Business Credit Score?

The truth is, any of these best small business credit card options will work to build business credit, but they will all want to see a business credit score before they grant approval. How do you get a business credit score without having credit to begin with? There is a very specific process, and if you follow it, it works like a charm.

It starts with establishing your business as a separate entity from yourself that appears fundable to lenders. How does that happen? Well, first your business needs its own contact information. It’s tempting in the beginning to just use your own address and phone number, but it isn’t wise. Those are identifying factors related to you personally, so anything attached to them will end up on your personal credit report rather than your business credit report.

Other Ways to Make Your Business Appear Fundable to Lenders

- Formally incorporate. You need to organize your business as a corporation, S-corp, or LLC. Start at gov.

- Get an EIN. It works like an SSN, but for your business. You can get one for free on the IRS Be sure to use it instead of your SSN when applying for business credit cards.

- Get a separate business bank account.

- Make sure you have a useable, professionally put together website. Pay for hosting, as the free hosting services make you look unprofessional. Along the same lines, be sure your business email address has the same URL as your website. Free email services such as Yahoo or Gmail are not appropriate for this purpose.

- Get a D-U-N-S number. This is how you establish your record with Dun & That’s important, because they are the largest and most commonly used business credit reporting agency. If you do not have a D-U-N-S number, you cannot have a business credit score with them. It is free to get one on the Dun & Bradstreet website.

Once these things are taken care of, it’s time to start building that business credit score.

Work Through the Credit Tiers

When it comes to building business credit, there are 4 tiers that you must work through. Most often, whatever the best small business credit card is for your needs, it will be in the top tier, known as the cash credit tier.

Before you can qualify for credit in this tier however, you must work through the other tiers. What are the other tiers? I am so glad you asked.

Vendor Credit Tier

This tier is where you will find starter vendors that will extend invoices with net terms without a credit check. You may have to place a few orders with them first, and there may be some minimum time in business or income requirements, but credit will not come into the picture.

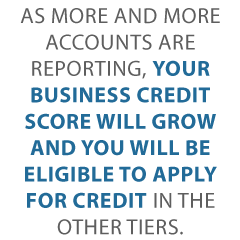

Once you get net terms and start making payments, these starter vendors will report those payments to the credit reporting agencies, also knowns as CRAs. If you have set up your business as a separate entity and set up your vendor account with your business information, they will report your payments to the business CRAs. As more and more accounts are reporting, your business credit score will grow and you will be eligible to apply for credit in the other tiers.

Hit the jackpot with our best webinar and its trustworthy list of seven vendors who can help you build business credit.

The Retail Credit Tier

This is where you find store specific cards. They like to see a minimum business credit score, which is why you apply for them after the vendor credit tier. The vendor credit tier is how you establish that initial score. You’ll need to get 8 or so of these accounts reporting your payments to the business CRAs before you can start applying for cards in the next tier.

The Fleet Credit Tier

These are the cards that help you manage fuel and auto maintenance and repair costs. They come from companies like Fuelman and Shell. You’ll need several of these reporting payments along with the cards from the retail credit tier before you can move on to the cash credit tier.

The Cash Credit Tier

This is where pretty much every best small business credit card mentioned above will be found. As you work through the other tiers your credit score will build like a snowball rolling downhill. If you manage your credit properly, you’ll have a strong score that will qualify for any of these cards. It takes time, but if you want the best small business credit card for your business, you must build business credit.

Don’t Let the Best Small Business Card for You Slip Through Your Fingers

If you already qualify for cards in the cash credit tier, then use our research above as a starting point for your own research. If you need to build business credit first, follow our proven process and you will be eligible for any of these cards when the time comes.

The post The Best Small Business Credit Card of 2019 for Any Situation appeared first on Credit Suite.

Email Marketing in 2019: Are You Utilizing Its Power?

Email marketing in 2019: Are You Utilizing Its Power? When it comes to marketing online, you can’t afford to ignore something as valuable as email marketing. In 2019, it is still going strong and is possibly one of the best strategies for your business. You might wonder, with so many ways to reach your prospects … Continue reading Email Marketing in 2019: Are You Utilizing Its Power?

The 4 Best Small Business Loans of 2019

And 5 Practical Tips for Landing the Best Small Business Loans

If you need a small business loan, you shouldn’t settle for just any loan. You want the best. You’re in luck, because we not only have a list of the best small business loans of the year, but we also have in depth reviews and practical tips to help you find not just the best, but the best for your specific business. Let’s take a closer look.

Where Do You Find the Best Small Business Loans?

I know, you are wondering how there can be more than one best. The best is the best, and there is only one best when it comes to most things. Business loans don’t work exactly the same way. The best loan for your business may be different than the best loan for the next business. That’s because your business will likely have different needs and qualifications than the next one.

US News handles this by naming the best small business loans in different categories. This year, these took the prize:

- OnDeck: Best Lender for Small Business Loans of Up to $500,000

- BlueVine: Best Lender for Fast Funding

- Funding Circle: Best Lender for Small Business Loans with a Low APR

- StreetShares: Best Lender with Prequalification Available

In addition to this list from US News, we would like to add our own bonus category of “Best Lender for Faster, Easier SBA Loans.” That award, in our opinion, would go to SmartBiz. They have totally streamlined the Small Business Administration loan program application process making it both faster and easier.

Well that’s all great of course, but to make a true informed decision, you need details. What makes these the best?

Learn business loan secrets with our free, sure-fire guide.

OnDeck

OnDeck offers lines of credit and term loans with fixed interest rates. You can’t get up to $500,000 with a term loan. They also have an A rating with the Better Business Bureau. The minimum FICO they require is 600. In addition, you must have $100,000 minimum annual revenue and be in business for at least one year. Find out more about OnDeck in our review.

BlueVine

BlueVine offers a number of financing options including term loans, invoice financing, equipment financing, lines of credit, and merchant cash advances. They require you to be in business for at least 6 months. If you need a term loan or a line of credit, then they require a minimum annual revenue of $100,000. If you are trying to get invoice factoring, the minimum credit score is just 530! For a line of credit or term loan, you will need a minimum credit score of 600. They have an A+ rating with the BBB. Find out more about BlueVine in this review.

Funding Circle

If you’re looking for a low APR, then Funding Circle is your go-to. They have fixed rate term loans and require a credit score of 620 or above. There is no minimum revenue requirement, but they do require you to be in business for at least 2 years. They have an A+ BBB rating. Find out more in our Funding Circle review.

StreetShares

This is considered by US News to be the best lender with prequalification available. They offer invoice financing, term loans, and lines of credit. The number of years in business requirement is one. They require less minimum annual revenue than the others at only $25,000. The minimum credit score is 600, and they also have an A+ rating with the Better Business Bureau. You guessed it. You can find out more about StreetShares in our review, here.

SmartBiz

SBA loans typically take a lot of time and paperwork. SmartBiz found a way to speed things up, making it easier than ever. The requirements are a little more strict however. Your credit score has to be 650, and you have to be in business for 2 years or more. In addition, annual revenue has to be $50,000 at least, and there can be no outstanding liens, bankruptcies, or foreclosures in the past 3 years.

Tips for Landing One of the Best Business Loans

1. Appear Fundable

What is fundable? A business that appears fundable to a lender is an established business separate from its owner. It is complete, organized, and either has solid revenue or a solid plan if a startup.

To appear fundable, a business needs:

- To be formally incorporated as an S-corp, LLC, or a corporation.

- An EIN from the IRS. This is an identifying number for your business that function similar to the way your SSN does for you personally.

- A dedicated business bank account.

- Contact information that is different from the owner’s. A separate telephone number on a toll-free exchange and a dedicated physical address are imperative.

- A professional website and an email address that has the same URL. Free web hosting and email services won’t do the job in this case.

2. Have a Killer Business Plan

Lenders are also going to want to see a professional business plan. Even if you are not a startup a plan is necessary. Startups have to show what they are planning and that they have done the research to make it work. Established businesses need to show how they plan to use the funds, and that they have research to show the market supports that plan.

At a minimum, a business plan should have the following sections.

- An Executive Summary– This is a complete summary of the business idea.

- Description– The description goes into further detail than the summary, describing the business. What type of business is it? What product or service will it offer?

- Strategies-Layout your plan for getting started. Do you have a marketing plan, area in mind for location, or idea of how many employees you will start with?

- Market Analysis– All that market research you did goes here and should include not only a market analysis but an analysis of the competition as well.

- Plan for Design and Development: How is all of this going to play out, from start to finish. What steps are you going to take? This is more detailed than your strategies section.

- Plan for Operation and Management– Who will own or does own the business and who will run or currently runs it from day to day.

- Financial Information– This section includes current financials, projections, and a budget plan for the loan funds you are applying for.

3. Be Prepared

It is almost impossible to over prepare when applying for a loan. Anticipate any questions they may ask. Pull together any forms or documentation they might ask for. Items such as past tax returns, financials, and licenses are common. The more you have ready to go before you start, the faster and easier the process will be.

Learn business loan secrets with our free, sure-fire guide.

4. Have Solid Personal Credit

You need a solid personal credit score to land the best small business loans. There is just no way around it. As you can see above, a score of at least 600 is required almost across the board with the exception of some invoice factoring options. If you do not have this score however, all is not lost.

It is possible to improve your personal credit score. The first step is to get a copy of your credit report. You can get a free copy each year. Look for what may be impacting your score negatively. If there are mistakes, contact the credit agency in writing to have them removed. If late payments are a problem, start paying on time. Knowing what you need to work on is the first step.

5. Have Solid Business Credit

Of course, when it comes to the best small business loans, you cannot ignore business credit. While it isn’t listed as a primary requirement for most lenders, it can only help you to have strong business credit.

If a lender sees a personal score that isn’t exactly what they need, it is possible they will take business credit into consideration when making their decision. In addition, if you qualify and have stellar business credit, you may be able to get a lower interest rate.

More Benefits of Business Credit

Since business credit is the one topic out of these 5 that people seem to question the most often, let’s talk about why it’s important. There are a number of reasons. The first one is, if you have business credit, your business transactions will not affect your personal credit report.

You may be thinking that it doesn’t matter, because you pay all your bills anyway. You would be wrong however. It absolutely matters. Here’s the thing. Personal credit cards often have lower limits than business credit cards. Conversely, business expenses are typically much higher than personal expenses. This means, if you are using personal cards for business expenses, you are likely to keep balances at or near your limits.

Consistent balances near your limits has a negative impact on your credit score even if you are making regular payments. If you have business credit cards, your limits will be higher and better able to accommodate the high expense of running a business.

How do You Get Business Credit?

The steps to looking fundable are also the first steps toward business credit. Your business has to be separate from yourself before business credit can be established. In addition, you will need a D-U-N-S number.

This is a number from Dun & Bradstreet that they use to enter you into their system and issue a business credit score. If you do not have a D-U-N-S number you will not have a credit file with them. Since they are the largest and most commonly used business credit reporting agency, you need to have a business credit profile with them. Get a D-U-N-S number for free on their website.

How Do You Get Business Credit if You Do Not Already Have It?

If you do not yet have business credit, you will need to open accounts in the vendor credit tier after you finish these steps. We all know that it is almost impossible to get credit if you do not already have credit. However, the vendor credit tier consists of vendors that will offer net 30 terms without a credit check, and then report your payments to the credit reporting agencies. After you have enough of these types of accounts reporting, you will have a credit score and be able to apply for accounts from different types of companies to grow it even more. Find out more about the vendor credit tier and building credit here.

Keep an Eye on Your Credit Reports

Both credit scores are so vital to being able to get the best business loans, it is important to talk about monitoring them. With personal credit scores, this is easy. You can get a free copy of your personal credit report every year. In addition, there are numerous websites that allow you to monitor your credit on a monthly basis for free.

Business credit monitoring isn’t as easy, and it definitely isn’t free. The credit agencies charge from $50 to over $100 for just one report. You can monitor your business credit at a fraction of the price at https://www.creditsuite.com/monitoring.

Don’t Forget Traditional Lenders

These business loans are from non-traditional lenders. This is because non-traditional lenders are generally more friendly toward small businesses than the traditional banks. Do not neglect to check into what your local traditional lenders may have available however. If your personal credit score is above 650, they may very well offer even better rates and terms than those listed above.

While big banks are not typically friendly toward small businesses, local community banks can be favorable if your credit is strong. Credit Unions are another option if you have a good credit score and are a member. Do your research before making a final decision.

Learn business loan secrets with our free, sure-fire guide.

The Best Small Business Loans Can be Yours

How do you land the best small business loans of the year? In short, you prepare. Do a fast check to ensure your business will appear fundable to lenders. Do some research to determine which loan options best fit your needs and qualification abilities. Don’t forget to see what traditional lenders have to offer as well. Get all the necessary paperwork, including your business plan, together before you begin the process. Then, take note of both your personal and business credit scores and determine if you need to make some adjustments to improve them. With these items checked off your list, the best small business loans really can be yours.

The post The 4 Best Small Business Loans of 2019 appeared first on Credit Suite.

Ben Stiller on 'Tropic Thunder,' Comedy in 2019, the Knicks, and His Biggest Career Lessons, Plus Bill's Dad | The Bill Simmons Podcast

HBO and The Ringer’s Bill Simmons is joined by Ben Stiller to discuss his new Showtime series ‘Escape at Dannemora,’ and making films including ‘Reality Bites,’ ‘The Cable Guy,’ ‘Something About Mary,’ ‘Meet The Parents,’ and ‘Zoolander.’ They talk about the difficulty of pursuing comedy in 2019, tortured Knicks fandom, and more (3:50). Then Bill calls up his dad to discuss Joel Embiid’s dominance, the Celtics’ playoffs hopes, the Patriots’ free agency, and more (1:28:25).

The post Ben Stiller on 'Tropic Thunder,' Comedy in 2019, the Knicks, and His Biggest Career Lessons, Plus Bill's Dad | The Bill Simmons Podcast appeared first on Buy It At A Bargain – Deals And Reviews.

The post Ben Stiller on 'Tropic Thunder,' Comedy in 2019, the Knicks, and His Biggest Career Lessons, Plus Bill's Dad | The Bill Simmons Podcast appeared first on WE TEACH MONEY LIFE SELF DEFENSE WITH FINANCIAL GOALS IN MIND.

The post Ben Stiller on 'Tropic Thunder,' Comedy in 2019, the Knicks, and His Biggest Career Lessons, Plus Bill's Dad | The Bill Simmons Podcast appeared first on Buy It At A Bargain – Deals And Reviews.

Stephen A. Smith on OKC’s Lost Chance, 2019 Talking Heads, and GSW’s Mini Dynasty. Plus: 2019 TV With Wesley Morris | The Bill Simmons Podcast

HBO and The Ringer’s Bill Simmons is joined by ESPN’s Stephen A. Smith to discuss NBA superteams, the 2020 NBA season, Kevin Durant’s search for … something, saving the Knicks, players vs. the media, and more (2:15). Then Bill sits down with the NYT’s Wesley Morris to discuss 2019 TV, including ‘Euphoria,’ ‘Fleabag,’ ‘Succession,’ ‘Billions,’ ‘PEN15,’ and more (56:29).

The post Stephen A. Smith on OKC’s Lost Chance, 2019 Talking Heads, and GSW’s Mini Dynasty. Plus: 2019 TV With Wesley Morris | The Bill Simmons Podcast appeared first on Buy It At A Bargain – Deals And Reviews.