The Fundability™ Roadmap: Your Business Credit Guide

Business credit is a journey, not a destination. The destination is Fundability , and business credit is just one of many tools you need along the way. If you’re interested, our business credit guide can help any user ensure their toolbox is well stocked.

, and business credit is just one of many tools you need along the way. If you’re interested, our business credit guide can help any user ensure their toolbox is well stocked.

Making this trip isn’t easy, but some routes are easier than others. We have the roadmap to starting Fundability, but you have to trust the process.

Business Credit Guide: What is Fundability?

It might help if we first define Fundability. Fundability is the ability of any business to get the funding it needs. Obviously any business will be interested in funding for the purpose of improving and to grow. That is the way to success, and being Fundable means you have access to the money to do it.

Business Credit Guide: How Businesses Can Get Started

The first step, before you even open the roadmap, is also one of the most important steps in the journey. Think of it like choosing the most efficient and comfortable vehicle for your trip. It doesn’t take an expert to figure out some types of transportation are better than others.

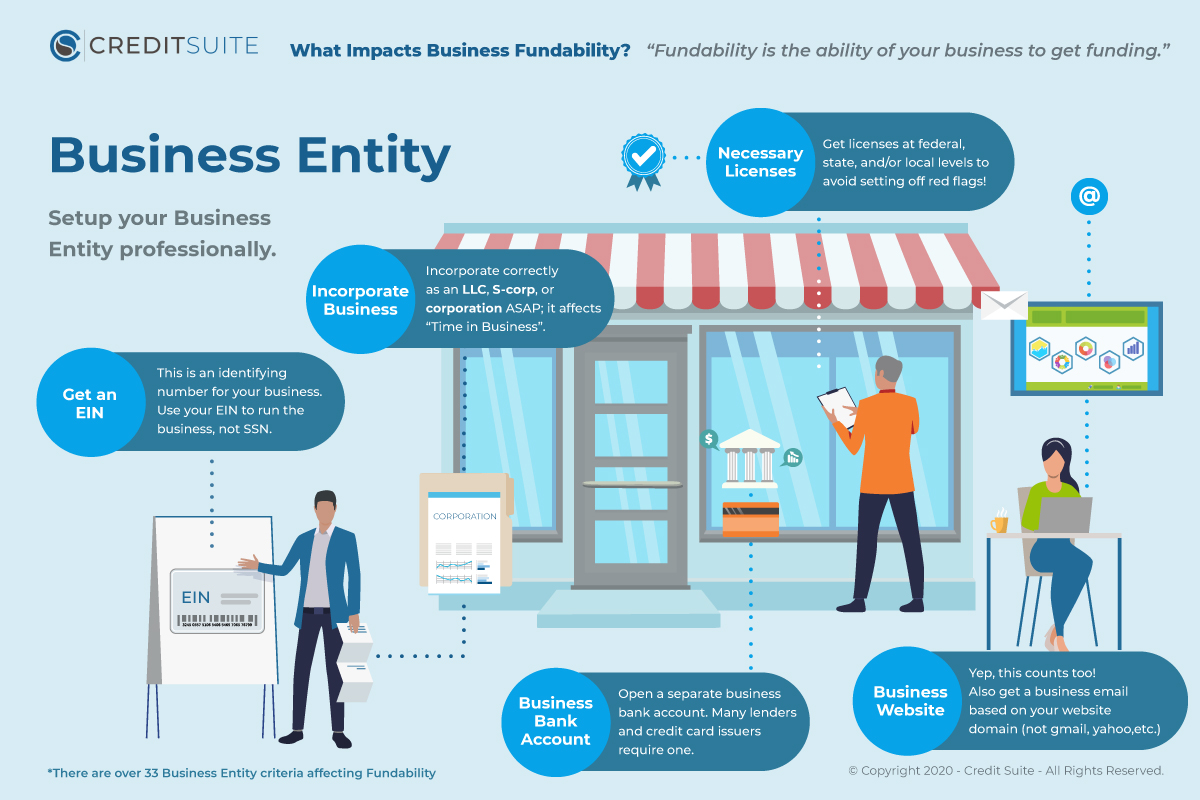

Just like that, a Fundable Foundation gives you the best start not just with Fundability, but with business credit as well. It will help you avoid issues that can slow down your ability to get approved for credit.

Businesses with a Fundable

- Separate business contact information

- EIN

- They are incorporated

- Business bank account

- Licenses

- Website and email separate from the founder

This is the easy part, but it is vitally important.

To be successful on the road to Fundability, there is more than this to consider. The goal is to have lenders see your business and you as the owner as low risk. Here are some things to think about.

Your Business Name Makes a Difference

When developing your business name, it’s best to leave any indication of a risky industry out of it. This may not help you get financing, but it will minimize the likelihood of being turned down immediately due to being linked to a risky industry before you get a chance.

It’s also important for your company name to be consistent and in alignment everywhere. Even inconsistencies in small details, like using the word “and” sometimes and an ampersand at others, can indicate higher risk. Lenders are not interested in why there is an inconsistency. They will just deny it.

Get a D-U-N-S Number from Dun & Bradstreet

All entrepreneurs need a D-U-N-S number from Dun & Bradstreet for their organization. Set your business up for success by getting it as soon as you can. It is how Dun & Bradstreet will identify your business in their network and how your PAYDEX is linked to your business.

Business Credit Guide: Start The Journey

Once you have the foundation, or the right vehicle to make the journey, it’s time to get on the road. Making sure you are prepared is the only way to reach where you are going.

The foundation is definitely something you can control. After that, it’s time to start establishing and building strong business credit. This is only part of what makes a business Fundable, but it is a big part. It’s important for most any type of company financing if you want to run a profitable business.

Business Credit Guide: Use Vendor Credit to Fuel Your Way to Becoming a Profitable Business

Now, it’s time to fill the car up with gas. That gas is business credit accounts that report payments to your business credit reports. It all starts with vendors. Not just any vendors however. Just like any journey, you have to start at the beginning.

Starter vendors are those that will give net terms on invoices. They are not as interested in credit scores, so you can get approved with less focus on that and more on other factors. Not only that, but they will also report the positive payment experience to the business credit reporting agencies.

How Do You Get Starter Vendors to Grow Business Credit?

At Credit Suite we discuss vendors in terms of tiers. Starter vendors are those in Tier 1. Since most vendors do not classify themselves as such, how do you get them? A simple search will give you a few options. However, how do you know if those vendors work with your company marketing and growth strategies? Furthermore, the information changes without warning.

It’s Worth It to Get Help from An Expert

The answer to all of these questions is Credit Suite. Our product includes select vendors that we know report, and what they require for approval.

We also track changes with recommended vendors. So, if they change requirements or reporting standards in ways that make them no longer align with the values we have for our clients, we can adjust.

Maybe they now rely more heavily on personal finance data and need to be moved from Tier 1 to another tier. Maybe they decided to adjust their minimum business credit requirement. Perhaps they no longer report payments? All of these things will stunt business credit growth.

Credit Suite will check in with your business at each level in the process. We will discuss the risk you present to lenders, and determine what needs to be done in order to reduce that risk.

Credit Suite Can Save You Time and Money

Our processes allow us to keep our vendor database updated. Our industry experts have the skills necessary to help clients find the best vendor options for them. Whatever stage of the journey our clients are in when they come to us, we can help them find the vendors that can best help them be successful, with confidence.

Working with Credit Suite to find starter vendors and to figure out which vendors to apply for when is kind of like using help to find a gas station that’s open in the middle of the night. It lets you avoid paying more money than you have to for gasoline.

Our resources get you where you are going faster. Team recommended strategies save you both time and money, and one of the best benefits is your business can grow and transform along the way. Our team uses best practices to add value.

Business Credit Guide: Refill Your Fuel Tanks and Get Financing to Grow

Starter vendors are just the first fill-up a company makes to get on the road, but it will only get you so far before your check engine light comes on. As you move further into the process, you’ll need to get credit with more vendors and apply for business credit cards to continue to operate. You can’t just sit back and read a good book, you have to keep moving.

If you handle your approved credit responsibly, you’ll soon have enough accounts reporting to more easily get business credit cards. Even better, you should be able to get higher limits, better rates, and less if any personal guarantee. This is the best way to grow and increase earnings. There are no shortcuts.

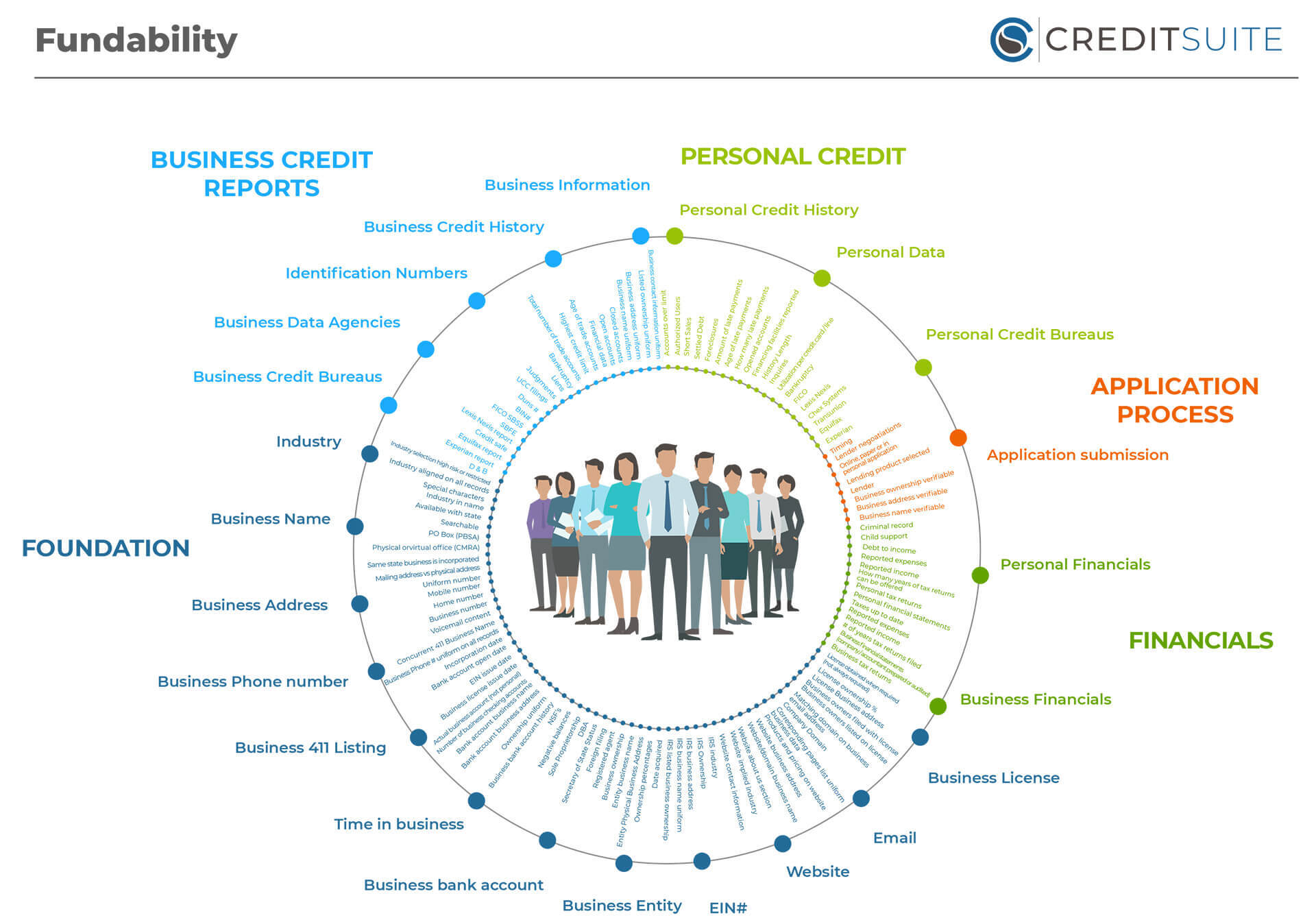

Other Factors that Support Fundability

Of course there are parts of the car you cannot see. There are curves and bumps in the road you may not be able to predict. As a result, things happen that you cannot control, making the trip quite uncomfortable at times. However, you can do your best to be prepared.

Here are a few things that can affect Fundability, and thus your ability to get money for your company easily, that you have less control over.

Other Business Data Agencies

In addition to the business credit reporting agencies that directly calculate and issue credit reports, there are other business data agencies that affect those reports indirectly. This can throw a kink in your business journey if you aren’t careful.

Two clear examples of this are LexisNexis and The Small Business Finance Exchange. These two agencies gather data on businesses from a variety of sources, including public records. This means they could even have access to data relating to automobile accidents and liens. They share this information with their partners, some of which are business credit bureaus.

Fight Back With Positive Data

While you may not be able to access or change the data these agencies have on your business, you can be making sure you always use strategies to guarantee any new information they receive is positive.

Enough positive data can help counteract any negative data from the past and reduce those risks over time. Consequently, your personal risk tolerance with underwriters will be easier to overcome. This is how you start to see your company success grow.

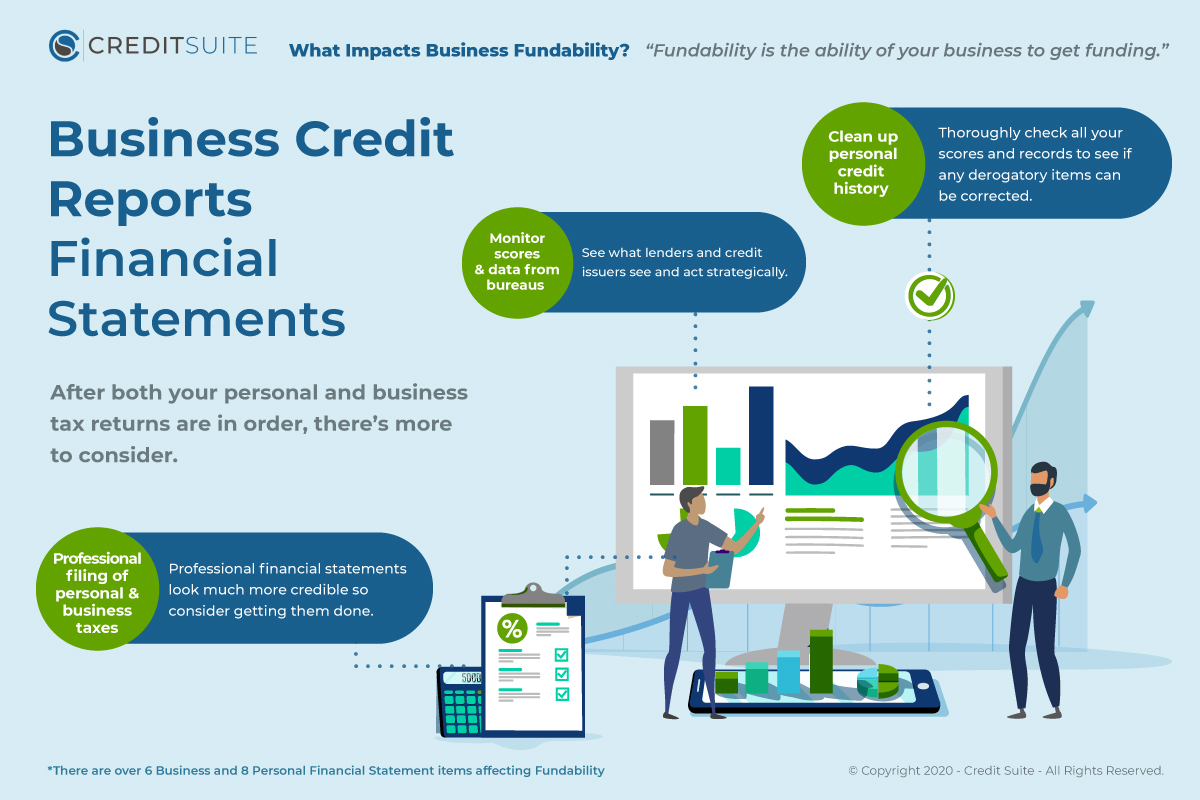

Financial Statements

Lenders are going to ask for both personal and business financials. They want to see income and profit. They need to know you have the money to pay back any financing you get. The numbers are what they are, and underwriters will verify them. Don’t try to create a false idea about money, whether personal or business. It is not worth the risk.

Bureaus

There are other agencies that hold data related to your personal money as well. Take ChexSystems for example . This agency keeps up with bad check activity. That makes a difference when it comes to your bank score, your ability to open a checking account, and definitely Fundability.

Personal Credit History

Personal credit can affect business credit. Not only do many lenders consider owner credit background alongside business credit, but some business credit reporting agencies use your personal credit score in their business credit score calculation.

Business Credit Guide: The Road Goes on Forever

You never stop building business credit. But, after a point you will want to keep your progress at a steady pace. Just don’t stop. That’s where many businesses go wrong. Business credit that isn’t growing is doing nothing. They do not understand that, the only option if you want to stay successful, is to continue to use it. Then, be sure to let it keep growing.

Business Credit Guide: Credit Suite Can Be One of Your Best Resources

Interested in business credit and want to explore more about how Credit Suite can help you? We love to share how to utilize our products to launch your own business credit journey. We want to help businesses understand what we do and how we can help them.

Check out our free business finance assessment now. We will discuss and explore where your business is currently, so we can best learn how to help you. We’ll work to understand what you need, and help you determine what your next steps should be.

The post The Fundability™ Roadmap: Your Business Credit Guide appeared first on Credit Suite.