The Los Angeles Times editorial board is arguing for a cease-fire in the Israel-Hamas war, following weeks of fighting after Hamas launched the October 7 terrorist attacks on Israel.

The editorial board claimed that it “has become impossible to distinguish between Israel’s decidedly non-surgical operation against Hamas militants in Gaza and the indiscriminate killing of Palestinian civilians.”

“It is time for a cease-fire,” the board wrote. “It is time for the Biden administration to assert strong and sustained pressure on the government of Benjamin Netanyahu to stop attacks that have reportedly already killed more than 11,000 Gazans. The world cannot stand by to witness more slaughter of civilians.”

“Remaining mindful of America’s mistakes, it is incumbent upon the Biden administration now to avoid complicity with Israel’s,” the board wrote. “We are past the time to excuse the horror in Gaza. Biden has to press Netanyahu hard to stop the mass, indiscriminate killing. That starts with a call for a cease-fire.”

The board conceded that while Hamas is a “radical militant organization” that also is in control of the Gaza government, “Hamas’ atrocities do not justify atrocities in kind.”

The board continued: “Following Hamas’ initial attack, Israel instructed the people of northern Gaza to leave their homes and made no commitment that they would ever be able to return. Israel’s reprisal destroyed homes and cut off power and communications, making it impossible for survivors of the bombing even to search for the remains of family and neighbors beneath the rubble.”

Prominent members of Congress and big-name Democratic politicians are divided on the issue of a cease-fire.

Rep. Jamaal Bowman, D-N.Y., was criticized this week for saying that by calling for a cease-fire in Gaza, he was “uplifting deeply what it actually means to be Jewish.” Rep. Alexandria Ocasio-Cortez, D-N.Y., has also led renewed calls for Biden to support a cease-fire between Israel and Hamas over the “grave violations” being committed against children in the war.

On the other side, former Secretary of State Hillary Clinton rejected calls for a cease-fire in the Israel-Hamas war on “The View” in early November, instead throwing her support behind “humanitarian pauses.”

Biden’s press office did not respond to a request for comment from Fox News Digital.

New York Times columnist Bret Stephens published an op-ed Thursday admitting he was wrong about Trump voters and expressing regret for calling them “appalling.”

Economic Uncertainty Isn’t on the Horizon—It’s Already Here

It’s an understatement to say that times are uncertain right now. Inflation, the (hopefully) winding down pandemic, current supply chain issues, and the situation in Ukraine are all creating massive global economic uncertainty. There’s even economic policy uncertainty in our government.

As a result of this kind of instability, protecting your business assets should be up there. Markets are changing rapidly, as are consumer attitudes toward spending. Succeeding just might get a bit tougher. There is always risk and uncertainty in economics. But now, it’s on steroids.

Protecting Your Business Assets During Economic Uncertainty Should be Top of Mind

Fortunately, there are ways to protect your assets. And yes, business credit and financing are the way to go. Right now is the time when good business credit and a Fundable foundation are key.

Spend Better During Times of Economic Uncertainty

While no one knows what the future will bring, one thing is for certain. Prices are going to be in flux, because economic uncertainty can influence the price of just about anything. Is it better to stock up now, expecting a price rise? Or is it better to try to wait it out and see if prices will get better?

Whichever decision you make, business credit and financing can help.

Stock Up Now with Inventory Financing

If you want to stock up now, then you might not have enough cash on hand to cover a big purchase. This is where inventory financing can come into play. It can make it possible for you to buy big today in anticipation of bigger sales tomorrow.

Inventory financing is a revolving line of credit, or a short-term loan acquired by a company so it can purchase products for sale later. The products serve as the collateral for the loan. There may be restrictions on the type of inventory you can use. This can include not allowing cannabis, alcohol, firearms, etc., or perishable goods. There can be revenue requirements. And there may also be minimum FICO score requirements.

Get approved for a line of credit for 50% of inventory value, regardless of personal credit quality.

Rates are usually 5 – 15% depending on type of inventory. You can get funding within 3 weeks or less. But note that it can’t be lumped together inventory, like office equipment.

Or Wait Out Economic Uncertainty With Merchant Cash Advances

If you want to wait, then a good use of your time can be to enhance your relationships with your preexisting customers. This can include offering better payment terms. But it can hurt your bottom line if you end up waiting for payments from your customers. Not to worry. MCAs can make it possible for you to give your customers more time to pay without harming your own bottom line.

Details on Merchant Cash Advances

An MCA technically isn’t a loan. Rather, it is a cash advance based upon the credit card sales of a business. A small business can apply for an MCA and have an advance deposited into its account fairly quickly. So you can offer Net 30 terms, but not have to wait a month to get paid.

A merchant financing program is ideal for business owners who accept credit cards and are looking for fast and easy business financing. An MCA program works to help you get funding, based strictly on your cash flow as verifiable per your business bank statements. Hence lenders in general will not have any burdensome document requests.

A lender will review three months of bank and merchant account statements. They are looking for consistent deposits. There should be deposits showing revenue is $50,000 or higher per year. A lender also verify time in business of six months or more.

Lenders also want to see that you don’t have a lot of Non-Sufficient-Funds (NSFs) showing on your bank statements. You shouldn’t have a lot of chargebacks on your merchant statements. And you should have more than ten deposits in a month going into your bank account.

In essence, a lender wants to know that you manage your bank and merchant accounts responsibly. And they want to see that have a decent number of consistent credit card transaction deposits each month.

Save More During Times of Economic Uncertainty

How can you save more money when you’ve still got to get supplies for your business? Putting everything on credit is a recipe for a future default. But what about saving when you spend? Or getting rewarded for spending?

The Wex Fleet Card and Wex Flex Card

These are great cards for business credit building because they report to Experian and D&B. Wex offers universal fleet cards, heavy truck cards, and universally accepted business fleet cards. Their cards have features supporting a small business, including a rewards program. But before applying for multiple accounts with WEX Fleet cards, only apply for two cards at a time. Then, make sure to leave at least two months between applications so that they don’t red flag your account. This will not mean an automatic decline, but it could reduce the amount of credit for which you are approved.

Apply online or over the phone. Terms are Net 15 for the Wex Fleet Card, and Net 15 or revolving for the Wex FlexCard.

To qualify for either card, you need a business entity in good standing with Secretary of State. You also need your EIN and D-U-N-S numbers. Plus you must have a business address which matches everywhere, and all necessary business licenses, if applicable. You’ll need a business bank account, and your business phone number must have a listing on 411. Apply online or over the phone, at (800) 395-0812 (then select option 3).

The Wex Fleet Card

You must be in business for at least one year, with a strong business credit history. In addition, you will have to provide your Social Security number for informational purposes. But if a pull on your personal credit concerns you, contact their Credit Department before applying. Also, they want you to have a good PAYDEX score of 80 or better.

However, if you are in business less than four years or your business credit history is too sparse for the approval to hinge on it, they will require a Personal Guarantee or a deposit of $500 to secure the card.

With this card, you will need to pay it off in full each month.

The Wex FlexCard

There is no minimum time in business requirement. However, you must provide a Personal Guarantee.

Get a rebate of up to 3 cents per gallon on gasoline. Pay no annual fee. You can carry a balance with this card, if necessary.

Brex

Another great card to help you save more as you spend is the Brex card. It is a particularly good card for startups.

Brex is a business money management system that integrates with your accounting software. It allows you to track expenses and, depending on the level of service you choose, can also help with paying bills and controlling spending.

The easiest way to use Brex for both managing finances and building business credit is to open a Brex Cash account. Brex is not a bank, but rather a banking alternative. They have a partnership with the FDIC and your funds are secure.

Everyone that opens a Brex cash account gets a corporate card. It works just like a debit card, drawing from your Brex Cash balance daily. However, unlike a debit card, Brex reports these payments to Dun & Bradstreet, Experian, and Equifax every month, thus helping build your business credit score.

Since this card is secured by the balance in your Brex cash account, and limited to that balance, you do not have to worry about underwriting.

This card offers rewards in terms of points that can be redeemed for travel, cryptocurrency, cash back, statement credits, gift cards, and more. There are even virtual card options for online spending. Brex integrates with common accounting programs including Quickbooks, Xero, NetSuite, and Gust.

Since the card is paid off monthly, you do not pay interest. There is no fee for standard service, but you can upgrade to premium at a cost. Currently premium accounts start at $49.99 and offer more expense management options. And you can even use rewards points to pay for it.

Terms

This card is paid daily from your balance of money deposited into a Brex Cash account. No minimum balance is necessary.

Brex does not offer balance transfers from other cards to Brex, due to not requiring a personal guarantee. However, they will perform balance transfers within Brex accounts.

Qualifying

To qualify for a Brex card, you need a business entity in good standing with Secretary of State. You also need your EIN and D-U-N-S numbers. Plus you must have a business address which matches everywhere, and all necessary business licenses, if applicable. You’ll need a business bank account,

In addition, you will have to provide your Social Security number on your application, for informational purposes. But if a pull on your personal credit concerns you, talk to a representative before applying.

Apply online.

Protect Your Business During Economic Uncertainty: Takeaways

While our economy is in flux, your main focus should be to maintain and grow your business’s assets. Good business credit will help your business now and, in the future, when economic uncertainty starts to diminish.

A tough-as-nails Chicago police officer sent a message to her fellow cops early Saturday, hours after being shot several times while investigating a shooting Friday night that left a young man dead and a teenager wounded, according to reports.

No doubt this is a hard time to grow a local business. Coronavirus has likely forced you to make big changes to the way you operate. It’s almost certainly hit your bottom line too.

However, it’s still absolutely possible to grow your local business at a time like this. You just have to be smart about it. In this article, I’ll talk you through how to do that. First, though, here’s a bit of detail on why this is such a challenging time for businesses like yours.

The Effects of the COVID-19 Pandemic on Local Businesses

You’re probably sick of reading and hearing the word “unprecedented.” I know I am. Unfortunately, it’s just the best word to describe the current climate for local businesses.

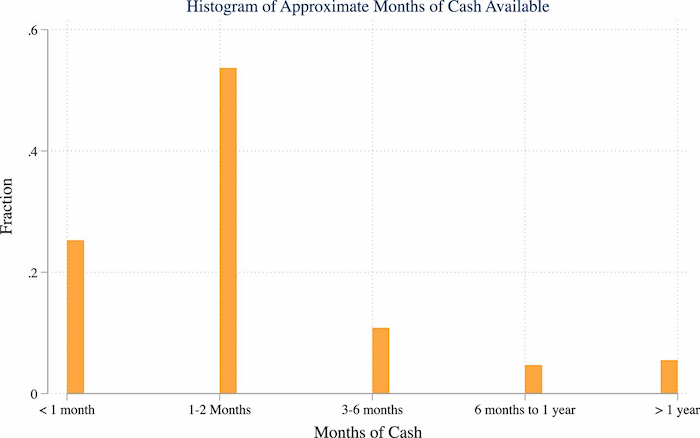

By the end of March, 32 states had locked down in response to the pandemic. Two in five small businesses across the US had temporarily closed by this point, with nearly all of those closures due to COVID-19.

Closing your doors has big financial implications. It is concerning that the vast majority of local businesses aren’t in a position to handle even short-term pressure on their earnings, with around four-fifths only having up to two months of cash available to pay their expenses.

Because of this, it’s hardly surprising that the number of active business owners in the US plummeted by 3.3 million (or 22%) in the two months from February to April alone. That’s the largest drop on record, and it affected practically every industry.

Luckily, if you have access to the right strategies (like local promotions) and tools (such as messaging services like Podium), you may still be able to grow your business even in these uncertain times.

Six Strategies to Grow Your Business During the Age of Coronavirus

The pandemic might have affected your business growth in any number of ways. Maybe you’ve been forced to shutter your store(s) for a certain amount of time. Maybe your customers are buying less at the moment. Or maybe the industry you’re in means you’ve barely even got a “product” to sell, like cinemas and travel companies.

Whatever the case, if you’re going to grow your local business in the current climate, you need to adapt. Here are tips on how to do it:

1. Use the Right Tools

I know what you’re thinking: “I’m already worried about cash flow, now this guy’s telling me to invest in a bunch of tools!” Well, what if I told you that by choosing the right tools (some of which are free, by the way), you massively increase your chances of growing your local business?

You likely know that there are thousands of tools designed to drive small business growth, but I’ve focused on the areas where you can really shift the dial:

Issue: Customer Messaging

There are so many benefits to improving your communications with existing and potential customers.

You can generate more reviews, which act as a trust factor and make your business more credible. You can collect payments faster and with less hassle. You can issue more timely (and more effective) reminders, reducing the chances of no-shows.

To solve your customer messaging you can use a tool like Podium. Here’s how I use it:

Set up one inbox to rule them all: What’s the biggest barrier to better communications? Trying to keep track of all your different platforms. Customers could be messaging you via Facebook, Twitter, phone, and your website (and maybe a bunch of others, too). Podium brings all those communications together in one place, ensuring you never miss a message.

Connect remotely with website visitors: Ever wish you could get closer to the people on your website? Find out what stops them from buying or converting there and then? With Podium, you can. Add live chat to your site and every time they ask a question, they’ll automatically move to a text conversation, so you’re no longer tied to your computer (and nor are they).

Enable on-the-go customer service: You likely don’t have a dedicated customer service team. In fact, you might be your whole customer service team. So what happens when you’re not at your desk or in the store? Stuff gets missed! Podium allows you to text quick responses when you’re out and about, so you never leave anyone hanging.

Chat face-to-face: Texting is great. But sometimes it’s just not the best way to respond to a customer or prospect. Maybe they’ve got a complex question or require a nuanced response that’s hard to tap out on your phone’s keypad. Podium offers video chat software that makes connecting remotely with customers as easy as sending a text. Send your customers a link and you can be video chatting in seconds, making it super simple to show details, answer questions, and share your screen.

Create tailored promotions: Say you own a coffee shop. You run a loyalty program and you’ve captured your best customers’ email addresses and phone numbers. Wouldn’t it be great if you could quickly send those customers targeted promotions? Maybe offer them a deal on a new single-origin coffee you’ve just started stocking? You can do that as well.

Provide to-the-minute advice and updates: There are a lot of variables in the world right now. Customers might want to know how busy you are at a certain time, or what measures you’ve put in place during the pandemic. Or they might have product-specific questions. A customer messaging platform makes it easier for you to respond in real-time.

No one likes scheduling meetings at the best of times. Throw coronavirus into the mix and it becomes even more of a challenge. Should it be in-person or remote? Which platform should we use? What date and time work best?

Meeting schedulers are designed to handle the legwork for you. One of the best is Arrangr, which reserves tentative meeting times, automatically frees up untaken slots, and can even suggest the ideal location for all parties.

Another great option is Calendly. Integrating directly with your Google or Office 365 calendar, it gives you a personalized URL that allows customers to see your availability and schedule their preferred meeting time. Best of all, there’s a basic free plan available.

Issue: Email Automation

You can’t grow a local business at a time like this without doing some marketing.

Unfortunately, you likely don’t have time to build and execute complex campaigns.

That’s why you need email automation software! One of the most popular tools, Mailchimp, helps you send effective email marketing communications at scale. In fact, Mailchimp claims to boost open rates by 93% and click rates by 174% compared to the average bulk email.

Customer Relationship Management

Your customer relationships have never been more valuable than they are right now, so you need to manage them effectively. To do that, you need to invest in a customer relationship management (CRM) tool.

There are a bunch of CRMs aimed at local businesses, but HubSpot Sales Hub is one of the most popular. It’s loaded with sales engagement tools, pricing functionality to help you deliver complex quotes, and analytics software to measure what’s working (and what isn’t).

2. Improve Your Digital Marketing Strategy

In more “normal” times, you might not put a lot of thought into your marketing. Maybe you just write the occasional social post or send a couple of email promotions a month.

During times of uncertainty, that just won’t cut it. People have a lot on their minds right now, so that one baseball gif you tweeted isn’t going to have much impact.

Let me give you an example: you sell business supplies to other local businesses.

Because you’re small and local, your big differentiator is your flexibility and bespoke approach. You can source whatever product your customer needs, your delivery times are rapid, and you’re easy to reach. That’s the sort of stuff you talk about in your marketing emails.

Well, wouldn’t it be good if you made that the foundation for a whole campaign?

Maybe you create a bunch of case studies and testimonials that show your unique selling point, (USPs), in action. You build a mailing list of local firms you’d love to do business with, and drip-feed your content to those prospects. Because you’ve built a whole strategy, you know the best times to reach those prospects, the platforms they use, and the sort of messaging that resonates with them.

That approach helps you strike up a conversation, which ultimately means you may close more deals.

3. Make Your Google My Business Profile Shine

Want people to see your name when they search on Google for businesses like yours? If you’re reading this article, I’m guessing you do, and that means you need a (good) Google My Business profile.

Setting up a free profile makes it more likely that your business shows up in relevant searches, along with useful information like:

Ensuring your information is accurate and comprehensive

Sharing business updates, like new opening hours or product launches

Asking customers for Google reviews (and responding to them)

On that last point, I know it can be hard persuading customers to review your business. They’re busy. They don’t want to spend their valuable time seeking out your Google My Business profile or Facebook Business Page.

Podium makes it a lot easier, helping you provide social proof that demonstrates your brand can be trusted. Text customers asking them for a review and they’ll be linked straight to your Facebook, Google, and Tripadvisor pages, so there’s hardly any clicks (and hardly any work) for them. That’s why Podium has powered more than 15 million business reviews for its users.

4. Create and Execute a Local Paid Marketing Strategy

Sometimes it takes money to make money. If you’re serious about growing your local business right now, you’ll want to consider investing in some sort of paid activity.

Google Ads can be super effective for smaller firms, especially web-based businesses targeting online traffic and/or conversions. Local keyword phrases like “lawyers near me,” or “realtor in Denver,” are typically a lot less competitive than broader, non-geographic terms like “realtor.” That means you could get a lot of visibility and clicks with a relatively small outlay.

In addition to Google Ads, consider advertising on social platforms like Facebook and LinkedIn. Social ads are less intention-based than paid search because your audience isn’t actively looking for the thing you’re advertising.

However, ads on social media often cost less than Google Ads. For instance, if you’re a law firm, you’re paying on average $10.96 per click on Google Ads, but on Facebook, that figure drops to just $1.32.

5. Use Analytics to Track and Improve Site Performance

When times are hard, you need to squeeze every last dollar from your potential customers. Analytics software (like Google Analytics) can help you do that by allowing you to identify trends, plan new strategies, and measure the results of your current efforts.

Let’s say you’re a mechanic. You’ve just added a page to your site to promote a special offer on new tires. A month later, you click into Google Analytics and see that a bunch of people have landed on that page, but your conversion rate is low.

You compare it to other, similar pages on your site. They’re performing much better. Now you know there’s a problem, such as:

Your current offer is priced too high

Your new page isn’t engaging or persuasive enough

You don’t make it easy enough for customers to convert, so they leave

You don’t provide enough detail about the offer

By comparing against better-performing pages, you can tweak your approach and improve results.

6. Conduct Local Community Promotions

Now isn’t a good time to invite hundreds of people to a big party. But there are definitely opportunities for community engagement. You just need to get a little creative.

Say you’ve opened a new store in a location you haven’t served before. Maybe you target properties within a certain zip code, or on certain streets, with a special offer that encourages customers to visit your store.

Perhaps in the age of social distancing, you’ve introduced a new takeout service. Why not give customers in your area 10% off their first promotion, or combine it with a loyalty scheme? Tailor your offer to what your customers want right now, then promote it on Facebook, in the local press, via email marketing, or through direct mail.

7. Optimize Your Social Media Accounts

There are dozens of social platforms out there, but when it comes to growing a local business, you want to focus on those that give you the best reach, like:

Facebook

Twitter

Instagram

LinkedIn

Pinterest

YouTube

Tumblr

Finding the right platform will depend on the type of business you run. On a basic level, if you’re B2B, LinkedIn’s likely your best channel. Otherwise, almost everyone is on Facebook, but if your product is highly visual you might see more success on Instagram, Pinterest, or YouTube.

Whichever platform(s) you choose, you need to identify some tactics that ultimately help you sell more, like:

Showcasing and/or auctioning your products on Facebook Live

Starting conversations with new prospects in LinkedIn Groups

Setting up Instagram Shopping so people can browse your products in photos and videos while in-app

Conclusion

Growing a local business is never easy, and it’s certainly a whole lot harder right now.

However, if you’ve set up your own business, you’re likely comfortable with hustling for results. You’re naturally entrepreneurial and you’re driven to make this work.

Combine that attitude with the right growth strategies, and execute them effectively, and there’s no reason why you can’t come out of the pandemic in a stronger position.

What plans have you put in place to grow your business? How’s it going for you so far?

No doubt this is a hard time to grow a local business. Coronavirus has likely forced you to make big changes to the way you operate. It’s almost certainly hit your bottom line too. However, it’s still absolutely possible to grow your local business at a time like this. You just have to be smart … Continue reading How to Grow Your Local Business During Uncertain Times

No one realized when the year started that a crushing recession would follow a global pandemic. And yet, here we are living in this post COVID-19 world. Here’s how a good D&B business credit file can help you survive.

Everything you Need to Know about Your D&B Business Credit File and the Other Business Credit Reporting Agencies

When it comes to your business, business credit is one of the most important things you can focus on. Of course, you should keep your main focus on actually running the business. In hard times however, like during a recession, you will be glad you paid some attention to your business credit. Dun and Bradstreet is the largest and most widely used business credit reporting agency, or CRA. If you do not have a D&B business credit file, many lenders consider you to not have credit. There are other CRAs that are worth mentioning however.

It can help to understand a little more about business credit and how it can help in a recession. What makes it so special? Who needs it? How do you get it?

Why Business Credit?

There are a number of reasons why it is important to actively build business credit.

It Shields Your Personal Credit Report

It is important to organization success that you develop business credit. Without a business credit score, your capability to fund your business rests entirely on your individual credit score. That’s not a big deal if you have great personal credit.

However, business financing can impact your personal credit scores as well. If you finance your business on the merits of your personal credit, you will likely find your balances stay near your limits. On personal cards the limits are not as high as most business cards allow.

Discover our business credit and finance guide, jam-packed with new ways to finance your business without emptying your wallet. Save your money during the recession!

This has a negative effect on your credit report. It is true even if you are making your payments on time. If your business has its very own credit report, it’s not a problem. Limits are higher, so you have a lot more credit to deal with. Regardless, it doesn’t impact your personal credit score.

When you have solid business credit, you have access to the funds you need to run your business. Not only that, but you can do what you need to do without worrying about exhausting cash reserves.

In short, business credit opens the door to higher limits, lower interest rates, and it protects your business transactions from affecting your personal credit. This is especially important during a recession. Imagine how much harder hard times would be if your personal credit was declining due to business issues.

Business Credit vs. Personal Credit

It is also difficult to see how a D&B Business credit file, or any business credit file, is necessary if you do not understand the differences between business credit and personal credit. We break it down here.

Key Differences Between Personal Credit Reports and Business Credit Reports:

Personal FICO scores range from 300 to 850

Business credit scores usually range from 0 to 100.

FICO algorithms are commonly used by consumer credit bureaus to generate a credit score.

Business credit scores do not follow industry standard algorithms, meaning they can vary greatly between credit reporting agencies.

Business credit usually include only accounts that are in your company’s name. Your personal accounts are on your personal credit report.

You can get a free copy of your personal credit report from the three major consumer credit reporting agencies each year. This includes Experian, Equifax, and TransUnion. There are also several free options for getting a glimpse at your credit scores at any given time.

Business credit is quite different when it comes to accessibility. You have to pay to see your company’s credit report and to find out the score at all three major business credit reporting agencies, including Dun and Bradstreet, Experian, and Equifax.

Not just anyone can see your personal credit report, but business credit reports are public. Anyone that wants to pay can see your business credit, including your D&B business credit file.

What Makes the D&B Business Credit File So Special?

Besides being the largest and most commonly uses, they offer way more than just a single business credit score. There are many reporting options that lenders can choose from to assess the credit worthiness of a specific business. Here is a breakdown of what they offer, with an explanation of what it all means.

Credit Reporting at Dun and Bradstreet: What Does Dun and Bradstreet Do?

The quick answer is they provide lenders with business credit reports to help them make lending decisions.

There are six different Dun and Bradstreet reporting options. All of them measure different areas of credit worthiness. The most popular option is also the easiest to understand. It is the PAYDEX. Generally speaking, this is the Dun and Bradstreet credit score most like the consumer FICO score. It measures the speed of payment. The score ranges from 1 to 100. A 70 or higher is “good.” For example, a score of 100 means that the company makes payments in advance, and a score of 1 indicates that they pay 120 days late, or more.

What Else Does a D&B Business Credit File Include?

In addition to the PAYDEX, there are many other options for a business credit report on you D&B business credit file.

● Dun and BradstreetDelinquency Predictor Score

The delinquency predictor score measures the likelihood the company will not pay, will be late paying, or will fall into bankruptcy. The scale is 1 to 5, and a 2 is good.

● Financial Stress Score

The financial stress score is a measurement of the pressure on a company’s balance sheet. It indicates the likelihood of a shutdown within a year. It measures with a minimum of 5 and a maximum of 1, with a score of 2 being a good thing.

Supplier Evaluation Risk Rating

This is a rating that ranks the odds of a company surviving 12 months. The minimum score is 9 and the maximum is 1. A score of 5 is good.

Credit Limit Recommendation

The credit limit recommendation shows a business’s borrowing capacity. It is a dollar amount recommendation for how much debt a company can handle. Typically creditors use it to determine how much credit to extend.

D&B Credit Rating

This is an estimation of overall business risk on a scale of 4 to 1. A two is good. The rating includes letters, the combination of which indicate a company’s net worth.

Even if there isn’t enough information on a business to assign a regular rating, Dun and Bradstreet will assign what they call a Credit Appraisal Score. This is based on number of employees. Another option is an alternative rating based on what data is actually available.

What Goes into a Credit Rating on Your D&B Business Credit File?

The different scores and ratings are based on information from a number of places. The first is the business itself, but they also tap into public records. A business must submit a financial statement to D&B before they can have a full rating. In the absence of that, they give a limited rating based on number of employees. For example, the rating would be 1R if the business has 10 employees or more, and 2R if they have less than 2 employees.

A composite credit appraisal may also be available in the absence of a financial statement in your D&B business credit file. A business is only eligible for a rating up to a 2 in this case however. You do not get a 1 rating without a financial statement.

You can also self-report trade references to D&B, in addition to financial statement. This makes it easier to build business credit faster. You will need a D-U-N-S number, of course. It is free and easy to get on their website.

Discover our business credit and finance guide, jam-packed with new ways to finance your business without emptying your wallet. Save your money during the recession!

Dun and Bradstreet and the Commercial Credit Score

The commercial credit score is the term used to describe the actual business credit score. It has three separate parts. Each predicts how likely the business is to default on bills or become delinquent. Following are the three parts and the scales by which they are ranked.

● Commercial credit score

Measured on a scale of 101 to 670, it predicts the probability of a company becoming delinquent. A score of 101 is most probable, so that’s bad. A score of around 500 is good.

● Commercial credit percentile

This is measured on a scale of 0 to 100. It measures the probability of delinquency as well, but against other companies in the Dun and Bradstreet system. A score of 1 is the highest probability compared to other businesses in the system, and most say a score of 80 is good.

● Commercial credit class

This is a method of dividing businesses into classes based on the probability of delinquency. Companies in class 1 are the least likely to be delinquent. If you are in class 2, that’s good.

Who Are the Other CRAs?

You hear so much about Dun and Bradstreet, it is easy to forget that there are other agencies that offer business credit reports.

Equifax

They collect their information in ways similar Dun and Bradstreet, including: information from public records, financial data from the business, and payment history from creditors. In addition, they factor information about credit utilization, or how much credit a business is currently using versus how much they have available, into their calculation.

They then use the information collected to generate various scores, similar to those on your D&B business credit file, but not the same. These scores include the business credit risk score and the business failure score. The business credit risk score measures how likely it is that a business will become 90 days or more delinquent on bills over the next 12 months. It ranges from 101 to 992. The business failure score ranges from 1,000 to 1610, and it predicts how likely it is that the business will file for bankruptcy over the next year. The lower the score, the higher the risk.

Another score they offer is the business payment index. This is their version of the D&B PAYDEX, and it even runs on the same scale, 0 to 100. It indicates payment history over the past year. Different from the PAYDEX however, you have to reach a score of 90 or higher for it to be a “good” score.

Equifax also offers business identity reports that serve as confirmation that a company actually exists. It also verifies details such as the company’s tax ID, number of employees, and yearly sales.

Equifax does not allow business owners to request a report on their company. They decide themselves when to start a credit file on a specific company.

Experian

Your Experian report could be a lot different than the one from your D&B business credit file. Their credit ranking, Intelliscore, uses more than 800 variables to predict a company’s risk of defaulting or becoming delinquent. A 76 or higher is considered good with Intelliscore. That indicates a low risk of late payments or default. A score from 51 to 75 indicates a low to medium risk and 26 to 50 indicates medium risk. From 25 down 1 is medium high to high risk.

Intelliscore is considered a blended score of both the business and business owner’s information. It offers insights into a business’s public record findings, collections, payment trends, and overall business background. A major difference between Experian and the other two characters is that they do not ask businesses to self-report at all. Rather, they collect all the information themselves. Since it includes personal information, you do have to give permission for a lender to view this report.

Specifically, the Experian credit ranking gives insights into a company’s payment trends, public record filings, collections, and general business background. The result is a blended score calculated using both the business and business owner’s information.

Discover our business credit and finance guide, jam-packed with new ways to finance your business without emptying your wallet. Save your money during the recession!

The Experian Database and Credit Report Generation

Experian’s database has information on over 27 million businesses. Reports are generated with information from the database, which houses information on bankruptcy filings, payment history, collections, banking, insurance, and leases.

There has to be a minimum amount of information in the database about a business before Experian will generate a score for it. There must be at least one tradeline in the system, so you should definitely do business with a company that will report to Experian if you want to build business credit.

Your D&B Business Credit File and Those from Experian and Equifax Can Make All the Difference During a Recession

You can’t know or choose which one your lender will use to base their decision upon. That means it is important to build strong business credit with each one. While a lot of this is out of your control, you can choose which starter vendors you work with. Since not all starter vendors report to all credit reporting agencies, you need to make sure you do business with a variety that report to each one. Then you can be on your way to building strong business credit.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

foundation are key.

foundation are key.