Business credit is credit you get in the name of a business. It does not attach to the business owner’s SSN. It is not dependent on the entrepreneur’s ability to pay debts. But it does depend on whether the business can pay its bills. Better business credit means your business can get more funding when it needs it, at better rates and terms than if you don’t work to build your business credit. Here are 3 ways to build business credit.

Business Credit is Not Automatic

You have to actively work to build it. Did you know over 9 out of every 10 vendors do not report to the business credit reporting agencies, Dun & Bradstreet, Experian, and Equifax? Therefore, except for requesting a trade reference, those nonreporting vendors don’t help you build business credit. So, what do you do? The following actions will help you no matter which method you use to build your company’s business credit.

Check Out Ways to Build Business Credit

Improving business credit scores means paying your bills on time. It also means paying with credit rather than cash when you can. This increases the number of accounts and purchases on your reports. And use the credit you already have regularly, so those accounts are not eventually closed due to inactivity.

A business starts building a brand-new credit profile much the same as a consumer does. Both start with no credit profile. The business gets approval for new credit reporting to the business credit reporting agencies. The business uses the credit and pays the bill timely. This establishes a positive business credit profile. As the business continues using credit and pays bills timely it will qualify for more credit.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

The First of 3 Ways to Build Business Credit: Vendor Accounts

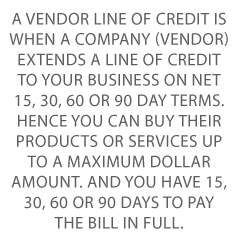

One of the three ways to build business credit is with starter vendor accounts. These are companies which will approve your business with little fuss. A vendor line of credit is when a company (vendor) extends a line of credit to your business on Net 15, 30, 60 or 90 day terms. Hence you can buy their products or services up to a maximum dollar amount. And you have 15, 30, 60 or 90 days to pay the bill in full.

Since vendor accounts generally don’t ultimately come from a bank, like major credit cards (Visa, etc.) do, you can try to apply without using your Social Security number. Always apply first without using your SSN. Some vendors will request it and some will even tell you on the phone they must have it. But try to submit first without it.

Starter Vendors and D&B

When your first Net 30 account reports your tradeline to Dun & Bradstreet, the D-U-N-S system will automatically activate your file if it isn’t active already. This is also true for Experian and Equifax. Applying without your SSN means the vendor won’t pull your personal credit. As a result, you will be building business credit and not personal credit!

You need at least 3 vendor accounts reporting to move on. It can take a billing cycle to get your payment to show up in D&B’s system. Some vendors may want you to prepay or may have a minimal order requirement before they reporting to a business CRA. They may have minimal FICO score requirements as well. But you can often get around a minimum FICO requirement by working with a guarantor with good personal credit.

One of the Ways to Build Business Credit is to Go Beyond Starter Vendor Accounts

As you continue to prove yourself and your business, it becomes possible to qualify for revolving store credit. You can also qualify for fleet credit to buy fuel or repair and maintain vehicles. And you can even qualify for more universal cash credit from Visa and MasterCard and the like. So don’t stop with starter vendor accounts!

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

The Second of 3 Ways to Build Business Credit: Our Credit Line Hybrid

You can get a line of credit for up to $150,000. This is no doc financing. Pay 0% for up to 18 months. It helps build business credit because your payments are reported. You must have a 680 or better FICO score. For more information, surf on over to my.creditsuite.com/qualifier-form.

This program works to help clients get funding based strictly on personal credit quality. Our lenders will not ask for financials, bank statements, business plans, resumes, or any of the other burdensome document requests which most conventional lenders demand.

Our lenders will review your credit report to ensure there are no derogatory items on it. To get approval, you shouldn’t have any open collections, late payments, tax liens, judgments, or the like on your report.

To qualify you should also have fewer than 5 inquiries on your credit report, within the last 6 months. You should have established credit. This includes open revolving accounts now reported on your credit report, with balances below 40% of your limits.

The Third of 3 Ways to Build Business Credit: Using the D&BCreditBuilder

Dun & Bradstreet has their own credit builder. It can help you get better business credit, but only with D&B. Dun & Bradstreet is huge, so concentrating just on them could be an effective strategy.

D&B offers advice for building business credit. A lot of it should be familiar. Their seven steps are to establish your business as a separate entity, register for a D-U-N-S number, get an EIN from the IRS, open a bank account for your business, make on-time payments, ask vendors to supply trade references to Dun & Bradstreet, and monitor your business credit scores and ratings.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

D&B’s CreditBuilder Plus

CreditBuilder Plus is essentially a monitoring service exclusive to Dun & Bradstreet. One major advantage is getting a D-U-N-S number faster than most businesses do. You can use it to get alerts when others request your business credit report. And you can get a D-U-N-S Number and business credit file in 5 business days or less.

Plus you can get unlimited access to your D&B scores and ratings. And you can add 12 positive payment experiences to your business credit file and monitor your CreditBuilder account email address to know if it may have been compromised online.

3 Ways to Build Your Business Credit: Takeaways

Getting starter business credit means your business has more chances to get funding, and at the best terms and rates. Building business credit in any manner starts with fundability. Set up your business credibly to satisfy lender requirements. Working with starter vendors is a great way to get going. Starter vendors will approve you for lines of credit with little fuss.

Our credit line hybrid is the most excellent of these three ways to build business credit. Your payments are reported, and you won’t have to provide extensive documentation. Using the D&B CreditBuilder is another fine way to build your first business credit. One massive advantage to CreditBuilder is getting a D-U-N-S faster than other businesses.

But no matter which method(s) you choose, let’s take the next step together.

You may have heard the term small business inventory loans. But do you really know what it is all about? We break it all down for you right here. This form of funding just might be perfect for your business. It’s also called inventoryfinancing.

According to a definition from Investopedia – “Inventory financing is a revolving line of credit or a short-term loan that is acquired by a company so it can purchase products for sale later. The products serve as the collateral for the loan.” See investopedia.com/terms/i/inventory-financing.asp.

You can get a low rate credit line. And all you need to do is use your current inventory as collateral. Inventory is valuable! It is perfect for collateral for small business inventory loans.

Check out these Credit Line Details

Keep in mind that your inventory must be worth $500,000 or higher. You can get approval for a line with low rates, regardless of your personal credit quality.

You can get approval for a line of credit for 50% of inventory value. Rates are usually 5 – 15% depending on type of inventory. And you can get funding within 3 weeks or less. It can’t be lumped together inventory, like office equipment.

With inventory financing, there may be restrictions on the type of inventory you can use. This can include not allowing cannabis, alcohol, firearms, etc., or perishable goods. And there can be revenue requirements. There may also be minimum FICO score requirements.

Let’s look at Qualifying for Small Business Inventory Loans

You will not need financials, or good personal credit. Your business must have existing inventory now that is valued over $500,000. Lender will also check the quality of your inventory management system.

The inventory might be of supplies, retail merchandise. materials used to produce your product, or other non-obsolete inventory. The lender will review your existing inventory. If you have inventory that qualifies you can get approval quickly with just a review of your inventory records.

You Can Get Fast Funding with Inventory Financing

After the lenders review your inventory summaries, you can get your initial approval and funding in 3 weeks or less. And you can get a working capital credit line to use for whatever purposes you need.

But What if You Have Credit Issues?

This program is perfect for business owners with credit issues. Lenders are not looking for, nor do they require good credit to qualify. You can even get approval for a credit line with low rates, even with severely challenged personal credit and low credit scores.

You can get approval regardless of personal credit quality. So this is even if you have recent derogatory items and major collections on your credit report. This is one of the best and easiest business financing programs in existence that you can qualify for. And you can get really good terms even with severe personal credit problems.

Get 24 hour preapproval and get secure financing of 50% of your inventory value. It is just an easy inventory review for approval. And you will pay no application fees.

You can get approval even with poor credit. Go from application to funding in 3 weeks or less. You can get approval with no revenue requirements. This is low rate financing. Enjoy credit line amounts range up to $500,000.

What are the Approval Amounts?

You can get up to $500,000, and bad credit is accepted. Your inventory serves as your collateral. No financials are necessary.

Let’s Look at Qualifying for Inventory Financing from Credit Suite

You will need over $300,000 in inventory. So, this means no jewelry, apparel, highly seasonal items, or high tech items subject to rapid obsolescence.

What do the Approval Amounts Depend on?

You can get approval for $150,000 or more. The approval amount is based on the actual value of the inventory. You can get approval for financing up to 50%.

What are the Interest Rates?

Interest is very low. It is typically as low as 2% monthly. And you can get approval in 3 weeks or less.

What if Small Business Inventory Loans are Impossible to Get Now?

There are other ways to get financing for your business. Your business – and you – have assets beyond inventory. And you can tap these assets as collateral. You can use a 401(k) or IRA, accounts receivable, or stocks or bonds. Did you know that the 401(k), stocks, or bonds do not even have to be yours? You can work with a partner with these kinds of assets.

Check out Securities-Based Financing

So you can use existing stocks as leverage to get business financing. Borrow as much as 90% of their value. You continue to earn interest on the stocks pledged as collateral. And closing and funding takes less than 3 weeks.

Take a Look at 401(k) Financing

You can use your existing 401(k) or IRA as collateral for business financing. This program uses IRS proven strategies, called ROBS. And you will pay no tax penalties.

You still earn interest on your 401(k). Pay low rates, often less than 5%. And you can close and fund in less than 3 weeks. You can usually get up to 100% of what is “rollable” within your 401(k).

Note: your 401(k) has to be with a company that is no longer employing you.

You can use your outstanding account receivables for financing. In this instance, you can get as much as 80% of receivables advanced ongoing in less than 24 hours. The remainder of the accounts receivable are released as soon as the invoice is paid in full. And closing takes 2 weeks or less. Pay factor rates as low as 1.33%. These are accounts receivable credit line with rates of less than 1% with no consumer credit requirement.

The receivables should be with the government or another business. If you also have purchase orders, you can get financing to have those filled. And you will not need to use your cash flow in order to do so.

Check Out what OnDeck has to Offer

OnDeck offers inventory loans and business lines of credit. Term loans run $5,000 to $250,000, with 12-month terms, paid back daily or weekly.

Their lines of credit run from $6,000 to $100,000. Pay back over 12 months, with automatic weekly payments. Find them online at ondeck.com/loantype-inventory-loans.

Or how about an Amazon Corporate Credit Line?

Do you have an online business? Then you can get a revolving credit line from Amazon. Make minimum payments or pay in full monthly. Pay 12.99% purchase APR (minimum interest charge is $1). You get an option to apply as a personal guarantor to build business credit. And you will enjoy 24/7 Customer Service.

Consider Amazon Lines of Credit and Working Capital Loans

If your business is eligible, you will see funding options when you log into Seller Central. Currently, lines of credit are offered by Marcus by Goldman Sachs. Loans come from Amazon Lending – specific terms are tailored to the business. Get access to loan funds within 5 days. Learn more at sell.amazon.com/programs/amazon-lending.html.

Your inventory is a valuable business asset. You can leverage it to get business funding. Get approval with excellent terms, even if your personal credit is not so hot. And consider alternatives like 401(k) financing or OnDeck and more if you can’t get small business inventory loans right now.

Business Grants for Minority Women and So Much More

Are you a minority woman in business? Or are you starting a business? Money is always going to be an issue. What if you could get what is essentially free money? That’s what grants are – for the most part. So it would behoove you to look into business grants for minority women.

Business Grants for Minority Women and More Funding for Minority Businesswomen

How do you find the best options for you? How do you know if you need to be looking for grants or business loans for minority women? We recommend that you explore every option. This is because it will probably take a combination of funding options to fully fund your business.

There are business loans for minority women. But they’re often not for them exclusively. But there are other funding choices out there. Loans, crowdfunding, and even angel investors are all viable options. More on those later.

Business Grants for Minority Women

The government and private organizations want to GIVE you money! They’re highly competitive and rarely enough to fund a business on their own. Still, grants are a great way to supplement other business funding. And they are still worth the effort to apply. There really isn’t anything to lose except time – it’s free money. Here are a few you can start with.

Amber Grant

The Amber Grant awards one prize of $10,000 per month to a woman-owned business. One of the recipients also receives an additional $25,000 grant at the end of the year. Applicants only need to tell their story and turn it in with a $15 application fee. See ambergrantsforwomen.com/get-an-amber-grant/apply-now.

Cartier Women’s Initiative Award

This award is for women but there’s no specification that a woman be a member of a minority group. The Cartier Women’s Initiative Award has a regional category award and a science and technology award. The regional award is $100,000 for first place, and $30,000 for second and third place.

The award goes to three women from each of seven international regions. This award is a grant to 21 female business owners from around the world each year. Women business owners who are just getting started may qualify. Look over the complete application for more information. See cartierwomensinitiative.com/about-us.

The Cartier Science and Technology Pioneer Award

The Cartier Science and Technology Pioneer award is new as of 2021. With this award, three more women impact entrepreneurs at the forefront of scientific and technological innovation will get recognition. Open to women entrepreneurs from any country and sector. This award will highlight disruptive solutions built around unique, protected, or hard-to-reproduce technological or scientific advances. The laureate will get a $100,000 grant. Each of the two remaining finalists will get a $30,000 grant.

Cartier Fellowships

Cartier also offers a fellowship program. The fellowship is an educational program geared towards the 24 fellows selected each year. The fellowship program aims to equip the fellows with necessary skills to grow their business. And it helps them to build their leadership capacity. It does so by drawing upon the experience and expertise of many academics, practitioners, industry experts, and entrepreneurs.

The fellowship isn’t exactly a grant. But while it’s not a monetary award, the mentoring and networking opportunities could be worthwhile to apply for. See cartierwomensinitiative.com/fellowship-programme.

National Black MBA Association Scale-Up Pitch Challenge

Also known as NBMBAA, the Scale-Up Pitch Challenge has cash prizes from $1,000 to $50,000. The association’s purpose is to help newer businesses with African American ownership. This is a pitch competition for startup businesses. See nbmbaa.org/scale-up-pitch-challenge.

The Minority Business Development Agency

The US Department of Commerce runs the Minority Business Development Agency (MBDA). It works to help minority-owned businesses get the resources they need to grow and succeed. The MBDA is not just for women. Grant competitions are regularly changing.

Visit the MBDA’s website for info on all current opportunities. Currently, the MBDA helps its members apply for grants via Grants.gov. This involves help with how to apply for government grants. See mbda.gov/grants.

The MBDA oversees the Enterprising Women of Color (EWOC) Initiative. The initiative focuses on the fast-expanding minority women entrepreneur population as a revenue generators for families, communities, and the nation. Minority women are the fastest growing population of entrepreneurs. While many women are making tremendous strides in the business world, they still face obstacles as entrepreneurs

MBDA is an advocate for women’s economic empowerment. They support efforts to advance women’s equality and promote women economic advancement programming. The vision of EWOC is to ensure women worldwide reach their economic potential. See mbda.gov.

Business Grants for Minority Women – Native Americans

First Nations Development Institute Grants

The mission of this group is to offer grants that help Alaska Natives, Native Hawaiians, and Native Americans. These grants are for any gender. So you would be competing against Native Hawaiian, Alaskan, and Native American men. They help in the application process in addition to funds.

First Nations also helps point individuals to appropriate grants offered by other organizations, including the US government. This includes help with writing grant proposals. See firstnations.org/grantmaking.

The Native American Business Development Institute (NABDI) Grant

The NABDI Grant is funded by the US Department of the Interior’s Bureau of Indian Affairs. It is not just for women. It provides funding to business owners of Native American or Alaskan Native descent. In 2019, the program provided more than $727,000 to 21 indigenous tribes. So this was to support economic feasibility studies for specific economic development projects or business startups.

For 2020, NABDI planned to award 20-25 grants. There is no minimum or maximum amount of funding you can request. But most awards range $25,000 to $75,000. They only fund projects for one year at a time, which is when they expect projects to be completed. To apply for a NABDI grant for your proposed economic development feasibility study, go to bia.gov/service/grants/tedc/apply-nabdi-grant.

Indian Affairs

There is more available via the Bureau of Indian Affairs. Businesses owned by Native Americans can get financing from the federal government through the Indian Affairs branch. These are not just for women. An individual can fill out an application for up to $500,000. But business entities and tribal enterprises may apply for more.

Potential borrowers can apply with any lending institution, they just have to use the application for Indian Affairs. Additional requirements are in place if the funds are used for construction, renovation, or refinancing. In general, you must supply a list of collateral, a credit report, and an analysis of business operations. See bia.gov/as-ia/ieed/loan-guaranty-insurance-and-interest-subsidy-program

Business Grants for Minority Women – Asian Woman

The South Asian Arts Resiliency Fund

If your business is in the arts, and you’re of South Asian descent, then check out this fund. The fund is operated by the India Center Foundation. It is designed to support US-based South Asian arts workers impacted by the COVID-19 pandemic

The fund will disburse grants up to $2,000, depending on financial need to US-based arts workers of South Asian descent. This includes those in the performing arts, film, visual arts, and literature. It’s for people with heritage from Afghanistan, Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan, and Sri Lanka. Initial funding for the program is $20,000. But the India Center Foundation is soliciting donations to expand the grant program.

Applicants must be of South Asian descent, work in the arts and demonstrate loss of income due to COVID-19. Additionally, applicants must be at least 21 years old. You can’t be enrolled in a degree program. Plus they must be able to receive taxable income in the US. Grant funding can go toward any artistic project you can develop, create, and present within 4-6 weeks of getting funding. See theindiacenter.us/artsfund.

Business Grants for Minority Women – Grants for All

Grants.gov

The federal government gives out grants to all genders and all races. Grants.gov is a running list of over 1,000 available government grants. So this includes minority business grants. The website compiles grants from more than two dozen government agencies. These are agencies like the SBA, USDA, and the US Department of Commerce. To find grants right for your business, use the Search Grants tool on the site. Sort the list of grants by keyword or opportunity number.

Once you have located the grant you wish to apply for, click the hyperlinked opportunity number for more detail. There, you will find more information about the specific grant as well as any associated documentation you might need. To apply for a grant through Grants.gov, you must first register. Then, you will be able to download an application package for the grant you want. Be ready for a lengthy process. See grants.gov.

More Types of Funding

Crowdfunding

If you’d rather not rely on grants so much to start and run your business, crowdfunding is a viable option. Still, not everyone with a campaign on a crowdfunding site is successful. This is because more unique products and services tend to do better. Kickstarter and Indiegogo are two of the most popular crowdfunding platforms to use. Some platforms may have higher success rates for women than others.

Angel Investors

Angel investors are informal investors. So essentially, you are selling a part of your business to them. They tend to not want a huge percentage of your business. And they won’t pass by more conventional businesses, like with crowdfunding and venture capital. Hence they can be another supplement or replacement for grants.

Business Center for New Americans

If grants aren’t an option, loans might work. So if you’re an immigrant, try the Business Center for New Americans. They offer a pilot program for microloans up to $75,000. They work with immigrants, refugees, women, and other minority entrepreneurs. The goal is to help minority business owners who have not been able to get traditional financing. Terms are 3% interest. Loan repayment term goes up to a year. See accompanycapital.org.

Business Grants for Minority Women: Takeaways

So there are several options for grants for minorities and for women. Minority women should apply for grants they feel they are most likely to get. Other options for funding include crowdfunding, angel investors, and loans. Credit Suite can help you get the funding you need.

While on the surface it may seem that business borrowing from family and friends is a simple solution to a hard problem, there is actually a lot more to it. It can be tricky, and many unforeseen issues can arise.

Make Business Borrowing From Family and Friends Work for You

There are some outside-of-the -box methods however, that allow for business borrowing from family and friends without all the drama. These options are much better than borrowing directly from loved ones. Of course, mixing business and family or friends will probably never be drama free, but these tips can make it a lot easier.

Business Borrowing from Family and Friends: Angel Investors

This option does include getting funding directly from friends or family. However, it works differently than a loan. Angels tend to be a lot more informal than most types of funding. They can be people you know. They can also be people you connect with through networking or other means. Your mom, dad, brother, sister, aunt, uncle, best friend, cousin, pretty much anyone can be an angle investor!

Angels are not covered by the Securities Exchange Commission’s (SEC) standards for accredited investors. But a lot of them are accredited investors anyway.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

To become an accredited investor, a person has to have a minimal net worth of $1 million, and an annual income of $200,000.

But, they don’t have to be millionaires. They could be friends or colleagues sitting on home equity, or local professionals who are looking to invest. Consider people you know well and people you don’t know so well. Angel investors could be people you grew up with or have done business with.

Even if you do not use friends or family as investors, finding an angel investor could convince those closest to you to help in another way.

Business Borrowing from Family and Friends: Crowdfunding

Here’s how crowdfunding works. You market your business on a crowdfunding platform, and anyone who wants to can invest in the company. Some platforms will even accept donations as low as $5 or $10 dollars, though most do require more. With rewards-based crowdfunding, you get some token of thanks for your donation. With equity-based crowdfunding, which almost always requires $500 or more, investors get an interest in the company.

This is not a sure thing. While there are a lot of successful crowdfunding campaigns, the majority are not able to fully fund their business through crowdfunding. According to Startups.com, the average success rate of a campaign is 50%, and 78% of crowdfunding campaigns reach their goal. It’s a good way to give friends and family a chance to help fund your business without them having to give a large sum of cash at one time.

Business Borrowing from Family and Friends: Kiva

Kiva is an online lender that is a little different. For example, the interest rate is 0%. That means even though you have to pay it back, it is absolutely free money. They don’t even check your credit. However, there is one catch. You have to get at least 5 family members or friends to give to your business. In addition, you have to pitch in a $25 loan to another business on the platform. This is another way those you love can help you fund your business without giving up a pile of cash all at once.

Business Borrowing from Family and Friends: Guarantor Loans

A guarantor loan is a loan that you get, but someone else signs on to guarantee that they will repay if you default. It could be a business partner, a friend, or even a family member. This is sometimes a better option for having a family member help with funding than getting funds from them directly. Still, the same caveats exist when a guarantor is using their credit to help you out. If your business fails, or you default on the loan, then your guarantor will bear the brunt of that – and they will, most likely, come after you to make up for any losses they incur.

If you have friends or family that qualify as a guarantor, they may be more willing to go this route. They can let you piggyback off their good credit without giving up any cash initially. Hopefully, they never will.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

Credit Line Hybrid

This is a type of loan that you can use a guarantor to get. The credit line hybrid may be for you if you have a credit score over 680 or have friends or family that do and are willing to cosign. You can usually get a loan of 5x the amount of your highest revolving credit limit account, up to $150,000. Honestly, this is more than what you could get on your own when applying for credit cards. Furthermore, you can get cash out on this program.

Also, there is no impact on your personal credit with this type of financing. It will not even affect a guarantor’s personal credit. A lot of business owners use the good credit of friends or family to help them get the funding they need. All payments report to the business credit profile, so you can build business credit at the same time.

Build Your Business Credit Score and Pay it Forward

Once you get the funding you need, work on building your business credit score. There are a few things you need to do to make this happen. However, once it’s done, you will have access to the funding you need, and you could be in a better position to help others rather than asking for help.

First Steps

The first step in the process is to establish your business credit profile. You do that by setting up your business to be a fundable entity separate from you the owner. That includes having separate contact information, using an EIN rather than your personal SSN, formally incorporating, and opening a separate, dedicated business bank account.

Once that is said and done, you can rest assured that your business accounts that are reporting will show up on your business credit report, thus causing your business credit score to climb. Not all accounts will report, but the Credit Line Hybrid does. That’s a good start. A business credit expert at Credit Suite can guide you through finding other vendors that you qualify to get an account with that will report as well.

Check out our best webinar with its trustworthy list of seven vendors to help you build business credit.

Business Borrowing from Your Family and Friends is a Stepping Stone

It’s not a long term solution. There are many business owners who get their start with the help of friends and family. That’s a good thing. It’s a great way to get the ball rolling when your own resources are limited.

However, you don’t want business borrowing from friends and family to be your primary solution for the life of your business. Not only will this source of funds eventually dry up, but it can also cause some major drama.

The key to being able to fund your own business, and keep everyone else on your side, is to work toward building a business that is fundable on its own. As you do so, you will see that your friends and family continue to cheer you on, and eventually that’s the only help you’ll need.

With a number like this, small business owners need a competitive edge. If you are building a business, chances are you’re looking for ways to get your leg up on the competition. To accomplish this, you’ll need a good marketing strategy and access to the best digital marketing tools.

In this post, I’m going to outline 21 digital marketing tools you need when starting a business. You may be familiar with a marketing tool or two in here; others might be new to you.

From simplifying your social media marketing efforts and project management to finding freelancers, each of these tools will help you get the competitive edge you’re after.

Are you ready to grow your business with digital marketing?

This isn’t something you should wait on. Instead, you should implement an email marketing strategy on day one.

With more than 12 million customers, MailChimp has claimed its spot as one of the top email marketing providers and digital marketing tools in the world.

While there are alternatives, this tool remains one of the best, for many reasons:

History dating back to 2001, well before most companies began using email marketing

Self-service support options, ensuring that you can quickly find answers to all of your questions

Free plan for those with less than 2,000 subscribers and those who don’t send more than 12,000 emails per month

When starting a business, it’s not likely that you will have more than 2,000 subscribers. For this reason, you can get started with MailChimp early using the tool for free as you get your feet wet with email marketing and then move to a paid plan as you scale.

There is no stone left unturned, when you rely on HubSpot’s all-in-one marketing software.That’s why it’s a top choice for those who are starting a business.

With everything you need in one place, you don’t have to pull yourself in many different directions. This will help you to find success in the early days and help you as you grow.

Trello is a digital marketing tool that helps you to manage projects and stay on the same page as your team–a sound digital marketing practice if you want to save time and frustration.

For example, you can share blog posts on Trello before you publish them. This gives others on your team the opportunity to review the post, weigh in with their thoughts and make changes that could strengthen the piece before it goes live.

In the past, before the days of Trello and similar programs, email was the best way to collaborate with your team. While this is still helpful, to a certain degree, it can lead to confusion, missed messages, and frustration.

With Trello, everything related to your online marketing strategy can be shared in the same place. It only takes a few minutes to set up a board. Even better, you can quickly invite your entire staff, all of whom can jump in on the action without delay.

Trello isn’t the only digital marketing tool of its kind, but it’s, by far, one of the best. When it comes to collaborating with others regarding marketing tasks, this tool is hard to beat.

Social media plays a big part in the success of any company, regardless of size, age, or industry. In fact, I’d argue that social media marketing is a must to thrive in this digital era.

Digital marketing tools like Hootsuite allow you to schedule social media posts in advance, thus saving you loads of time.

Hootsuite offers tons of features to help you grow your business. For example, you can:

Identify influencers for your marketing team and leads for your sales team

Reply to comments and mentions through the dashboard–there’s no reason to visit each individual platform

Take advantage of pre-written responses

Schedule posts when your audience is most active (even if you’re asleep!)

Social media marketing is not as difficult as it sounds, especially when you rely on tools like Hootsuite. With this particular tool, you can schedule and manage social media profiles for more than 30 platforms.

Imagine doing this by hand, without a central dashboard to guide you. It would be enough to frustrate even the most experienced entrepreneur, let alone a new business owner. Let Hootsuite take over like the social media marketing manager it is.

As one of the top free tools from Google, Analytics should be part of your digital marketing strategy from the very start. In fact, I’d argue it’s one of the most powerful digital marketing tools out there.

It only takes a couple of minutes to add the Analytics code to your website, giving you the ability to track every action by every visitor.

This is considered by many to be nothing more than a traffic tool, but it can actually have a big impact on your marketing strategy, if you know what you’re doing.

Take, for example, the ability to see where your traffic comes from:

Maybe you realize that a particular social media campaign is driving tons of traffic to your website. With this data, you can adjust your future strategy, in an attempt to capture the same results.

Or, maybe you find that a particular set of keywords is doing wonders for your organic traffic. Again, you can turn your attention to these keywords, ensuring that you keep these in mind as you create content down the road.

Google Analytics isn’t one of those digital marketing tools you can ignore. Installing this early on is a key decision, in regards to your digital marketing strategy. The data you can collect is extremely valuable.

The tagline of this digital marketing tool says it all:

Track, analyze and optimize your digital marketing performance. See what’s working and what’s not, across all campaigns, mobile and web.

It’s good that you want to spend so much time on digital marketing in the early days of your business. But, do you really want to make decisions that aren’t having an impact?

You need to track and analyze every move that you make, as this is the only way to focus on the tactics that are providing the best return on investment (ROI).

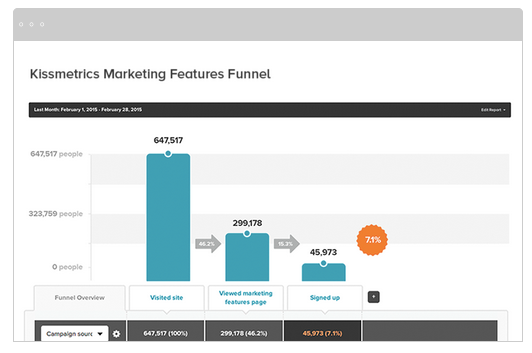

With KISSmetrics, you can easily see what’s working and what’s not, across all of your campaigns.

Take, for example, its Analytics products. With a funnel report, you can see if there are any “leaks” in your business. Here’s a screenshot of what to expect:

Starting at $120/month, KISSmetrics isn’t the cheapest digital marketing tool on this list. Even so, it’s one that you’ll want to think about, as your business gets up and running.

With a variety of products at your fingertips, the insights you receive will be invaluable to your company’s growth.

While this is a great way to engage your audience and send traffic to your website, it’ll only work in your favor if you have a solid plan in place.

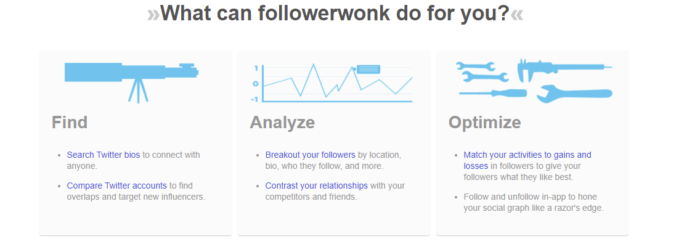

Tools, such as Followerwonk, are designed to help you improve your social media marketing strategy, such as by digging into your Twitter analytics data.

I included this digital marketing tool on the list for two reasons: it’s easy to use and it’s extremely effective.

Followerwonk breaks down its service into three distinct categories:

Find: Use the tool to search Twitter bios and compare accounts.

Analyze: Breakdown your follower list by bio, location, who they follow, and many other criteria.

Optimize: match your strategy to follower gains and losses, to understand what type of content performs best.

The only downside of Followerwonk is that it can’t be used with other social media platforms, such as Facebook, Instagram and LinkedIn. However, if you have big plans for Twitter, this is a digital marketing tool you should use often.

Even though you may not use it on a daily basis, it can come in handy from time to time. After all, it’s imperative that you understand your audience.

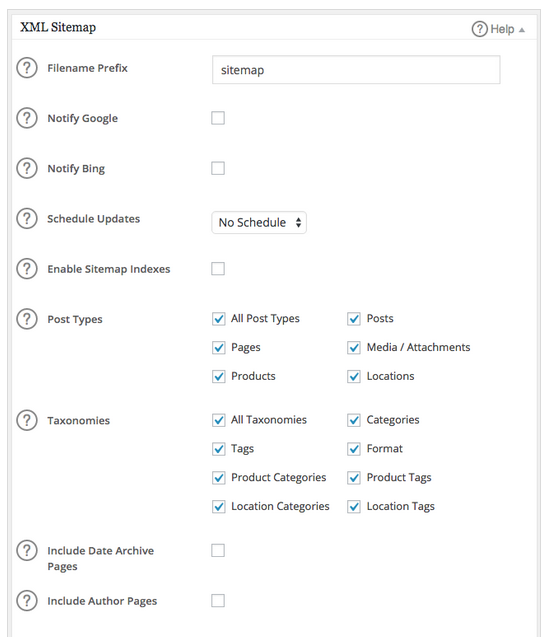

If WordPress is your content management system (CMS) of choice, you shouldn’t hesitate to install the All in One SEO Pack plugin.

A big part of your digital marketing strategy should be based around search engine optimization (SEO) and this digital marketing tool will ensure that you always make good decisions regarding your content and its appeal to search engines.

Automatically notifies major search engines, including Google and Bing, of any site changes

Even though all of these features are exciting, it’s something else that has made it one of the most popular WordPress plugins of all time: its ease of use.

Here’s a screenshot, showing a small portion of the tool’s back end:

You don’t have to make many decisions in order to get started. And, if you’re ever confused as to what you should be doing, there is help to be had. All you have to do is click the “?” symbol and you’re provided with more information and advice.

The All in One SEO Pack plugin has more than a million active installs. You won’t have to look far to find competitors, but there’s a reason why so many people use this digital marketing tool.

Not only is it free and simple, but it’s results can’t be denied. It will definitely help your website from an SEO perspective, which is something all new businesses need.

BuzzSumo is a big deal for people who need to learn more about their market.

When you start a business, it’s safe to say you know a thing or two about your industry and primary competitors. But, once you dig around more, you’ll find that there is tons of data you can use to your advantage.

If you want to better understand your competition or if you want to learn what type of content performs best with search engines and your audience, you don’t need any other digital marketing tool by your side.

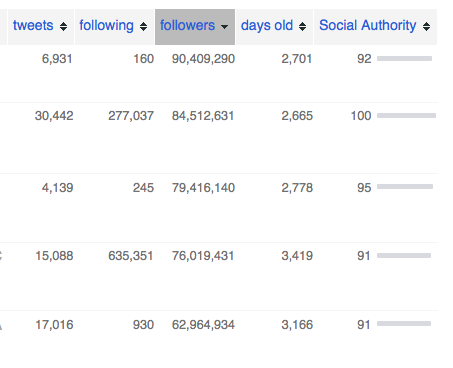

A BuzzSumo search results page looks something like this:

Additionally, there is high level data associated with each result:

This information can come in handy at many times, such as when you are creating content for your blog.

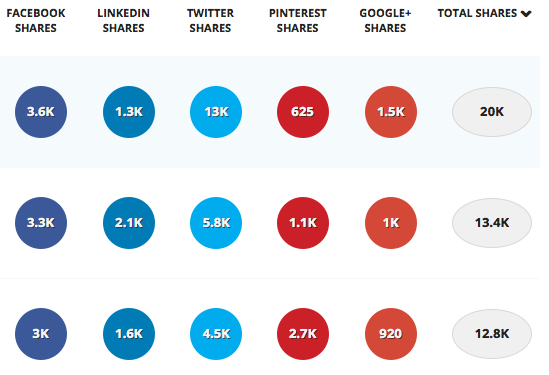

Why guess as to what is performing best in your niche? You can use BuzzSumo to answer this question with 100 percent accuracy.

With this search, you see that the top result has approximately 20k social shares. You now know what to strive for, if you want to achieve the same level of success.

As a big fan of BuzzSumo, this is a ditial marketing tool that I use on a regular basis. Even if you don’t do much with the data at first, each search will help you to better understand your competition and target audience.

Do you ever find yourself asking this question: what’s working and what’s not about my website?

This is where Crazy Egg can step in and provide assistance.

There are two keys here:

You can use Crazy Egg to make website changes that generate better results.

You don’t need much, if any, IT help to get started.

When you’re new to your business, you don’t want to spend countless hours dealing with IT issues. Unfortunately, this often happens when it comes to split testing. Unless you use Crazy Egg, of course.

The tool is packed with features, such as:

heatmaps and mouse recording

analysis and reporting

platforms and integrations

targeting and personalization

research and user feedback

A tool that helps you understand what your website visitors like and don’t like, so you can maximize your sales and leads, means that you have to give Crazy Egg a try. It’s one of those digital marketing tools that you don’t know you need, until you use it one time.

Not only is keyword research a challenging task, but it can also get expensive with the price of premium keyword research tools. Your typical free software won’t offer you much but UberSuggest isn’t your typical free software.

As a whole, this digital marketing tool is easy for beginners because the dashboard is simple to navigate so you can quickly find the data you want. You’ll start by entering a root keyword or domain that you want to research. You get up to three free searches per day on the free version and you can upgrade to a paid software as well.

UberSuggest provides useful keyword information such as total search volume, difficulty, and paid difficulty if you’re thinking of running an ad campaign around that keyword.

As you work your way down you’ll see historical data that will show you how that keyword has trended over time. This is helpful for determining seasonal keywords or ones that are popular now but may die off over time.

You also get keyword ideas and suggestions that are relevant to the one you’re searching for so you can update older content or develop a content marketing plan.

Overall, UberSuggest is an amazing free keyword research tool that is a great choice for beginners and has enough value as a paid tool for those who are scaling as well.

CoFoundersLab is a great digital marketing tool for small businesses that are growing but need a little help to take things to the next level. It uses AI to help you find a cofounder, additional member, or advisor based on a certain set of criteria.

The best digital marketing tools make life easier. CoFoundersLab intends on helping to create a large ecosystem of business owners, entrepreneurs, consultants, and advisors so it’s that much easier to find whatever you need at the current stage in your business.

For example, you can search for someone with a specific skill and find them instantly without having to post on job boards, conduct interviews, and do onboarding. If you’re looking for an SEO content creator, you’ll simply fill out that set of criteria and be instantly connected to someone who can fill that role.

It’s similar to other freelancing platforms out there, but what separates CoFoundersLab is you can find someone who is on the same level. If you’re looking for someone to financially back your business or simply support you equally in your venture, this might be the place to do it.

When it comes to must-have digital marketing tools, Adobe Sign more than makes the cut. It’s a cloud-based e-signature service that helps you use less paper, save time, and get signatures using an automated signature system. You can send documents, sign, and manage the whole process via desktop or mobile device.

There are also integrations to keep records of all the signatures you’ve received so you can reference back if you lose something important.

This simple but useful tool solves a major problem that a lot of businesses have. More and more people are working remotely and may not have access to printers and scanners. This creates delays in your workflow and can frustrate customers if you’re unable to get them what they want because you’re waiting on signatures and approvals.

Adobe Sign is also usable from anywhere on any device. Someone can be on their way to a meeting in the car and sign on their mobile device using their fingertip. No need to print anything, scan, fax, anything. It’s completely digital, safe, and secure.

DropBox is an essential piece of the modern digital business. It allows all the working pieces of your business to come together in one place to eliminate clutter and save time looking for things.

Organization is the key to a successful business, and downloading and sharing files simply doesn’t cut it anymore. With people working from home, you can’t have everyone downloading personal company files onto their computers, misplacing them, or potentially abusing them.

DropBox prevents this from happening by being a totally cloud-based document sharing platform that allows you to set permission levels so certain people can only see what they need to.

You can also connect other tools like Slack and Zoom to DropBox so you have everything in one place. All company data stays in one place so it’s organized, safe, and accounted for.

If you’re still manually downloading files to your computer, attaching them to emails, and sending them off into space, you’ll find DropBox is a much more efficient and safer way to keep track of documents and document sharing in your business.

I don’t know where I would be without the full line of Gmail products. There used to be a time when we’d create pieces of content in Word platform, download it, and then attach it to an email and send it off.

The next person would mark it up with notes and adjustments, send it back, and the process would start over.

Thankfully, those days are long gone.

With Google Docs and Sheets, you can share documents in real-time and actually mark them up with the writer looking at them so you can see what they’re doing. There’s a chat feature and a suggestion area, too where you can ask questions and provide responses as to why a certain adjustment was made.

There’s a level of security and protection here, as well. Different permission levels ranging from “view” to “edit” give you complete control over your documents. If you’re sending a document off as a reference to something, you might not want that person to make any changes to it without making a copy for themselves, the Gmail Suite of products can do that.

Plus, everything syncs with your Google Calendar. If you’re talking in an email about setting up a call in three days, you can instantly set that appointment on your calendar and you’ll receive reminders across all your devices.

oDeskWork is a freelancer platform that connects you with the right virtual assistant or freelancer to support your business. At some point, every business needs to start hiring. No matter what business you’re in, to grow and scale, you need a support system because you can’t do everything.

This is where digital marketing tools like oDeskWork come into play. You can upload current projects that you need completed, browse profiles, and start communicating with potential candidates.

The platform also offers payment protection, so you ensure you get the services you anticipated. Payments are only released to the freelancer when you’re satisfied with the work they completed.

oDeskWork has experts and freelancers in all different kinds of niches including digital marketing, virtual assisting, transcribing, proofreading, writing, editing, SEO, WordPress, and more.

Upwork is a freelancer platform that connects you with qualified candidates who can help your business grow, making it a must-have digital marketing tool. What I like most about Upwork is the transparency you get and the fact that you can see all types of work that the freelancers have completed.

For example, if you’re browsing for someone to build you a WordPress website, you wouldn’t hire someone without first seeing what type of work they do, right?

The platform will show you examples of their work, their job success rating, a description of their skills, their rate per hour, as well as any badges they’ve earned for continuous performance.

When you’re searching for tools for digital marketing agencies, the last thing you need is to waste time with people who can’t deliver. Upwork ensures that doesn’t happen with their escrow protection as well. None of the money you pay for a job will be released until you are happy with it.

I also find that Upwork is a great place to find long-term working relationships with freelancers that you can use on an ongoing basis versus a one-off job.

I like to think of Fiverr as Upwork’s little brother. When you’re looking to create long-term working relationships and hire someone who can really provide you with a premium service, you should turn to Upwork.

Sometimes though, you’re just looking for a quick job that someone can turn around fast for an affordable price. For example, if you need someone to do up a quick logo for an affiliate site for five dollars, Fiverr is the way to go.

One thing I really like about Fiverr is you can quickly sift through freelancers using the search feature. Type in the service you’re interested in, and you’ll find information such as overall rating and average starting cost.

Fiverr also provides certain freelancers with titles like “top-rated seller” and “level 2 seller.” These will help you determine what level of experience you’re looking for in the job you need to be completed. The best digital marketing tools offer this kind of trust.

This tool is best for one-off jobs that are lower budget and not as difficult, but I wouldn’t recommend hiring off Fiverr for anything too involved such as link building or content creation.

Need to stay on task? This digital marketing tool can help.

OmniFocus is a task management tool that helps you manage all your operations in one place. You can keep track of everything that’s going on all from your browser or mobile device.

You can tag certain projects, assign them to the individual you want to complete them, and set due dates so you can lay out your week in the most productive way possible. As work comes in, you can assign support workers to handle the task and close it out when it’s complete.

One of my favorite things about OmniFocus is the forecast feature where you can get an overall snapshot of what you have coming up in the future including recurring tasks that might only happen once per quarter, bi-annually, or even every few years. This ensures that no one forgets anything.

The main downside is that this tool is only available for Apple users at this point. For all the Windows and Android people out there, you’ll have to go with something else like Trello or ClickUp for now.

We all know Zoom as the video conferencing software used to bring people together no matter where they are on the planet. We’re all facing our own unique remote working situation but we still need to connect sometimes and Zoom allows that to happen. The best digital marketing tools help bring businesses together.

You can share your screen, draw on the screen, record meetings, and invite others to join in as well. Zoom offers free video conferencing for up to 100 participants for up to 40 minutes.

If you’re holding a one-on-one meeting that runs longer than 40 minutes, I’ve found in the past that Zoom will often extend the meeting for free with no time limit.

Toggl helps bring this list of digital marketing tools together. For all the work you’re doing, freelancers you’re managing, and documents you’re sharing; you need to have an idea of how long everything takes.

This tool does that with time tracking, reporting, and project planning. You can use Toggl to get an accurate representation of how long a task or project will take so you can know how many resources you need to allot for next time.

Toggl offers a few different tools for time tracking, project planning, and candidate-screening so it’s an all-inclusive tool for businesses that manage a remote team.

Conclusion

Starting or growing a business isn’t easy, but it doesn’t have to be overwhelming, either.

The first step is to create a strong digital marketing strategy–one that incorporates social media marketing, search engine optimization, email marketing, and consistent, valuable content that truly speaks to your audience.

Ensuring your business succeeds means using the right digital marketing tools at the right time. It’s my hope that this list will help you in your digital marketing efforts and bring you the success you seek.

Would you add any other tools to this list? Did you use any of these as you launched your small business? Share your thoughts in the comment section below.

0% APR Business Credit Cards Can Be Within Your Reach

Are you an entrepreneur looking for 0% APR Business Credit Cards? Check out our choices – you can make it work for your business.

We looked into lots of low and zero APR business credit cards for you. So, here are our choices.

0% APR Business Credit Cards Can Be a Great Choice

Per the SBA, business credit card limits are a whopping 10 – 100 times that of personal credit cards!

This reveals you can get a lot more cash with business bank card.

And you will not need collateral, cash flow, or financials to get small business credit.

Company Credit Card Benefits

Benefits can vary. So, see to it to select the benefit you like from this selection of alternatives.

And always check rates on the appropriate sites.

0% APR Business Credit Cards: Introductory APR– Pay Zero!

Blue Business® Plus Credit Card from American Express

Take a look at the Blue Business® Plus Credit Card from American Express. It has no yearly charge. There is a 0% introductory APR for the initial year. Afterwards, the APR is a variable 13.24– 19.24%.

Get double Membership Rewards® points on everyday business purchases like office supplies or client suppers for the initial $50,000 spent each year. Get 1 point per dollar later on.

You will need good to superb credit scores to qualify.

Also have a look at the American Express ® Blue Business Cash Card. Note: the American Express ® Blue Business Cash Card the same as the Blue Business® Plus Credit Card from American Express. Yet its rewards are in cash versus points.

Get 2% cash back on all qualified purchases on up to $50,000 per calendar year. After that get 1%.

It has no annual fee. There is a 0% initial APR for the first year. Afterwards, the APR is a variable 13.24– 19.24%.

You will need great to excellent credit to qualify.

Bank of America ® Business Advantage Cash Rewards MasterCard ® credit card

Take a look at the Bank of America ® Business Cash Rewards MasterCard ® credit card. Get an 0% introductory APR for the first 9 billing cycles of the account. Afterwards, the APR is 12.24%– 22.24% variable. There is no annual charge. You can get a $300 statement credit deal.

Get 3% cash back in the category of your choice. So these are gasoline stations (default), office supply stores, travel, TV/telecom & wireless, computer services or business consulting services. Earn 2% cash back on dining. So this is for the initial $50,000 in combined choice category/dining purchases each calendar year. After that earn 1% after, with no restrictions.

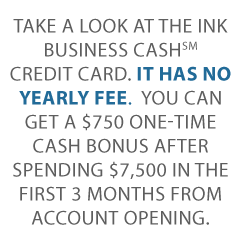

Take a look at the Ink Business Cash℠ Credit Card. It has no yearly fee. There is a 0% initial APR for the first year. After that, the APR is a variable 13.24– 19.24%. You can get a $750 one-time cash bonus after spending $7,500 in the first 3 months from account opening.

You can get 5% cash back on the initial $25,000 spent in combined purchases at office supply stores and on web, cable, and phone services each account anniversary year.

Get 2% cash back on the first $25,000 spent in combined purchases at filling stations and restaurants each account anniversary year. Earn 1% cash back on all other purchases. There is no limit to the amount you can earn.

Take a look at the Capital One ® Spark® Cash for Business card. It has an introductory $0 annual charge for the initial year. After that, this card costs $95 annually. There is no initial APR deal. The regular APR is a variable 20.99%.

You can get a $500 one-time cash bonus after spending $4,500 in the first three months from account opening. Get unlimited 1.5% cash back with Cash Select.

You will need great to impressive credit to qualify.

Check out the Discover it ® Business Card. It has no yearly fee. These are 0% APR business credit cards for one year. Afterwards the regular APR is a variable 14.49– 22.49%.

Get unlimited 1.5% cash back on all purchases, without any category constraints or bonuses. They double the 1.5% Cashback Match at the end of the initial year. There is no minimal spend requirement.

You can download transactions quickly to Quicken, QuickBooks, and Excel. Note: you will need good to outstanding credit to get approved for this card. https://www.discover.com/credit-cards/business/

Irresistible Cards for Jackpot Rewards That Never Expire

Capital One ® Spark® Cash Select for Business

Take a look at the Capital One ® Spark® Cash Select for Business card. It has no yearly fee. You can get 1.5% cash back on every purchase. There is no limitation on the cash back you can earn. Additionally earn a one-time $200 cash bonus once you spend $3,000 on purchases in the very first 3 months. Rewards never expire.

Pay a 0% introductory APR for 9 months. Then pay 13.99%– 23.99% variable APR after that.

You will need good to outstanding credit scores to qualify.

Alternatives to 0% APR Business Credit Cards: Business Credit Cards for Extravagant Travel

Flat-rate Travel Rewards

Capital One ® Spark® Miles for Business

Take a look at the Capital One ® Spark® Miles for Business card. It has an initial annual fee of $0 for the initial year, which after that rises to $95. The regular APR is 20.99%, variable due to the prime rate. There is no introductory annual percentage rate. Pay no transfer costs. Late fees go up to $39.

This card is great for travel if your expenses do not fall under common reward categories. You can get unlimited double miles on all purchases, without any limitations. Earn 5x miles on rental cars and hotels if you book via Capital One Travel.

Get an introductory bonus of 50,000 miles. That’s the same as $500 in travel. But you only get it if you spend $4,500 in the initial 3 months from account opening. There is no foreign transaction charge. You will need a great to superb FICO rating to qualify.

Earn 50,000 bonus miles if you spend at least $4,500 within 3 months of your rewards membership enrollment date

For an excellent sign-up offer and bonus categories, take a look at the Ink Business Preferred ℠ Credit Card.

Pay an annual fee of $95. Regular APR is 15.99– 20.499%, variable. There is no initial APR offer.

Get 100,000 bonus points after spending $15,000 in the first 3 months after account opening. This works out to $1,250 toward travel rewards if you redeem through Chase Ultimate Rewards.

Get 3 points per dollar of the first $150,000 you spend with this card. So this is for purchases on travel, shipping, net, cable, and phone services. Plus it includes marketing purchases made with social media sites and search engines each account anniversary year.

You can get 25% more in travel redemption when you redeem for travel via Chase Ultimate Rewards. You will need a good to remarkable FICO score to qualify.

Bank of America ® Business Advantage Travel Rewards World MasterCard® credit card

For no yearly fee while still getting travel rewards, take a look at this card from Bank of America. It has no annual fee and a 0% initial APR for acquisitions throughout the first 9 billing cycles. Afterwards, its regular APR is 12.24– 22.24% variable.

You can get 30,000 bonus points when you make a minimum of $3,000 in net purchases. So this is within 90 days of your account opening. You can redeem these points for a $300 statement credit towards travel purchases.

Get limitless 1.5 points for every $1 you spend on all purchases, anywhere, every time. And this is regardless of how much you spend.

Likewise earn 3 points per every dollar spent when you book your travel (automobile, hotel, airline) with the Bank of America ® Travel Center. There is no limit to the number of points you can get and points do not expire.

You can earn up to 75% more points on every purchase if you have a corporate checking account with Bank of America and qualify for Preferred Rewards for Business.

Alternatives to 0% APR Business Credit Cards: Safe Corporate Credit Cards for Fair Credit

Capital One® Spark® Classic for Business

Look at the Capital One® Spark® Classic for Business. It has no yearly cost. There is no introductory APR offer. The regular APR is a variable 26.99%. You can get unlimited 1% cash back on every purchase for your company, with no minimum to redeem.

While this card is available if you have average credit scores, beware of the APR. Nonetheless if you can pay on schedule, and in full, then it’s a bargain.

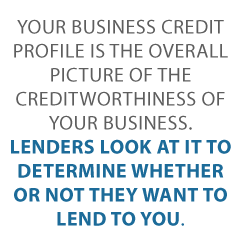

Your business credit profile is the overall picture of the creditworthiness of your business. Lenders look at it to determine whether or not they want to lend to you. Your business credit score is likely the most important piece of this. As such, it’s important to know the best way to raise credit score. You have a personal credit profile alsol, and that is considered by most lenders as well.

Total Business Credit Profile Management: The Sure-Fire Best Way to Raise Credit Score

In fact, many lenders look at your personal credit profile first. However, if you have a strong business credit profile, it can only help you. Your business credit score is a huge part of that, so you need to know the best way to raise credit score for business.

Best Way to Raise Credit Score: What Is a Credit Profile?

Of course, you cannot let the rest of your business credit profile go unattended. Before you can work to execute the best way to raise credit score, you have to understand and learn how to manage your total business credit profile.

Your business credit profile is everything the business credit reporting agencies have on your business. For example, your open trade accounts, payment history, how you stand up in relation to other businesses, and more. The top three business credit reporting agencies are Dun & Bradstreent, Experian, and Equifax. FICO also offers a business credit report known as the FICO SBSS.

When a potential lender looks at your business credit profit, it can pull from any of these. The report will contain a business credit score, but it will contain a lot more as well.

Best Ways to Raise Credit Score: What is a Business Credit Score

So, what exactly is a business credit score? It is similar to your personal credit score, but it is for your business. Unlike your personal credit score, it is connected to your EIN, not your social security number. It is a numeric rating assigned to your business that helps a lender determine how likely your business is to repay debt. The number is calculated based on a number of things. The most influential factor is your payment history.

The more positive payment history you have, the better. That means two things. First, the longer you have been paying accounts on time the better your credit score will be. Also, the more accounts you are paying on time the better your score will be.

Best Way to Raise Credit Score?

So, what is the best way to raise your business credit score? The simple answer is to increase positive payment history and reduce negative payment history. Let’s break it down further.

Add More Trade Accounts

It sounds simple, but it’s not really. Unlike personal credit, not all business credit accounts report to the business credit reporting agencies. With personal credit, your payments on accounts are automatically reported to personal credit.

You have to be intentional about finding business credit accounts that will report. This can take some time and digging. A business credit expert can come in really handy here. Most vendors do not make it easy for the average Joe to find out if they report or not. A business credit expert will likely have relationships with vendors that allow them to know or find out this information more easily.

Aside from this, you can talk to vendors you already have a relationship with. You can ask them to report your payments if they already extend you credit or net terms on invoices. If they do not, you can ask if they will, and if they will then report. They don’t have to , but if they do, this can be the best way to raise credit score quickly.

You can also talk to providers that you pay monthly. Everyone pays utilities, phone, and internet bills. Ask those providers to report your payments to the business credit reporting agencies. They do not have to, but they might. If they do, this is another great way to improve your business credit score.

Handle Accounts Responsibly

Handling your business responsibly in every way affects your entire business credit profile. However, handling your trade accounts responsibly by making consistent, on-time payments is the number one best way to increase credit score. After all, the business credit score tells lenders how likely you are to pay, and nothing predicts future behavior like current habits.

Monitor and Correct Your Business Credit Report

Sometimes the best way to raise your credit score is as simple as correcting mistakes. However, without credit monitoring, you cannot know what those mistakes are, or if there are any at all. Personal credit monitoring is easy. You can access a full, complete report annually for free. Not only that, there are a plethora of free apps that offer a peek at your credit score and summary report throughout the year.

That is not the case with your business credit report however. You have to pay to get a glimpse of it at all. Each of the big three offer monitoring options, for a fee. Credit Suite can help you monitor your business credit for a fraction of the price.

Business Credit Profile vs. Personal Credit Profile

To better understand the best way to raise credit score for your business, it can help to understand some of the differences between business credit profiles and personal profiles. There are many, but these specifically seem to cause a lot of misunderstanding and confusion among borrowers when they are denied funding.

Late Payments

Both business and personal credit reports are affected greatly by late payments. Yet, business credit scores are affected faster. Late payments are not reported to personal credit reports typically until they are 30 days past due. Late payments on business credit accounts are reported if only one day late.

Inquiries

Hard credit checks on your personal credit will lower your credit score. However, business credit reports are different. A credit check on your business credit profile does not affect your business credit score.

Data Reported

In addition to late payments being reported much more quickly, accounts on your business credit profile are listed by industry. In contrast, personal credit lists the name of the company that issues the credit.

Also, personal credit reports show the exact amounts of accounts, while business credit reports show rounded amounts. How long data stays on a personal credit report varies, but typically it’s the life of the file. Information stays on business credit reports an average of 3 years.

Also, with personal credit accounts, almost every account reports to the credit reporting agencies. In contrast, only about 7% of business credit accounts report to business credit reporting agencies. This is why you have to be intentional to get accounts reporting to business credit, and that is only one of many reasons working with a business credit expert is the way to go.

One last thing to note about business credit versus personal credit is this. While your business credit profile is totally separate from your personal credit profile and does not affect in any way, the reverse is not true. Your personal credit information can affect your business credit profile, and in some cases, even your business credit score.

What’s the Best Way to Raise Credit Score for Your Business?

There isn’t really one best way to raise credit score. In reality, the best way depends on what is pulling your score down to begin with. Is it a lack of sufficient history? Then you just have to give it time. Are there not enough accounts? You need to add more. Are you not paying on time? Start paying on time! Are there mistakes on your business credit report? Fix them. However, one thing is for sure. Whatever the problem is, paying your accounts consistently on-time will only raise your score. You cannot go wrong there.

Fundability is like a puzzle. There are many different pieces that make up the complete picture. Financial statements are part of that, both business and personal. Business tax returns are just one piece of the puzzle.

The Basics of business Tax Returns and How They Affect Fundability

According to the IRS, except for partnerships, all businesses have to file an income tax return. There are different forms. The one you need to use depends on the business structure you choose. In addition to partnerships, there are sole proprietorships, corporations, S-corps, and LLCs.

Business Tax Returns for Beginners

If you are a new business owner, there are some things about paying business income taxes you need to know. They are not exactly the same as paying personal income tax. One of the major differences is that you may have to pay estimated tax.

Estimated Tax

Federal business income tax is pay-as-you-go. You have to pay the tax as you earn or receive income.

Sole proprietors and S-corps that expect to owe tax of $1,000 or more when they file their business tax return, will generally need to make estimated payments. For corporations, those that expect to owe $500 or will need to pay estimated taxes.

Documentation

You are going to have to track expenses, asset purchases, income and more. The absolute best way to do this is to implement an excellent bookkeeping system from day one. HIring a bookkeeper or bookkeeping agency is best. If you cannot do this, at least choose one of the many great accounting software options available.

With these options, you can print reports at the end of each tax period. Then just hand them over to your tax preparer.

Learn more here and get started with building business credit with your company’s EIN and not your SSN.

Tax Preparation

Do nottry to prepare tax returns for your business on your own. Just hire a tax professional. The cost will be well worth the time and money you save. You reduce the chances of a mistake, and you have back up if your business has to undergo an audit.

Note that your tax preparer should not be the same person as your bookkeeper or accountant. Whoever keeps the books should not do the tax returns. Larger corporations are not even allowed to have the same firm handle bookkeeping and taxes. With smaller businesses the same firm is ok, but it is not wise for the same person to do both. This helps deter and detect fraud.

This means, even if you have an in-house bookkeeper or accountant, they can prepare everything the tax preparer needs. However, they should not complete the tax forms themselves.

Other Choices You Have to Make Before Filing Your First Business Tax Return

When it comes to filing tax returns for your business, you have some choices to make. Discuss these with your tax professional thoroughly before making any decisions.

Cash vs. Accrual

You will need to choose your method of accounting. You can choose either cash or accrual basis. With the cash basis, you count income as revenue when it is collected. In the same way, you count expenses when you pay them. With accrual basis accounting, you record income when you earn it. You count expenses when they are incurred.

For example, using cash basis accounting, you don’t necessarily count revenue as soon as an item sells. You count it when you get the cash. That means, unless the buyer pays cash on the spot, you do not record revenue until the customer pays the invoice. You do not carry receivables on your books.

Using accrual basis accounting, you will record revenue when the item sells. A receivable for the invoice will go on the books..

If your business is new, you may have more unpaid expenses and more uncollected income at the end of the year. Then, it looks best for you to take those outstanding expenses as a deduction. That’s accrual basis accounting.

Yet, later on when your business is profitable, your outstanding receivables will likely be higher than outstanding expenses or payables. If you are using the accrual method, you will be recording more net income and thus paying more in taxes under the accrual method. Consider this when making your decision.

Learn more here and get started with building business credit with your company’s EIN and not your SSN.

Once you decide which method to use, you will have to stick with it through the life of your business. Although, there are exceptions that allow for changes to be permitted. Also, certain businesses, like those with larger revenues or that carry inventory, do not have a choice. They must use the accrual method.

Depreciation

There are a few different options about depreciation. Discuss this thoroughly with your tax preparer to ensure you are doing what is best for your business. The first choice will be about first year depreciation. Typically depreciation on assets is written off over the course of 5 to 7 year. However, the IRS allows a first year deduction of up to $100,000 for equipment and most furniture instead. This is an election most business owners take.

However, if you do not make a profit you cannot take the $100,000 deduction. You can carry it forward to a year that you do make a profit.

Early on, you might want to think about using the slower depreciation method. Then, you can use the deductions later. At that time, there will likely be more income. You may be in a higher tax bracket than the startup phase. The depreciation deductions may come in handy.

The most important thing in making any tax decision is to discuss it with your tax professional.

Business Tax Returns and Fundability Crossover

Fundability is, in the most simple terms, the ability of your business to get funding. For a business to be fundable, it needs to be fully recognizable as an entity separate from its owner. There is a lot of crossover between fundability and business taxes.

Fundability, Business Tax Returns, and Entity Type