How to Grow Your Local Business During Uncertain Times

No doubt this is a hard time to grow a local business. Coronavirus has likely forced you to make big changes to the way you operate. It’s almost certainly hit your bottom line too.

However, it’s still absolutely possible to grow your local business at a time like this. You just have to be smart about it. In this article, I’ll talk you through how to do that. First, though, here’s a bit of detail on why this is such a challenging time for businesses like yours.

The Effects of the COVID-19 Pandemic on Local Businesses

You’re probably sick of reading and hearing the word “unprecedented.” I know I am. Unfortunately, it’s just the best word to describe the current climate for local businesses.

By the end of March, 32 states had locked down in response to the pandemic. Two in five small businesses across the US had temporarily closed by this point, with nearly all of those closures due to COVID-19.

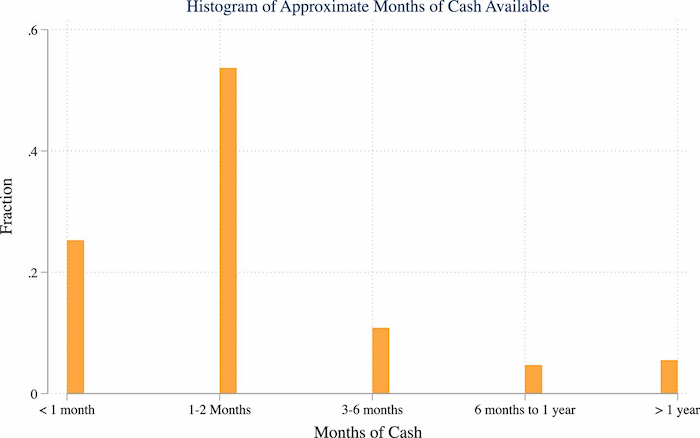

Closing your doors has big financial implications. It is concerning that the vast majority of local businesses aren’t in a position to handle even short-term pressure on their earnings, with around four-fifths only having up to two months of cash available to pay their expenses.

Because of this, it’s hardly surprising that the number of active business owners in the US plummeted by 3.3 million (or 22%) in the two months from February to April alone. That’s the largest drop on record, and it affected practically every industry.

Luckily, if you have access to the right strategies (like local promotions) and tools (such as messaging services like Podium), you may still be able to grow your business even in these uncertain times.

Six Strategies to Grow Your Business During the Age of Coronavirus

The pandemic might have affected your business growth in any number of ways. Maybe you’ve been forced to shutter your store(s) for a certain amount of time. Maybe your customers are buying less at the moment. Or maybe the industry you’re in means you’ve barely even got a “product” to sell, like cinemas and travel companies.

Whatever the case, if you’re going to grow your local business in the current climate, you need to adapt. Here are tips on how to do it:

1. Use the Right Tools

I know what you’re thinking: “I’m already worried about cash flow, now this guy’s telling me to invest in a bunch of tools!” Well, what if I told you that by choosing the right tools (some of which are free, by the way), you massively increase your chances of growing your local business?

You likely know that there are thousands of tools designed to drive small business growth, but I’ve focused on the areas where you can really shift the dial:

Issue: Customer Messaging

There are so many benefits to improving your communications with existing and potential customers.

You can generate more reviews, which act as a trust factor and make your business more credible. You can collect payments faster and with less hassle. You can issue more timely (and more effective) reminders, reducing the chances of no-shows.

To solve your customer messaging you can use a tool like Podium. Here’s how I use it:

- Set up one inbox to rule them all: What’s the biggest barrier to better communications? Trying to keep track of all your different platforms. Customers could be messaging you via Facebook, Twitter, phone, and your website (and maybe a bunch of others, too). Podium brings all those communications together in one place, ensuring you never miss a message.

- Connect remotely with website visitors: Ever wish you could get closer to the people on your website? Find out what stops them from buying or converting there and then? With Podium, you can. Add live chat to your site and every time they ask a question, they’ll automatically move to a text conversation, so you’re no longer tied to your computer (and nor are they).

- Enable on-the-go customer service: You likely don’t have a dedicated customer service team. In fact, you might be your whole customer service team. So what happens when you’re not at your desk or in the store? Stuff gets missed! Podium allows you to text quick responses when you’re out and about, so you never leave anyone hanging.

- Chat face-to-face: Texting is great. But sometimes it’s just not the best way to respond to a customer or prospect. Maybe they’ve got a complex question or require a nuanced response that’s hard to tap out on your phone’s keypad. Podium offers video chat software that makes connecting remotely with customers as easy as sending a text. Send your customers a link and you can be video chatting in seconds, making it super simple to show details, answer questions, and share your screen.

- Create tailored promotions: Say you own a coffee shop. You run a loyalty program and you’ve captured your best customers’ email addresses and phone numbers. Wouldn’t it be great if you could quickly send those customers targeted promotions? Maybe offer them a deal on a new single-origin coffee you’ve just started stocking? You can do that as well.

- Provide to-the-minute advice and updates: There are a lot of variables in the world right now. Customers might want to know how busy you are at a certain time, or what measures you’ve put in place during the pandemic. Or they might have product-specific questions. A customer messaging platform makes it easier for you to respond in real-time.

Oh and an easy way to get started is to just sign up for a free Podium account.

Issue: Scheduling Meetings

No one likes scheduling meetings at the best of times. Throw coronavirus into the mix and it becomes even more of a challenge. Should it be in-person or remote? Which platform should we use? What date and time work best?

Meeting schedulers are designed to handle the legwork for you. One of the best is Arrangr, which reserves tentative meeting times, automatically frees up untaken slots, and can even suggest the ideal location for all parties.

Another great option is Calendly. Integrating directly with your Google or Office 365 calendar, it gives you a personalized URL that allows customers to see your availability and schedule their preferred meeting time. Best of all, there’s a basic free plan available.

Issue: Email Automation

You can’t grow a local business at a time like this without doing some marketing.

Unfortunately, you likely don’t have time to build and execute complex campaigns.

That’s why you need email automation software! One of the most popular tools, Mailchimp, helps you send effective email marketing communications at scale. In fact, Mailchimp claims to boost open rates by 93% and click rates by 174% compared to the average bulk email.

Customer Relationship Management

Your customer relationships have never been more valuable than they are right now, so you need to manage them effectively. To do that, you need to invest in a customer relationship management (CRM) tool.

There are a bunch of CRMs aimed at local businesses, but HubSpot Sales Hub is one of the most popular. It’s loaded with sales engagement tools, pricing functionality to help you deliver complex quotes, and analytics software to measure what’s working (and what isn’t).

2. Improve Your Digital Marketing Strategy

In more “normal” times, you might not put a lot of thought into your marketing. Maybe you just write the occasional social post or send a couple of email promotions a month.

During times of uncertainty, that just won’t cut it. People have a lot on their minds right now, so that one baseball gif you tweeted isn’t going to have much impact.

You need a proper digital marketing strategy.

Let me give you an example: you sell business supplies to other local businesses.

Because you’re small and local, your big differentiator is your flexibility and bespoke approach. You can source whatever product your customer needs, your delivery times are rapid, and you’re easy to reach. That’s the sort of stuff you talk about in your marketing emails.

Well, wouldn’t it be good if you made that the foundation for a whole campaign?

Maybe you create a bunch of case studies and testimonials that show your unique selling point, (USPs), in action. You build a mailing list of local firms you’d love to do business with, and drip-feed your content to those prospects. Because you’ve built a whole strategy, you know the best times to reach those prospects, the platforms they use, and the sort of messaging that resonates with them.

That approach helps you strike up a conversation, which ultimately means you may close more deals.

3. Make Your Google My Business Profile Shine

Want people to see your name when they search on Google for businesses like yours? If you’re reading this article, I’m guessing you do, and that means you need a (good) Google My Business profile.

Setting up a free profile makes it more likely that your business shows up in relevant searches, along with useful information like:

- The type of service you offer

- Your opening times

- Your address

Once you’ve set it up, optimize your Google My Business profile by:

- Ensuring your information is accurate and comprehensive

- Sharing business updates, like new opening hours or product launches

- Asking customers for Google reviews (and responding to them)

On that last point, I know it can be hard persuading customers to review your business. They’re busy. They don’t want to spend their valuable time seeking out your Google My Business profile or Facebook Business Page.

Podium makes it a lot easier, helping you provide social proof that demonstrates your brand can be trusted. Text customers asking them for a review and they’ll be linked straight to your Facebook, Google, and Tripadvisor pages, so there’s hardly any clicks (and hardly any work) for them. That’s why Podium has powered more than 15 million business reviews for its users.

4. Create and Execute a Local Paid Marketing Strategy

Sometimes it takes money to make money. If you’re serious about growing your local business right now, you’ll want to consider investing in some sort of paid activity.

Google Ads can be super effective for smaller firms, especially web-based businesses targeting online traffic and/or conversions. Local keyword phrases like “lawyers near me,” or “realtor in Denver,” are typically a lot less competitive than broader, non-geographic terms like “realtor.” That means you could get a lot of visibility and clicks with a relatively small outlay.

In addition to Google Ads, consider advertising on social platforms like Facebook and LinkedIn. Social ads are less intention-based than paid search because your audience isn’t actively looking for the thing you’re advertising.

However, ads on social media often cost less than Google Ads. For instance, if you’re a law firm, you’re paying on average $10.96 per click on Google Ads, but on Facebook, that figure drops to just $1.32.

5. Use Analytics to Track and Improve Site Performance

When times are hard, you need to squeeze every last dollar from your potential customers. Analytics software (like Google Analytics) can help you do that by allowing you to identify trends, plan new strategies, and measure the results of your current efforts.

Let’s say you’re a mechanic. You’ve just added a page to your site to promote a special offer on new tires. A month later, you click into Google Analytics and see that a bunch of people have landed on that page, but your conversion rate is low.

You compare it to other, similar pages on your site. They’re performing much better. Now you know there’s a problem, such as:

- Your current offer is priced too high

- Your new page isn’t engaging or persuasive enough

- You don’t make it easy enough for customers to convert, so they leave

- You don’t provide enough detail about the offer

By comparing against better-performing pages, you can tweak your approach and improve results.

6. Conduct Local Community Promotions

Now isn’t a good time to invite hundreds of people to a big party. But there are definitely opportunities for community engagement. You just need to get a little creative.

Say you’ve opened a new store in a location you haven’t served before. Maybe you target properties within a certain zip code, or on certain streets, with a special offer that encourages customers to visit your store.

Perhaps in the age of social distancing, you’ve introduced a new takeout service. Why not give customers in your area 10% off their first promotion, or combine it with a loyalty scheme? Tailor your offer to what your customers want right now, then promote it on Facebook, in the local press, via email marketing, or through direct mail.

7. Optimize Your Social Media Accounts

There are dozens of social platforms out there, but when it comes to growing a local business, you want to focus on those that give you the best reach, like:

- YouTube

- Tumblr

Finding the right platform will depend on the type of business you run. On a basic level, if you’re B2B, LinkedIn’s likely your best channel. Otherwise, almost everyone is on Facebook, but if your product is highly visual you might see more success on Instagram, Pinterest, or YouTube.

Whichever platform(s) you choose, you need to identify some tactics that ultimately help you sell more, like:

- Showcasing and/or auctioning your products on Facebook Live

- Starting conversations with new prospects in LinkedIn Groups

- Setting up Instagram Shopping so people can browse your products in photos and videos while in-app

Conclusion

Growing a local business is never easy, and it’s certainly a whole lot harder right now.

However, if you’ve set up your own business, you’re likely comfortable with hustling for results. You’re naturally entrepreneurial and you’re driven to make this work.

Combine that attitude with the right growth strategies, and execute them effectively, and there’s no reason why you can’t come out of the pandemic in a stronger position.

What plans have you put in place to grow your business? How’s it going for you so far?

The post How to Grow Your Local Business During Uncertain Times appeared first on Neil Patel.