The Ringer’s Bill Simmons is joined by Ryen Russillo to discuss top NBA draft prospect Cade Cunningham after Oklahoma State’s loss to Oregon State in the NCAA tournament (2:30), LeBron James’s ankle sprain and his unprecedented durability over the years (26:00), updated NBA MVP odds (47:45), the upcoming NBA trade deadline (1:19:00), and more.

People always ask me the same question about AdWords:

“What’s a ‘good’ cost per click?”

My response back to them is always the same:

“Why do you care?”

See, most people have AdWords wrong. They obsess over the costs.

They know that more and more competitors are advertising on the platform, which drives up prices.

So they’re zeroed-in on how much they’re going to have to spend.

That’s the wrong approach.

Instead, they should be concerned with what they’re going to get back in return.

I know this sounds counterintuitive. However, I almost never worry about the Cost Per Click for keywords.

In fact, I almost always ignore them.

I’m going to show you why CPC’s don’t matter in many cases. I’ll show you how worrying about keyword costs can mislead you time and time again.

Then, I’ll show what you should be analyzing to make sure you’re not leaving tons of money on the table.

Why Cost Per Click Doesn’t Matter (and What to Analyze Instead)

Each year, companies analyze the most expensive keywords in the country.

These are typically competitive phrases in law or insurance and can cost as much $50 for just a single click.

The insane thing is almost none of those clicks will turn into customers immediately.

Instead, they’ll usually opt-into a form, first.

That means you might have to front the bill for 50 or 100 clicks before someone ever converts.

We’re talking thousands of dollars for a single customer.

It makes sense on the surface; CPC ultimately determines how much you need to spend.

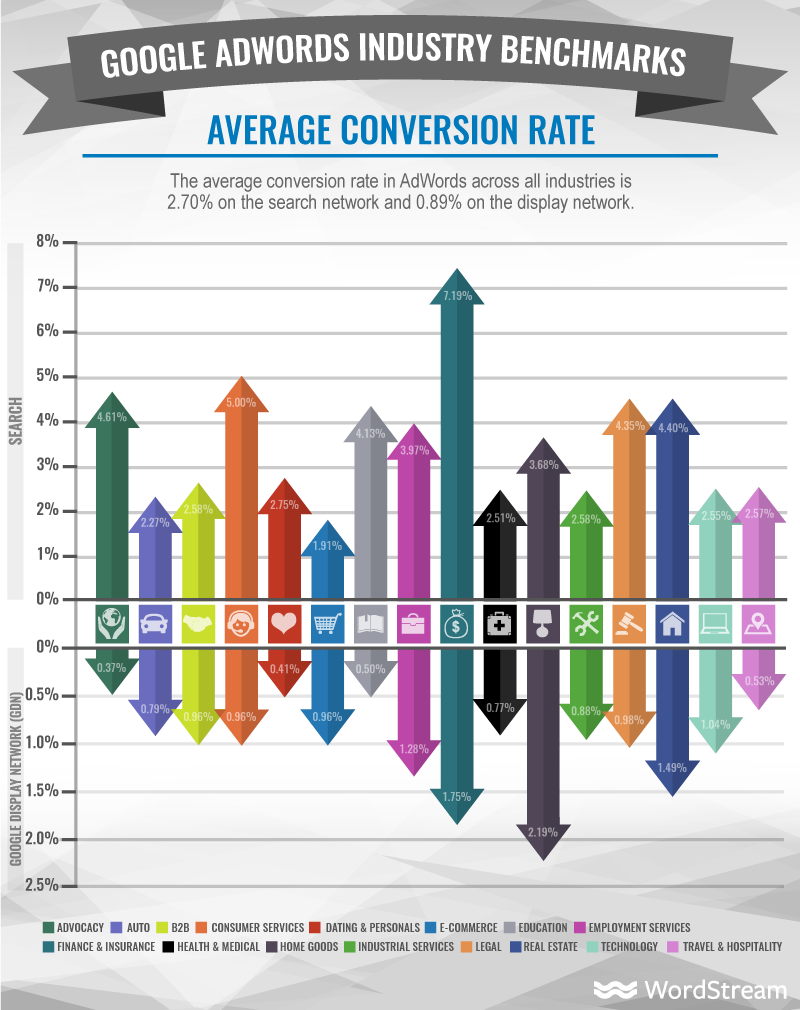

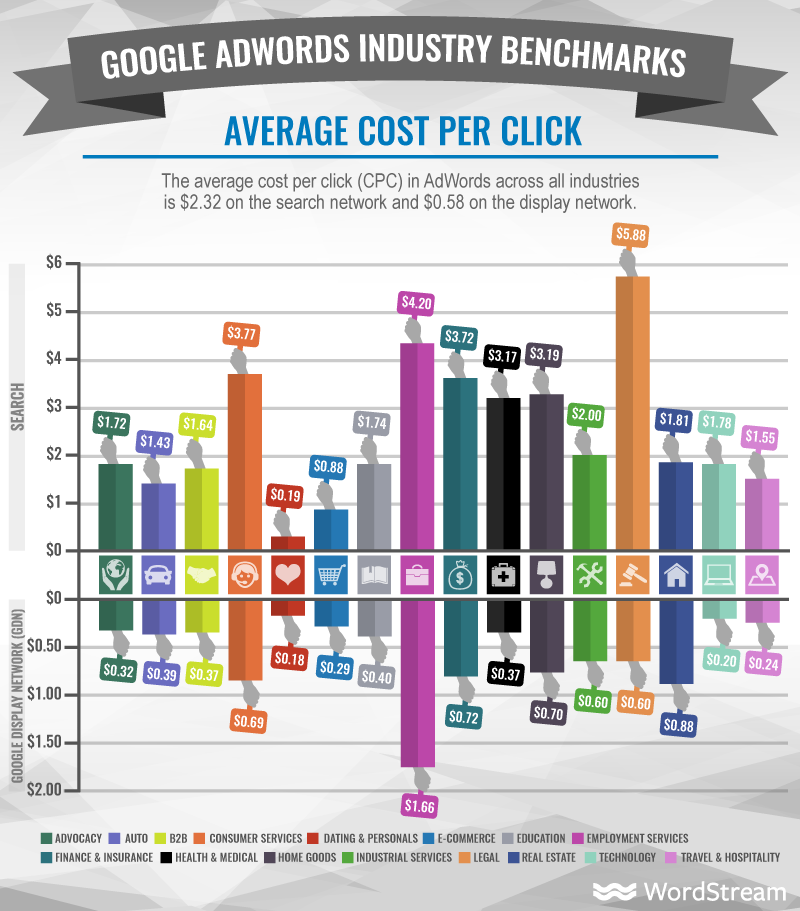

WordStream, for example, always releases an annual update on Cost Per Click benchmarks across industries.

The businesses I own are all software-related. But we work with clients across different industries. So it’s always interesting to look at these cost breakdowns.

Average ecommerce CPC’s might only be around a dollar, while law might run up to around six dollars (these are higher than most Bing Shopping campaigns, which should be considered for e-commerce businesses as well).

To be honest, though, I don’t obsess over costs, alone.

The first reason comes down to what the study says at the top: Averages.

Average CPCs don’t really mean all that much.

Popular, generic terms aren’t usually all that expensive.

Only a tiny percentage of the people who ever click on those will convert. Whereas, a more commercial long-tail keyword will be incredibly expensive.

Just compare the difference in costs between “tax” and “file back taxes”:

See? It’s not even close.

That makes it hard to use a standard, “industry average benchmark” for any in-depth analysis.

There’s another reason why I don’t like to just look at costs — because you’re often forgetting the other side of the equation.

Conversions ultimately have a much bigger impact than costs.

If you remember, the industry average CPC for ecommerce was only around a dollar. In fact, it was one of cheapest CPC’s on the entire list.

But if you now look at the average conversion rates, you’ll see why.

Their conversion rates are also among the lowest.

What does it matter if CPCs are ‘inexpensive’ if the conversions are equally low?

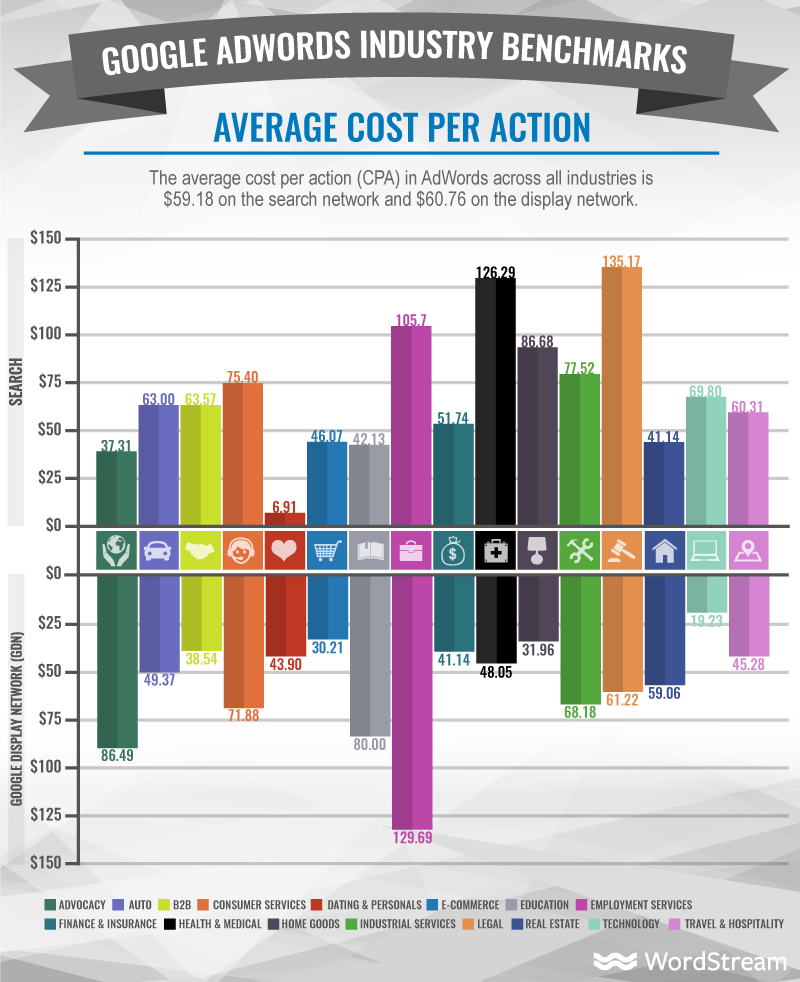

That’s why you often want to look at the Cost Per Action (or Acquisition) when putting together advertising estimates.

This is the effective price you pay to generate a lead, for instance.

It’s a performance ratio. It starts to take into account things like costs vs. conversions to help you determine a much better figure: ROI.

The industry average Cost Per Action for ecommerce lines up with education on the search network.

So from an ROI standpoint, there’s almost no difference.

This is why CPC is almost meaningless.

Yes, it’s important to a point because it drives things like your Cost Per Action.

However, what’s ultimately more important is the revenue you can generate.

It doesn’t matter whether we’re talking about Google AdWords, Facebook, or even Twitter ads. The message is still the same.

Digital Marketer once ran a Twitter Lead Gen campaign, testing the effective Cost Per Action (or Lead).

One campaign was able to see a $7.81 cost per lead.

They then ran the same study with the same ad and audience targeting. But this time, they optimized the campaigns to increase conversions.

It generated a $1.38 Cost Per Lead, which came out to a five time lead increase on the same ad budget.

They were able to 5X conversions simply by focusing on conversions and Cost Per Lead. They didn’t even have to touch the CPC.

You can see this time and time again.

Jacob Baadsgaard of Disruptive Advertising confirms that the best PPC metrics are revenue-focused. They track lead data all the way through to closed sales.

Then, and only then, will they make a decision about which ad campaign is best.

It’s not that costs don’t matter. They do, of course. But they only matter in context to how much revenue you can generate from it.

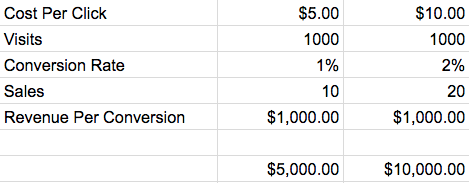

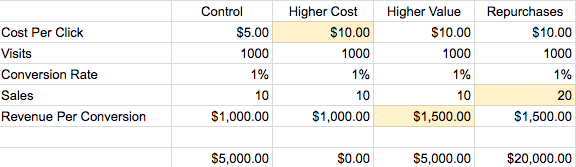

Here’s a very simple example to illustrate.

Let’s say you run two ad campaigns side-by-side.

The Cost Per Click for the second campaign is twice as much as the first. But because the conversion rate is 2% instead of 1%, you’re able to double revenue.

Would you pay twice as high a Cost Per Click to generate twice as much revenue? Of course you would!

This is after reducing revenue by your ad costs. So it’s already accounting for the higher ad budget.

At the end of the day, you’re still doubling revenue. It’s totally worth it!

Obsessing over CPC doesn’t just leave money on the table. It can also make you waste a ton of what you’re already spending.

Here are a few examples.

Obsessing Over CPCs Can Make You Pull The Plug Too Early (or Too Late)

There are many things that separate big companies from small ones.

But here’s one of the biggest: Big companies spend more on advertising than small ones do.

Duh, right? Of course big companies have bigger budgets.

We’re not just talking about dollars spent, but percentage of revenue

Because you still might leave a lot of money on the table.

If your CPCs start edging up, the campaigns will back off or stop.

Then your lead flow will stop, too.

That’s why I like using CPAs as targets if possible, instead of CPCs.

Watch CPA Instead of CPC

Cost Per Action is a better performance than Cost Per Click.

It’s not as good as Revenue, though–and there’s the problem.

CPAs can still be subjective.

Is a ‘high’ CPA bad? Maybe, maybe not.

If your CPA is over $100 in ecommerce, that might be bad.

Almost every single campaign CPA will be over $100 in law, for example. So it’s not bad at all.

Its still a much better metric to control ad campaign performance, though.

You can still figure out an upper range that starts to make ad campaigns unprofitable. You’ll base this on your average sale per customer. (More on this later.)

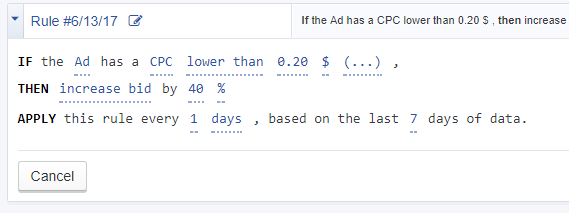

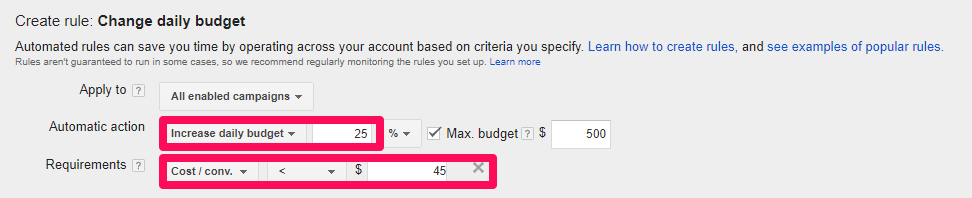

For starters, you can set automated rules to increase or decrease the total budget based on your CPA.

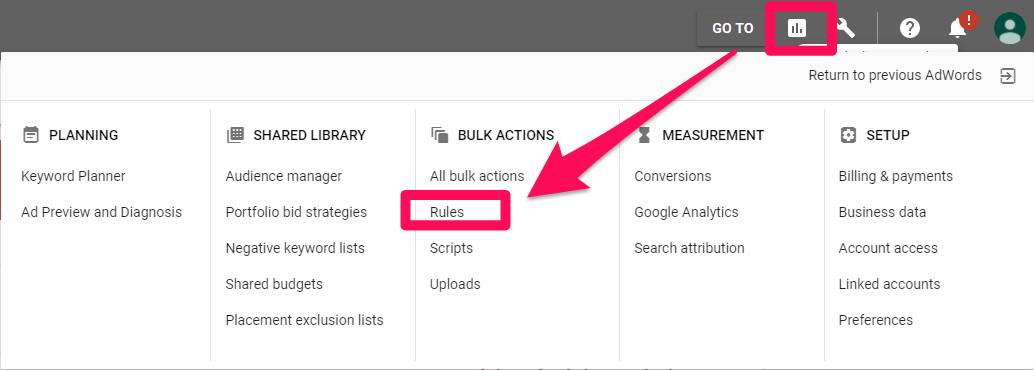

Inside AdWords, you can go to “Bulk Actions” and create new “Rules” for these ranges:

Under “Change budgets,” you can set an automated rule to either increase or decrease budgets based on cost per conversion numbers.

This tells AdWords to automatically increase your daily budget 25 percent if the CPA is within a certain dollar range.

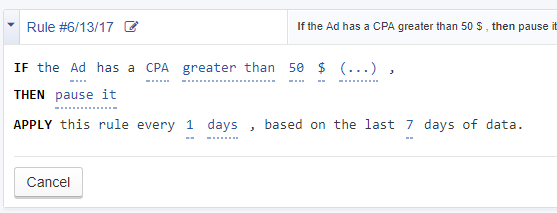

You can do this same exact strategy inside Facebook, too.

You’ll set a rule to increase, decrease, or stop a campaign if the CPA hits a certain threshold.

Managing ad campaigns by CPA can net you more customers and revenue.

There’s still one big section we’re forgetting.

Keyword pricing or competitive pressure aren’t the only factors to worry about.

Many times, your customer base could be going through their own issues, and that’s not something you can change.

That’s why focusing on revenue is always the best approach.

Increase the Revenue-Side of the Equation to Overcome Outside Factors

Spearmint Love is one my favorite success stories.

The craziest part is that it almost didn’t happen.

They were growing like a weed, until…everything just stopped.

Results were declining across the board and they couldn’t figure out why.

Until, one day while on a walk, it dawned on one of the co-founders.

Parents will buy baby clothes until that baby grows up. In other words, their customers were kind of ‘moving on’ from the company.

The ad campaign decline had nothing to do with costs or his ad campaigns per se.

It had everything to do with their customer base.

How on Earth do you solve this problem?

By focusing on increasing revenue — not touching costs.

If the CPA is ‘too high’ to make your numbers work, start by increasing average order values.

Upsells are easy, for example, when you bundle similar products.

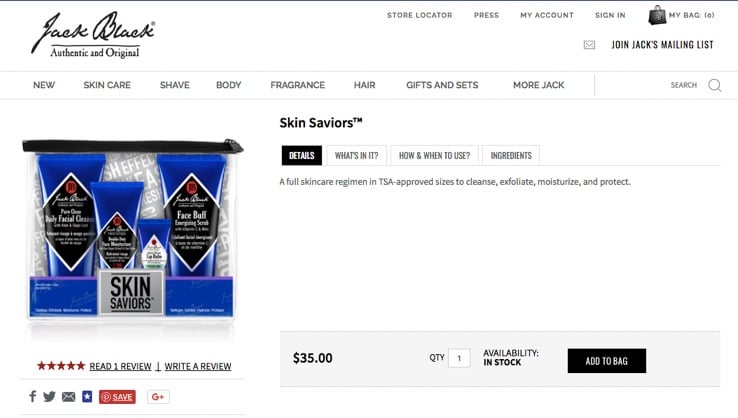

Think about the last time you flew somewhere. Chances are, you bought a travel-sized product at a store before going through TSA.

But that product probably only cost a few bucks, right?

Check out what Jack Black does here, bundling several travel products together.

You arguably need all of these products if you’re flying somewhere.

Instead of only charging you a few bucks each, they’re charging you $35 for the whole pack!

Simply bundling similar products allows them to charge 10x more. Which means you can afford a much higher initial advertising cost now, too.

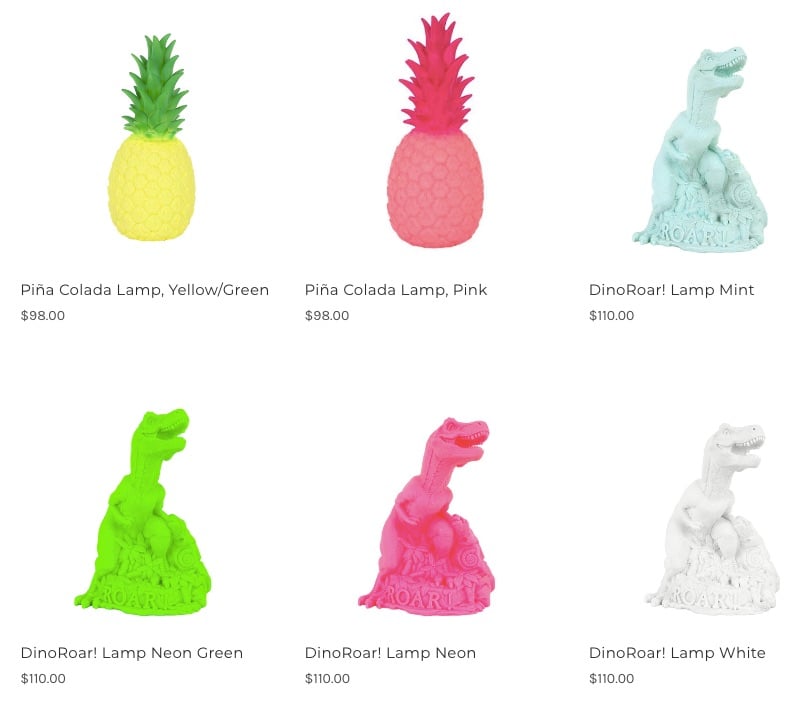

You can also cross-sell products to try and raise the average order value.

For example, right underneath this travel bundle, Jack Black offers a few related products to take with you:

One interesting thing to note is the price of all three items. They’re all slightly less than the initial $35 purchase.

Why?

They’re using price anchoring effect to make these additional products seem less expensive.

The Economist included a middle pricing tier for a print-only subscription. It was the same exact price as the ‘big’ plan for both the print and web editions.

Most people chose the combined third option because it seemed like the best deal.

There’s only one reason to spend money on ads at the end of the day: to make money.

Chasing the keywords with the lowest CPC is a losing proposition.

If anything, you should be spending more money. You should actually search out the highest CPC’s in your industry.

Why?

Often, they offer the most potential. You want to maximize the most sales per dollar spent.

So you know all those “industry benchmark CPC” numbers? Don’t worry about them.

Instead, start focusing on CPA. That’s the number it costs for you to acquire each new customer.

It’s not perfect by any stretch. But it’s a better number to optimize around than CPC.

From there, try to dig into revenue numbers.

Can you bundle a few products to raise the average order value? Can you cross-sell recommended products and use price anchoring to lower their perceived cost?

Then, figure out how you can keep customers around longer.

That might mean introducing new, related product lines. Or it might mean introducing ‘consumable’ products that people need to repurchase again and again and again.

The world of business loan companies is full of predatory lenders. If you are desperate for business funding, it can be easy to take the bait and fall into their trap. You need to know how to tell predators from legit creditors, especially if you need to veer away from traditional financing. You may think you know what to look for, but there are some predatory secrets that a lot of business owners are not privy to.

How to Avoid Predatory Lenders When Looking for Business Loan Companies

It can be helpful to work with a business credit expert. Not only can they steer you toward responsible lenders, but they can also help you choose the type of funding that will work best for your needs. A good one will help you build business credit at the same time.

Still, you need to know the signs of a predatory lender for yourself. If you do not, you will not even be able to tell if you are working with a good business credit expert, or not.

Signs of a Predatory Lender

Can you tell the difference between legit creditors and predatory lenders?

According to Investopedia:

“Predatory lending benefits the lender and ignores or hinders the borrower’s ability to repay a debt. These lending tactics often try to take advantage of a borrower’s lack of understanding concerning loans, terms, or financial literacy.”

Predatory lending when it comes to business loans is becoming an increasingly prevalent problem

How do you keep yourself from wading off into shark infested waters?

Find out why so many companies use our proven methods to get business loans.

Avoid Business Loan Companies That Focus on Monthly Payment Rather Than Actual Loan Amount

They may insist on one large payment at the end of the term with only interest payments being made each month until that point. This is known as a balloon payment. In business lending, this can be useful if you are waiting on large sums of money at the end of the contract to repay the loan, so it isn’t necessarily a deal breaker. However, you do need to know that your payments are only paying interest and not reducing principal.

Recognize if this is really the type of loan that you need. Lenders should always be willing to disclose your total loan amount and terms. You should not have to beg for this or search for it. Lenders that focus only on the payment may be sketchy.

There are many things they can do to make a monthly payment lower, like extending the loan period, adding a large payment at the end (a balloon payment), or making adjustments to loan terms. All of these things can make your monthly payments look low, while in reality you are getting stuck with a bad loan.

Note that while a balloon payment should be an automatic deal breaker, insistence on a balloon payment is an extra red flag.

Good Business Loan Companies Will Not Add Unnecessary Extras Without Your Knowledge

Another common practice of predatory lenders is adding extras onto the loan. These are usually things the borrower does not need. Furthermore, the borrower will not even know they are there. The most common “extra” seems to be insurance products that do not offer any benefit.

Business Loan Companies and Confessions of Judgement

New York plays a unique role in the world of predatory lending. Understanding this can help you understand if you are about to become the prey. It all comes down to a confession of judgement. If a borrower signs a confession of judgement, they are basically agreeing to lose in a court battle if there is a dispute about repayment. Many cash-advance companies, which make up a large faction of predatory lenders, have their borrowers sign one of these.

New York state law is friendly to this type of contract. Regardless of where a loan takes place, it may include a “New York confession of judgement.”

This could also mean you are agreeing that any lawsuits will be handled in New York state. That could greatly increase expenses if you do not live near there. If you see one of these in your loan documents, do not sign it. It is of no benefit to you. It only benefits the lender.

Find out why so many companies use our proven methods to get business loans.

Don’t Accept Punishment for Early Payment

Prepayment penalties should definitely be a red flag. Early payment is good, period. Even though the lender may lose some interest, they should not be too opposed to early repayment. By itself, it should not be the reason you do not take a loan. But it should make you continue with caution and look for other red flags.

Good Business Loan Companies Do Not Have to Seek the Weak

Business loan companies that specifically seek out underserved populations, such as minorities and immigrants, and those with bad credit should be considered carefully. This may include contacting business owners that fit into these types of categories directly, or targeting them with marketing campaigns designed for them specifically. If the focus is meant to make them think they are getting a great deal because they are in an underserved market, it could be sketchy. While there are programs designed to help serve underserved populations, if something seems too good to be true, it likely is.

A Good Business Loan Company Will Not Start With a Bad Deal

Some predatory lenders will try to earn trust by admitting they are offering a bad deal, then promising to fix it in the future. They claim they will allow for a refinance that will be a better option. Don’t fall for it. A bad deal is a bad deal. Just walk away.

Loan Flipping is a Classic Move for Predatory Business Loan Companies

This is not the same as house flipping. Flipping a house can be very profitable. Loan flipping is actually a classic predatory lending tactic. When a predatory lender sees that you are struggling, they will offer a refinance. However, you end up paying points and fees again. As a result, before it is over, you end up owing more than your original loan. Sometimes you may end up owing even more than your collateral is worth. It is a vicious cycle, and it can bury you quickly.

Find out why so many companies use our proven methods to get business loans.

The Responsible Business Lending Coalition

This is a network of nonprofit and for-profit lenders, investors, and small business advocates. They have a common commitment to innovation in the small business lending industry. They also have serious concerns about the increase of irresponsible small business lending.

What is the Easiest Way to Avoid Predatory Business Loan Companies?

Look for help when you can find it. Working with a company that specializes in helping small businesses find the fundsthey need can help you avoid predatory lenders. For example, Credit Suite works only with reputable lenders. With our Credit Line Hybrid and many other products, we connect businesses with lenders that we know to be safe to work with. Not only that, but we help you assess your fundablity at the same time, and work with you to figure out how to best fill in your business’s fundability weaknesses. If business credit is an issue, we can help you build that too! The time to take action is now, before you look for business loan companies. Don’t take the chance of falling prey.

The electric-vehicle maker will be added to the broad stock-market gauge before the start of trading Dec. 21, meaning most index-tracking funds that follow the S&P 500 will engage in a flurry of trading the Friday before.

Video Clip Blogging And Visitor Interaction Or you desire to introduce that your Dalmatian has currently eleven adorable young puppies? If you desire, after that video clip blog writing is what you require. What is video clip blog writing and also why is it one of the most popular tasks in the Internet? Blog site … Continue reading Video Clip Blogging And Visitor Interaction

If you are wondering how to get a small business loan, you may be thinking in terms of credit score. Of course, both your personal and business credit score make a huge difference in approval chances. That isn’t all there is to it however. Here is everything you need to know about how to get a small business loan.

How to Get a Small Business Loans: What You May Not Know

Did you know that how your business is set up, how you present your business to the lender, and even which type of lender and loan you are applying for can all affect your approval chances? These are the things no one really tells you. They do matter however, and lenders definitely take these things seriously.

How to Get a Small Business Loan: Fundable Foundation

First, it is almost guaranteed you are going to have to have a personal guarantee for a business loan. There are exceptions to this, but in general you can expect that your personal credit will come into play. However, this doesn’t mean that bad personal credit will keep you from funding your business. The first key to how to get a small business loan is to work on overall fundability. If your business as a whole is fundable, your personal credit will not have as much of an impact. The first step in that process, is to set up your business properly.

Find out why so many companies use our proven methods to get business loans.

How to Set Up Your Business to be Fundable

Here is what you need to do to set up your business to be as fundable as possible. The goal is to ensure your business is separated from yourself as the owner for credit purposes. This step is also important to solidifying your business as one that is legitimate and viable in the eyes of lenders.

Separate Contact Information

You can get a business phone number and fax number pretty easily that will work over the internet instead of phone lines. In addition, the phone number will forward to any phone you want it to so you can simply use your personal cell phone or landline. No need for a new phone! Whenever someone calls your business number it will ring straight to you.

Faxes can be sent to an online fax service, if anyone ever happens to actually fax you. This part may seem outdated, but it does help your business appear legitimate to lenders.

You can use a virtual office for a business address. What is that? It’s not what you may think. A virtual office is a business that offers a physical address for a fee, and sometimes they even offer mail service and live receptionist services. In addition, there are some that offer meeting spaces for those times you may need to meet a client or customer in person.

Get an EIN

The next thing you need to do is get an EIN for your business. This is an identifying number for your business that works in a way similar to how your SSN works for you personally. Some business owners used their SSN for their business. This is what a lot of sole proprietorships and partnerships do. However, it really doesn’t look professional to lenders, and it can cause your personal and business credit to get all mixed up. When you are looking to increase fundability, you need to apply for and use an EIN. You can get one for free from the IRS.

You Have to Incorporate

Incorporating your business as an LLC, S-corp, or corporation is vital to fundability. It lends to the appearance that your business is legitimate. It also offers some protection from liability.

When you incorporate, you become a new entity. You basically have to start over. You’ll also lose any positive payment history you may have accumulated as well.

This is why you have to incorporate as soon as possible. Not only is it necessary for fundability and for building business credit, but so is time in business. The longer you have been in business the more fundable you appear to be. Time in business starts on the date of incorporation, regardless of when you actually began doing business.

Separate, Dedicated Business Bank Account

You have to open a separate, dedicated business bank account. There are a few reasons for this. The main one for this purpose is, it further separates your business from you as the owner.

Get All Necessary Licenses

For a business to be legitimate it has to have all of the necessary licenses it needs to run. If it doesn’t, red flags are going to fly up all over the place. Do the research you need to do to ensure you have all of the licenses necessary to legitimately run your business on all levels.

Professional Business Website

Spend the time and money necessary to ensure your website is professionally designed and works well. Don’t use a free hosting service, and make sure your business has a dedicated business email address. Furthermore, it needs to have the same URL as your website. Don’t use a free service such as Yahoo or Gmail.

How to Get a Small Business Loan: Business Plan

The next step in how to get a small business loan is the business plan. You have to sell your business to lenders as one that will be a good investment. Honestly, it’s best to hire professional writers and researchers to help you put this together, but if you cannot, there are plenty of free resources online that can help. This includes templates. Generally, a well put together business plan should include the following.

An Executive Summary

Description

Strategies

Market Analysis

Analysis of audience

Competitive Analysis

Plan for Design and Development

Plan for Operation and Management

Financials

Financial Information

Find out why so many companies use our proven methods to get business loans.

How to Get a Small Business Loan: Research Lenders

The next step in how to get a small business loan is to choose the right type of lender for your needs. This will take research. There are generally three types of lenders. There are traditional lenders, SBA lenders, and private lenders.

Traditional Lenders

These are your standard financial institutions. They include large banks, smaller community banks, and credit unions.

SBA Lenders

For the most part, these are traditional lenders and sometimes non profits that lend funds with a federal guarantee through the Small Business Administration.

Private Lenders

These are lenders other than traditional banks and credit unions that offer terms loans. Usually they operate online. Occasionally they will have a brick and mortar location as well. The difference between these and traditional lenders is that the loans have looser approval requirements and a much faster application process. Most often you can simply apply online, get approval in as little as 24 hours, and the funds are in your account within 24 to 48 hours after approval. They are an option if your personal credit is okay and you need funding fast.

Many of these have popped up in the past decade as more and more people are branching out to start their own business. The need for a financing option from something other than traditional banks has encouraged this growth.

There are some benefits to using private business loans over traditional loans. The first is that they often have more flexible credit score minimums. Even though they still rely on your personal credit, they will often accept a score much lower than what traditional lenders require. Another benefit is that they will often report to the business credit reporting agencies, which helps build or improve business credit.

The tradeoff is that private business loans often have higher interest rates and less favorable terms. In the end though, the ability to get funding and the potential increase in business credit score can make it well worth it.

Find out why so many companies use our proven methods to get business loans.

How to Get a Small Business Loan: Research Types of Loans

Not only can you choose your lender type, but you can also choose your loan type. This is the next part of the process in how to get a small business loan. Choosing the right type of loan both for what you need, and for what you qualify to get, can make all the difference.

Traditional Term Loans

These are the loans that you go to the bank to get. As a business, your business credit score can help you get some types of funding even if your personal score isn’t awesome. That isn’t necessarily the case with this type of funding however.

With a traditional lender term loan, you are almost always going to have to give a personal guarantee. This means they will check your personal credit. If your personal credit score isn’t in order, you will likely not get approval.

What kind of personal credit score do you need to have in order to qualify for a traditional term loan? If you have at least a 750 you are in pretty good shape. Sometimes you can get approval with a score of 700+, but the terms will not be as favorable.

If you have really great business credit, your lender might be more inclined to be a little more flexible. However, your personal credit score will still weigh heavily on the terms and interest rate.

Of all of the different loan types, this is the hardest to get. It is usually worth the trouble though if possible, because these generally have the best rates and terms.

SBA Loans

These are traditional bank loans, but they have a guarantee from the federal government. The Small Business Administration, or SBA, works with lenders to offer small businesses funding solutions that they may not be able to get based on their own credit history. Because of the government guarantee, lenders are able to relax a little on the personal credit score requirements.

In fact, it is possible to get an SBA microloan with a personal credit score between 620 and 640. These are very small loans, up to $50,000. They may require personal collateral as well.

The trade-off with SBA loans is that the application progress is lengthy. There is a ton of red tape connected with these types of loans.

Business Line of Credit

This is basically the traditional lender’s version of a business credit card. It’s revolving credit, meaning you only pay back what you use, just like a credit card. However, rates are typically much better than a credit card. The application and approval process is more similar to that of a traditional term loan.

If you need revolving credit and can qualify for a term loan, this is the best of the available business funding types for you. It is great for bridging cash gaps and covering short term expenses without the high credit card interest rates.

There are no cash back rewards or loyalty points, though. This makes some business owners prefer business credit cards in some cases, despite higher interest rates.

Invoice Factoring

If you are an established business with accounts receivable, invoice factoring is one of the available business funding types that you have access to. This is where the lender buys your outstanding invoices at a premium, and then collects the full amount themselves. You get cash right away, without waiting for your customers to pay the invoices.

Invoice factoring is a good option if you need cash fast, or you do not qualify for other funding types. The interest rate varies based on the age of the receivables.

How to Get a Small Business Loan: Put It All Together

There is a lot to do when it comes to how to get a small business loan. The thing to remember is, while it all has to be done, it doesn’t all have to be done independently. You can work on setting up your business while simultaneously researching loans and writing your business plan.

If you are just getting started, you may not be able to complete the setup process until you get a loan. That’s okay. Do what you can when you can, and keep the big picture in mind. If you do these things and make your payments consistently on-time, you will find it easier and easier to get funding for your business.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

{kind=link}